MARKET INSIGHTS

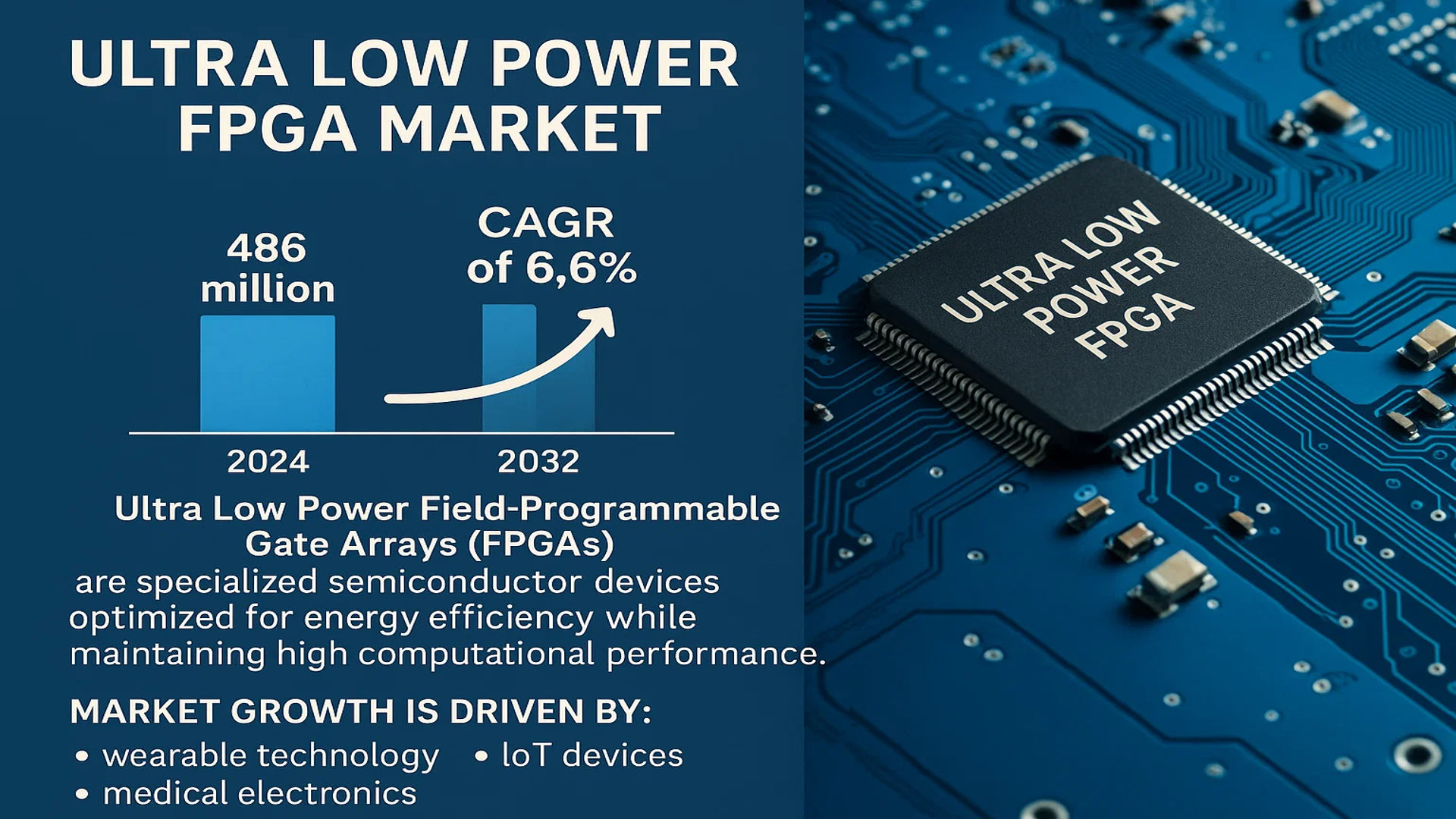

The global Ultra Low Power FPGA Market was valued at 486 million in 2024 and is projected to reach US$ 736 million by 2032, at a CAGR of 6.6% during the forecast period.

Ultra Low Power Field-Programmable Gate Arrays (FPGAs) are specialized semiconductor devices optimized for energy efficiency while maintaining high computational performance. These FPGAs leverage advanced fabrication processes, low-power architectures, and intelligent power management techniques to achieve significantly reduced power consumption compared to traditional FPGAs. Their compact form factor and ultra-low energy requirements make them particularly suitable for battery-powered applications where extended operation and space constraints are critical considerations.

The market growth is driven by increasing demand for energy-efficient computing solutions across industries such as wearable technology, IoT devices, and medical electronics. Recent technological advancements in FPGA architectures, particularly in 28nm and 22nm process nodes, have further enhanced their power efficiency. Key players like Lattice Semiconductor and Microchip Technology are actively expanding their ultra low power FPGA portfolios, with the top five manufacturers collectively holding a significant market share in 2024. The SRAM-based FPGA segment remains dominant, though flash-based alternatives are gaining traction in specific applications requiring lower standby power.

MARKET DYNAMICS

MARKET DRIVERS

Growing Adoption of IoT and Wearable Devices Fuels Demand for Ultra Low Power FPGAs

The rapid expansion of Internet of Things (IoT) applications and wearable technology is a primary driver for ultra low power FPGAs. Global IoT device connections surpassed 15 billion units in 2024 and are projected to double by 2030. These applications require energy-efficient processing solutions with minimal standby power consumption – precisely the strength of ultra low power FPGAs. Their ability to offer sophisticated processing capabilities while maintaining power budgets below 1 mW makes them indispensable for always-on edge computing applications. Recent product innovations from leading semiconductor companies focus on optimizing power-performance characteristics for IoT endpoint devices.

Advancements in Medical Electronics Drive Adoption in Healthcare Sector

The healthcare industry’s digital transformation significantly contributes to market growth, with medical devices accounting for over 25% of ultra low power FPGA applications. Portable diagnostic equipment, continuous patient monitoring systems, and implantable medical devices increasingly incorporate these chips due to their configurable nature and ultra-low power profiles. The global market for medical electronics is expected to reach $88 billion by 2026, creating substantial opportunities. Pharmaceutical companies are investing heavily in chip-enabled smart packaging solutions that leverage ultra low power FPGAs for temperature monitoring and authentication during drug distribution.

Additionally, the shift towards AI-enabled edge processing in industrial automation presents significant growth prospects.

➤ For instance, modern predictive maintenance systems in manufacturing plants now integrate ultra low power FPGAs to enable real-time vibration analysis while operating within strict power constraints of battery-powered sensors.

The combination of these growing application areas with continuous technological improvements in semiconductor fabrication ensures robust market expansion prospects.

MARKET RESTRAINTS

High Development Complexity Limits Widespread Adoption

While ultra low power FPGAs offer numerous technical benefits, their adoption faces significant barriers due to complex development requirements. Programming these devices demands specialized knowledge of hardware description languages like VHDL or Verilog, skills that are scarce compared to conventional software development expertise. Industry surveys suggest over 40% of embedded system projects experience delays due to FPGA programming challenges. This creates a substantial barrier to entry for small and medium enterprises that may lack resources for dedicated FPGA development teams.

Competition from Alternative Low-Power Solutions Constrains Market Growth

The market faces intensifying competition from application-specific integrated circuits (ASICs) and microcontrollers optimized for low-power operation. While FPGAs provide superior flexibility, ASICs offer better power efficiency at high volumes – making them preferable for mass-produced consumer devices. The microcontroller market has seen significant innovation with new devices integrating hardware accelerators while maintaining sub-100μA/MHz power consumption, directly competing with FPGA solutions for many battery-powered applications. This competitive landscape requires FPGA vendors to continuously improve their power efficiency while maintaining cost competitiveness.

MARKET CHALLENGES

Balancing Performance and Power Efficiency Remains Key Technical Hurdle

FPGA vendors face the persistent challenge of delivering increasingly complex functionality within strict power budgets. Each new process node brings power reduction opportunities but also introduces leakage current challenges. Advanced packaging techniques like 3D chip stacking, while reducing power consumption, significantly increase manufacturing complexity and cost. Achieving sub-10μW standby power while maintaining instant-on capabilities requires innovative architectural approaches that balance transistor characteristics with functional requirements.

Other Challenges

Supply Chain Volatility

The semiconductor industry’s ongoing supply chain disruptions impact FPGA availability and pricing. Specialty manufacturing equipment required for ultra low power FPGA production remains difficult to procure, with lead times exceeding 12 months for some critical tools.

Design Verification Complexities

Validating power consumption across all operational modes presents significant challenges during product development. Comprehensive power analysis requires sophisticated simulation tools and extensive test vectors that prolong development cycles and increase costs.

MARKET OPPORTUNITIES

Emerging AI at the Edge Applications Create New Growth Avenues

The proliferation of AI inference at edge devices represents a significant growth opportunity. Ultra low power FPGAs are well-positioned to enable machine learning applications in power-constrained environments, with the edge AI chip market projected to exceed $30 billion by 2030. Their reconfigurable nature allows for efficient implementation of evolving neural network architectures while meeting stringent power budgets. Recent innovations in FPGA-based AI accelerators demonstrate 10-100x improvements in performance-per-watt compared to traditional microcontroller implementations for common machine learning workloads.

Automotive Electronics Transition Creates Significant Potential

The automotive industry’s shift towards electrification and autonomous systems requires new computing architectures that ultra low power FPGAs can effectively address. Advanced driver assistance systems (ADAS) in electric vehicles particularly benefit from the combination of deterministic performance and power efficiency that these devices offer. With the automotive semiconductor market expected to grow at 8% CAGR through 2030, FPGA vendors are developing automotive-grade solutions meeting stringent reliability requirements while delivering the low power consumption needed for ever-more sophisticated vehicle electronics.

ULTRA LOW POWER FPGA MARKET TRENDS

Growing Demand for Energy-Efficient Solutions Drives Market Expansion

The global Ultra Low Power FPGA market, valued at $486 million in 2024, is projected to reach $736 million by 2032, growing at a CAGR of 6.6% over the forecast period. One of the most prominent trends driving this growth is the rising need for energy-efficient semiconductor solutions in battery-powered and portable applications. Ultra Low Power FPGAs are being increasingly adopted in wearable technology, IoT devices, and medical implants, where minimizing power consumption is critical. These FPGAs leverage advanced fabrication processes like FinFET technology and 28nm or smaller nodes, enabling significant reductions in leakage currents while maintaining high performance.

Other Trends

Rise of IoT and Edge Computing

The proliferation of IoT devices and edge computing applications has amplified the demand for ultra-low-power programmable logic. With an estimated 30 billion IoT devices expected in operation by 2030, Ultra Low Power FPGAs are becoming indispensable for real-time data processing at the edge, while reducing reliance on cloud-based computing. These FPGAs enable sensor nodes, smart gateways, and wearable devices to operate longer on small batteries while still delivering high computational efficiency. Manufacturers are now integrating machine learning accelerators within these FPGAs to support AI-driven edge applications without compromising power budgets.

Advancements in Embedded and Medical Applications

Ultra Low Power FPGAs are gaining traction in medical devices, particularly in implantable and portable diagnostic equipment where power efficiency and reliability are paramount. The medical electronics sector is expected to contribute over 20% of FPGA market demand by 2030, driven by applications like heart rate monitors, glucose sensors, and neural prosthetics. Additionally, the automotive sector is leveraging these FPGAs for advanced driver-assistance systems (ADAS) and in-vehicle infotainment systems that require low-power processing. Leading manufacturers such as Lattice Semiconductor and Microchip Technology are focusing on enhancing power optimization techniques to cater to these high-growth segments.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Investments Drive Market Leadership in Ultra Low Power FPGA Space

The global Ultra Low Power FPGA market is characterized by dynamic competition among established semiconductor companies and emerging innovators. Lattice Semiconductor dominates the market with approximately 30% revenue share in 2024, attributed to its comprehensive portfolio of ultra-efficient FPGA solutions and strong focus on edge computing applications. Their recent acquisition of specialized fabless design teams has further strengthened their position in low-power architectures.

Microchip Technology and Renesas Electronics follow closely, collectively holding about 35% of the market share. Their success stems from vertical integration strategies, combining FPGA technology with microcontroller units (MCUs) to create energy-optimized system-on-chip solutions. Both companies have made significant R&D investments in 65nm and 40nm FPGA process technologies specifically tailored for ultra-low-power applications.

The competitive intensity is increasing as companies expand into high-growth application segments like IoT edge devices and wearable health monitors. QuickLogic Corporation has differentiated itself through patented “Flexible Fusion Engine” technology, achieving 50% power consumption reductions compared to conventional FPGAs in similar process nodes.

Emerging challengers like Gowin Semiconductor and Efinix Inc are disrupting the market with innovative FPGA architectures. Gowin’s “LittleBee” series has gained traction in the Asian market for consumer electronics, while Efinix’s Quantum architecture demonstrates how architectural innovations can achieve power efficiency without compromising performance.

List of Leading Ultra Low Power FPGA Manufacturers

- Lattice Semiconductor (U.S.)

- Microchip Technology (U.S.)

- Renesas Electronics (Japan)

- QuickLogic Corporation (U.S.)

- Gowin Semiconductor (China)

- AMD (U.S.)

- Efinix Inc (U.S.)

- Enclustra GmbH (Switzerland)

Segment Analysis:

By Type

SRAM-Based FPGAs Segment Leads the Market Due to High Performance and Reconfigurability

The market is segmented based on type into:

- SRAM-Based FPGAs

- Subtypes: Low-density, Mid-density, and High-density FPGAs

- Flash-Based FPGAs

- Subtypes: Single-chip and Multi-chip solutions

- Others

By Application

IoT Devices Segment Dominates Due to Rising Demand for Edge Computing Solutions

The market is segmented based on application into:

- Wearable Technology

- IoT Devices

- Medical Devices

- Consumer Electronics

- Others

By Configuration

Low-Density FPGAs Segment Gains Popularity for Power-Sensitive Applications

The market is segmented based on configuration into:

- Low-Density FPGAs

- Mid-Density FPGAs

- High-Density FPGAs

By Power Consumption

Ultra Low Power Segment Leads Owing to Demand for Battery-Powered Devices

The market is segmented based on power consumption into:

- Ultra Low Power (sub-100mW)

- Low Power (100mW-1W)

- Medium Power (1W-5W)

Regional Analysis: Ultra Low Power FPGA Market

Asia-Pacific

The Asia-Pacific region dominates the Ultra Low Power FPGA market, driven by China, Japan, and South Korea’s thriving semiconductor industries. China’s aggressive investments in IoT and AI applications, coupled with a surge in consumer electronics manufacturing, fuel demand for energy-efficient FPGAs. Japan contributes with innovations in wearables and medical devices, while South Korea’s advanced 5G infrastructure boosts adoption rates. India is emerging as a key player due to rising domestic IoT adoption and smart device production. Despite cost sensitivity favoring traditional solutions, the shift toward energy efficiency in densely populated urban areas is accelerating ultra low power FPGA adoption across the region.

North America

North America leads in technological innovation, with the U.S. accounting for over 40% of global ultra low power FPGA R&D expenditure. The region’s focus on military, aerospace, and medical applications demands highly reliable, low-power silicon solutions. Key players like Lattice Semiconductor and Microchip Technology drive advancements in SRAM-based FPGA architectures. Strict power consumption regulations for electronics and expansive 5G network rollouts further propel market growth. Canada’s growing healthcare IoT sector and Mexico’s expanding automotive electronics manufacturing provide additional demand drivers, though supply chain dependencies pose intermittent challenges.

Europe

European markets prioritize ultra low power FPGAs for industrial automation and automotive applications, with Germany and France leading adoption. The EU’s stringent energy efficiency directives (Ecodesign 2021) mandate low-power components in consumer electronics, creating sustained demand. The region excels in flash-based FPGA innovation, particularly for harsh environment applications. While Brexit introduced temporary supply chain complexities, the U.K. maintains strong design capabilities in medical and defense sectors. Nordic countries contribute significantly through FPGA applications in energy harvesting and wireless sensor networks, though market growth faces occasional constraints from semiconductor import dependencies.

South America

South America presents a developing market with Brazil and Argentina showing gradual adoption of ultra low power FPGAs, primarily in agricultural IoT and oil/gas monitoring systems. Economic volatility and limited domestic semiconductor production capacity hinder widespread deployment, creating reliance on imports. However, increasing smart city initiatives in major urban centers and government-backed technology modernization programs are driving cautious market expansion. The region’s unique requirements for rugged, low-maintenance electronics in remote locations offer niche opportunities for tailored FPGA solutions.

Middle East & Africa

This emerging market demonstrates growing interest in ultra low power FPGAs for telecommunications infrastructure and oilfield monitoring applications. Israel’s thriving tech sector contributes FPGA innovations in defense and cybersecurity, while UAE’s smart city projects create demand for efficient edge computing solutions. The region faces challenges from limited technical expertise and high import costs, but strategic investments in 5G networks and renewable energy systems are establishing foundations for future FPGA adoption. Africa’s mobile payment revolution and distributed healthcare solutions present long-term growth opportunities despite current infrastructure limitations.

Report Scope

This market research report provides a comprehensive analysis of the global Ultra Low Power FPGA market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Ultra Low Power FPGA market was valued at USD 486 million in 2024 and is projected to reach USD 736 million by 2032, growing at a CAGR of 6.6%.

- Segmentation Analysis: Detailed breakdown by product type (SRAM-Based FPGAs, Flash-Based FPGAs, Others), application (Wearable Technology, IoT Devices, Medical Devices, Consumer Electronics), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America (U.S., Canada, Mexico), Europe (Germany, France, U.K.), Asia-Pacific (China, Japan, South Korea), and other key regions, including country-level analysis.

- Competitive Landscape: Profiles of leading market participants including Lattice Semiconductor, Microchip Technology, QuickLogic Corporation, Renesas Electronics, and Gowin Semiconductor, covering their product portfolios, R&D investments, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging low-power architectures, integration with AI/ML algorithms, advanced fabrication nodes (28nm and below), and power optimization techniques.

- Market Drivers & Restraints: Evaluation of factors such as growing IoT adoption, demand for energy-efficient electronics, and challenges like design complexity and high development costs.

- Stakeholder Analysis: Strategic insights for semiconductor manufacturers, system integrators, OEMs, and investors regarding market opportunities and technological advancements.

The research methodology combines primary interviews with industry experts and secondary data from verified sources to ensure accuracy and reliability of market insights.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Ultra Low Power FPGA Market?

-> Ultra Low Power FPGA Market was valued at 486 million in 2024 and is projected to reach US$ 736 million by 2032, at a CAGR of 6.6% during the forecast period.

Which key companies operate in Global Ultra Low Power FPGA Market?

-> Key players include Lattice Semiconductor, Microchip Technology, QuickLogic Corporation, Renesas Electronics, and Gowin Semiconductor, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for energy-efficient electronics, growth in IoT applications, and increasing adoption in wearable devices.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region due to electronics manufacturing growth, while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include integration with AI accelerators, development of sub-28nm FPGAs, and increasing adoption in edge computing applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...