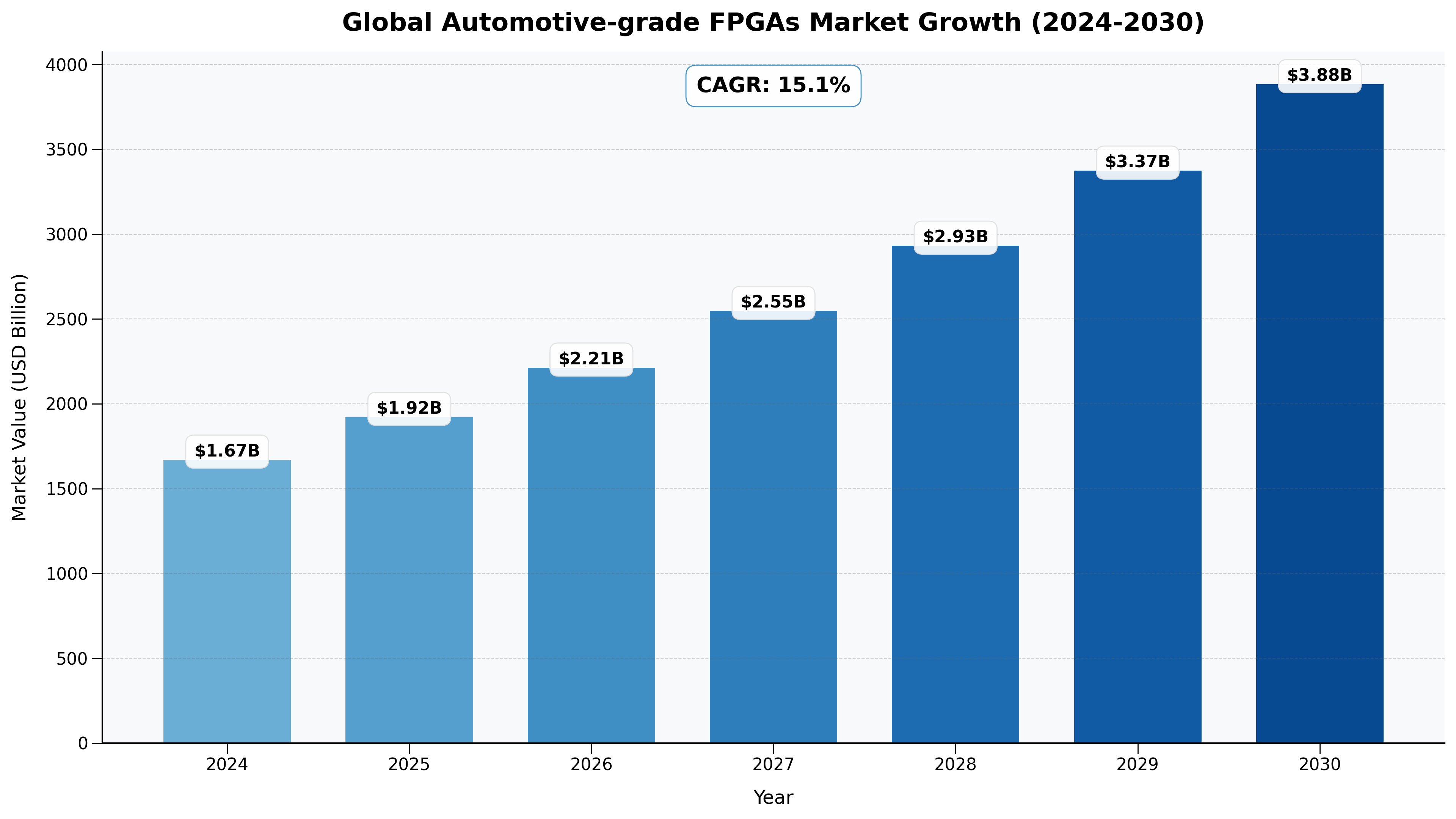

The Global Automotive-grade FPGAs Market size was valued at US$ 1.67 billion in 2024 and is projected to reach US$ 3.88 billion by 2030, at a CAGR of 15.1% during the forecast period 2024-2030.

The United States Automotive-grade FPGAs market size was valued at US$ 437.5 million in 2024 and is projected to reach US$ 994.6 million by 2030, at a CAGR of 14.7% during the forecast period 2024-2030.

Automotive-qualified FPGAs meeting stringent industry standards.

Report Overview

FPGAs in vehicles appear to be particularly strong in the embedded vision chain, including sensors and displays, as well as networking, artificial intelligence (AI), and security.

This report provides a deep insight into the global Automotive-grade FPGAs market covering all its essential aspects. This ranges from a macro overview of the market to micro details of the market size, competitive landscape, development trend, niche market, key market drivers and challenges, SWOT analysis, value chain analysis, etc.

The analysis helps the reader to shape the competition within the industries and strategies for the competitive environment to enhance the potential profit. Furthermore, it provides a simple framework for evaluating and accessing the position of the business organization. The report structure also focuses on the competitive landscape of the Global Automotive-grade FPGAs Market, this report introduces in detail the market share, market performance, product situation, operation situation, etc. of the main players, which helps the readers in the industry to identify the main competitors and deeply understand the competition pattern of the market.

In a word, this report is a must-read for industry players, investors, researchers, consultants, business strategists, and all those who have any kind of stake or are planning to foray into the Automotive-grade FPGAs market in any manner.

Global Automotive-grade FPGAs Market: Market Segmentation Analysis

The research report includes specific segments by region (country), manufacturers, Type, and Application. Market segmentation creates subsets of a market based on product type, end-user or application, Geographic, and other factors. By understanding the market segments, the decision-maker can leverage this targeting in the product, sales, and marketing strategies. Market segments can power your product development cycles by informing how you create product offerings for different segments.

Key Company

- Xilinx(AMD)

- Intel

- Microchip

- latTic

- Achronix

- Gowin Semiconductor Corp

- Low-End

- Mid-Range

- High-End

- OEM

- Aftermarket

- North America (USA, Canada, Mexico)

- Europe (Germany, UK, France, Russia, Italy, Rest of Europe)

- Asia-Pacific (China, Japan, South Korea, India, Southeast Asia, Rest of Asia-Pacific)

- South America (Brazil, Argentina, Columbia, Rest of South America)

- The Middle East and Africa (Saudi Arabia, UAE, Egypt, Nigeria, South Africa, Rest of MEA)

- Industry drivers, restraints, and opportunities covered in the study

- Neutral perspective on the market performance

- Recent industry trends and developments

- Competitive landscape & strategies of key players

- Potential & niche segments and regions exhibiting promising growth covered

- Historical, current, and projected market size, in terms of value

- In-depth analysis of the Automotive-grade FPGAs Market

- Overview of the regional outlook of the Automotive-grade FPGAs Market:

- Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

- This enables you to anticipate market changes to remain ahead of your competitors

- You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations, or other strategic documents

- The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

- Provision of market value (USD Billion) data for each segment and sub-segment

- Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

- Analysis by geography highlighting the consumption of the product/service in the region as well as indicating the factors that are affecting the market within each region

- Competitive landscape which incorporates the market ranking of the major players, along with new service/product launches, partnerships, business expansions, and acquisitions in the past five years of companies profiled

- Extensive company profiles comprising of company overview, company insights, product benchmarking, and SWOT analysis for the major market players

- The current as well as the future market outlook of the industry concerning recent developments which involve growth opportunities and drivers as well as challenges and restraints of both emerging as well as developed regions

- Includes in-depth analysis of the market from various perspectives through Porters five forces analysis

- Provides insight into the market through Value Chain

- Market dynamics scenario, along with growth opportunities of the market in the years to come

- 6-month post-sales analyst support

Customization of the Report

In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are met.

Drivers

- Increased Adoption of Advanced Driver Assistance Systems (ADAS):

Automotive-grade FPGAs are pivotal for real-time processing in ADAS systems, including adaptive cruise control, lane-keeping assistance, and autonomous driving. The growing emphasis on road safety and autonomous vehicle adoption has driven demand for high-performance, programmable logic devices. - Rising Demand for In-Vehicle Connectivity:

Modern vehicles require robust connectivity for infotainment, diagnostics, and navigation. FPGAs, with their flexibility and ability to handle high data throughput, cater to these requirements, supporting Ethernet, CAN, and LIN protocols seamlessly. - Electrification of Vehicles:

The transition to electric vehicles (EVs) necessitates advanced power management and control systems. Automotive-grade FPGAs are integral for efficient battery management, inverter control, and energy recovery systems, driving their adoption in EV architectures. - Customization and Scalability:

Unlike fixed-function ICs, FPGAs offer customizable hardware solutions, enabling automakers to optimize designs for specific functionalities. This adaptability aligns with the trend of modular vehicle platforms and evolving software-defined vehicle architectures.

Restraints

- High Cost of Development and Implementation:

Automotive-grade FPGAs are relatively expensive compared to other ICs like ASICs or MCUs. The cost associated with development tools, licensing, and testing makes it challenging for smaller OEMs or low-budget vehicle segments to adopt FPGAs extensively. - Power Consumption Concerns:

Despite advances in FPGA technology, their power consumption can be higher than ASICs, especially for continuous, intensive workloads. This can pose challenges in EVs, where energy efficiency is paramount. - Complex Design Process:

Programming and optimizing FPGAs require specialized skills, making it difficult for companies without a strong engineering base to deploy them effectively. Additionally, ensuring functional safety standards (like ISO 26262) adds complexity to FPGA-based designs.

Opportunities

- Growth in Autonomous Vehicle Technology:

The accelerating development of fully autonomous vehicles presents a lucrative opportunity for FPGA manufacturers. These devices offer the computational horsepower and flexibility needed for LIDAR processing, AI acceleration, and sensor fusion. - Integration of AI and ML in Automotive Applications:

The rising integration of AI for predictive maintenance, driver behavior analysis, and real-time decision-making is boosting demand for FPGAs with AI/ML acceleration capabilities, ensuring their relevance in next-generation vehicle systems. - Regional Market Expansion:

Emerging markets in Asia-Pacific, Latin America, and Eastern Europe are increasingly adopting advanced automotive technologies. These regions represent untapped potential for FPGA adoption as regulatory frameworks evolve and disposable incomes rise. - Collaboration with Semiconductor Ecosystem:

Partnerships between FPGA vendors, automakers, and software developers can foster innovation and accelerate time-to-market for FPGA-powered automotive solutions. Collaboration also facilitates better alignment with industry-specific needs.

Challenges

- Intense Competition from ASICs and SoCs:

ASICs and SoCs offer cost and energy efficiency for high-volume applications, making them strong competitors in the automotive semiconductor space. Convincing automakers to choose FPGAs over these alternatives remains a challenge. - Supply Chain Vulnerabilities:

Semiconductor supply chain disruptions, as seen during the COVID-19 pandemic, affect the availability of FPGAs. Ensuring a reliable supply chain is critical to meet automotive production timelines. - Adherence to Stringent Automotive Standards:

The automotive industry demands high reliability, longevity, and compliance with stringent standards. FPGA manufacturers must invest heavily in testing and validation processes, increasing time-to-market and costs. - Lack of Standardization:

The absence of universal standards for FPGA deployment in automotive applications creates compatibility issues and complicates integration with existing automotive systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...