MARKET INSIGHTS

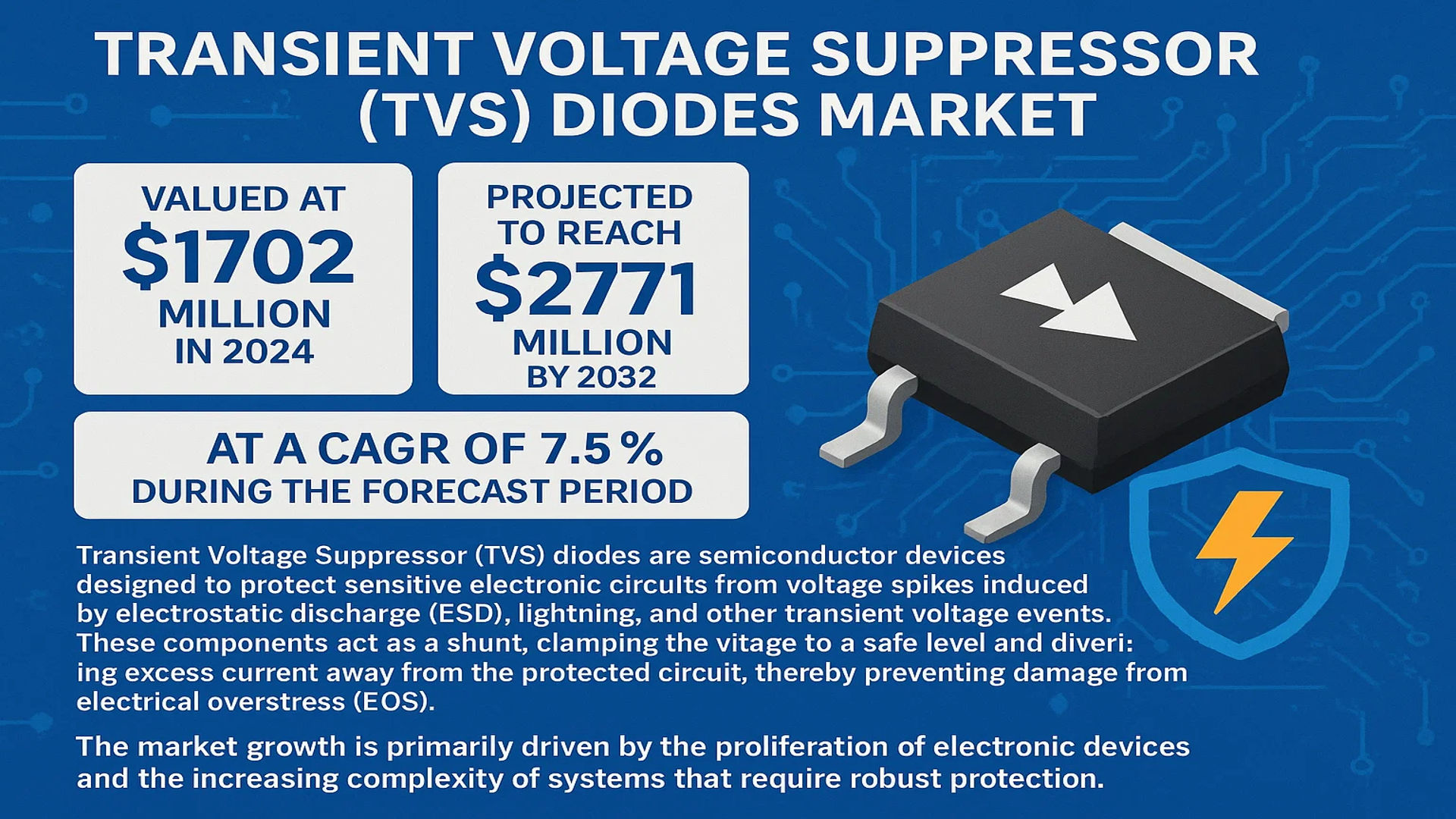

The global Transient Voltage Suppressor (TVS) Diodes Market was valued at 1702 million in 2024 and is projected to reach US$ 2771 million by 2032, at a CAGR of 7.5% during the forecast period.

Transient Voltage Suppressor (TVS) diodes are semiconductor devices designed to protect sensitive electronic circuits from voltage spikes induced by electrostatic discharge (ESD), lightning, and other transient voltage events. These components act as a shunt, clamping the voltage to a safe level and diverting excess current away from the protected circuit, thereby preventing damage from electrical overstress (EOS).

The market growth is primarily driven by the proliferation of electronic devices and the increasing complexity of systems that require robust protection. The surge in Internet of Things (IoT) deployments, which are inherently susceptible to ESD, is a significant contributor. Furthermore, stringent safety regulations across industries like automotive and telecommunications mandate the use of TVS diodes. Recent developments include a trend towards miniaturization and the integration of protection solutions, with key players like Littelfuse, Infineon, and ON Semiconductor leading innovation in low-capacitance and high-speed TVS diodes for 5G and automotive applications.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of IoT Devices and Connected Electronics to Drive Market Expansion

The exponential growth of Internet of Things (IoT) devices is significantly driving the TVS diode market, as these connected electronics are inherently vulnerable to electrostatic discharge (ESD) and electrical overstress events. The global IoT market is projected to exceed 29 billion active devices by 2030, creating substantial demand for robust circuit protection solutions. TVS diodes provide critical protection against voltage transients that can damage sensitive semiconductor components in IoT sensors, smart home devices, and industrial automation systems. The increasing deployment of 5G networks, which enables massive machine-type communications, further amplifies this demand as more devices become interconnected and require reliable protection mechanisms. This technological evolution creates a sustained growth trajectory for TVS diodes across multiple application segments.

Stringent Safety Regulations and Standards Compliance to Accelerate Adoption

Increasing regulatory requirements across various industries are compelling manufacturers to incorporate TVS diodes into their electronic designs. Automotive safety standards such as ISO 7637-2 and ISO 16750-2 mandate robust protection against electrical transients in vehicle electronics, particularly with the rise of electric and autonomous vehicles. Similarly, industrial equipment must comply with IEC 61000-4-2 and IEC 61000-4-5 standards for ESD and surge immunity. The telecommunications industry faces requirements from standards such as ITU-T K.20 and K.21 for lightning and surge protection. These regulatory frameworks create a non-negotiable market driver, as electronic system manufacturers must integrate TVS protection to meet certification requirements and ensure product reliability in harsh operating environments.

Advancements in Wireless Communication Technologies to Fuel Market Growth

The rapid evolution of wireless communication technologies, including 5G infrastructure, Wi-Fi 6/6E, and Bluetooth Low Energy, is creating substantial opportunities for TVS diode manufacturers. These high-frequency communication systems are particularly susceptible to electromagnetic interference and voltage transients that can degrade signal integrity and cause system failures. The global deployment of 5G base stations is expected to reach nearly 7 million units by 2025, each requiring multiple TVS diodes for protection. Additionally, the increasing data transmission speeds in modern communication protocols necessitate TVS diodes with lower capacitance values to minimize signal distortion while providing effective transient voltage suppression. This technological progression drives continuous innovation and demand in the TVS diode market.

MARKET CHALLENGES

Intense Price Competition and Margin Pressure to Challenge Market Sustainability

The TVS diode market faces significant challenges from intense price competition, particularly from Asian manufacturers who have achieved substantial economies of scale. The average selling price of standard TVS diodes has declined by approximately 15-20% over the past three years, putting pressure on profit margins across the industry. This price erosion is particularly pronounced in consumer electronics applications, where cost sensitivity is extreme. Manufacturers must balance the need for high-reliability components with aggressive cost reduction targets, creating a challenging environment for maintaining quality standards while remaining competitive. The situation is further complicated by fluctuating raw material costs and increasing manufacturing expenses, forcing companies to optimize their production processes and supply chain management continuously.

Other Challenges

Technical Performance Limitations

Developing TVS diodes that meet the increasingly demanding requirements of modern electronic systems presents significant technical challenges. As operating frequencies exceed 10 GHz in 5G applications, TVS diodes must provide effective protection while maintaining capacitance values below 0.5 pF to avoid signal degradation. Simultaneously, breakdown voltages must be precisely controlled within narrow tolerances to protect sensitive integrated circuits. Achieving these conflicting performance parameters requires advanced semiconductor processing techniques and innovative packaging solutions, increasing development costs and time-to-market for new products.

Supply Chain Vulnerabilities

The global semiconductor supply chain disruptions experienced in recent years have highlighted vulnerabilities in the TVS diode market. Dependence on specialized raw materials, including silicon wafers and precious metals for packaging, creates exposure to price volatility and availability constraints. The industry-wide shortage of semiconductor fabrication capacity has affected TVS diode production, leading to extended lead times and allocation situations. These supply chain challenges complicate production planning and inventory management for both manufacturers and their customers.

MARKET RESTRAINTS

Technical Complexity in High-Frequency Applications to Limit Market Penetration

The increasing operating frequencies of modern electronic systems present significant technical challenges for TVS diode implementation. In high-speed data communication applications exceeding 10 Gbps, the parasitic capacitance of TVS diodes can cause signal integrity issues, including rise time degradation and increased bit error rates. This technical constraint limits the adoption of traditional TVS solutions in cutting-edge applications such as 400 Gigabit Ethernet, PCI Express 5.0, and emerging memory interfaces. Manufacturers must develop innovative solutions with ultra-low capacitance characteristics while maintaining robust clamping performance, requiring substantial research and development investments. This technical barrier restrains market growth in the most advanced electronic segments until appropriate solutions become commercially viable and cost-effective.

Design Integration Challenges and Space Constraints to Hinder Adoption

The ongoing miniaturization of electronic devices creates significant integration challenges for TVS diode implementation. With printed circuit board real estate becoming increasingly precious, designers often face difficult trade-offs between protection level and available space. The trend toward system-in-package and chip-scale packaging approaches further complicates the integration of discrete TVS components. Additionally, the thermal management requirements of TVS diodes in high-energy transient conditions conflict with the desire for smaller form factors. These design constraints frequently lead engineers to consider alternative protection strategies or compromise on protection levels, particularly in space-constrained applications such as mobile devices, wearables, and ultra-compact IoT sensors.

Limited Awareness and Understanding Among Design Engineers to Slow Market Growth

Despite the critical importance of circuit protection, many design engineers lack comprehensive understanding of TVS diode selection and implementation principles. This knowledge gap often leads to suboptimal protection schemes or complete omission of transient voltage protection in electronic designs. The complexity of TVS diode parameters, including breakdown voltage, clamping voltage, peak pulse power, and capacitance, creates confusion among designers who may prioritize more familiar components. Educational initiatives and application support from manufacturers help address this issue, but the learning curve remains steep, particularly for engineers working on their first designs in sensitive applications. This awareness challenge restrains market growth by delaying the adoption of proper protection methodologies across the electronics industry.

MARKET OPPORTUNITIES

Emerging Electric Vehicle and Automotive Electronics Revolution to Create Substantial Growth Opportunities

The rapid transformation of the automotive industry toward electrification and autonomous driving presents unprecedented opportunities for TVS diode manufacturers. Modern vehicles incorporate hundreds of electronic control units and sensors that require robust protection against voltage transients from various sources, including load dump, alternator field decay, and inductive load switching. The increasing adoption of advanced driver assistance systems (ADAS), in-vehicle networking, and electric powertrain components drives demand for high-reliability TVS solutions. With the global electric vehicle market projected to grow at a compound annual growth rate exceeding 25% through 2030, the automotive segment represents one of the most promising growth avenues for TVS diode suppliers seeking to capitalize on this technological transformation.

Expansion of Renewable Energy Infrastructure to Drive Demand for High-Power TVS Solutions

The global transition toward renewable energy sources creates significant opportunities for high-power TVS diodes in solar inverters, wind turbine controllers, and energy storage systems. These applications require robust protection against lightning-induced surges and switching transients that can damage expensive power electronics components. The increasing installation of solar photovoltaic systems, expected to reach over 2 terawatts of global capacity by 2030, drives demand for TVS diodes capable of handling high energy transients while withstanding harsh environmental conditions. Similarly, the growing adoption of energy storage systems for grid stabilization and backup power applications creates additional opportunities for TVS protection in battery management systems and power conversion equipment.

Development of Advanced Packaging and Integration Technologies to Enable New Applications

Innovations in semiconductor packaging technologies create opportunities for TVS diode integration into multi-chip modules and system-in-package solutions. The development of embedded TVS structures within integrated circuits and advanced packaging approaches allows for more compact and efficient protection schemes. These technological advancements enable TVS diode implementation in applications where discrete components were previously impractical, including radio-frequency front-end modules, high-speed serial interfaces, and advanced sensor arrays. The ongoing miniaturization trend in electronics, coupled with these packaging innovations, opens new market segments for TVS protection that were previously inaccessible due to size and performance constraints.

TRANSIENT VOLTAGE SUPPRESSOR (TVS) DIODES MARKET TRENDS

Proliferation of IoT and Connected Devices to Emerge as a Dominant Trend

The unprecedented proliferation of Internet of Things (IoT) devices is a primary catalyst driving the global TVS diode market. Billions of new connected endpoints, from industrial sensors to consumer wearables, are being deployed annually, each requiring robust protection against electrostatic discharge (ESD) and electrical overstress (EOS). These devices are inherently vulnerable due to their frequent interaction with the external environment and users, making integrated circuit protection not just an enhancement but a fundamental design requirement. The automotive sector, a major adopter of IoT for applications like telematics and advanced driver-assistance systems (ADAS), further amplifies this demand. This trend is fundamentally reshaping product development strategies, with manufacturers now prioritizing ultra-low capacitance TVS diodes that can protect high-speed data lines without compromising signal integrity in 5G and high-frequency applications.

Other Trends

Miniaturization and Integration

The relentless drive towards smaller, more powerful electronics is compelling a parallel trend in TVS diode technology: miniaturization. There is a growing demand for chip-scale packages and surface-mount devices (SMDs) that occupy minimal board space while offering superior performance. This is particularly critical in applications like smartphones, where board real estate is at a premium. Furthermore, the market is witnessing a significant shift towards integrated protection solutions. Instead of using discrete components, designers are increasingly adopting multi-channel array devices that combine several TVS diodes into a single package, often integrating additional features like EMI filtering. This approach simplifies board layout, reduces the bill of materials, and enhances overall system reliability, making it highly attractive for high-volume consumer electronics and automotive applications.

Advancements in Material Science and High-Speed Applications

Material innovation is a key frontier for TVS diode performance, directly addressing the needs of next-generation electronics. While silicon-based devices remain the workhorse of the industry, developments in wide-bandgap semiconductors are gaining traction for specialized, high-power applications. However, the most impactful advancements are occurring within silicon technology itself, leading to devices with remarkably lower clamping voltages and reduced leakage currents. This evolution is crucial for protecting the increasingly sensitive and low-voltage semiconductors found in modern computing and communication infrastructure. Concurrently, the rollout of 5G networks and the adoption of high-speed data interfaces like USB4 and HDMI 2.1 are creating a substantial market for TVS diodes engineered specifically for high-frequency operation. These specialized diodes feature ultra-low capacitance, often below 0.5pF, to prevent signal degradation and ensure data integrity at multi-gigabit speeds, which is a non-negotiable requirement in telecommunications and data centers.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Focus on Product Innovation and Global Expansion Drives Competition

The global Transient Voltage Suppressor (TVS) Diodes market exhibits a semi-consolidated structure, characterized by the presence of several established multinational corporations alongside numerous specialized regional manufacturers. This dynamic creates a competitive environment where technological leadership, manufacturing scale, and strategic market positioning are paramount. The market’s growth, projected at a CAGR of 7.5% through 2032, is intensifying competition as companies vie for a larger share of this high-value segment.

Littelfuse, Inc. is widely recognized as a dominant force in the global TVS diode landscape. Its leadership is anchored in a comprehensive and technologically advanced product portfolio that caters to a vast array of applications, from automotive electronics to industrial equipment. The company’s significant investment in research and development has yielded innovative solutions, such as ultra-low capacitance diodes for high-speed data lines, solidifying its position across North America, Europe, and Asia-Pacific. Similarly, Vishay Intertechnology, Inc. and Infineon Technologies AG command substantial market share. Their strength is derived from deep vertical integration, extensive patent libraries, and a strong focus on the automotive and telecommunications sectors, which are among the largest consumers of TVS protection solutions.

These leading players are not merely resting on their laurels; they are actively pursuing growth through aggressive strategies. This includes geographical expansion into emerging markets with growing electronics manufacturing, as well as a continuous pipeline of new product launches designed to meet evolving demands for miniaturization and higher performance. For instance, recent developments have focused on developing TVS arrays in compact packages to protect multiple lines in space-constrained IoT devices.

Meanwhile, other significant participants like ON Semiconductor and STMicroelectronics are strengthening their market presence through substantial investments in expanding production capacity and forming strategic partnerships with major OEMs. Their strategy often involves offering integrated protection solutions that combine TVS diodes with other circuit protection components, providing added value and system-level reliability to customers. This focus on providing complete solutions, rather than just discrete components, is a key differentiator in the current competitive climate.

List of Key Transient Voltage Suppressor (TVS) Diodes Companies Profiled

- Littelfuse, Inc. (U.S.)

- Vishay Intertechnology, Inc. (U.S.)

- Infineon Technologies AG (Germany)

- ON Semiconductor (U.S.)

- STMicroelectronics N.V. (Switzerland)

- Nexperia (Netherlands)

- SEMTECH Corporation (U.S.)

- Bourns, Inc. (U.S.)

- Diodes Incorporated (U.S.)

- Toshiba Electronic Devices & Storage Corporation (Japan)

- PROTEK Devices (U.S.)

- WAYON Electronic Co., Ltd. (China)

Segment Analysis:

By Type

Uni-polar TVS Segment Dominates the Market Due to Widespread Use in DC Circuit Protection

The market is segmented based on type into:

- Uni-polar TVS

- Bi-polar TVS

By Application

Automotive Segment Leads Due to Critical Need for ESD Protection in Vehicle Electronics

The market is segmented based on application into:

- Automotive

- Industrial

- Power Supplies

- Military/Aerospace

- Telecommunication

- Computing

- Consumer Goods

- Others

By Technology

Surface Mount Technology Gains Traction Due to Miniaturization Trends in Electronics

The market is segmented based on technology into:

- Surface Mount Devices (SMD)

- Through-Hole Devices (THD)

By Power Rating

Low Power Segment Holds Significant Share Due to High Volume Consumer Electronics Demand

The market is segmented based on power rating into:

- Low Power TVS Diodes

- Medium Power TVS Diodes

- High Power TVS Diodes

Regional Analysis: Transient Voltage Suppressor (TVS) Diodes Market

Asia-Pacific

The Asia-Pacific region is the dominant force in the global TVS diode market, accounting for the largest revenue share, estimated at over 45% in 2024. This leadership is driven by its position as the world’s primary electronics manufacturing hub. China, South Korea, Japan, and Taiwan are home to a dense ecosystem of consumer electronics brands, telecommunications equipment manufacturers, and automotive electronics suppliers. The proliferation of IoT devices, the aggressive rollout of 5G infrastructure, and the massive production of smartphones and computing hardware create immense, sustained demand for circuit protection components. While cost-competitiveness is a key purchasing factor, leading manufacturers in the region are also at the forefront of innovation, developing miniaturized and high-performance TVS diodes to meet the requirements of next-generation compact and high-speed devices.

North America

North America represents a highly advanced and mature market for TVS diodes, characterized by stringent regulatory standards and a strong emphasis on high-reliability applications. The automotive sector is a significant driver, with the integration of advanced driver-assistance systems (ADAS) and in-vehicle networking requiring robust protection against ESD and electrical transients. Furthermore, the region’s substantial investments in aerospace, defense, and data center infrastructure necessitate components that meet rigorous performance and quality certifications. The presence of major semiconductor companies and a thriving startup culture focused on electric vehicles and industrial IoT ensures a continuous demand for both standard and custom TVS solutions, with a focus on integrated protection modules.

Europe

The European market is propelled by its strong industrial and automotive manufacturing base, particularly in Germany, France, and Italy. Strict EU directives on electromagnetic compatibility (EMC) and product safety compel OEMs to incorporate effective transient voltage protection into their designs. The region’s push towards Industry 4.0 and smart automation is increasing the deployment of sensitive industrial control systems and sensors, all of which require protection. The automotive industry’s transition to electric vehicles (EVs) is a particularly potent growth driver, as EV power management and charging systems are highly susceptible to voltage spikes. Innovation is focused on developing TVS diodes with low clamping voltages and minimal leakage currents to protect increasingly sensitive semiconductors.

South America

The South American market for TVS diodes is in a developing phase, with growth primarily tied to the expansion of telecommunications networks and the increasing local assembly of consumer electronics and automobiles. Brazil and Argentina are the key markets in the region. However, economic volatility and inconsistent regulatory enforcement can lead to a higher prevalence of lower-cost, often less reliable, electronic components. This price sensitivity can sometimes hinder the widespread adoption of premium, high-performance TVS diodes. Nonetheless, as infrastructure modernizes and consumer demand for reliable electronics grows, the market for quality circuit protection is expected to gradually increase.

Middle East & Africa

This region presents an emerging opportunity for the TVS diode market, though its development is uneven. Growth is concentrated in Gulf Cooperation Council (GCC) nations like Saudi Arabia and the UAE, where investments in smart city projects, telecommunications, and oil & gas infrastructure are creating demand for robust electronic systems. The need for protection against power surges and lightning strikes in these applications is critical. However, across much of Africa, market development is constrained by limited local electronics manufacturing, economic challenges, and less developed supply chains. The long-term potential is tied to broader economic development and infrastructure investment across the continent.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Semiconductor and Electronics markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Transient Voltage Suppressor (TVS) Diodes Market?

-> Transient Voltage Suppressor (TVS) Diodes Market was valued at 1702 million in 2024 and is projected to reach US$ 2771 million by 2032, at a CAGR of 7.5% during the forecast period.

Which key companies operate in Global Transient Voltage Suppressor (TVS) Diodes Market?

-> Key players include Infineon, Nexperia, SEMTECH, Vishay, Littelfuse, STMicroelectronics, ON Semiconductor, Bourns, TOSHIBA, and Diodes Inc., among others.

What are the key growth drivers?

-> Key growth drivers include proliferation of IoT devices, stringent safety regulations, increasing adoption of wireless communication technologies, and rising demand for electronic protection in automotive and industrial applications.

Which region dominates the market?

-> Asia-Pacific is the dominant market, accounting for over 45% of global revenue in 2024, driven by strong electronics manufacturing in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include miniaturization of components, development of high-speed low-capacitance TVS diodes, integration with other protection components, and material innovations for enhanced performance.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...