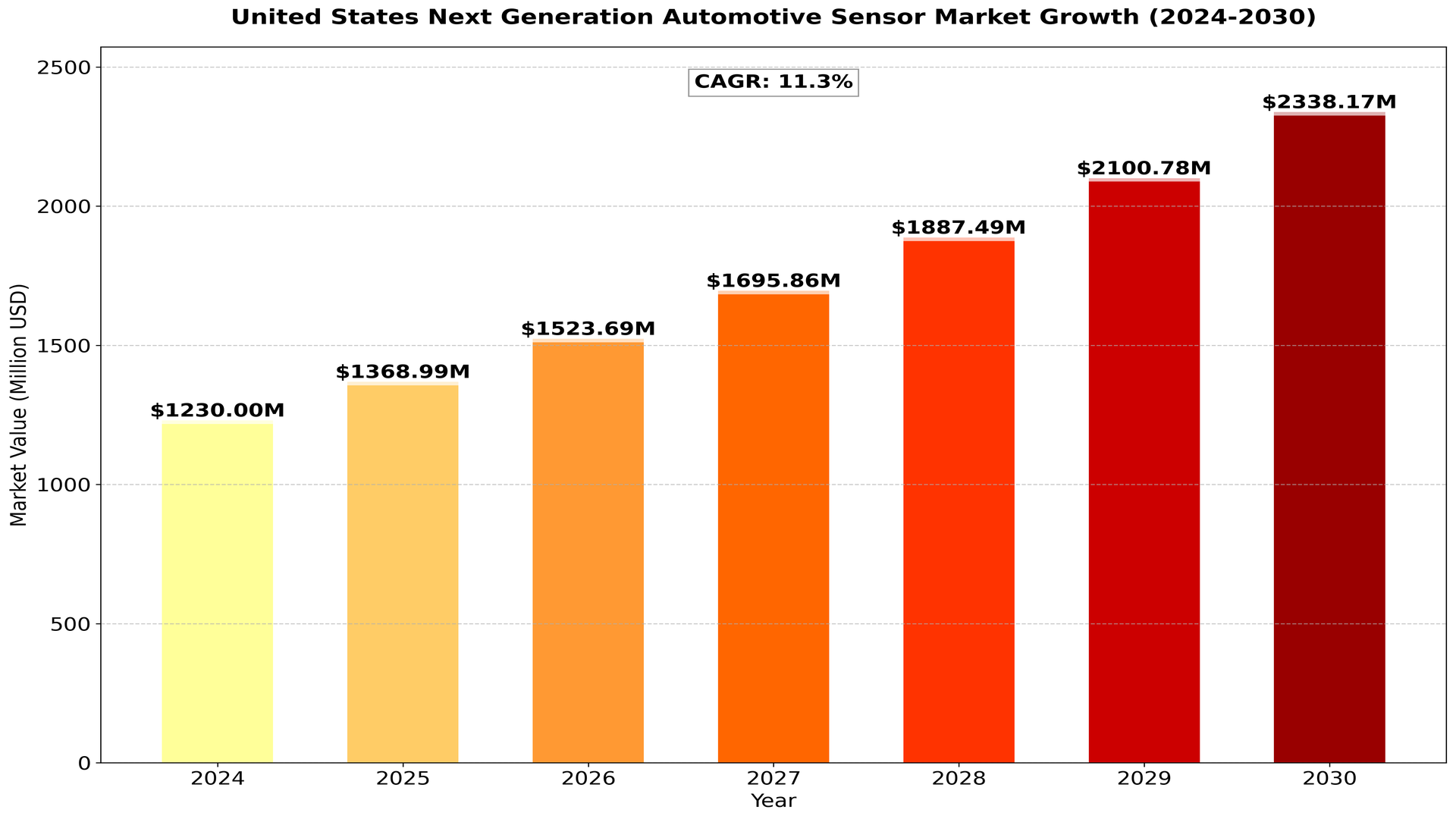

United States Next Generation Automotive Sensor market was valued at US$ 1.23 billion in 2024 and is projected to reach US$ 2.33 billion by 2030, at a CAGR of 11.3% during the forecast period 2024-2030.

Advanced sensors used in modern vehicles for improved safety, performance, and autonomous driving capabilities.

Strong growth driven by increasing adoption of ADAS and autonomous driving technologies. Rising demand for electric and connected vehicles boosting sensor requirements. Advancements in sensor fusion and AI improving overall vehicle intelligence.

This report contains market size and forecasts of Next Generation Automotive Sensor in United States, including the following market information:

• United States Next Generation Automotive Sensor Market Revenue, 2019-2024, 2024-2030, ($ millions)

• United States Next Generation Automotive Sensor Market Sales, 2019-2024, 2024-2030,

• United States Top five Next Generation Automotive Sensor companies in 2023 (%)

Report Includes

This report presents an overview of United States market for Next Generation Automotive Sensor , sales, revenue and price. Analyses of the United States market trends, with historic market revenue/sales data for 2019 – 2023, estimates for 2024, and projections of CAGR through 2030.

This report focuses on the Next Generation Automotive Sensor sales, revenue, market share and industry ranking of main manufacturers, data from 2019 to 2024. Identification of the major stakeholders in the United States Next Generation Automotive Sensor market, and analysis of their competitive landscape and market positioning based on recent developments and segmental revenues.

This report will help stakeholders to understand the competitive landscape and gain more insights and position their businesses and market strategies in a better way.

This report analyzes the segments data by Type, and by Sales Channels, sales, revenue, and price, from 2019 to 2030. Evaluation and forecast the market size for Humidifier sales, projected growth trends, production technology, sales channels and end-user industry.

Segment by Type

• Image Sensor

• Radar Sensor

• Other

Segment by Applications

• Power System

• Transmission System

• Chassis and Body Safety System

• Body Comfort System

Key Companies covered in this report:

• Texas Instruments

• Analog Devices, Inc.

• TE Connectivity

• Sensata Technologies

• Allegro Microsystems, LLC

• Littelfuse, Inc.

• Quanergy Systems, Inc.

• Velodyne Lidar, Inc.

• Aptiv

• Autoliv Inc.

Including or excluding key companies relevant to your analysis.

Competitor Analysis

The report also provides analysis of leading market participants including:

• Key companies Next Generation Automotive Sensor revenues in United Statesn market, 2019-2024 (Estimated), ($ millions)

• Key companies Next Generation Automotive Sensor revenues share in United Statesn market, 2023 (%)

• Key companies Next Generation Automotive Sensor sales in United Statesn market, 2019-2024 (Estimated),

• Key companies Next Generation Automotive Sensor sales share in United Statesn market, 2023 (%)

Drivers:

- Increased Demand for Advanced Driver Assistance Systems (ADAS): The rapid adoption of Advanced Driver Assistance Systems (ADAS) in vehicles, including lane departure warning, adaptive cruise control, and automatic emergency braking, has significantly boosted the demand for next-generation sensors. These systems rely on a complex network of sensors, such as cameras, radars, and LiDAR, to ensure driver safety and semi-autonomous driving.

- Rise of Electric and Autonomous Vehicles: The push towards electric vehicles (EVs) and fully autonomous driving is driving the need for high-precision, reliable sensors. Electric vehicles need advanced thermal management systems, battery monitoring, and collision avoidance, all of which rely heavily on sophisticated sensors to ensure smooth and safe operations.

- Government Regulations and Safety Standards: Stringent government regulations focusing on vehicle safety are pushing automakers to incorporate more advanced sensor technologies. For example, mandates from the National Highway Traffic Safety Administration (NHTSA) for incorporating automatic braking systems in vehicles have accelerated sensor demand.

- Technological Advancements in Sensor Technology: Recent breakthroughs in sensor miniaturization, increased sensitivity, and energy efficiency have made it possible for automotive manufacturers to integrate more sensors in vehicles without compromising space or power. This is particularly important for modern car designs, where space is often limited.

- Consumer Demand for Enhanced Safety and Comfort: Increasing consumer demand for features that enhance comfort, convenience, and safety is propelling the growth of the automotive sensor market. Advanced features such as 360-degree cameras, parking assistance, and blind-spot detection rely on sensor-driven technology.

Restraints:

- High Cost of Advanced Sensors: The integration of cutting-edge sensors such as LiDAR, radar, and ultrasonic sensors significantly increases the overall cost of vehicles. These high costs may deter widespread adoption in lower to mid-range vehicles, which could slow down the market’s growth.

- Complex Integration and Calibration: Advanced sensors require precise calibration and integration with the vehicle’s control systems. The complexity of integrating multiple sensors from various manufacturers into a seamless system poses a challenge to automakers and can delay product rollouts or increase development costs.

- Limited Infrastructure for Autonomous Vehicles: The full potential of next-generation automotive sensors, especially those supporting autonomous vehicles, cannot be realized without a robust supporting infrastructure. The slow pace of infrastructure development for autonomous driving in the U.S. may restrict the immediate expansion of this market segment.

- Data Privacy and Cybersecurity Concerns: The increasing connectivity of vehicles and the reliance on sensors to collect vast amounts of data have raised concerns over data privacy and cybersecurity risks. In a highly connected automotive ecosystem, the potential for hacking or data breaches could dampen consumer confidence and slow sensor adoption.

Opportunities:

- Expansion of Smart Cities and Vehicle-to-Everything (V2X) Communication: The rise of smart cities and the development of Vehicle-to-Everything (V2X) communication technologies present new growth avenues for next-generation automotive sensors. Sensors will play a key role in enabling real-time communication between vehicles, infrastructure, and other systems, improving safety and traffic management.

- Growth in Electric Vehicle Adoption: The growing trend towards electrification of vehicles presents significant opportunities for sensor manufacturers. Sensors that monitor battery performance, temperature, and charge levels are critical for ensuring the optimal functioning of electric vehicles.

- Development of 5G Technology: The widespread adoption of 5G technology will enhance the capabilities of next-gen sensors by enabling faster, more reliable data transmission. This will significantly benefit autonomous and semi-autonomous vehicle systems that rely on real-time data for decision-making and navigation.

- Increased Focus on Environmental Sustainability: As automakers focus on reducing emissions and creating more fuel-efficient vehicles, sensors that monitor emissions, fuel consumption, and engine performance are in high demand. This presents an opportunity for sensor manufacturers to provide eco-friendly solutions to support the automotive industry’s sustainability goals.

- Aftermarket Growth for Sensors: With the increasing complexity of modern vehicles, the aftermarket segment for automotive sensors is expected to grow. Vehicle owners will seek sensor replacements and upgrades, creating additional revenue streams for sensor manufacturers.

Challenges:

- Technical Limitations of Sensors: Despite advancements, current sensor technologies still face limitations in harsh environments, such as extreme weather conditions or at night. For instance, LiDAR systems can struggle in heavy rain, fog, or snow, affecting their reliability and performance. Overcoming these limitations is a significant challenge for the industry.

- Global Supply Chain Disruptions: The global automotive sensor supply chain has been impacted by various factors, including semiconductor shortages, trade restrictions, and geopolitical tensions. These disruptions have resulted in delayed production schedules and increased costs, posing a challenge for manufacturers.

- Consumer Hesitation Towards Autonomous Vehicles: While the technology for fully autonomous vehicles is progressing rapidly, consumer trust and acceptance of such vehicles remain a challenge. Concerns over safety, liability, and loss of control could slow the adoption of autonomous driving technology, affecting the demand for high-end sensors.

- Rapid Evolution of Technology: The fast-paced innovation in automotive sensor technology can make existing systems obsolete within a short period. This rapid evolution can be a challenge for both manufacturers and consumers, as they must continually invest in upgrades to stay relevant and competitive in the market.

Key Indicators Analysed

• Market Players & Competitor Analysis: The report covers the key players of the industry including Company Profile, Product Specifications, Production Capacity/Sales, Revenue, Price and Gross Margin 2019-2030 & Sales with a thorough analysis of the market’s competitive landscape and detailed information on vendors and comprehensive details of factors that will challenge the growth of major market vendors.

• United Statesn Market Analysis: The report includes United Statesn market status and outlook 2019-2030. Further the report provides break down details about each region & countries covered in the report. Identifying its sales, sales volume & revenue forecast. With detailed analysis by types and applications.

• Market Trends: Market key trends which include Increased Competition and Continuous Innovations.

• Opportunities and Drivers: Identifying the Growing Demands and New Technology

• Porters Five Force Analysis: The report provides with the state of competition in industry depending on five basic forces: threat of new entrants, bargaining power of suppliers, bargaining power of buyers, threat of substitute products or services, and existing industry rivalry.

Key Benefits of This Market Research:

• Industry drivers, restraints, and opportunities covered in the study

• Neutral perspective on the market performance

• Recent industry trends and developments

• Competitive landscape & strategies of key players

• Potential & niche segments and regions exhibiting promising growth covered

• Historical, current, and projected market size, in terms of value

• In-depth analysis of the Next Generation Automotive Sensor Market

• Overview of the regional outlook of the Next Generation Automotive Sensor Market

Key Reasons to Buy this Report:

• Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

• This enables you to anticipate market changes to remain ahead of your competitors

• You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations or other strategic documents

• The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

• Provision of market value (USD Billion) data for each segment and sub-segment

• Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

• Analysis by geography highlighting the consumption of the product/service in the region as well as indicating the factors that are affecting the market within each region

• Competitive landscape which incorporates the market ranking of the major players, along with new service/product launches, partnerships, business expansions, and acquisitions in the past five years of companies profiled

• Extensive company profiles comprising of company overview, company insights, product benchmarking, and SWOT analysis for the major market players

• The current as well as the future market outlook of the industry concerning recent developments which involve growth opportunities and drivers as well as challenges and restraints of both emerging as well as developed regions

• Includes in-depth analysis of the market from various perspectives through Porter’s five forces analysis

• Provides insight into the market through Value Chain

• Market dynamics scenario, along with growth opportunities of the market in the years to come

• 6-month post-sales analyst support

We offer additional regional and global reports that are similar:

• Global Next Generation Automotive Sensor Market

• United States Next Generation Automotive Sensor Market

• Japan Next Generation Automotive Sensor Market

• Germany Next Generation Automotive Sensor Market

• South Korea Next Generation Automotive Sensor Market

• Indonesia Next Generation Automotive Sensor Market

• Brazil Next Generation Automotive Sensor Market

Customization of the Report: In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are meet.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...