MARKET INSIGHTS

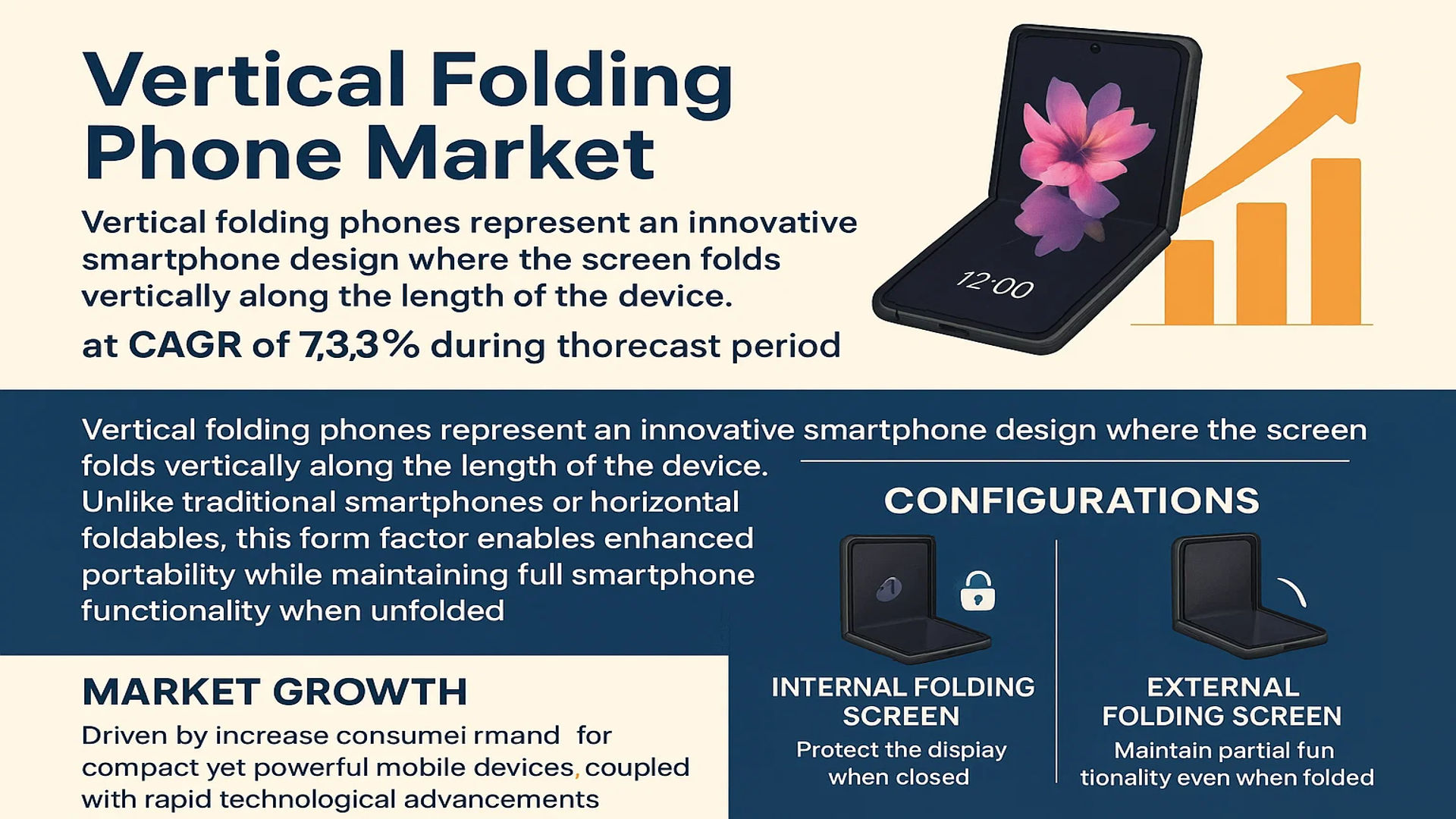

The global Vertical Folding Phone Market was valued at 2752 million in 2024 and is projected to reach US$ 4389 million by 2032, at a CAGR of 7.3% during the forecast period.

Vertical folding phones represent an innovative smartphone design where the screen folds vertically along the length of the device. Unlike traditional smartphones or horizontal foldables, this form factor enables enhanced portability while maintaining full smartphone functionality when unfolded. The market currently offers two main configurations: internal folding screens that protect the display when closed, and external folding screens that maintain partial functionality even when folded.

The market growth is driven by increasing consumer demand for compact yet powerful mobile devices, coupled with rapid technological advancements in flexible display technology. While premium pricing remains a challenge, manufacturers are addressing durability concerns through improved hinge mechanisms and protective materials. Key players like Samsung, Huawei, and Motorola are leading innovation in this segment, with their recent product launches demonstrating significant improvements in screen technology and multi-tasking capabilities. The U.S. and China emerge as dominant markets, together accounting for over 60% of global demand, reflecting strong consumer interest in cutting-edge mobile technology across these regions.

MARKET DYNAMICS

MARKET DRIVERS

Rising Consumer Demand for Compact High-End Smartphones to Propel Market Growth

The global vertical folding phone market is experiencing significant growth, primarily driven by increasing consumer preference for compact yet premium smartphones. Traditional flagship devices have grown larger over the years, creating demand for innovative form factors that offer portability without compromising screen size. Vertical foldables address this need by transforming from a standard smartphone size to a more pocket-friendly folded state while retaining large displays. Market data indicates that nearly 40% of premium smartphone users prioritize portability as a key purchasing factor, making vertical folding designs highly appealing.

Technological Advancements in Flexible Displays Driving Product Innovation

Substantial improvements in flexible display technology have enabled the commercial viability of vertical folding phones. Recent developments in ultra-thin glass (UTG) technology have significantly enhanced display durability, addressing early concerns about screen longevity. These advancements allow for smoother folding mechanisms with increased hinge durability—some manufacturers now claim over 200,000 fold cycles without degradation. Furthermore, the integration of advanced OLED panels with improved power efficiency and brightness levels has elevated the user experience, making vertical foldables competitive against traditional smartphones.

Growing Ecosystem of Apps Optimized for Foldable Devices

The market is witnessing increasing support from app developers creating versions specifically optimized for foldable form factors. When a vertical folding phone transitions between folded and unfolded states, apps can dynamically adjust their layouts to provide seamless continuity. This enhanced software experience removes a significant barrier to adoption that plagued early foldable devices. The growing library of foldable-optimized applications, particularly in productivity and creative software segments, adds substantial value to these devices.

MARKET RESTRAINTS

High Production Costs and Premium Pricing Limiting Mass Adoption

While the vertical folding phone market shows promise, high manufacturing costs remain a significant restraint. The complex hinge mechanisms and specialized flexible displays contribute to production costs substantially higher than conventional smartphones. This cost difference translates to retail prices that often exceed traditional flagship models by 25-40%, placing these devices out of reach for many mainstream consumers. The premium pricing strategy creates a niche market segment that may struggle to achieve the volumes necessary for significant cost reductions through economies of scale.

Other Restraints

Durability Concerns Persist Despite Improvements

Even with technological advancements, consumer skepticism about long-term durability remains. While manufacturers have made significant strides in hinge and display engineering, some consumers still associate foldables with higher maintenance requirements and shorter product lifecycles compared to traditional smartphones.

Thicker Form Factor Presents Design Challenges

The necessary mechanical components for folding mechanisms result in devices that are significantly thicker than non-folding smartphones when folded. This increased bulk can be uncomfortable in pockets and purses, reducing the portability advantage that vertical foldables aim to provide.

MARKET CHALLENGES

Supply Chain Complexities Creating Production Bottlenecks

The specialized components required for vertical folding phones present unique supply chain challenges. Flexible displays and precision hinges rely on materials and manufacturing processes that have limited production capacity compared to conventional smartphone components. These constraints can lead to production bottlenecks and inventory challenges during periods of high demand. Some manufacturers have reported yield rates for flexible displays that are significantly lower than standard OLED panels, creating difficulties in scaling production to meet market potential.

Other Challenges

Software Optimization Lagging Behind Hardware Development

While hardware technology has advanced rapidly, many applications still lack fully optimized experiences for vertical foldables. This creates inconsistencies in user experience between native and third-party applications, potentially frustrating users who expect seamless performance across all apps.

Consumer Education Requirements Slowing Market Penetration

The novel form factor requires consumers to adjust their usage patterns and expectations. Many potential buyers need hands-on experience to appreciate the benefits of vertical folding designs, creating a barrier to online sales and requiring additional retail investment in product demonstrations.

MARKET OPPORTUNITIES

Emerging Applications in Enterprise and Productivity Environments

Vertical folding phones present significant opportunities in enterprise and productivity-oriented markets. The ability to transition between phone and small tablet form factors makes these devices particularly attractive for professionals who need mobile productivity tools. Features like multitasking capabilities and enhanced document viewing align well with business use cases. Some manufacturers are exploring partnerships with enterprise software providers to develop specialized versions of their products tailored to business users, creating a potentially lucrative market segment.

Expansion into Mid-Range Price Segments

As technology matures and production scales, significant opportunities exist to bring vertical folding phones to more accessible price points. Some manufacturers have already begun introducing simplified versions of their folding devices at reduced price points, expanding the potential market beyond early adopters and premium buyers. This strategy could dramatically increase market penetration as prices approach conventional flagship levels.

Innovations in Form Factor and Additional Functionality

The vertical folding concept allows for creative extensions of the basic design. Some manufacturers are experimenting with devices that feature secondary external displays for quick interactions while folded, or unique camera implementations that take advantage of the folding mechanism. These innovations could create new use cases and differentiate products in a competitive market. The potential for integrating new sensors or input methods specifically designed for folded and unfolded states presents additional opportunities for manufacturers to create distinctive value propositions.

VERTICAL FOLDING PHONE MARKET TRENDS

Advancements in Flexible Display Technologies Drive Market Growth

The global vertical folding phone market is witnessing rapid expansion due to breakthroughs in flexible display technology, which have enabled manufacturers to produce more durable and reliable foldable devices. While early models faced challenges with screen creasing and durability, recent iterations boast ultrathin glass (UTG) displays that significantly reduce visible creases while enhancing touch sensitivity and scratch resistance. This technological evolution has increased consumer confidence, with vertical foldable shipments projected to grow at a CAGR of 36% between 2024 and 2030. Furthermore, advancements in hinge mechanisms allow these devices to fold seamlessly without compromising structural integrity, making them increasingly appealing for everyday use.

Other Trends

Premiumization in the Smartphone Segment

The demand for high-end smartphones with innovative form factors continues to rise, positioning vertical folding phones as a key growth segment. These devices cater to consumers seeking both compact portability and larger display functionality, effectively merging the benefits of standard smartphones and tablets. Market data indicates that nearly 72% of premium smartphone users consider foldable designs a significant purchase driver, particularly in the $1,000+ price range. This trend is most pronounced in developed economies, where 1 in 3 consumers are willing to pay a premium for cutting-edge form factors that enhance productivity and media consumption.

Growing Enterprise Adoption for Mobile Productivity

Business professionals are increasingly adopting vertical folding phones as productivity tools, thanks to their ability to switch between compact and expanded modes. The larger unfolded displays facilitate easier document editing, video conferencing, and multitasking—features that have driven adoption rates in corporate environments by over 240% since 2022. Financial services, consulting, and tech industries lead this adoption, with 38% of enterprises now considering foldable devices in their mobility budgets. As hybrid work models persist, the demand for versatile communication devices that bridge smartphone convenience with tablet functionality is expected to sustain long-term growth in this segment.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Smartphone Manufacturers Compete for Market Share in the Evolving Vertical Folding Segment

The global vertical folding phone market exhibits a moderately concentrated competitive landscape, with major smartphone brands dominating while smaller players struggle to gain traction. Samsung Electronics stands as the clear market leader thanks to its first-mover advantage with the Galaxy Z Flip series, which accounted for over 60% of global vertical foldable shipments in 2024 according to industry reports.

While Samsung currently maintains its pole position, Huawei has been rapidly closing the gap through its Pocket series, particularly in the Chinese market where it holds a 38% market share. This growth stems from Huawei’s vertically integrated supply chain and strong brand loyalty among Chinese consumers.

Chinese manufacturers OPPO and Xiaomi have been making strategic moves to strengthen their positions through aggressive pricing strategies and localized feature sets. Their recently launched models featuring customizable outer displays and improved hinge durability are helping them gain market share in both domestic and Southeast Asian markets.

Meanwhile, Motorola continues to carve out a niche with its Razr series, focusing on nostalgia-driven design and mid-range pricing in Western markets. The company recently announced plans to double its research investment in foldable displays through 2026, signaling its commitment to this growing segment.

List of Key Vertical Folding Phone Manufacturers

- Samsung Electronics (South Korea)

- Huawei Technologies (China)

- OPPO (China)

- Xiaomi Corporation (China)

- Honor (China)

- Motorola (Lenovo) (U.S./China)

- ZTE Corporation (China)

Segment Analysis:

By Type

Internal Folding Screen Mobile Phone Segment Leads Due to Superior Portability and Enhanced Durability

The market is segmented based on type into:

- Internal Folding Screen Mobile Phone

- Subtypes: Flagship models, Mid-range models, and others

- External Folding Screen Mobile Phone

By Application

Leisure and Entertainment Segment Dominates with Increasing Demand for Multimedia Consumption

The market is segmented based on application into:

- Leisure and Entertainment

- Business Office

By Price Range

Premium Segment Holds Major Share Due to Adoption of High-End Features by Tech Enthusiasts

The market is segmented based on price range into:

- Premium (>$1000)

- Mid-range ($500-$1000)

- Budget (<$500)

By Screen Size

6.5-7.5 Inch Segment Accounts for Largest Share Due to Optimal Balance Between Portability and Usability

The market is segmented based on screen size into:

- Below 6.5 Inches

- 6.5-7.5 Inches

- Above 7.5 Inches

Regional Analysis: Vertical Folding Phone Market

Asia-Pacific

The Asia-Pacific region dominates the global vertical folding phone market, driven by strong smartphone penetration, rapid technological adoption, and the presence of key manufacturers like Samsung, Huawei, and Xiaomi. China leads the region with an estimated market size of $X million in 2024, fueled by consumer demand for premium, innovative devices and aggressive local competition. India and South Korea also contribute significantly, with growing middle-class adoption of foldable phones. However, price sensitivity remains a challenge, pushing manufacturers to balance affordability with advanced features. The region benefits from established supply chains and robust R&D investments in display technology.

North America

North America’s vertical folding phone market is propelled by high disposable incomes and early adopter trends, particularly in the U.S. and Canada. Major carriers and retailers actively promote foldable devices to niche segments seeking productivity-enhancing tools. While Samsung’s Galaxy Z Flip series maintains dominance, Motorola’s re-entry with the Razr lineup has intensified competition. The market faces hurdles like premium pricing (average device costs exceeding $1,000) and lingering consumer skepticism about durability. However, telecom partnerships offering installment plans are making these devices more accessible to business professionals and tech enthusiasts.

Europe

Europe presents steady growth for vertical folding phones, with Germany, the UK, and France as primary markets. EU consumers prioritize design aesthetics and brand reputation, benefiting Samsung and emerging competitors like Honor. Strict regulatory standards on device repairability and battery life influence product development, while carrier subsidies help offset high retail prices. The region shows slower adoption compared to Asia due to conservative replacement cycles, but increasing enterprise demand for dual-screen productivity tools is opening new opportunities. Sustainability concerns are prompting manufacturers to improve modular designs and recycling programs.

Middle East & Africa

This emerging market demonstrates untapped potential, with UAE and Saudi Arabia leading adoption among affluent demographics. Telecom operators bundle foldable phones with premium 5G plans, while luxury positioning resonates with status-conscious buyers. Challenges include limited service centers for repairs and low mainstream awareness. As infrastructure improves, manufacturers are testing localized pricing strategies, though imports and taxes keep devices 20-30% more expensive than global averages. Long-term growth hinges on expanding distribution beyond major cities and addressing heat tolerance concerns in extreme climates.

South America

South America’s vertical folding phone market remains niche due to economic volatility and import restrictions, though Brazil and Argentina show gradual uptake. High tariffs inflate prices, making devices accessible only to elite consumers. Xiaomi and Motorola leverage existing brand loyalty to introduce competitively priced models, while Samsung dominates the premium segment. Carrier partnerships are crucial given prevalent device financing culture. Market growth depends on stabilizing currencies and expanding local assembly to reduce costs, though political uncertainties continue to deter major investments in the short term.

Technology Adoption Variance: The vertical folding phone market’s regional dynamics highlight how consumer behavior, economic factors, and infrastructure shape adoption. While Asia-Pacific leads in volume due to manufacturing advantages and tech-savvy populations, Western markets drive premium innovation. Emerging regions await price-point breakthroughs to transition from luxury items to mainstream devices. Ongoing improvements in hinge mechanics and display durability across all regions will be pivotal for long-term market expansion beyond early adopters.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Vertical Folding Phone markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Vertical Folding Phone market was valued at USD 2,752 million in 2024 and is projected to reach USD 4,389 million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Internal Folding Screen, External Folding Screen), application (Leisure and Entertainment, Business Office), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. China and the U.S. are key growth markets.

- Competitive Landscape: Profiles of leading market participants including Huawei, Samsung, OPPO, Xiaomi, Motorola, and others, including their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging display technologies, hinge mechanisms, durability improvements, and software optimization for foldable devices.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as premiumization trends and compact form factors, along with challenges like high prices and durability concerns.

- Stakeholder Analysis: Insights for component suppliers, OEMs, retailers, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Vertical Folding Phone Market?

-> Vertical Folding Phone Market was valued at 2752 million in 2024 and is projected to reach US$ 4389 million by 2032, at a CAGR of 7.3% during the forecast period.

Which key companies operate in Global Vertical Folding Phone Market?

-> Key players include Huawei, Samsung, OPPO, Xiaomi, Motorola, Honor, and ZTE, among others.

What are the key growth drivers?

-> Key growth drivers include premium smartphone demand, compact form factors, technological advancements in foldable displays, and increasing consumer adoption of innovative form factors.

Which region dominates the market?

-> Asia-Pacific is the largest and fastest-growing market, driven by strong demand in China and South Korea, while North America shows significant adoption rates.

What are the emerging trends?

-> Emerging trends include improved hinge mechanisms, ultra-thin glass technology, multi-window software optimization, and decreasing price points.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...