USA AI Rad-Hard By Design IP Licensing for National Security Space Market Insights

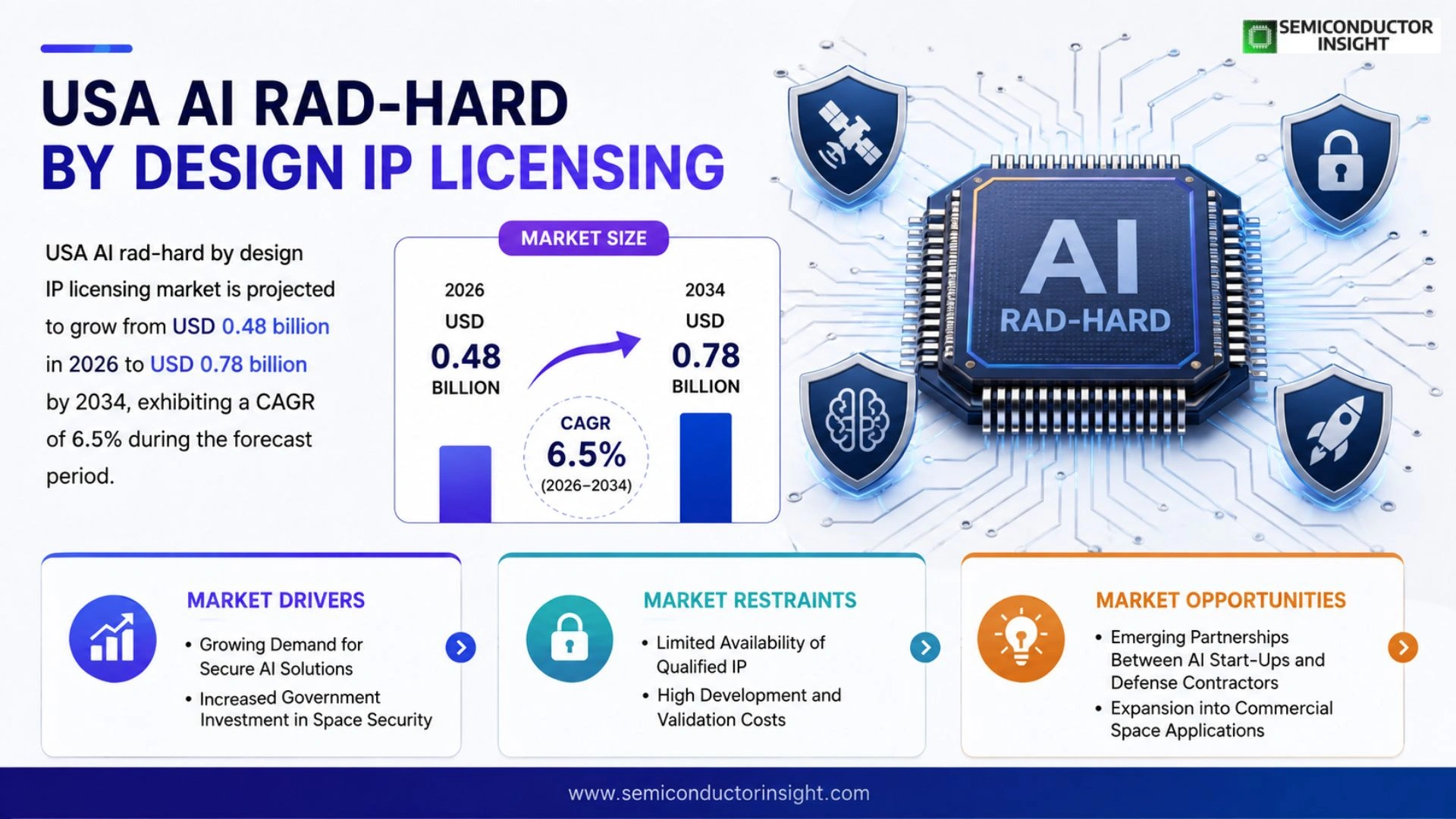

Global USA AI rad‑hard by design IP licensing market size was valued at USD 0.45 billion in 2025. The market is projected to grow from USD 0.48 billion in 2026 to USD 0.78 billion by 2034, exhibiting a CAGR of 6.5% during the forecast period.

AI rad‑hard by design IP licensing enables manufacturers of national‑security space systems to embed radiation‑tolerant artificial‑intelligence architectures directly into hardware designs under legally protected intellectual‑property agreements. This approach ensures that critical on‑orbit payloads maintain functional integrity against high‑energy particle environments while leveraging proprietary AI algorithms.

The market is accelerating because U.S. defense budgets have allocated over USD 12 billion to resilient space capabilities since FY2023, and the Space Development Agency has issued multiple licensing solicitations for rad‑hard AI modules in low‑Earth orbit constellations. Furthermore, collaborations between firms such as Lockheed Martin and academic labs are expanding the pool of qualified patents, driving broader adoption across satellite manufacturers.

MARKET DRIVERS

Growing Demand for Secure AI Solutions

USA AI Rad-Hard By Design IP Licensing for National Security Space Market is being propelled by heightened awareness of cyber‑physical threats to satellite platforms. Agencies are prioritizing AI models that are inherently radiation‑hardening to ensure mission continuity in the harsh space environment. This strategic shift creates a clear preference for licensed technologies that demonstrate proven resilience.

Government Investment in Space Resilience

Recent budget allocations underscore a sustained commitment to modernizing national security space assets. Funding streams are earmarked for IP licensing programs that integrate AI‑driven analytics with rad‑hard design principles, enabling faster anomaly detection and autonomous decision‑making on orbit. Companies that align with these investment priorities gain a competitive advantage.

➤ “Secure AI that endures space radiation is no longer a niche requirement; it is becoming a baseline expectation for all national security missions.”

These drivers collectively reinforce a market trajectory where trusted AI capabilities become a prerequisite for future space operations, accelerating the adoption of rad‑hard licensing frameworks.

MARKET CHALLENGES

Regulatory Uncertainty

While the strategic importance of USA AI Rad-Hard By Design IP Licensing for National Security Space Market is clear, the evolving regulatory landscape introduces ambiguity. Agencies must reconcile emerging AI governance policies with existing export‑control regimes, which can delay licensing negotiations and increase compliance costs.

Other Challenges

Technical Integration

Integrating rad‑hard AI modules into legacy satellite architectures demands rigorous testing and validation. The need to certify both radiation tolerance and AI performance simultaneously adds complexity, often extending development timelines.

MARKET RESTRAINTS

Limited Availability of Qualified IP

The pool of vendors offering AI systems specifically engineered for radiation environments remains modest. This scarcity can constrain procurement options and lead to higher licensing fees, potentially restraining smaller contractors from participating in the market.

MARKET OPPORTUNITIES

Emerging Partnerships Between AI Start‑Ups and Defense Contractors

Collaborative models that pair innovative AI start‑ups with established defense aerospace firms are creating new pathways for technology transfer. Such alliances enable rapid scaling of rad‑hard AI capabilities, opening significant growth opportunities within USA AI Rad-Hard By Design IP Licensing for National Security Space Market.

Additionally, the push toward modular satellite designs invites a broader set of licensing arrangements, allowing multiple stakeholders to leverage reusable AI IP blocks across diverse missions, further expanding market potential.

USA AI Rad-Hard By Design IP Licensing for National Security Space Market Trends

Growth Drivers and Funding Landscape

USA AI Rad-Hard By Design IP Licensing for National Security Space Market is experiencing rapid expansion as the global AI rad‑hard by design IP licensing market increased from USD 0.45 billion in 2025 to USD 0.48 billion in 2026 and is projected to reach USD 0.78 billion by 2034, reflecting a 6.5 % CAGR. This upward trajectory is underpinned by the U.S. defense establishment allocating more than USD 12 billion toward resilient space capabilities since FY2023, and the Space Development Agency’s recent solicitation of licensing agreements for radiation‑tolerant AI modules in low‑Earth‑orbit constellations. The alignment of these investments with the National Defense Authorization Act’s focus on AI resilience has created a clear policy pathway that encourages private‑sector participation and accelerates certification timelines.

Other Trends

Patent Landscape Expansion

Patent activity is accelerating as major contractors such as Lockheed Martin partner with university research labs to file new rad‑hard AI inventions. The resulting portfolio of licensed intellectual property now covers a broader spectrum of sensor‑fusion algorithms, autonomous navigation routines, and on‑board decision‑making kernels, enabling satellite manufacturers to embed certified AI directly into radiation‑exposed hardware without additional clearance delays. Licensing agreements typically grant manufacturers exclusive rights to implement the AI cores for a defined mission class, while preserving the ability of the originator to pursue further research, a model that balances commercial incentive with national‑security imperatives.

Emerging Deployment Scenarios

Deployment strategies are shifting toward modular constellation architectures where each node incorporates a pre‑qualified AI rad‑hard IP block. This design‑by‑license approach shortens development cycles, reduces integration risk, and supports the United States’ strategic objective of maintaining continuous on‑orbit processing capabilities. As more agencies adopt the licensing model, the market is set to consolidate around a handful of vetted IP providers, driving further standardization and cost efficiencies across the national‑security space sector. Analysts anticipate that by 2030 the licensing ecosystem will support at least three major satellite constellations, delivering continuous AI‑enhanced situational awareness and reinforcing the United States’ strategic posture in contested space.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Dynamics in USA AI Rad‑Hard By Design IP Licensing for National Security Space

The market is dominated by a few large defense contractors that have deep integration capabilities with both government agencies and academic research labs. Lockheed Martin leads the space, leveraging its long‑standing relationships with the Space Development Agency (SDA) and U.S. Space Force to embed patented rad‑hard AI architectures into next‑generation satellite buses. Its portfolio of licensed patents covers radiation‑tolerant neural inference engines, fault‑tolerant memory subsystems, and secure model update mechanisms, positioning it as the primary IP licensor for large constellations. The market structure is tiered: a core of integrated system integrators controls the majority of licensing volume, while a surrounding layer of specialized component makers provides niche algorithmic and firmware modules that feed into the broader ecosystem.

Beyond the lead integrator, a robust set of niche players contributes critical capabilities that broaden the license pool. Northrop Grumman and Boeing supply hardened avionics and signal‑processing IP, whereas Raytheon Technologies offers radiation‑shielded AI accelerator patents for payload processing. Maxar Technologies and Sierra Nevada Corp focus on adaptable AI payloads for Earth‑observation and ISR missions, while L3Harris and Mercury Systems specialize in secure boot and cryptographic AI kernels. Smaller innovators such as Blue Canyon Technologies, Kratos Defense, and Teledyne provide lightweight AI modules for cubesats and rapid‑deployment platforms. The collective effort creates a diversified licensing landscape that supports both high‑value flagship programs and emerging small‑sat constellations.

List of Key AI Rad‑Hard By Design Companies Profiled

- Lockheed Martin

- Northrop Grumman

- Raytheon Technologies

- Boeing

- Maxar Technologies

- L3Harris Technologies

- Sierra Nevada Corporation

- Mercury Systems

- BAE Systems Inc.

- Leidos

- SpaceX

- Blue Canyon Technologies

- Kratos Defense & Security Solutions

- Teledyne Technologies

- General Dynamics Mission Systems

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Radiation‑hardened AI chips

|

| By Application |

|

On‑orbit autonomous navigation

|

| By End User |

|

U.S. Space Force

|

| By Mission Phase |

|

On‑orbit operations

|

| By Patenting Strategy |

|

Exclusive licensing

|

Regional Analysis: USA AI Rad-Hard By Design IP Licensing for National Security Space Market

The regulatory landscape emphasizes strict compliance with export controls and security classifications, while providing streamlined pathways for rad‑hard AI licensing. Agencies coordinate to align standards across defense, civilian, and commercial sectors, ensuring that intellectual property remains protected yet accessible for mission‑critical projects.

Prominent aerospace firms and emerging AI specialists drive innovation, often partnering with research institutions to co‑develop rad‑hard solutions. Their deep expertise in both AI algorithms and radiation tolerance positions them at the forefront of licensing negotiations and technology transfer.

Integration strategies focus on embedding AI directly into hardware resilient to space radiation, allowing autonomous decision‑making while maintaining system integrity. Collaborative testing environments validate performance under simulated orbital conditions.

The outlook anticipates deeper alignment between national security priorities and commercial innovation, fostering a robust pipeline of licensed AI rad‑hard technologies that support next‑generation space missions.

Europe

European nations are cultivating a collaborative framework for AI‑driven rad‑hard capabilities, leveraging joint research programs and cross‑border licensing agreements. Emphasis is placed on harmonizing standards to enable seamless technology exchange while safeguarding sovereign IP. Regional defense agencies prioritize resilient AI architectures that can withstand harsh space environments, encouraging partnerships between aerospace manufacturers and AI innovators.

Asia‑Pacific

The Asia‑Pacific region is accelerating its investment in secure AI technologies for space applications, driven by emerging national space programs and strategic security concerns. Countries are establishing dedicated licensing channels that balance intellectual property protection with rapid technology adoption, fostering an ecosystem where AI rad‑hard solutions can be quickly integrated into satellite constellations.

South America

South American markets are beginning to explore AI rad‑hard licensing as part of broader efforts to modernize their space capabilities. Collaborative initiatives with established aerospace hubs aim to transfer expertise and adapt resilient AI designs for regional satellite missions, emphasizing capacity building and secure technology sharing.

Middle East & Africa

In the Middle East and Africa, emerging space ambitions are prompting interest in AI‑enabled rad‑hard technologies. Nations are crafting licensing frameworks that protect emerging IP while encouraging partnerships with global AI specialists, seeking to embed resilient AI capabilities into their nascent satellite infrastructures.

Report Scope

This market research report provides a comprehensive analysis of the USA AI Rad-Hard By Design IP Licensing for National Security Space Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of USA AI Rad-Hard By Design IP Licensing for National Security Space Market?

-> USA AI rad‑hard by design IP licensing market is projected to grow from USD 0.48 billion in 2026 to USD 0.78 billion by 2034, exhibiting a CAGR of 6.5%

Which key companies operate in USA AI Rad-Hard By Design IP Licensing for National Security Space Market?

-> Key players include Lockheed Martin, Northrop Grumman, Raytheon Technologies, Boeing, and leading academic research labs that are actively developing rad‑hard AI patents.

What are the key growth drivers?

-> Key growth drivers include U.S. defense budget allocations exceeding USD 12 billion for resilient space capabilities, Space Development Agency licensing solicitations for low‑Earth‑orbit rad‑hard AI modules, and increasing demand for radiation‑tolerant AI to protect on‑orbit payloads.

Which region dominates the market?

-> North America leads the market, driven by substantial federal funding, a mature defense industrial base, and concentrated licensing activity.

What are the emerging trends?

-> Emerging trends include integration of proprietary AI algorithms within radiation‑hard semiconductor architectures, expanded public‑private patent collaborations, and the development of modular rad‑hard AI kits for rapid deployment in satellite constellations.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...