MARKET INSIGHTS

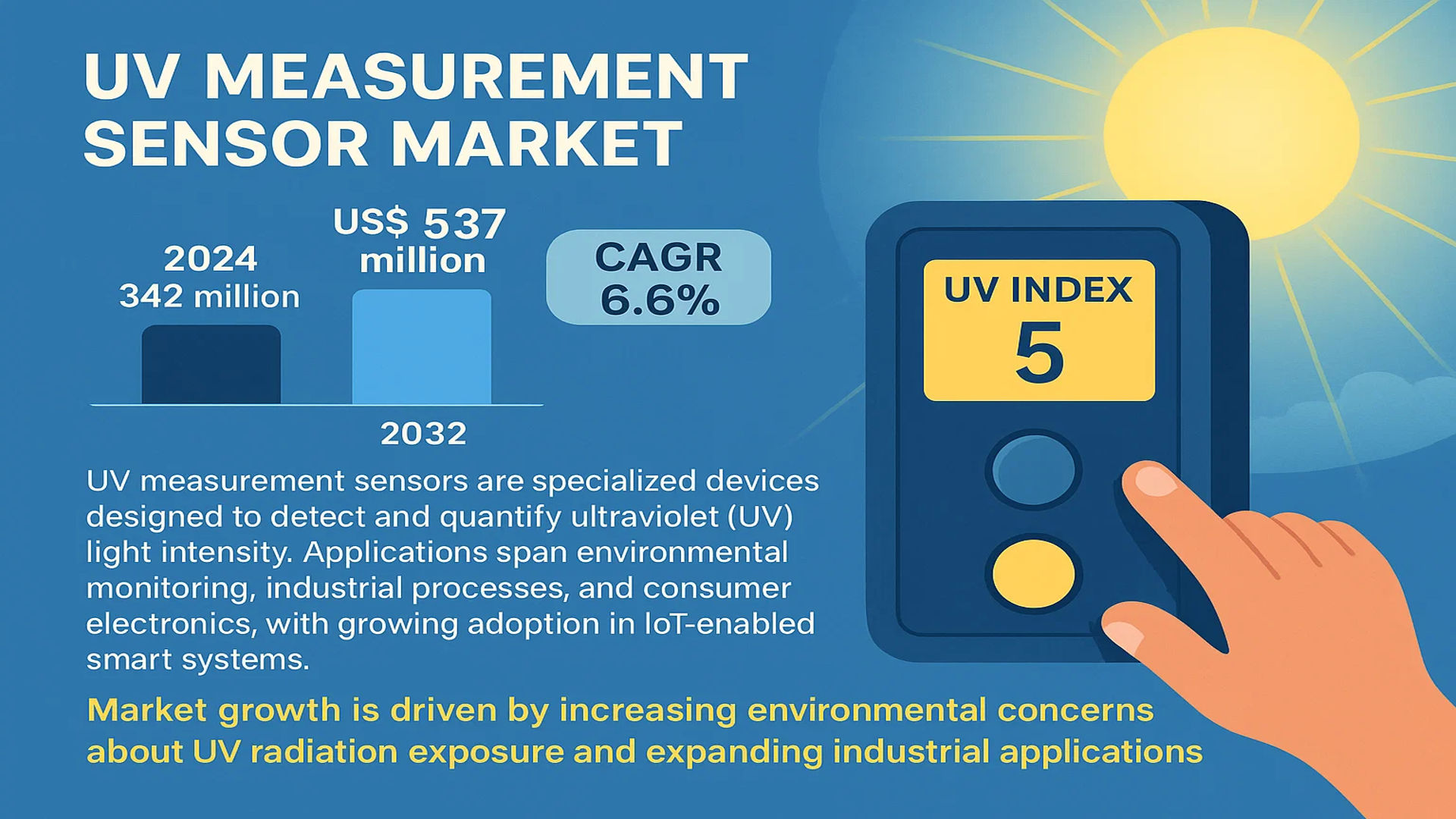

The global UV Measurement Sensor Market was valued at 342 million in 2024 and is projected to reach US$ 537 million by 2032, at a CAGR of 6.6% during the forecast period.

UV measurement sensors are specialized devices designed to detect and quantify ultraviolet (UV) light intensity. These sensors operate on the principle of photoelectric conversion, where UV radiation excites electrons in photosensitive materials, generating measurable electrical signals proportional to light intensity. Applications span environmental monitoring, industrial processes, and consumer electronics, with growing adoption in IoT-enabled smart systems.

Market growth is driven by increasing environmental concerns about UV radiation exposure and expanding industrial applications. The sensors play critical roles in UV curing processes for coatings and adhesives, semiconductor photolithography, and real-time UV index monitoring for public health. Recent industry developments include sensor miniaturization and IoT integration, exemplified by smart agriculture systems that optimize crop growth through UV light exposure adjustments. Key players like Panasonic, ST Microelectronics, and Vishay are expanding their portfolios with advanced sensor solutions to meet diverse application needs.

MARKET DYNAMICS

MARKET DRIVERS

Increased Demand for Skin Cancer Prevention to Fuel UV Sensor Adoption

The global rise in skin cancer cases has significantly boosted demand for UV measurement sensors in healthcare and retail sectors. With over 1.5 million skin cancer diagnoses annually worldwide, wearable UV sensors and public monitoring systems have become critical tools for prevention. Consumers increasingly rely on real-time UV index readings from smartphones and smartwatches to manage sun exposure. The medical community’s emphasis on early detection has further accelerated integration of these sensors into dermatological devices and hospital monitoring systems.

Industrial Automation Revolution to Accelerate Market Growth

UV curing applications in manufacturing processes are driving unprecedented demand for high-precision UV sensors across multiple industries. The automotive sector alone accounts for over 25% of industrial UV sensor usage, primarily for paint curing and adhesive bonding applications. As manufacturers increasingly automate production lines, the need for integrated quality control systems with UV measurement capabilities has surged. Semiconductor fabrication facilities have also expanded adoption, with photolithography processes requiring nanoscale UV intensity monitoring to maintain chip yield rates above 96% in advanced nodes.

Smart City Initiatives to Create New Application Areas

Urban infrastructure projects worldwide are incorporating UV sensors into environmental monitoring networks and public health systems. Many municipalities now integrate these sensors with weather stations to issue real-time UV exposure alerts via mobile apps and digital signage. Tourism-dependent regions have particularly embraced this technology, with coastal cities deploying sensor networks that adjust public shading systems automatically based on UV radiation levels. These smart city applications currently represent the fastest-growing segment, with annual installations increasing by over 35% in major metropolitan areas.

MARKET CHALLENGES

Precision Calibration Requirements Increase Implementation Costs

UV sensor manufacturers face significant technical hurdles in maintaining measurement accuracy across diverse environmental conditions. Unlike other optical sensors, UV detectors require meticulous calibration to account for atmospheric variables such as humidity and particulate matter. Industrial-grade sensors must withstand extreme operating conditions while maintaining sensitivity within ±2% tolerance, driving up production costs substantially. Many small and medium enterprises find the required investment in calibration equipment and skilled technicians prohibitive, limiting market penetration in price-sensitive sectors.

Cross-Sensitivity Issues Compromise Data Reliability

Modern UV sensors frequently encounter interference from visible and infrared light, leading to measurement inaccuracies that undermine their effectiveness. This spectral sensitivity challenge becomes particularly acute in industrial settings where multiple light sources coexist. Some photolithography applications have reported up to 15% measurement variance due to ambient light pollution, forcing manufacturers to implement costly shielding solutions. The research community continues to seek breakthrough materials that can provide better wavelength discrimination without sacrificing sensor responsiveness or durability.

Regulatory Fragmentation Slows Market Standardization

The absence of unified global standards for UV measurement creates compliance challenges for sensor manufacturers serving multiple regions. While medical applications follow strict FDA guidelines, industrial and consumer products face a patchwork of conflicting regional requirements. This regulatory complexity forces companies to maintain multiple product variants, increasing inventory costs by an estimated 20-30%. The lack of harmonization particularly impacts IoT applications, where cross-border data compatibility issues frequently arise between different regulatory frameworks.

MARKET RESTRAINTS

Limited Consumer Awareness Hinders Mass Adoption

Despite growing health concerns, many consumers remain unaware of UV measurement technologies beyond basic sunscreen recommendations. Surveys indicate that less than 30% of smartphone users actively utilize built-in UV sensing capabilities, reflecting a significant education gap. This limited market awareness directly impacts adoption rates for standalone UV monitoring devices, particularly in emerging economies where prevention messaging focuses on basic precautions rather than technological solutions. Manufacturers face the dual challenge of developing affordable products while simultaneously educating potential buyers about their benefits.

Material Science Limitations Constrain Innovation

Current UV sensor technologies face inherent material constraints that limit performance improvements. Silicon-based detectors, while cost-effective, struggle with sensitivity below 300nm, creating accuracy gaps in critical UV-C monitoring applications. Emerging wide-bandgap semiconductors show promise but remain prohibitively expensive for most commercial uses, with production costs approximately 50% higher than conventional solutions. These material limitations have created an innovation bottleneck, particularly for applications requiring continuous monitoring under harsh environmental conditions.

MARKET OPPORTUNITIES

AI-Powered Analytics to Create Next-Generation Solutions

The integration of machine learning with UV sensor networks presents a transformative opportunity for predictive maintenance and precision monitoring. Advanced algorithms can now compensate for environmental variables in real-time, improving measurement accuracy by up to 40% compared to traditional calibration methods. Several industrial equipment manufacturers have already begun embedding AI chips directly into UV sensors, enabling localized data processing that reduces cloud dependency. This technological convergence is particularly valuable for remote monitoring applications in agriculture and energy, where connectivity limitations previously restricted implementation.

Emerging Applications in Food Safety Monitoring

Food processing facilities are increasingly adopting UV sensors as part of HACCP compliance systems, creating a high-growth niche market. UV measurement plays a critical role in verifying the effectiveness of surface disinfection systems, with major poultry processors reporting a 30% reduction in contamination incidents after implementation. The phytosanitary treatment sector has also shown strong uptake, using UV intensity monitoring to ensure optimal exposure for fresh produce without compromising quality. As food safety regulations tighten globally, this application segment is projected to grow at an above-market rate of 9.2% annually.

Miniaturization Trend to Enable Wearable Innovation

Breakthroughs in MEMS technology are enabling a new generation of sub-miniature UV sensors suitable for integration into smart textiles and disposable medical devices. Several dermatology research groups have prototyped adhesive UV monitors smaller than a postage stamp that can provide continuous exposure tracking over multi-day periods. The consumer electronics sector anticipates integrating these microsensors into next-generation wearables, potentially creating a market for over 500 million units annually by 2030. This miniaturization drive aligns perfectly with the growing demand for personalized health monitoring solutions across all demographics.

UV MEASUREMENT SENSOR MARKET TRENDS

Rising Environmental and Health Concerns Fuel UV Sensor Demand

The global UV measurement sensor market is experiencing significant growth due to increasing awareness about the harmful effects of ultraviolet (UV) radiation on human health and the environment. With the ozone layer’s depletion contributing to higher UV exposure, governments and health organizations are prioritizing real-time UV monitoring to issue public advisories. The market for UV sensors in environmental monitoring applications is projected to grow at a CAGR of 6.6% from 2024 to 2032, driven by stringent regulations and the need for precise UV index measurements. In addition, rising concerns about skin cancer risks are accelerating the adoption of UV sensors in wearable devices and weather stations.

Other Trends

Industrial Automation and UV Curing Applications

The demand for UV sensors in industrial applications, particularly UV curing processes, is growing rapidly. Industries such as coatings, adhesives, and printing rely on UV sensors to maintain product quality by ensuring uniform curing. The market for industrial UV sensors is expected to reach $185 million by 2027, owing to the increasing use of UV-curable materials in automotive and electronics manufacturing. Furthermore, semiconductor manufacturers utilize high-precision UV sensors in photolithography, where accurate UV exposure is critical for microchip production.

IoT Integration and Smart System Developments

Advancements in IoT and smart technologies are revolutionizing the UV sensor market by enabling remote monitoring and automated control. In agriculture, UV sensors integrated with smart irrigation systems help optimize plant growth by adjusting UV exposure levels dynamically. The adoption of IoT-enabled UV sensors in smart cities and air quality monitoring networks is further boosting market expansion. Countries with high solar radiation, such as Australia and India, are leading in deploying these technologies to mitigate UV-related health risks and enhance environmental surveillance.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Partnerships Drive Market Competition

The global UV measurement sensor market exhibits a highly competitive landscape, characterized by a mix of established industrial players, specialized sensor manufacturers, and emerging technology firms. Vishay Intertechnology, Inc. currently holds a dominant position in the market, with its broad portfolio of UV photodiodes and sensors used across industrial, automotive, and consumer electronics applications. The company’s 2023 revenue from optoelectronic components exceeded $850 million, demonstrating its strong foothold in light sensing technologies.

STMicroelectronics and Broadcom Inc. follow closely, having captured significant market share through their advanced semiconductor-based UV sensor solutions. STMicroelectronics’ recent launch of the UVIS25 ultraviolet light sensor with embedded algorithms for UV index calculation has strengthened its position in wearable and IoT applications. Broadcom’s expertise in optoelectronics has enabled it to secure contracts with major consumer electronics manufacturers for smartphone UV sensing applications.

The market also features specialized players like Skye Instruments Ltd and Solar Light Company, who focus specifically on environmental and meteorological UV measurement systems. These companies have benefited from increasing demand for UV monitoring in weather stations and climate research, with Skye Instruments reporting 12% year-over-year growth in its sensor division for 2023.

Strategic collaborations are shaping the competitive dynamics, as seen in Panasonic’s partnership with major sunscreen manufacturers to develop UV sensors for personal care products. Meanwhile, emerging players like Sglux and uv technik international are gaining traction through innovative UV sensor solutions for industrial curing and water sterilization applications.

List of Key UV Measurement Sensor Companies Profiled

- Vishay Intertechnology, Inc. (U.S.)

- STMicroelectronics (Switzerland)

- Broadcom Inc. (U.S.)

- Panasonic Corporation (Japan)

- Skye Instruments Ltd (U.K.)

- Solar Light Company (U.S.)

- Sglux (Germany)

- uv technik international (Germany)

- Vernier Software & Technology (U.S.)

Segment Analysis:

By Type

Plug-In Sensors Segment Leads Due to High Precision and Ease of Integration

The market is segmented based on type into:

- Plug-In Sensors

- Subtypes: Photodiode-based, CMOS-based, and others

- Non-Plug-In Sensors

- Subtypes: Handheld devices, wearable sensors, and others

By Application

Industrial Applications Drive Market Growth With Rising Demand for UV Curing Processes

The market is segmented based on application into:

- Industrial

- Consumer Electronics

- Automotive

- Medical Industry

- Others

By Technology

Photodiode-Based Sensors Dominant Due to Better UV Wavelength Sensitivity

The market is segmented based on technology into:

- Photodiode-based

- CMOS-based

- GaN-based

- Others

By End User

Environmental Monitoring Sector Shows Strong Growth With Increased UV Index Tracking

The market is segmented based on end user into:

- Manufacturing

- Healthcare

- Environmental Monitoring

- Research Institutions

- Others

Regional Analysis: UV Measurement Sensor Market

Asia-Pacific

The Asia-Pacific region leads the global UV measurement sensor market, driven by rapid industrialization, growing environmental monitoring initiatives, and strong demand for consumer electronics. China dominates with its thriving semiconductor sector, where UV sensors are critical for photolithography applications in chip manufacturing. Japan and South Korea follow closely, with their advanced automotive and medical device industries adopting UV sensing technologies for quality control. India’s expanding healthcare infrastructure and government-backed air quality monitoring projects contribute to regional growth. The adoption of smart agriculture technologies in Southeast Asia further boosts demand for IoT-integrated UV sensors to optimize crop yields.

North America

North America maintains a technologically advanced UV sensor market, with the U.S. accounting for over 60% of regional revenue. Stringent workplace safety regulations under OSHA drive demand for industrial UV monitoring in manufacturing sectors. The region’s mature healthcare sector utilizes UV sensors for sterilization equipment and dermatological applications. Canada’s focus on environmental conservation supports weather monitoring station deployments. Research institutions and universities collaborate with sensor manufacturers to develop next-generation UV detection technologies, particularly for space and defense applications.

Europe

Europe’s UV sensor market benefits from strict environmental regulations and high industrial automation adoption. Germany leads in industrial applications, particularly in automotive coating processes and printing industries. The EU’s emphasis on renewable energy has increased demand for UV monitoring in solar panel efficiency testing. Scandinavian countries invest heavily in climate research, utilizing advanced UV sensors for atmospheric studies. Medical device manufacturers in Switzerland and France incorporate UV sensors into diagnostic equipment, while Southern European nations focus on tourism-related UV index monitoring systems for public health.

South America

South America’s UV sensor market shows gradual growth, with Brazil and Argentina emerging as key consumers. Mining operations utilize UV sensors for mineral analysis, while agricultural exporters adopt the technology for food safety monitoring. Challenges include economic instability limiting capital investments and fragmented regulatory frameworks slowing standardization. However, increasing awareness of skin cancer risks drives demand for consumer-grade UV monitoring devices in urban coastal areas. Government initiatives for water purification projects present new opportunities for UV sensor applications in public health infrastructure.

Middle East & Africa

The MEA region exhibits uneven market development for UV sensors. Gulf Cooperation Council countries lead in adoption, particularly for water treatment plants and oil refinery processes. Israel’s thriving tech sector develops advanced military and aerospace sensor applications. Africa’s market remains nascent but shows potential in agricultural monitoring and mining operations. Infrastructure limitations and low technology penetration hinder widespread adoption, though foreign investments in smart city projects are gradually introducing UV sensing technologies for environmental monitoring applications in select urban centers.

Report Scope

This market research report provides a comprehensive analysis of the global UV Measurement Sensor market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global UV Measurement Sensor market was valued at USD 342 million in 2024 and is projected to reach USD 537 million by 2032, growing at a CAGR of 6.6%.

- Segmentation Analysis: Detailed breakdown by product type (Plug-In Sensor, Non-Plug-In Sensors), application (Industrial, Consumer Electronics, Automotive, Medical Industry, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. In 2024, Asia-Pacific held the largest market share (38%), followed by North America (28%).

- Competitive Landscape: Profiles of 17 leading market participants including Panasonic, Vishay, ST Microelectronics, and Broadcom, covering their product portfolios, market share (top 5 companies held 42% share in 2024), and recent developments.

- Technology Trends: Analysis of IoT integration in UV sensors, advancements in photoelectric conversion technology, and emerging applications in smart agriculture and industrial automation.

- Market Drivers & Restraints: Key growth drivers include increasing UV radiation monitoring needs (72% of weather stations now incorporate UV sensors) and industrial UV curing applications. Challenges include high costs of precision sensors.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, OEMs, system integrators, and investors in the UV measurement ecosystem.

The research methodology combines primary interviews with industry experts and analysis of verified market data from regulatory bodies and industry associations, ensuring report accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global UV Measurement Sensor Market?

-> UV Measurement Sensor Market was valued at 342 million in 2024 and is projected to reach US$ 537 million by 2032, at a CAGR of 6.6% during the forecast period..

Which key companies operate in Global UV Measurement Sensor Market?

-> Key players include Panasonic, Vishay, ST Microelectronics, Broadcom, Silicon Labs, and Skye Instruments, with the top 5 companies holding 42% market share in 2024.

What are the key growth drivers?

-> Growth is driven by increasing UV radiation monitoring needs (72% adoption in weather stations), industrial UV curing applications, and IoT integration in smart agriculture systems.

Which region dominates the market?

-> Asia-Pacific leads with 38% market share in 2024, driven by industrial growth in China and Japan, followed by North America at 28%.

What are the emerging trends?

-> Emerging trends include miniaturization of sensors, IoT-enabled remote monitoring systems, and increased adoption in medical sterilization applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...