MARKET INSIGHTS

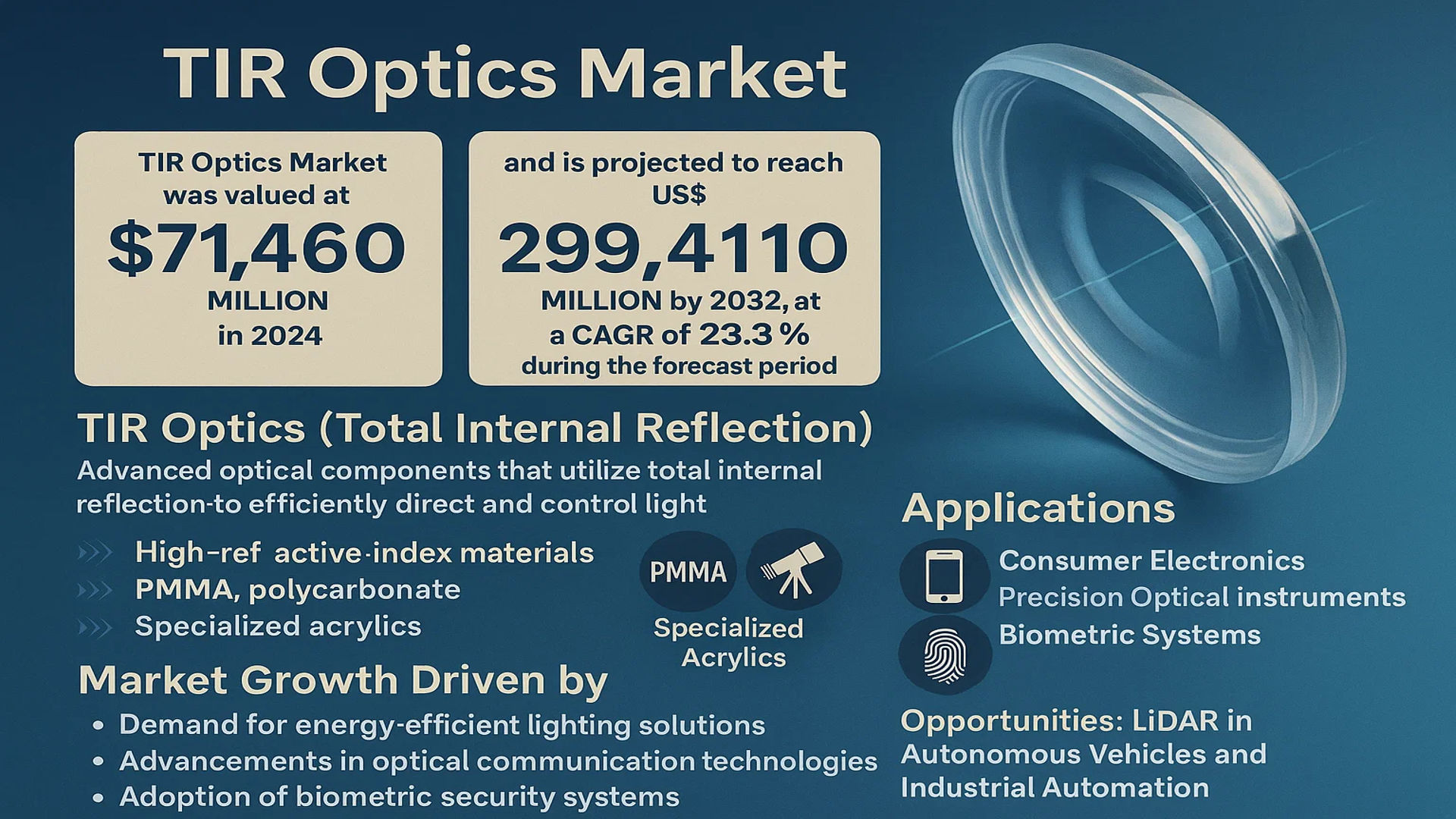

The global TIR Optics Market was valued at 71460 million in 2024 and is projected to reach US$ 299410 million by 2032, at a CAGR of 23.3% during the forecast period.

TIR (Total Internal Reflection) optics are advanced optical components that utilize the principle of total internal reflection to efficiently direct and control light. These lenses are engineered with high-refractive-index materials, such as polymethylmethacrylate (PMMA), polycarbonate, and specialized acrylics, to enhance light transmission while minimizing losses. TIR optics find critical applications across industries including consumer electronics, precision optical instruments, and biometric systems.

The market growth is primarily driven by increasing demand for energy-efficient lighting solutions, rapid advancements in optical communication technologies, and the expanding adoption of biometric security systems. Furthermore, the rise of LiDAR applications in autonomous vehicles and industrial automation is creating new opportunities for TIR optics manufacturers. Key players such as Thorlabs, Osram Sylvania, and Shanghai Optics are actively innovating to meet these demands, with strategic partnerships and product launches accelerating market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Efficiency Optical Solutions in Consumer Electronics Fuels Market Expansion

The global TIR optics market is experiencing robust growth driven by the rapidly expanding consumer electronics sector. With smartphone manufacturers increasingly incorporating advanced camera systems and augmented reality features, the demand for precision optical components has surged. Modern flagship smartphones now integrate 4-5 TIR lenses per device for tasks ranging from depth sensing to facial recognition. This trend is accelerating as manufacturers push the boundaries of computational photography and 3D sensing technologies. The consumer electronics segment accounted for over 42% of total TIR optics revenue in 2024, establishing it as the dominant application category.

Advancements in Optical Communication Infrastructure Create New Demand

Telecommunications infrastructure upgrades worldwide are driving significant adoption of TIR optics in fiber optic networks. As 5G rollouts accelerate and data centers expand to handle growing cloud computing demands, optical components that minimize signal loss while maximizing efficiency become critical. TIR lenses demonstrate up to 99.5% light transmission efficiency in commercial applications, making them indispensable for next-gen communication systems. Major network equipment providers are increasingly specifying TIR-based solutions for their performance advantages in signal integrity and thermal stability.

Automotive LiDAR Adoption Presents Substantial Growth Opportunity

The automotive industry’s rapid embrace of autonomous driving technologies is creating a new high-growth sector for TIR optics. Modern LiDAR systems for advanced driver assistance (ADAS) and autonomous vehicles typically incorporate multiple TIR lenses to shape and direct laser beams with precision. With the global autonomous vehicle market projected to grow at over 21% CAGR through 2032, the demand for reliable, high-performance optical components continues to strengthen. Leading automotive suppliers are actively forming strategic partnerships with TIR optics manufacturers to secure supply chains for these mission-critical components.

MARKET RESTRAINTS

High Manufacturing Costs Constrain Price-Sensitive Market Segments

The TIR optics market faces significant challenges from the relatively high production costs associated with precision optical manufacturing. The fabrication process requires specialized equipment, ultra-pure materials, and controlled environments that drive up capital expenditures. Polymethylmethacrylate (PMMA) and polycarbonate substrates, while cost-effective for some applications, often require additional coatings to achieve the necessary optical performance. These factors currently limit adoption in price-sensitive consumer applications where manufacturers face intense margin pressures.

Material Limitations Create Design Constraints

While TIR optics offer excellent performance characteristics, the available substrate materials present certain technical limitations. Optical plastics like PMMA have relatively low maximum operating temperatures (typically below 85°C), restricting use in high-temperature automotive and industrial applications. Additionally, UV stability concerns with some polymer materials require careful engineering for outdoor deployments. These material constraints force design compromises in some applications, potentially limiting market penetration where extreme environmental conditions exist.

MARKET CHALLENGES

Global Supply Chain Disruptions Impact Component Availability

The TIR optics industry continues facing supply chain challenges affecting raw material availability and lead times. The precision optical components market relies heavily on specialized polymer resins from a limited number of suppliers, creating vulnerability to disruptions. Recent geopolitical tensions have exacerbated these issues, with some critical optical-grade materials experiencing price volatility upwards of 30% year-over-year. Manufacturers are responding by diversifying supplier networks and increasing inventory buffers, but these measures increase working capital requirements.

Intellectual Property Protection Presents Ongoing Concerns

As competition intensifies in the TIR optics space, intellectual property protection has become a critical challenge. The industry has seen increasing patent disputes related to optical designs and manufacturing processes, particularly in the biometric and LiDAR application segments. Smaller manufacturers without extensive patent portfolios face growing barriers to entry, potentially stifling innovation. This IP landscape requires companies to dedicate substantial resources to legal protection while navigating existing patent thickets that may limit design freedom.

MARKET OPPORTUNITIES

Medical Imaging and Diagnostic Equipment Present Growth Frontier

The healthcare sector offers significant untapped potential for TIR optics manufacturers. Advanced medical imaging systems increasingly incorporate optical components for applications ranging from endoscopy to laser surgery. TIR lenses’ ability to deliver high light throughput with minimal losses makes them ideal for sensitive diagnostic equipment where signal integrity is paramount. With global healthcare spending projected to exceed $10 trillion by 2025, medical applications represent a high-value growth vector for manufacturers able to meet stringent regulatory requirements.

Emerging AR/VR Markets Demand Innovative Optical Solutions

The rapid evolution of augmented and virtual reality technologies creates compelling opportunities for TIR optics innovation. Next-generation AR glasses and VR headsets require compact, lightweight optical systems capable of delivering crisp imagery while minimizing form factor. TIR-based waveguide solutions are gaining traction as they enable more ergonomic designs compared to traditional optics. With the AR/VR hardware market expected to grow at 26% CAGR through 2030, optics manufacturers investing in specialized TIR solutions stand to capture substantial value in this emerging sector.

TIR OPTICS MARKET TRENDS

Rising Demand in Consumer Electronics to Drive Growth

The global TIR Optics market is witnessing significant expansion, primarily driven by the explosive growth in consumer electronics. Smartphones, augmented reality (AR) glasses, and advanced display technologies increasingly utilize TIR lenses for superior light management and compact design integration. With the consumer electronics sector projected to maintain a compound annual growth rate (CAGR) of over 7% through 2030, manufacturers are prioritizing high-performance optical solutions that enhance display clarity while minimizing energy consumption. TIR optics are particularly valuable in devices requiring precise beam shaping, such as virtual reality headsets and LiDAR sensors for autonomous vehicles.

Other Trends

Precision Optical Instrument Innovations

The expansion of medical diagnostics and life sciences has accelerated the adoption of TIR optics in precision instruments like confocal microscopes and biosensors. These applications demand ultra-high light efficiency and minimal aberration, which TIR lenses deliver effectively. Furthermore, the surge in biometric security systems, including facial recognition and iris scanning technologies, relies on TIR optics for accurate light collimation across diverse environmental conditions. This trend aligns with global biometric market growth, anticipated to surpass $100 billion by 2030, creating sustained demand for specialized optical components.

Material Science Breakthroughs Reshaping Production

Polycarbonate and acrylic-based TIR lenses continue dominating the market due to their optimal refractive indices and durability, but recent material innovations are unlocking new possibilities. Advanced polymer blends with enhanced thermal stability (withstanding temperatures exceeding 120°C) are gaining traction in automotive lighting systems, while nano-structured surfaces enable unprecedented control over light dispersion patterns. These developments coincide with a 23% year-over-year increase in R&D investments by leading optical material suppliers, signaling strong industry commitment to next-generation TIR solutions. Concurrently, the shift toward eco-friendly manufacturing processes is prompting manufacturers to explore recyclable optical materials without compromising performance metrics.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Competition in the TIR Optics Market

The global TIR optics market is characterized by a mix of established players and emerging competitors, all vying for dominance in a rapidly evolving optical technologies landscape. Shanghai Optics leads the market with its cutting-edge TIR lens solutions, particularly in the precision optical instruments segment, where demand rose by 18% in 2024. The company’s dominance stems from its vertically integrated manufacturing and strong R&D capabilities across Asia and North America.

Thorlabs and Osram Sylvania maintain significant market shares, particularly in industrial and consumer electronics applications. These players benefit from their extensive distribution networks and ability to customize TIR optical solutions for niche applications. Recent investments by Thorlabs in hybrid optical systems incorporating TIR technology demonstrate the industry’s shift toward multifunctional components.

While large players dominate revenue shares, mid-sized companies like Carclo and Apollo Optical Systems are gaining traction through specialized offerings. Carclo’s precision injection-molded TIR optics, for instance, captured 12% of the automotive lighting segment last year. These companies compete through technological differentiation rather than scale, focusing on high-value applications in biometrics and medical devices.

The competitive intensity is further heightened by regional specialists. Shanghai Winvow Optoelectronics dominates China’s growing market, while NMB Italia maintains strong European footholds in industrial laser applications. Such geographical specialization creates pockets of intense competition, pushing all players toward continuous innovation.

List of Key TIR Optics Companies Profiled

- Shanghai Optics (China)

- Thorlabs, Inc. (U.S.)

- Osram Sylvania (Germany)

- Carclo Technical Plastics (U.K.)

- Apollo Optical Systems (U.S.)

- DMF Lighting (U.S.)

- Shanghai Winvow Optoelectronics Technology Co. Ltd (China)

- Okamoto Glass Co Ltd (Japan)

- Greenlight Optics (U.S.)

- NMB Italia S.r.l. (Italy)

Segment Analysis:

By Type

Polycarbonate Segment Leads Due to Superior Optical Clarity and Impact Resistance

The market is segmented based on material type into:

- Polymethylmethacrylate (PMMA)

- Acrylic Acid

- Polycarbonate

- Others

By Application

Consumer Electronics Drives Demand for High-Precision Optical Components

The market is segmented based on application into:

- Consumer Electronics

- Smartphone cameras

- Virtual reality headsets

- Augmented reality devices

- Precision Optical Instruments

- Microscopes

- Laser systems

- Spectrometers

- Biometric Security Systems

- Facial recognition

- Fingerprint scanners

- Others

By Light Source

LED Applications Dominate the Market for Energy-Efficient Lighting Solutions

The market is segmented based on light source compatibility into:

- LED

- Laser

- Halogen

- Others

By Design Type

Conical TIR Optics Gain Preference for Directional Light Control Applications

The market is segmented based on optical design into:

- Conical

- Spherical

- Aspherical

- Hybrid

Regional Analysis: TIR Optics Market

Asia-Pacific

The Asia-Pacific region dominates the TIR optics market, accounting for over 45% of global demand in 2024, with China spearheading growth through its flourishing electronics manufacturing sector. Major manufacturers such as Shanghai Optics and Shanghai Winvow Optoelectronics Technology Co. Ltd have established advanced production facilities in the region to cater to rising demand for optical components in consumer electronics and telecommunications. The proliferation of 5G networks and increasing investments in fiber-optic infrastructure are accelerating adoption, particularly for applications in precision optical instruments and biometric systems. While Japan and South Korea continue to innovate with high-performance polycarbonate-based optics, emerging economies face challenges in maintaining consistent quality standards across their supply chains.

North America

Characterized by strong R&D capabilities and stringent quality requirements, the North American market represents approximately 28% of global TIR optics revenue. The U.S. leads in specialized applications, with companies like Thorlabs and Apollo Optical Systems developing advanced solutions for medical lasers and defense systems. The region’s emphasis on miniaturization has driven demand for polymethylmethacrylate-based optics in compact electronic devices. However, higher production costs compared to Asian counterparts have led to strategic partnerships with overseas manufacturers to maintain competitiveness. Government-funded research initiatives in photonics further stimulate innovation, though supply chain disruptions remain a concern for critical infrastructure projects.

Europe

European manufacturers prioritize eco-friendly production methods and regulatory compliance, with Germany and the U.K. accounting for the majority of regional demand. Osram Sylvania and NMB Italia S.r.l. have gained prominence through precision-engineered optical solutions for automotive lighting and industrial lasers. The adoption of TIR optics in biometric security systems has increased steadily, supported by strict data protection regulations across EU member states. While the market demonstrates steady growth, price sensitivity in Eastern European countries has limited penetration of advanced acrylic acid-based optical components, creating a bifurcated demand landscape within the region.

South America

This emerging market shows gradual but inconsistent growth, primarily driven by Brazil’s expanding telecommunications sector. Economic instability and import dependence hinder local manufacturing development, forcing regional players to rely on cost-effective, mass-produced optical components from global suppliers. Recent investments in urban infrastructure have created opportunities for TIR optics in traffic management and public safety applications. However, the lack of specialized technical expertise and limited R&D investment have prevented the establishment of a robust domestic supply chain, keeping the region dependent on foreign technology transfers.

Middle East & Africa

The adoption of TIR optics remains in nascent stages across most of the region, with Israel and the UAE representing the primary markets due to their focus on advanced security and surveillance systems. Government initiatives to develop smart cities have increased demand for optical components in biometric identification and environmental monitoring applications. While the market shows long-term potential, inadequate technical infrastructure and the absence of local manufacturing capabilities have constrained growth. Strategic partnerships with European and Asian suppliers are gradually addressing these gaps, though progress varies significantly between oil-rich nations and less developed economies.

Report Scope

This market research report provides a comprehensive analysis of the global and regional TIR Optics markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global TIR Optics market was valued at USD 71,460 million in 2024 and is projected to reach USD 299,410 million by 2032, growing at a CAGR of 23.3%.

- Segmentation Analysis: Detailed breakdown by product type (Polymethylmethacrylate, Acrylic Acid, Polycarbonate), application (Consumer Electronics, Precision Optical Instruments, Biometric, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis of key markets.

- Competitive Landscape: Profiles of leading market participants including Shanghai Optics, Apollo Optical Systems, Carclo, DMF Lighting, and Thorlabs, covering their product portfolios and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging optical technologies, material science advancements, and integration with IoT/AI applications.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges in supply chain, raw material availability, and technical barriers.

- Stakeholder Analysis: Insights for optical component manufacturers, system integrators, research institutions, and investors regarding market opportunities.

Primary and secondary research methods are employed, including interviews with industry experts and data from verified sources to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global TIR Optics Market?

-> TIR Optics Market was valued at 71460 million in 2024 and is projected to reach US$ 299410 million by 2032, at a CAGR of 23.3% during the forecast period.

Which key companies operate in Global TIR Optics Market?

-> Key players include Shanghai Optics, Apollo Optical Systems, Carclo, DMF Lighting, Osram Sylvania, and Thorlabs, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for precision optics in consumer electronics, advancements in optical communication technologies, and growing applications in biometric security systems.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by manufacturing capabilities in China and Japan, while North America leads in technological innovation.

What are the emerging trends?

-> Emerging trends include development of hybrid optical materials, miniaturization of optical components, and integration with smart devices and IoT applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...