MARKET INSIGHTS

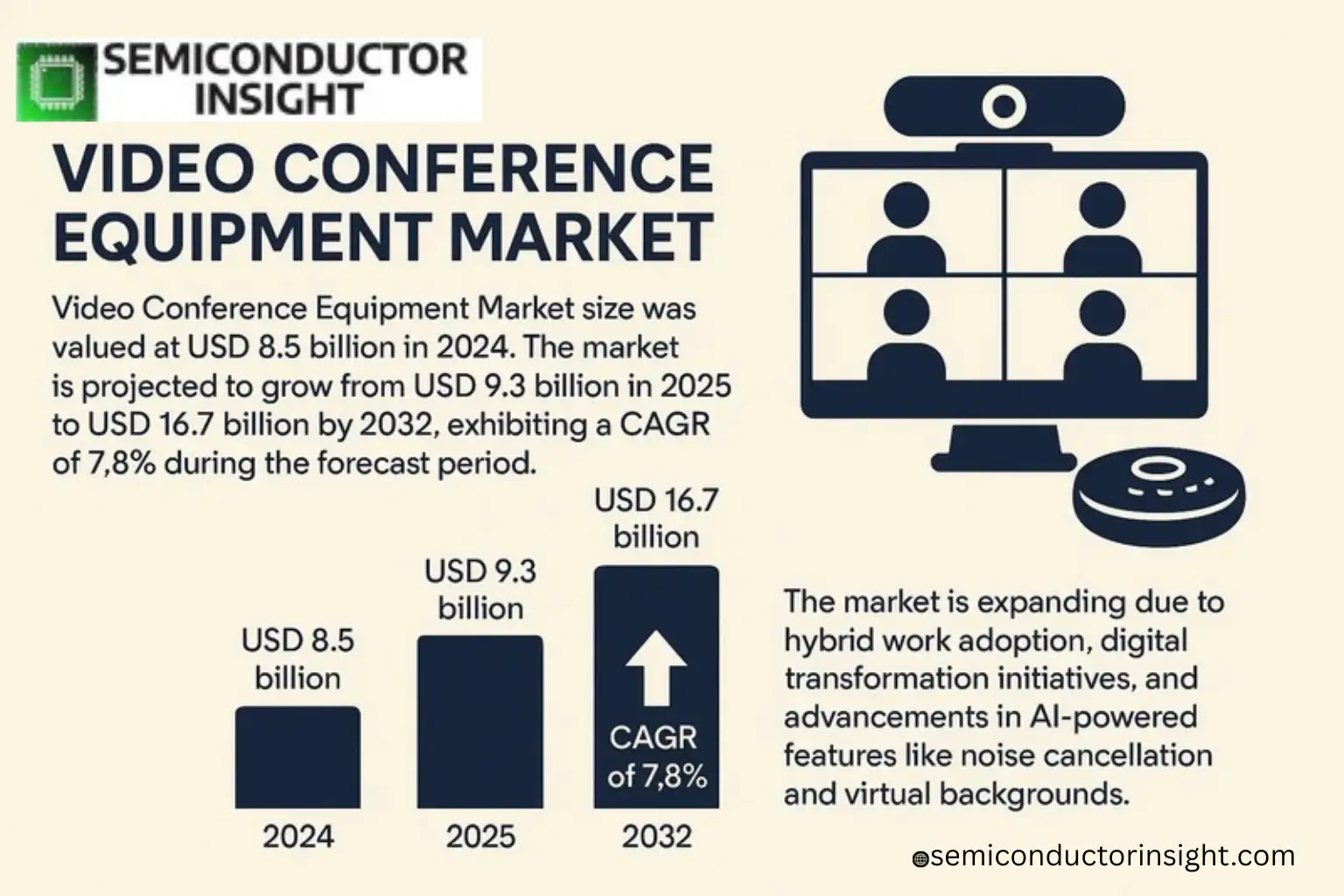

Global Video Conference Equipment Market size was valued at USD 8.5 billion in 2024. The market is projected to grow from USD 9.3 billion in 2025 to USD 16.7 billion by 2032, exhibiting a CAGR of 7.8% during the forecast period.

Video conference equipment refers to hardware and software solutions designed for real-time audio and visual communication, including cameras, microphones, displays, codecs, and collaboration platforms such as Zoom and Microsoft Teams. These systems enable seamless remote interactions across corporate, educational, healthcare, and government sectors.

The market is expanding due to hybrid work adoption, digital transformation initiatives, and advancements in AI-powered features like noise cancellation and virtual backgrounds. Key players such as Cisco Systems (Webex), Poly (formerly Polycom), and Zoom are driving innovation through strategic partnerships for instance, Zoom’s integration with Meta’s Horizon Workrooms for VR-enabled meetings in 2023.

MARKET DRIVERS

Hybrid Work Models Fueling Demand

Global shift toward hybrid work environments has significantly increased the adoption of video conference equipment. Over 65% of companies now maintain partial remote work policies, creating sustained demand for high-quality video collaboration tools. The Video Conference Equipment Market is experiencing rapid growth as organizations invest in seamless communication infrastructure.

Technological Advancements in AV Solutions

Recent innovations in 4K cameras, AI-powered noise cancellation, and beamforming microphones are driving upgrades in the Video Conference Equipment Market. Enterprises are prioritizing systems that offer immersive meeting experiences with minimal latency. Cloud-based solutions now represent over 40% of total market revenue as they eliminate hardware limitations.

Government regulations promoting digital transformation and corporate sustainability goals are accelerating the replacement of legacy systems with energy-efficient video conference equipment.

MARKET CHALLENGES

Integration Complexity Across Platforms

Many organizations face technical hurdles when integrating new video conference equipment with existing collaboration ecosystems. Compatibility issues between different manufacturers’ hardware and software platforms create adoption barriers, particularly in enterprises with multi-vendor environments. Security concerns regarding endpoint vulnerabilities also deter some buyers in the Video Conference Equipment Market.

Other Challenges

High Initial Investment Costs

Premium video conferencing systems require significant capital expenditure, with complete room solutions ranging from USD 15,000-USD 50,000, creating budget constraints for SMBs. Ongoing maintenance and IT support costs add to the total cost of ownership.

MARKET RESTRAINTS

Economic Uncertainty Impacting IT Budgets

Global economic volatility has caused 32% of enterprises to delay or scale back video conference equipment purchases in 2023. The Video Conference Equipment Market faces pressure as companies prioritize essential infrastructure over collaboration technology upgrades. Extended hardware replacement cycles are now averaging 5-7 years compared to the previous 3-5 year standard.

MARKET OPPORTUNITIES

AI-Powered Meeting Analytics

The integration of artificial intelligence into video conference equipment presents significant growth potential. Advanced features like real-time transcription, sentiment analysis, and automated meeting summaries are becoming key differentiators. The Video Conference Equipment Market is expanding as vendors develop specialized solutions for education, healthcare, and legal verticals with customized features.

Video Conference Equipment Market Trends

Hybrid Work Models Drive Market Expansion

Global Video Conference Equipment Market is projected to grow significantly, driven by the sustained adoption of hybrid work environments. Enterprises continue to invest in high-quality cameras, microphones, and AI-powered software solutions to enhance remote collaboration. Cloud-based conferencing platforms now account for over 60% of deployments, offering scalability and ease of integration with existing IT infrastructure.

Other Trends

Vertical-Specific Solution Demand

Healthcare organizations prioritize ultra-low latency systems for telemedicine, while educational institutions focus on interactive features like virtual classrooms. Corporate clients increasingly favor immersive conferencing solutions with AR/VR capabilities, creating new revenue streams for equipment manufacturers.

Technology Innovation as Competitive Differentiator

Manufacturers are integrating advanced noise cancellation, 4K resolution, and AI-driven features like real-time translation to maintain market share. The emergence of 5G networks enables higher-quality transmissions, particularly benefiting emerging markets where mobile-first solutions gain traction. Data security remains a critical consideration, with encryption technologies becoming standard across premium offerings.

Other Trends

Regional Market Developments

Asia-Pacific shows the fastest growth due to digital transformation initiatives, while North America maintains leadership in advanced system adoption. Emerging markets are witnessing increased demand for cost-effective, bandwidth-efficient solutions as small businesses enter the digital workspace ecosystem.

Supply Chain and Competitive Landscape

The market remains concentrated among major players like Cisco, Poly, and Zoom, though regional providers are gaining share through localization strategies. Component shortages continue to impact hardware production, accelerating the shift toward software-defined solutions that leverage existing enterprise devices.

COMPETITIVE LANDSCAPE

Key Industry Players

Video Conference Equipment Market Dominated by Hybrid Solutions and Cloud Platforms

The Video Conference Equipment Market is dominated by established players like Zoom Video Communications and Cisco (WebEx), which control significant market share through integrated hardware-software ecosystems. Poly (formerly Polycom) remains a leader in professional-grade conference room systems, while Microsoft Teams has rapidly gained traction through Office 365 integration. The market structure shows clear segmentation between high-end enterprise solutions (Cisco, Poly) and mass-market cloud platforms (Zoom, GoToMeeting).

Niche players like Sony specialize in premium AV equipment for boardrooms, while regional champions like Huawei and Tencent Meeting dominate Asian markets. Emerging competitors like Owl Labs are disrupting traditional setups with AI-powered 360° cameras. The rise of hybrid work has enabled newer entrants like Whereby and Around to gain traction with browser-based solutions requiring minimal hardware.

List of Key Video Conference Equipment Companies Profiled

- Zoom Video Communications

- Poly (Polycom)

- Cisco Systems (WebEx)

- Microsoft (Teams)

- Huawei

- Sony

- Logitech

- GoToMeeting

- Tencent Meeting

- Alibaba (DingTalk)

- Owl Labs

- Whereby

- Around

- BlueJeans (Verizon)

- Pexip

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Cloud-based solutions dominate as enterprises prioritize flexibility and scalability.

|

| By Application |

|

Corporate Enterprises remain the primary adopters with evolving needs:

|

| By End User |

|

SMEs show accelerated adoption due to:

|

| By Technology |

|

AI-powered Solutions drive innovation:

|

| By Deployment |

|

Integrated Suites gain preference:

|

Regional Analysis: Video Conference Equipment Market

Large corporations account for the majority of video conference equipment purchases, investing heavily in integrated room systems and executive-grade solutions. Financial services and tech firms lead adoption with dedicated video conferencing budgets.

Telemedicine adoption has accelerated demand for HIPAA-compliant video conference systems. Hospitals deploy specialized equipment for remote consultations, combining medical imaging with conferencing capabilities.

Universities and K-12 districts invest in classroom video systems supporting hybrid learning. Smartboards with integrated cameras and microphones are becoming standard in academic institutions.

Federal and state agencies prioritize secure video conferencing solutions for interdepartmental communications. Requirements include end-to-end encryption and compatibility with existing security protocols.

Europe

Europe demonstrates robust growth in video conference equipment adoption, driven by multinational corporations and public sector modernization. GDPR-compliant solutions gain traction, with Germany and UK leading in enterprise deployments. The region sees increasing demand for all-in-one systems that combine hardware and software with data protection features. Hybrid work policies across EU countries sustain steady equipment purchases.

Asia-Pacific

APAC emerges as the fastest-growing market, fueled by digital transformation in India and China. Small and medium enterprises increasingly adopt cost-effective video conference solutions. Government initiatives for smart cities integrate advanced conferencing infrastructure. Japan and South Korea focus on high-end equipment with AI features.

South America

Brazil and Mexico show growing interest in video conference equipment among financial and educational institutions. Price sensitivity drives demand for mid-range solutions, while multinational subsidiaries invest in premium systems. Infrastructure limitations in remote areas present both challenges and opportunities.

Middle East & Africa

GCC countries lead regional adoption through smart government initiatives and corporate expansions. Dubai and Abu Dhabi require advanced video conferencing in business hubs. African growth is concentrated in South Africa and Kenya, focusing on cloud-based solutions for mobile workforce connectivity.

Report Scope

This market research report provides a comprehensive analysis of the Global Video Conference Equipment Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of video conferencing solutions in enabling digital transformation across industries such as corporate enterprises, education, healthcare, and government.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (On-premise, Cloud-based, Hybrid), application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/AR/VR, and evolving industry standards in video conferencing.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, security concerns, and market-entry barriers.

- Stakeholder Insights: Strategic opportunities for hardware manufacturers, software providers, system integrators, and investors in the evolving ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Video Conference Equipment Market?

-> Video Conference Equipment Market size was valued at USD 8.5 billion in 2024. The market is projected to grow from USD 9.3 billion in 2025 to USD 16.7 billion by 2032, exhibiting a CAGR of 7.8% during the forecast period.

Which key companies operate in Video Conference Equipment Market?

-> Key players include Zoom Video Communications, Poly, Cisco, Microsoft Teams, Huawei, Tencent Meeting, and DingTalk, among others.

What are the key growth drivers?

-> Key growth drivers include hybrid work adoption, digital transformation initiatives, 5G proliferation, and increasing demand from education and healthcare sectors.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is expected to witness the fastest growth.

What are the emerging trends?

-> Emerging trends include AI-powered meeting features, immersive AR/VR conferencing, and increased focus on data security.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...