MARKET INSIGHTS

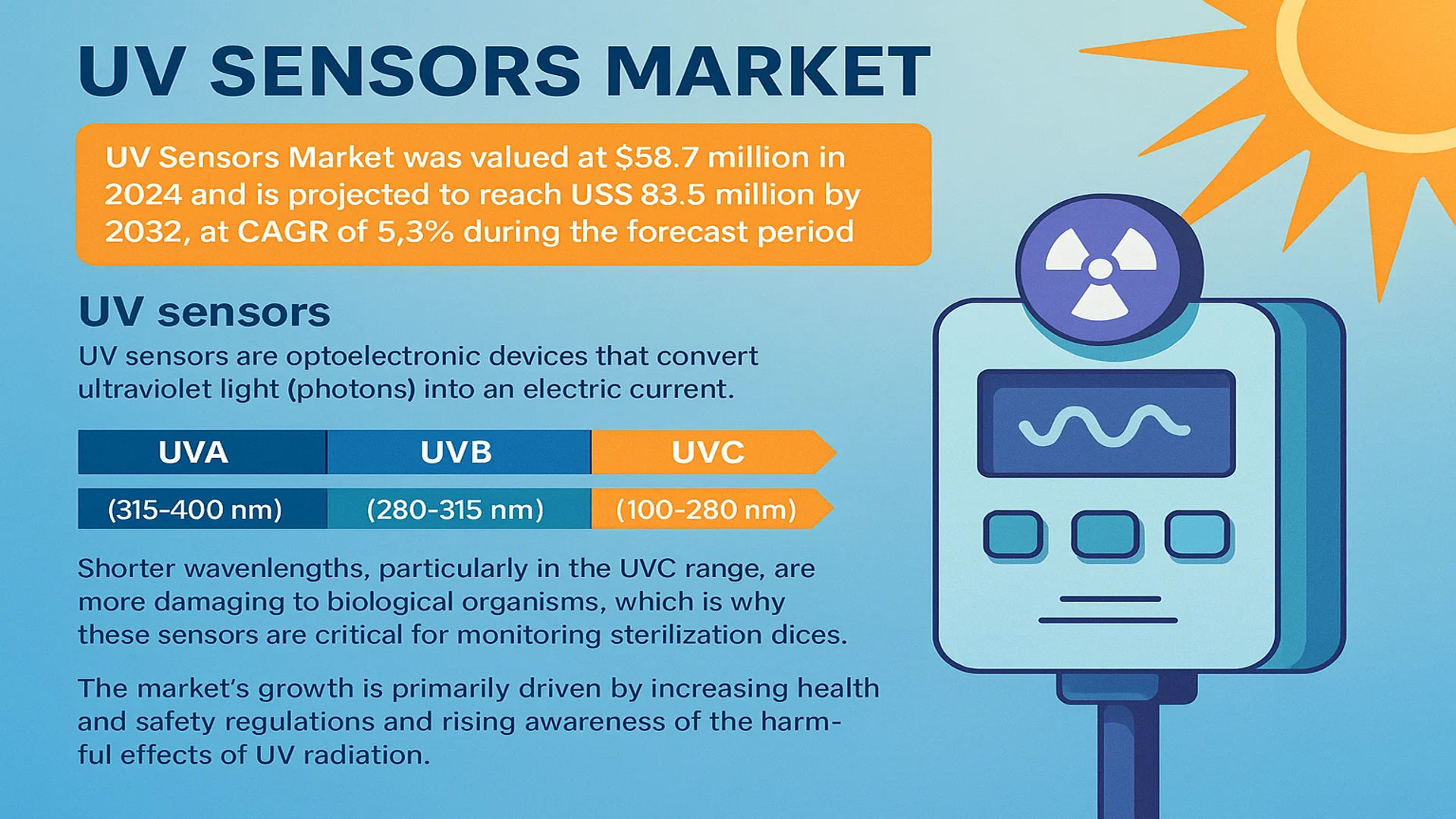

The global UV Sensors Market was valued at 58.7 million in 2024 and is projected to reach US$ 83.5 million by 2032, at a CAGR of 5.3% during the forecast period.

UV sensors are optoelectronic devices that convert ultraviolet light (photons) into an electric current. These components are highly sensitive to specific wavelengths of light in the ultraviolet spectrum, which is classified into three primary bands: UVA (315-400 nm), UVB (280-315 nm), and UVC (100-280 nm). Shorter wavelengths, particularly in the UVC range, are more damaging to biological organisms, which is why these sensors are critical for monitoring sterilization equipment. Conversely, sensors for UVA and UVB are widely deployed in consumer and medical devices to measure sun exposure.

The market’s growth is primarily driven by increasing health and safety regulations and a rising awareness of the harmful effects of UV radiation. Furthermore, the expansion of applications in industrial sterilization, automotive (for smart sunroofs and convertible tops), and wearable consumer electronics is contributing significantly to market expansion. In the competitive landscape, the top five manufacturers collectively hold approximately 75% of the market share, with key players such as Vishay, Silicon Labs, and Panasonic leading through continuous innovation and a broad product portfolio.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for UV-C Disinfection Technologies in Healthcare and Industrial Sectors

The global health crisis has significantly accelerated the adoption of UV-C disinfection technologies across healthcare facilities, laboratories, and public spaces. UV sensors play a critical role in ensuring the effectiveness and safety of these disinfection systems by monitoring UV lamp intensity and verifying proper germicidal exposure levels. Healthcare-associated infections affect millions of patients annually worldwide, creating substantial demand for reliable disinfection solutions. The healthcare UV disinfection market has demonstrated robust growth, with UV sensors becoming essential components in automated disinfection robots, HVAC systems, and water treatment applications. This increased adoption is driving sensor manufacturers to develop more accurate and durable products capable of withstanding continuous operation in demanding environments.

Growing Integration in Consumer Electronics and Wearable Devices

Consumer awareness about sun exposure and skin health has driven the integration of UV sensors into smartphones, smartwatches, and wearable devices. Major technology companies have incorporated UV sensing capabilities to provide users with real-time sun exposure data and personalized recommendations. The global wearable technology market continues to expand rapidly, with health and fitness applications representing a significant growth segment. UV sensors in these devices help users monitor their UV exposure, receive alerts about high radiation levels, and track cumulative exposure over time. This functionality is particularly valuable in regions with high UV indices, where overexposure can lead to serious health concerns. The miniaturization of sensor technology and reduced power consumption have enabled seamless integration into consumer devices without compromising battery life or device form factors.

Stringent Environmental Monitoring Regulations and Standards

Government regulations and international standards regarding environmental monitoring have become increasingly stringent, particularly concerning UV radiation levels in occupational settings and public spaces. Regulatory bodies worldwide have established exposure limits and monitoring requirements for UV radiation in various industries, including manufacturing, construction, and outdoor occupations. These regulations mandate the use of certified UV monitoring equipment equipped with accurate sensors to protect workers from excessive exposure. The environmental monitoring segment has shown consistent growth as industries implement comprehensive safety programs and compliance measures. Additionally, meteorological organizations and climate research institutions utilize high-precision UV sensors for atmospheric monitoring and climate change studies, further driving market demand for advanced sensing solutions.

MARKET CHALLENGES

High Development and Manufacturing Costs Impacting Market Accessibility

The development and production of high-precision UV sensors involve significant technological challenges and substantial investment in research and development. Advanced semiconductor materials and specialized manufacturing processes required for UV-specific photodetectors contribute to higher production costs compared to conventional light sensors. The complex calibration procedures and stringent quality control measures necessary to ensure accuracy across varying environmental conditions further increase manufacturing expenses. These cost factors present challenges for market penetration in price-sensitive applications and emerging economies where budget constraints may limit adoption. While technological advancements have gradually reduced costs, the premium pricing of high-accuracy UV sensors remains a barrier for widespread implementation in cost-conscious market segments.

Other Challenges

Technical Limitations in Extreme Environmental Conditions

UV sensors face performance challenges in extreme environmental conditions, including temperature variations, humidity, and contamination. Sensor accuracy can be affected by temperature drifts, requiring sophisticated compensation algorithms and thermal management systems. High humidity environments may cause condensation on sensor surfaces, potentially affecting measurement reliability. Additionally, dust accumulation and environmental contaminants can degrade sensor performance over time, necessitating regular maintenance and calibration. These technical limitations pose significant challenges for outdoor applications and industrial environments where consistent performance under varying conditions is essential.

Interference from Other Light Sources and Spectral Overlap

The detection of specific UV wavelengths faces challenges due to potential interference from visible and infrared light sources. Many applications require precise measurement of narrow UV bands, particularly in disinfection systems where UV-C effectiveness is wavelength-dependent. Spectral overlap from other light sources can lead to measurement inaccuracies and false readings. Advanced optical filtering techniques and sophisticated signal processing algorithms are required to mitigate these issues, adding complexity and cost to sensor systems. The development of sensors with improved spectral selectivity remains an ongoing challenge for manufacturers seeking to enhance measurement accuracy across diverse application scenarios.

MARKET RESTRAINTS

Limited Awareness and Technical Understanding Among End-Users

Despite growing applications, limited awareness about UV sensor capabilities and technical specifications among potential end-users restrains market growth. Many industries and consumers lack comprehensive understanding of UV measurement principles, sensor specifications, and application requirements. This knowledge gap often leads to underutilization of available technology or inappropriate sensor selection for specific applications. The technical complexity of UV radiation measurement, including concepts such as spectral response, angular dependence, and calibration standards, creates barriers for non-specialist users. Educational initiatives and technical support requirements add to the overall cost of implementation, potentially discouraging adoption in applications where the benefits are not immediately apparent or easily quantifiable.

Supply Chain Constraints and Component Availability Issues

The UV sensor market faces constraints related to supply chain vulnerabilities and availability of specialized components. Many high-performance UV sensors require specific semiconductor materials and optical components that have limited manufacturing sources worldwide. Disruptions in the supply of these specialized materials can significantly impact production schedules and lead times. The global semiconductor shortage has particularly affected sensor manufacturers, causing extended delivery times and increased component costs. Additionally, the specialized nature of UV sensor manufacturing requires specific expertise and equipment, limiting the number of qualified production facilities and creating potential bottlenecks during periods of high demand.

Competition from Alternative Technologies and Integrated Solutions

The market faces restraint from competing technologies and integrated solutions that offer UV sensing as part of multifunctional systems. Many environmental monitoring and industrial control systems incorporate UV sensing capabilities within larger sensor packages, reducing the demand for standalone UV sensors. Additionally, alternative disinfection technologies and monitoring methods may provide competing solutions for certain applications. The development of smart sensor systems that combine multiple environmental parameters in single devices also presents competitive challenges for dedicated UV sensor manufacturers. This trend toward integration requires UV sensor providers to demonstrate clear value propositions and superior performance compared to multifunctional alternatives.

MARKET OPPORTUNITIES

Expansion in Automotive and Transportation Applications

The automotive industry presents significant growth opportunities for UV sensors through integration into advanced driver assistance systems and vehicle comfort features. UV sensors can enhance sun detection systems that automatically adjust climate control settings and window tinting based on solar radiation levels. The growing adoption of sophisticated automotive sensing systems and increasing consumer demand for comfort and convenience features create substantial market potential. The global automotive sensor market continues to expand, providing opportunities for UV sensor integration into next-generation vehicle systems. Additionally, public transportation systems and commercial fleets represent potential markets for UV monitoring solutions aimed at passenger comfort and energy efficiency optimization.

Emerging Applications in Agriculture and Food Safety

UV sensors offer promising opportunities in agricultural technology and food safety applications, where precise UV monitoring can optimize growing conditions and ensure product quality. Controlled environment agriculture increasingly utilizes UV measurements to enhance plant growth, improve crop quality, and manage pest control. The global market for agricultural technology continues to grow rapidly, driven by increasing food demand and sustainable farming practices. UV sensors can also play crucial roles in food processing and storage applications, where UV disinfection is employed to ensure product safety and extend shelf life. The expansion of these applications creates new market segments for UV sensor manufacturers seeking to diversify their customer base and application areas.

Advancements in IoT and Smart City Infrastructure

The proliferation of Internet of Things technologies and smart city initiatives creates substantial opportunities for UV sensor deployment in urban environmental monitoring networks. Municipalities worldwide are implementing comprehensive environmental monitoring systems to track air quality, weather conditions, and public health indicators. UV sensors can contribute valuable data for public health advisories, urban planning, and environmental management. The integration of UV sensing capabilities into existing smart city infrastructure allows for cost-effective expansion of monitoring capabilities without requiring separate sensor networks. The global smart city market demonstrates strong growth potential, providing opportunities for sensor manufacturers to develop solutions specifically designed for urban deployment and networked operation.

UV SENSORS MARKET TRENDS

Rising Demand for UV-C Disinfection Systems to Emerge as a Key Trend

The global emphasis on hygiene and infection control, particularly in the wake of recent global health challenges, has significantly accelerated the adoption of UV-C disinfection technologies. UV sensors are critical components in these systems, ensuring the proper dosage of germicidal ultraviolet light is delivered for effective pathogen inactivation. This trend is most pronounced in healthcare settings, where hospitals are increasingly integrating automated UV disinfection robots into their cleaning protocols. Beyond healthcare, the application has expanded into public transportation, hospitality, and food processing facilities. The reliability of these systems is paramount, driving demand for highly accurate sensors that can monitor UV lamp output in real-time to guarantee efficacy and safety. This surge is a primary factor propelling the market, with the industrial application segment commanding a significant share of the overall demand.

Other Trends

Integration into Consumer Electronics and Wearables

A notable trend is the growing integration of UV sensors into consumer electronics, particularly smartphones and wearable devices. This is driven by rising consumer awareness regarding the harmful effects of prolonged sun exposure, such as skin damage and increased cancer risk. Manufacturers are embedding these sensors to provide users with personalized UV index readings and sun safety recommendations. The miniaturization of sensor technology has been crucial for this trend, allowing for compact designs that do not compromise device aesthetics or functionality. This consumer-driven demand is creating a substantial new revenue stream within the market, moving beyond traditional industrial applications.

Advancements in Sensor Technology and Material Science

Technological innovation is a powerful force shaping the UV sensor landscape. Recent developments are focused on enhancing sensor performance, including improved sensitivity, faster response times, and greater spectral selectivity to distinguish between UV-A, UV-B, and UV-C wavelengths. There is also a significant push towards developing more robust and durable sensors capable of withstanding harsh environmental conditions, which is critical for outdoor and industrial applications. Furthermore, research into new semiconductor materials, such as gallium nitride (GaN) and aluminum gallium nitride (AlGaN), promises sensors with higher efficiency and better performance characteristics than traditional silicon-based options. These advancements are not only improving existing products but are also enabling entirely new applications in fields like environmental monitoring and automotive systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Leaders Focus on Innovation and Strategic Expansion to Capture Market Share

The global UV sensors market exhibits a semi-consolidated competitive structure, characterized by the presence of multinational electronics giants, specialized sensor manufacturers, and emerging technology firms. Panasonic Corporation and Vishay Intertechnology, Inc. are recognized as dominant players, collectively holding a significant portion of the 2024 market share. Their leadership is largely attributable to extensive distribution networks, diverse application-specific product portfolios, and strong brand recognition across consumer electronics and industrial sectors.

Silicon Labs and STMicroelectronics have also secured considerable market positions, driven by their expertise in semiconductor technology and integrated sensor solutions. These companies are particularly strong in applications requiring miniaturization and low power consumption, such as in wearable devices and IoT ecosystems. Their continuous investment in R&D allows them to introduce advanced sensors with higher accuracy and better performance, catering to the evolving demands of modern electronics.

Furthermore, companies are aggressively pursuing growth through strategic initiatives. Recent developments include expansions into high-growth regions like Asia-Pacific and new product launches designed for emerging applications in automotive UV sensing and environmental monitoring. These moves are critical for maintaining competitiveness in a market projected to grow at a CAGR of 5.3% through 2032.

Meanwhile, specialized players like Solar Light Company, Apogee Instruments, and Sglux are strengthening their niches through deep technical expertise and focus on high-accuracy measurement for scientific and industrial applications. Their strategy often involves partnerships with research institutions and industry-specific customers, ensuring steady demand in segments like environmental testing and medical equipment sterilization.

List of Key UV Sensor Companies Profiled

- Panasonic Corporation (Japan)

- Vishay Intertechnology, Inc. (U.S.)

- Silicon Laboratories Inc. (U.S.)

- STMicroelectronics N.V. (Switzerland)

- Solar Light Company, Inc. (U.S.)

- Apogee Instruments, Inc. (U.S.)

- Sglux GmbH (Germany)

- GaNo Optoelectronics Co., Ltd. (Taiwan)

- Hamamatsu Photonics K.K. (Japan)

- Balluff GmbH (Germany)

- GenUV (Germany)

- Broadcom Inc. (U.S.)

Segment Analysis:

By Type

UVA Sensors Segment Dominates the Market Due to Pervasive Use in Consumer Electronics and Automotive Applications

The market is segmented based on type into:

- UVA

- UVB

- UVC

By Application

Industrial Segment Leads Due to Critical Role in Sterilization and Process Control Systems

The market is segmented based on application into:

- Industrial

- Consumer Electronics

- Automotive

- Medical

- Environmental and Food Testing

- Other

By End User

Manufacturing Sector is the Largest End User Driven by Automation and Quality Control Needs

The market is segmented based on end user into:

- Manufacturing

- Healthcare

- Consumer Goods

- Research and Academia

- Others

By Technology

Photodiode-based Sensors Hold Major Share Owing to High Sensitivity and Cost-Effectiveness

The market is segmented based on technology into:

- Photodiode

- Phototransistor

- Others

Regional Analysis: UV Sensors Market

Asia-Pacific

The Asia-Pacific region dominates the global UV sensors market, accounting for approximately 45% of total market share by volume. This leadership position is driven by massive manufacturing output, particularly in China, which holds about 75% of regional manufacturing capacity through key players like HAMAMATSU, Vishay, and Silicon Labs. The region’s growth is fueled by expanding industrial applications, including UV sterilization equipment in food processing and healthcare facilities, alongside rising consumer electronics integration. While cost sensitivity maintains demand for conventional UVA sensors (representing about 55% of regional product mix), increasing environmental awareness and government initiatives are accelerating adoption of advanced UVB and UVC sensors for pollution monitoring and water treatment applications.

North America

North America represents a technologically advanced and regulated market for UV sensors, characterized by stringent quality standards and high adoption in medical and industrial sterilization applications. The United States leads the region with significant demand from healthcare facilities implementing UV-C disinfection systems, particularly following increased focus on infection control post-pandemic. The region shows strong growth in environmental monitoring applications, with UV sensors being integrated into air quality monitoring systems across major metropolitan areas. While manufacturing presence is limited compared to Asia-Pacific, North American companies focus on high-value, precision sensors for specialized applications in pharmaceuticals and biotechnology, driving premium pricing and higher profit margins.

Europe

The European UV sensor market is shaped by rigorous regulatory frameworks, particularly EU directives on environmental monitoring and industrial safety. Germany and France emerge as key markets, driven by advanced manufacturing sectors and strong adoption in automotive applications for sun exposure detection systems. The region demonstrates growing demand for UV sensors in food safety applications, with strict regulations driving implementation in packaging and processing equipment. European manufacturers emphasize research and development, focusing on energy-efficient and miniaturized sensor solutions. While the market faces pressure from cost-competitive Asian imports, European companies maintain competitiveness through technological innovation and compliance with stringent EU environmental and safety standards.

South America

South America represents an emerging market for UV sensors, with growth primarily driven by Brazil and Argentina’s developing industrial and healthcare sectors. The region shows increasing adoption in water treatment applications, particularly in urban areas addressing sanitation challenges. While market penetration remains limited compared to developed regions, growing awareness of UV technology’s benefits in medical sterilization and food safety presents significant opportunities. Economic volatility and infrastructure challenges currently restrain widespread adoption, but gradual industrial modernization and increasing foreign investment suggest long-term growth potential, particularly in industrial UV-C applications for manufacturing and processing facilities.

Middle East & Africa

The Middle East & Africa region demonstrates nascent but promising growth in UV sensor adoption, primarily driven by water purification and healthcare applications. Gulf Cooperation Council countries, particularly the UAE and Saudi Arabia, lead in adopting advanced UV technologies for desalination plants and medical facilities. The region shows increasing interest in environmental monitoring applications, addressing air quality concerns in rapidly urbanizing areas. While limited local manufacturing exists, the market relies heavily on imports from established global suppliers. Infrastructure development and growing healthcare investment present opportunities for market expansion, though progress is moderated by economic diversification priorities and evolving regulatory frameworks across the region.

Report Scope

This market research report provides a comprehensive analysis of the global and regional UV Sensors market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global UV Sensors Market?

-> UV Sensors Market was valued at 58.7 million in 2024 and is projected to reach US$ 83.5 million by 2032, at a CAGR of 5.3% during the forecast period.

Which key companies operate in Global UV Sensors Market?

-> Key players include Panasonic, Vishay, Silicon Labs, ST Microelectronics, Broadcom, and HAMAMATSU, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for UV sterilization in healthcare, rising adoption in consumer electronics for UV index monitoring, and stringent environmental monitoring regulations.

Which region dominates the market?

-> Asia-Pacific is the largest market, with China holding approximately 30% of the global market share, followed by North America and Europe.

What are the emerging trends?

-> Emerging trends include miniaturization of sensors for wearable devices, integration with IoT for real-time environmental monitoring, and development of multi-spectral UV sensors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...