MARKET INSIGHTS

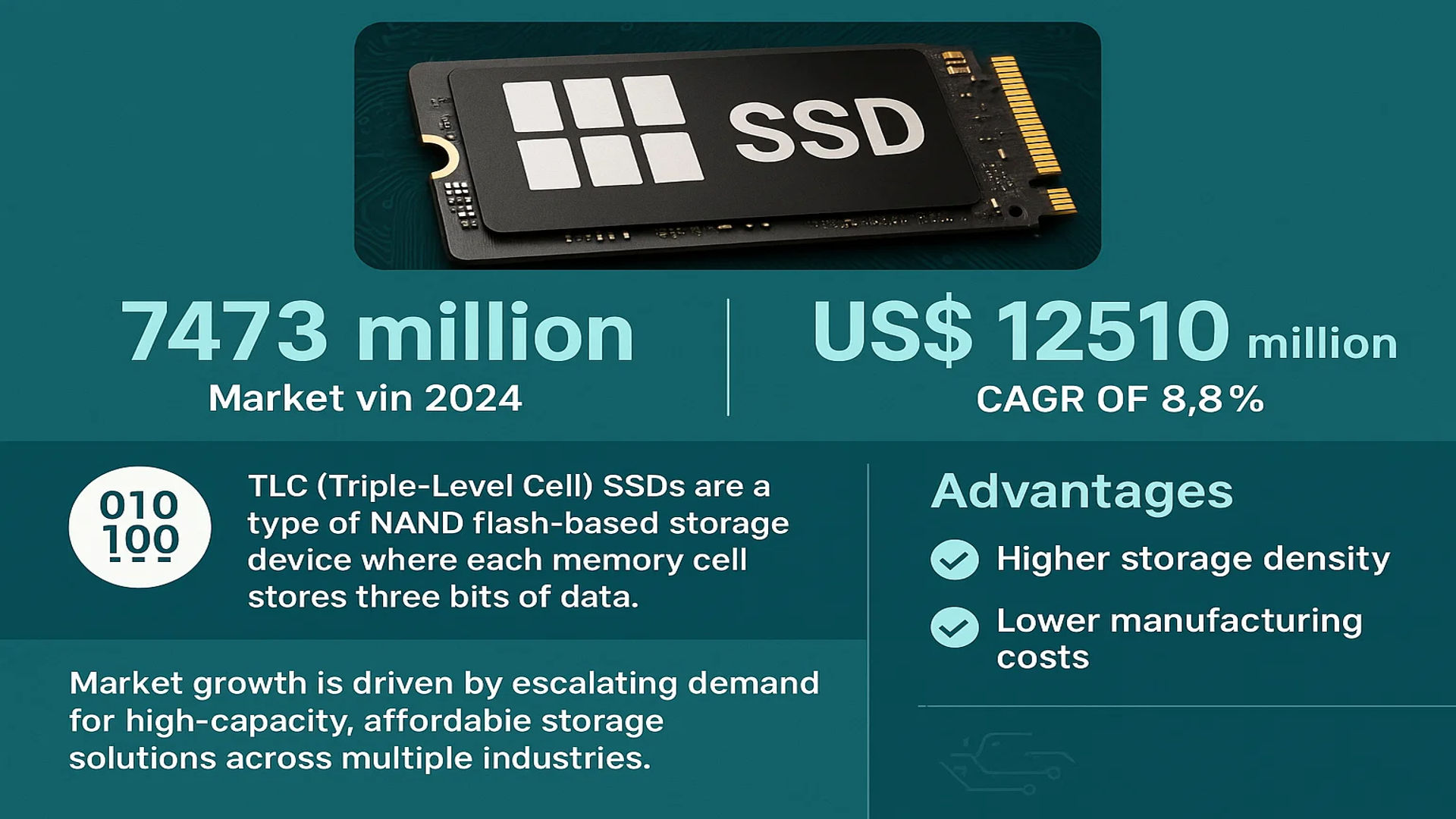

The global TLC SSD Market was valued at 7473 million in 2024 and is projected to reach US$ 12510 million by 2032, at a CAGR of 8.8% during the forecast period.

TLC (Triple-Level Cell) SSDs are a type of NAND flash-based storage device where each memory cell stores three bits of data. This technology offers a balance between cost efficiency and performance, making it ideal for consumer electronics, data centers, and enterprise applications. While TLC SSDs provide higher storage density and lower manufacturing costs compared to SLC (Single-Level Cell) and MLC (Multi-Level Cell) alternatives, they typically exhibit lower endurance and write speeds due to increased bit density.

The market growth is driven by escalating demand for high-capacity, affordable storage solutions across multiple industries. The proliferation of cloud computing, big data analytics, and IoT applications has significantly boosted adoption. Furthermore, advancements in 3D NAND technology have improved TLC SSD reliability, narrowing the performance gap with premium alternatives. Key players like Samsung, Western Digital, and SK Hynix are actively expanding their TLC SSD portfolios to cater to evolving market needs, particularly in the PCIe SSD segment which shows accelerated growth potential.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Cost-Effective High-Capacity Storage to Boost TLC SSD Adoption

The global TLC SSD market is witnessing significant growth due to increasing demand for cost-effective, high-density storage solutions across consumer electronics and enterprise applications. TLC NAND flash offers a compelling price-to-capacity ratio, with prices per gigabyte approximately 30-40% lower than MLC SSDs. This cost advantage is driving mass adoption in price-sensitive segments, particularly in emerging markets where storage capacity requirements are growing exponentially. The consumer electronics sector alone accounted for over 60% of TLC SSD shipments in 2024, with laptops and gaming consoles being primary adoption drivers.

Expanding Cloud Infrastructure and Data Center Deployments Fuel Market Growth

Cloud service providers and hyperscale data centers are increasingly adopting TLC SSDs for warm storage applications, leveraging their balance of performance and affordability. While enterprise SLC and MLC SSDs dominate mission-critical applications, TLC variants are gaining traction for secondary storage workloads. The global cloud storage market’s projected growth at 22% CAGR through 2032 is creating substantial opportunities for TLC SSD vendors. Major cloud providers have begun deploying TLC-based solutions for non-latency-sensitive applications, leading to enterprise-grade TLC SSD shipments growing at nearly 35% annually.

Technological Advancements in 3D NAND Extend TLC SSD Lifespan and Performance

Recent breakthroughs in 3D NAND architecture have significantly improved TLC SSD endurance and performance characteristics. The transition from planar to 3D NAND has increased write cycles from approximately 1,000 to over 3,000 in latest-generation TLC products. Controller innovations with advanced error correction algorithms and wear-leveling techniques have further narrowed the performance gap with MLC solutions. Leading manufacturers are now shipping 176-layer and 232-layer 3D TLC NAND SSDs that deliver sequential read speeds exceeding 3,500 MB/s, making them viable for broader enterprise applications.

MARKET RESTRAINTS

Lower Endurance Compared to SLC/MLC Limits High-Performance Applications

Despite technological improvements, TLC SSDs still face limitations in write endurance compared to SLC and MLC alternatives. While suitable for consumer workloads, the typical 3,000-5,000 program/erase cycles of TLC NAND restrict adoption in write-intensive enterprise scenarios requiring 30,000+ cycles. This performance gap becomes particularly apparent in database transaction processing and server caching applications where sustained write performance is critical. The growing awareness of these limitations among enterprise buyers is slowing TLC adoption in certain mission-critical segments.

Price Volatility in NAND Flash Market Creates Supply Chain Challenges

The TLC SSD market remains vulnerable to NAND flash pricing fluctuations caused by production capacity adjustments and inventory corrections. DRAMeXchange data indicates NAND flash prices have shown 20-30% quarterly volatility in recent years, making cost forecasting challenging for OEMs and system integrators. Such instability discourages long-term procurement planning and can temporarily suppress demand during price increase cycles. The capital-intensive nature of NAND fabrication also leads to periods of oversupply followed by shortages, complicating inventory management across the supply chain.

Emerging Storage Technologies Threaten Long-Term TLC SSD Dominance

While TLC currently leads the consumer SSD market, emerging technologies like QLC (Quad-Level Cell) and PLC (Penta-Level Cell) NAND promise even higher densities at lower costs. QLC SSDs already offer 33% higher density than TLC at only marginally higher prices, with PLC prototypes demonstrating further potential. Storage-class memory solutions like Intel Optane also threaten to displace TLC SSDs in performance-sensitive caching applications. These developments may gradually erode TLC’s value proposition in its core consumer and secondary storage markets over the next decade.

MARKET OPPORTUNITIES

Explosive Growth in Edge Computing Presents New Deployment Scenarios

The rapid expansion of edge computing infrastructure presents significant opportunities for TLC SSD adoption. Edge nodes require cost-effective storage with moderate endurance characteristics, making TLC an ideal solution. Projections indicate edge storage demand will grow at 28% CAGR through 2030, driven by IoT deployments and 5G network expansion. TLC SSDs are particularly well-suited for edge AI inferencing workloads that demand faster access than HDDs but don’t require enterprise-grade endurance. Major telecommunications providers are already integrating TLC-based storage solutions into their edge server deployments.

Automotive Storage Demand Creates New Growth Vertical

The automotive industry’s digital transformation is creating substantial demand for in-vehicle storage solutions. Modern vehicles now incorporate multiple infotainment systems, telematics units, and autonomous driving capabilities requiring reliable flash storage. TLC SSDs are emerging as preferred solutions for automotive applications due to their vibration resistance and lower power consumption compared to HDDs. The automotive SSD market is projected to expand at 35% CAGR through 2032, with TLC variants accounting for over 70% of shipments in non-safety-critical systems.

Emerging Markets Offer Significant Untapped Potential

Developing regions represent a major growth opportunity as digital penetration increases. Countries in Southeast Asia, Latin America, and Africa are experiencing rapid growth in PC and smartphone adoption, driving demand for affordable storage solutions. Price sensitivity in these markets makes TLC SSDs particularly attractive alternatives to higher-cost MLC options. Local manufacturing initiatives in India and Brazil are further accelerating TLC SSD adoption by reducing import dependencies and enabling competitive pricing strategies tailored to regional markets.

MARKET CHALLENGES

Technical Complexity in Scaling 3D NAND Creates Production Bottlenecks

While 3D NAND technology has extended TLC SSD capabilities, pushing layer counts beyond 200 presents significant manufacturing challenges. Yield rates decline substantially with each additional layer, requiring increasingly sophisticated fabrication techniques. The transition to newer nodes below 20nm also introduces cell-to-cell interference issues that degrade performance. These technical hurdles have led to production bottlenecks at major NAND fabs, constraining supply during periods of peak demand. Achieving consistent high-volume production of advanced TLC NAND remains an ongoing challenge for manufacturers.

Security Concerns in Enterprise Environments Limit Adoption

Enterprise customers remain cautious about deploying TLC SSDs in security-sensitive applications due to data remanence concerns. The complex charge trap technology in TLC cells makes secure data erasure more challenging compared to SLC solutions. Regulatory requirements in financial services and government sectors often mandate more secure storage alternatives, creating barriers for TLC adoption in these verticals. While encryption and sanitization technologies are improving, perception challenges persist among security-conscious organizations.

Intensifying Competition Squeezes Manufacturer Margins

The TLC SSD market has become increasingly competitive, with over 50 active manufacturers vying for share in key segments. Price competition has intensified particularly in the consumer space, driving gross margins below 15% for many entry-level products. Chinese manufacturers have gained significant market share through aggressive pricing, forcing established players to either match prices or differentiate through performance and reliability features. This competitive environment makes R&D investment recovery challenging, potentially slowing the pace of future innovation in TLC technology.

Increasing Adoption of High-Capacity Storage Solutions to Drive TLC SSD Market Growth

The global TLC SSD market is experiencing significant growth, driven by the rising demand for cost-effective, high-capacity storage solutions across multiple industries. With the consumer electronics sector expanding rapidly, particularly in emerging economies, manufacturers are increasingly turning to TLC-based SSDs as an optimal balance between affordability and performance. Recent market data indicates that over 60% of mid-range laptops now utilize TLC SSDs as their primary storage medium, reflecting their dominance in price-sensitive segments. While these drives offer lower endurance than SLC or MLC alternatives, advancements in wear-leveling algorithms and error correction technologies have significantly improved their reliability for everyday computing tasks.

Other Trends

Enterprise Storage Optimization

Enterprise applications are witnessing growing adoption of TLC SSDs for read-intensive workloads, where the technology’s cost-per-gigabyte advantage proves particularly compelling. Data centers are implementing hybrid storage architectures that combine high-endurance solutions for write-heavy operations with TLC-based arrays for archival and caching purposes. The ability to deploy 3D NAND-based TLC SSDs with capacities exceeding 4TB has made them viable for numerous enterprise scenarios, particularly in cloud storage and content delivery networks where density and cost efficiency outweigh absolute performance metrics.

Technology Innovations Enhancing TLC SSD Viability

The competitive landscape of TLC SSDs continues to evolve as manufacturers implement innovative technologies to mitigate the technology’s inherent limitations. Multi-layer caching solutions and dynamic SLC caching mechanisms now allow TLC SSDs to deliver burst performance comparable to higher-end solutions during typical usage patterns. Additionally, controller advancements have reduced write amplification factors below 1.2 in some implementations, extending drive longevity. These improvements are reflected in the market data showing TLC-based PCIe 4.0 SSDs achieving sequential read speeds exceeding 6,000 MB/s, narrowing the performance gap with premium alternatives while maintaining significant cost advantages.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Invest in Innovation to Dominate the Expanding TLC SSD Sector

The global TLC SSD market features a dynamic competitive environment with established tech giants and emerging manufacturers vying for market share. Samsung Electronics currently leads the sector, commanding a significant portion of global revenues in 2024 due to its vertically integrated NAND production and strong brand recognition in consumer electronics. The company’s continuous innovation in PCIe 4.0 and 5.0 interfaces gives it a technological edge in performance-driven applications.

Western Digital and SK Hynix follow closely, leveraging their expertise in NAND flash memory to deliver cost-effective solutions for both consumer and enterprise markets. These companies have been particularly aggressive in expanding their QLC (Quad-Level Cell) offerings while maintaining competitive TLC product lines, creating a diverse storage portfolio that appeals to different market segments.

The competitive landscape shows increasing specialization, with companies like Kingston Technology and ADATA focusing on value-oriented consumer products, while Intel and Micron (through its Crucial brand) target the enterprise and data center sectors with higher endurance offerings. This strategic segmentation helps manufacturers avoid direct price competition in oversaturated market segments.

Recent developments highlight the industry’s rapid evolution, with Chinese manufacturers such as Yangtze Memory Technologies and Longsys gaining traction through aggressive pricing and government-supported capacity expansions. While these newcomers currently hold smaller market shares, their growing production capabilities could significantly impact global pricing dynamics in coming years.

List of Key TLC SSD Manufacturers Profiled

- Samsung Electronics (South Korea)

- Western Digital (U.S.)

- Kingston Technology (U.S.)

- SK Hynix (South Korea)

- Intel Corporation (U.S.)

- Kioxia (Japan)

- Crucial (Micron Technology) (U.S.)

- Lenovo (China)

- Transcend Information (Taiwan)

- ADATA Technology (Taiwan)

- Seagate Technology (U.S.)

- Yangtze Memory Technologies (China)

- Longsys (China)

- Kingtech (Taiwan)

- Teclast (China)

Segment Analysis:

By Type

PCIe SSD Segment Leads Due to High-Speed Data Transfer and Growing Demand for Performance-Optimized Storage

The market is segmented based on type into:

- PCIe SSD

- Subtypes: NVMe, AHCI, and others

- SATA SSD

- eMMC

- Others

By Application

Embedded Systems Segment Dominates Owing to Increasing Adoption in Smart Devices and Industrial Automation

The market is segmented based on application into:

- Embedded Systems

- Industrial Control

- Internet of Things

- Other

By End User

Consumer Electronics Maintain Strong Demand Due to Cost-Effective Storage Solutions in Laptops and Smartphones

The market is segmented based on end user into:

- Consumer Electronics

- Enterprise

- Industrial

- Automotive

By Capacity

256GB-1TB Capacity Range Gains Traction as It Offers Optimal Balance Between Price and Storage Needs

The market is segmented based on capacity into:

- Below 256GB

- 256GB-1TB

- Above 1TB

Regional Analysis: TLC SSD Market

Asia-Pacific

The Asia-Pacific region dominates the global TLC SSD market, accounting for the largest revenue share in 2024. This leadership position is driven by surging demand from China, India, and South Korea, where rapid digitalization, expanding data center infrastructure, and booming consumer electronics industries fuel adoption. China alone contributes over 35% of the region’s market due to massive local production capabilities from manufacturers like YMTC (Yangtze Memory Technologies) and Lenovo. The affordability of TLC SSDs compared to SLC/MLC alternatives makes them highly attractive in price-sensitive APAC markets. However, increasing environmental regulations and a gradual shift toward higher-performance enterprise SSDs may reshape demand patterns in coming years.

North America

North America represents the second-largest TLC SSD market, characterized by strong enterprise adoption and technological innovation. The U.S. leads regional demand due to hyperscale data center expansions by tech giants like Google and Microsoft, alongside widespread consumer adoption in gaming PCs and laptops. While PCIe-based TLC SSDs are gaining traction for high-speed applications, cost-conscious SMBs continue driving SATA SSD sales. Interestingly, the region shows a faster adoption curve for next-generation TLC SSDs with 3D NAND architectures compared to other markets, boosted by R&D investments from Intel and Western Digital.

Europe

Europe maintains steady growth in TLC SSD adoption, with Germany, France, and the UK comprising nearly 60% of regional revenues. Stringent data protection regulations (GDPR) and emphasis on energy-efficient storage solutions are accelerating the replacement of HDDs with TLC SSDs across enterprise applications. The automotive sector presents a growing niche as connected vehicles require reliable flash storage. However, the market faces challenges from the premium pricing of EU-compliant SSDs and competition from local QLC SSD manufacturers offering higher densities at comparable price points.

South America

South America’s TLC SSD market remains in growth phase, with Brazil accounting for over 40% of regional demand. Economic constraints have slowed enterprise SSD adoption, making TLC variants the preferred entry-level solution for most businesses. The gaming and DIY PC building sectors show particular promise, though import dependencies and currency fluctuations create pricing volatility. Some local manufacturers like SMS Group are emerging to serve cost-sensitive segments, but multinational brands still dominate premium channels.

Middle East & Africa

MEA represents the smallest but fastest-growing regional market, projected to exceed 11% CAGR through 2032. UAE and Saudi Arabia lead adoption through smart city initiatives and data center investments. While consumer applications currently dominate, enterprises are gradually transitioning from HDDs to TLC SSDs for critical workloads. The region faces unique challenges including extreme climate conditions requiring specialized SSDs with extended temperature ranges, creating opportunities for ruggedized TLC solutions tailored to harsh environments.

Report Scope

This market research report provides a comprehensive analysis of the Global TLC SSD Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global TLC SSD market was valued at USD 7,473 million in 2024 and is projected to reach USD 12,510 million by 2032, growing at a CAGR of 8.8%.

- Segmentation Analysis: Detailed breakdown by product type (PCIe SSD, SATA SSD, eMMC, Others), application (Embedded Systems, Industrial Control, IoT, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific dominates the market, driven by strong demand in China and Japan.

- Competitive Landscape: Profiles of leading market participants, including Samsung, Western Digital, Kingston, SK Hynix, and Intel, with their product portfolios, R&D investments, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging NAND flash technologies, AI/ML integration in storage solutions, and advancements in TLC SSD endurance and performance.

- Market Drivers & Restraints: Evaluation of factors such as rising demand for cost-effective storage solutions, growth in data centers, and challenges related to durability and write performance limitations.

- Stakeholder Analysis: Strategic insights for SSD manufacturers, OEMs, distributors, and investors to navigate the evolving market landscape.

The report employs rigorous primary and secondary research methodologies, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of the Global TLC SSD Market?

-> TLC SSD Market was valued at 7473 million in 2024 and is projected to reach US$ 12510 million by 2032, at a CAGR of 8.8% during the forecast period.

Which key companies operate in the Global TLC SSD Market?

-> Key players include Samsung, Western Digital, Kingston, SK Hynix, Intel, Kioxia, Crucial (Micron), and Lenovo, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for affordable storage solutions, expansion of data centers, and increasing adoption of SSDs in consumer electronics.

Which region dominates the market?

-> Asia-Pacific is the largest and fastest-growing market, with significant contributions from China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include advancements in 3D NAND technology, PCIe Gen 5 adoption, and increasing use of TLC SSDs in IoT and edge computing applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...