MARKET INSIGHTS

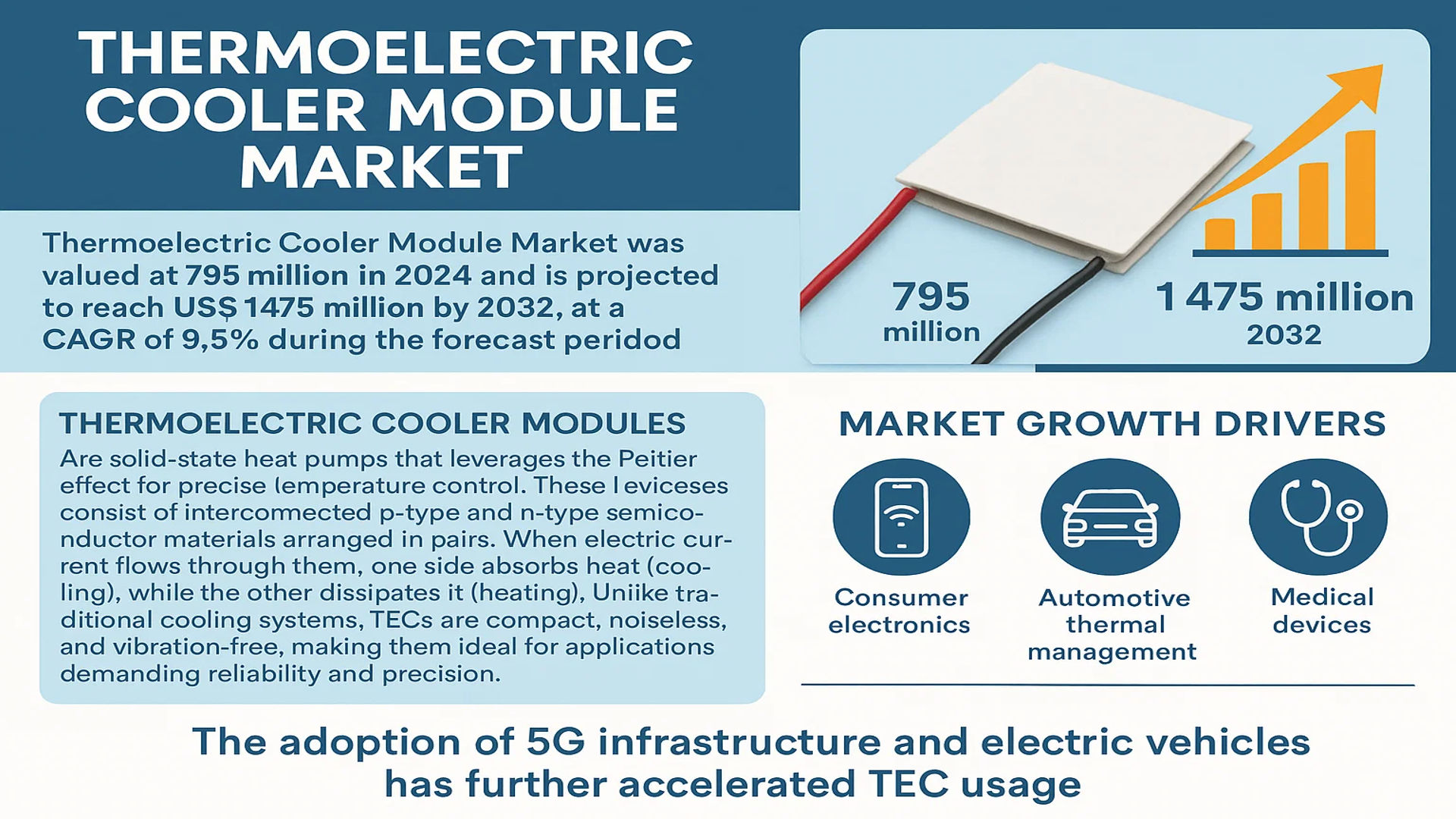

The global Thermoelectric Cooler Module Market was valued at 795 million in 2024 and is projected to reach US$ 1475 million by 2032, at a CAGR of 9.5% during the forecast period.

Thermoelectric cooler modules (TECs) are solid-state heat pumps that leverage the Peltier effect for precise temperature control. These devices consist of interconnected p-type and n-type semiconductor materials arranged in pairs. When electric current flows through them, one side absorbs heat (cooling), while the other dissipates it (heating). Unlike traditional cooling systems, TECs are compact, noiseless, and vibration-free, making them ideal for applications demanding reliability and precision.

Market growth is driven by rising demand in consumer electronics, automotive thermal management, and medical devices. The adoption of 5G infrastructure and electric vehicles has further accelerated TEC usage. Leading manufacturers like Ferrotec and Laird Thermal Systems dominate the competitive landscape, collectively holding over 50% market share. Asia-Pacific leads regional demand, accounting for more than half of global consumption in 2024.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Energy-Efficient Cooling Solutions to Propel Market Expansion

The global push for energy-efficient thermal management systems is driving significant adoption of thermoelectric cooler modules across multiple industries. With traditional compressor-based cooling systems consuming substantially more power, TECs are gaining traction due to their solid-state nature and precise temperature control capabilities. In consumer electronics alone, shipments of thermoelectric cooling modules exceeded 60 million units in 2024 as manufacturers seek compact cooling solutions for high-performance devices. The automotive sector also shows accelerating demand, particularly in electric vehicle battery thermal management systems where temperature precision is critical for safety and performance.

Emerging Medical Applications and Miniaturization Trends Fuel Market Growth

The medical sector presents a high-growth frontier for thermoelectric coolers, especially in portable medical devices and laboratory equipment requiring stable temperature conditions. Recent advances in medical imaging systems, portable insulin cooling cases, and DNA amplification equipment increasingly incorporate TEC technology. The global market for medical thermoelectric cooling applications is projected to grow at over 11% CAGR through 2030, outpacing many other sectors. Miniaturization trends across industries further drive demand for compact thermal solutions, with micro-TECs now enabling precise cooling in space-constrained applications like fiber optic components and semiconductor test equipment.

5G Infrastructure Deployment Drives Accelerated Adoption

The rapid global rollout of 5G networks is creating substantial demand for thermoelectric cooling solutions in base station equipment and optical communication systems. With 5G components generating significant heat in compact form factors, TECs provide reliable thermal management where conventional cooling methods prove inadequate. Telecommunications infrastructure investments exceeded $200 billion globally in 2024, with Asia-Pacific accounting for over 50% of deployments. This concentrated infrastructure buildout directly benefits thermoelectric module manufacturers catering to the telecom sector, particularly for cooling high-power amplifiers and laser diodes in network equipment.

MARKET RESTRAINTS

Lower Energy Efficiency Compared to Conventional Systems Limits Adoption

While thermoelectric coolers offer numerous advantages, their relatively lower coefficient of performance (COP) compared to vapor compression systems remains a significant barrier to wider adoption. Most commercial TECs achieve COPs between 0.3 and 0.7 under typical operating conditions, while traditional refrigeration systems often exceed 2.0. This efficiency gap becomes particularly problematic in high-heat load applications, where energy consumption considerations outweigh the benefits of precise temperature control. The situation is further compounded in price-sensitive markets where operating costs significantly influence purchasing decisions.

Raw Material Price Volatility Impacts Manufacturing Costs

Thermoelectric module production relies heavily on specialized semiconductor materials like bismuth telluride, whose prices have shown considerable volatility in recent years. Supply chain disruptions coupled with increasing demand from renewable energy and electronics sectors have created pricing pressures, with bismuth prices fluctuating by over 30% in the past two years alone. This instability makes production cost management challenging for manufacturers and may restrict investments in capacity expansion. The situation is particularly acute for smaller players who lack long-term supply contracts or vertical integration advantages.

Technical Limitations in High-Temperature Applications

Current thermoelectric materials exhibit performance degradation at elevated temperatures, limiting their application in environments exceeding 200°C. This thermal ceiling prevents broader adoption in industries like heavy manufacturing or aerospace propulsion systems where higher temperature differentials are required. While research into high-temperature thermoelectric materials continues, commercial solutions remain several years away from mass production. Manufacturers must therefore focus on optimizing existing material performance while developing hybrid cooling solutions for extreme temperature applications.

MARKET OPPORTUNITIES

Emerging Electric Vehicle Thermal Management Systems Present Growth Potential

The accelerating transition to electric vehicles creates substantial opportunities for thermoelectric cooling applications, particularly in battery temperature regulation systems. With global EV sales projected to surpass 45 million units annually by 2030, the demand for reliable thermal management solutions will grow accordingly. TECs are increasingly employed in battery cooling systems where their precise temperature control helps maintain optimal operating conditions and extend battery life. Automakers are also exploring thermoelectric applications for cabin comfort systems and electronic component cooling, potentially opening additional revenue streams for module manufacturers.

Advancements in IoT and Edge Computing Drive Cooling Demand

The proliferation of IoT devices and edge computing infrastructure creates growing demand for compact, reliable cooling solutions in distributed environments. As computing moves closer to data sources, thermoelectric modules provide ideal thermal management for edge servers, 5G small cells, and industrial IoT sensors operating in uncontrolled environments. The global edge computing market is forecast to exceed $250 billion by 2028, with corresponding growth potential for thermal management solutions. This trend benefits TEC manufacturers capable of delivering modules with the right balance of performance, reliability, and form factor for decentralized computing applications.

Development of Advanced Thermoelectric Materials Opens New Applications

Ongoing research into novel thermoelectric materials presents significant opportunities for performance improvements and market expansion. Recent developments in skutterudites, half-Heusler compounds, and quantum dot superlattices show promise for achieving higher ZT values (figure of merit) compared to traditional bismuth telluride-based materials. These advances could enable new applications in waste heat recovery systems and high-temperature industrial processes currently beyond the reach of conventional TECs. Manufacturers investing in material science R&D may gain first-mover advantages as these technologies mature and transition from laboratory to commercial production.

MARKET CHALLENGES

Intense Competition from Alternative Cooling Technologies

The thermoelectric cooling market faces strong competition from emerging alternative technologies like microchannel cooling, phase change materials, and advanced heat pipes. These solutions often demonstrate superior performance in specific applications, particularly those requiring high heat flux dissipation. For instance, liquid cooling systems can achieve significantly higher heat transfer coefficients than TECs in data center applications. Manufacturers must continually innovate to justify thermoelectric solutions’ value proposition while developing hybrid systems that combine strengths of multiple cooling methods.

Supply Chain Disruptions Impact Production Lead Times

Global supply chain volatility continues to affect thermoelectric module manufacturers, particularly regarding semiconductor components and rare earth materials. The average lead time for bismuth telluride wafers extended to 12-16 weeks in 2024, up from 8-10 weeks pre-pandemic. These delays create production bottlenecks and inventory management challenges across the value chain. Companies are responding through dual-sourcing strategies and inventory buffering, but these measures increase working capital requirements and may pressure margins in competitive market segments.

Technical Complexity in System Integration

Successful implementation of thermoelectric cooling systems often requires sophisticated thermal design and integration expertise that may not be readily available among end-users. The need for precise current control, heat sinking solutions, and thermal interface materials creates implementation challenges that can slow adoption. Manufacturers must invest in application engineering support and comprehensive design guidelines to overcome these barriers. The complexity is particularly pronounced in custom applications requiring specialized module configurations or operating conditions outside standard specifications.

THERMOELECTRIC COOLER MODULE MARKET TRENDS

Increasing Demand in Consumer Electronics Driving Market Growth

The global thermoelectric cooler module market is experiencing significant growth due to rising demand from the consumer electronics sector. With smartphones, wearables, and gaming devices requiring efficient thermal management solutions, thermoelectric coolers (TECs) have become indispensable. The ability of TECs to provide precise temperature control without moving parts makes them ideal for compact electronic designs. In 2024, the consumer electronics segment accounted for approximately 25% of the global market share, reflecting their crucial role in cooling high-performance processors and batteries. The shift toward 5G-enabled devices and AI-powered electronics is further accelerating adoption, as these technologies require advanced thermal management solutions to prevent overheating and maintain efficiency.

Other Trends

Rapid Expansion of Electric Vehicle Thermal Management

The automotive industry is increasingly adopting thermoelectric cooler modules for electric vehicle (EV) battery cooling and cabin climate control. Unlike traditional vapor compression systems, TECs offer silent operation and higher reliability, making them suitable for next-generation EVs. With global EV sales projected to grow at a CAGR of nearly 20% through 2030, thermoelectric cooling solutions are expected to play a vital role in thermal regulation. Manufacturers are also exploring reversible thermoelectric modules for both heating and cooling applications, improving energy efficiency in extreme weather conditions. This trend aligns with automakers’ focus on enhancing thermal performance and range optimization.

Technological Advancements and Miniaturization

Innovations in semiconductor materials and module design are significantly enhancing the efficiency of thermoelectric coolers. Recent advancements include the development of high-performance bismuth telluride (Bi2Te3) alloys and multi-stage modules capable of achieving ultra-low temperatures for specialized applications. The miniaturization of TECs has been particularly beneficial for medical and telecommunications equipment, where space constraints demand compact thermal solutions. With thermal management becoming critical in data centers and 5G infrastructure, manufacturers are investing heavily in R&D to improve heat dissipation capabilities. These technological strides are expected to push the market toward a valuation of $1.47 billion by 2032 as demand intensifies across multiple industries.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Expansions and Technological Innovations Drive Market Competition

The global thermoelectric cooler (TEC) module market exhibits a semi-consolidated competitive structure, with leading players controlling significant market share while smaller companies compete through niche applications. Ferrotec Corporation dominates the market with a 20% revenue share in 2024, leveraging its vertically integrated manufacturing capabilities and extensive patent portfolio. The company’s strong position stems from decades of expertise in thermoelectric materials and strategic acquisitions across North America and Asia.

Japanese precision engineering firms KELK Ltd. (Komatsu Group) and KYOCERA Corporation maintain technological leadership in high-performance cooling modules, particularly for telecommunications and automotive applications. Their focus on reliability testing and custom solutions has created significant barriers to entry in industrial-grade TEC segments. Meanwhile, Laird Thermal Systems continues to expand its medical and aerospace cooling solutions through partnerships with defense contractors, capturing nearly 15% of the specialized cooling market.

The competitive landscape is witnessing increased R&D investments in coefficient-of-performance (COP) improvements, with companies like Phononic and TE Technology developing novel semiconductor alloys that promise 30% higher efficiency. Additionally, Chinese manufacturers such as Guangdong Fuxin Technology are rapidly closing the technology gap through government-backed research initiatives, though they currently focus primarily on cost-sensitive consumer electronics applications.

Market consolidation appears inevitable as larger players acquire specialized firms to bolster their technological portfolios. Recent examples include Coherent Corp’s (formerly II-VI Incorporated) acquisition of thermoelectric material developers and Ferrotec’s strategic stake purchases in Chinese cooling module manufacturers. These moves suggest growing emphasis on securing supply chains while expanding geographical footprints.

List of Key Thermoelectric Cooler Module Manufacturers

- Ferrotec Corporation (Japan)

- KELK Ltd. (Komatsu Group) (Japan)

- Coherent Corp (U.S.)

- Laird Thermal Systems (U.K.)

- Z-MAX Co., Ltd. (Japan)

- KYOCERA Corporation (Japan)

- Thermonamic Electronics (China)

- TE Technology, Inc. (U.S.)

- Kryotherm Industries (Russia)

- Guangdong Fuxin Technology (China)

- Wakefield Thermal Solutions (U.S.)

- Pelonis Technologies (U.S.)

Segment Analysis:

By Type

Single-stage Thermoelectric Cooler Modules Lead the Market Due to Cost-Effectiveness and Widespread Adoption

The market is segmented based on type into:

- Single-stage Type

- Subtypes: Standard single-stage, High-performance single-stage

- Multi-stage Type

- Subtypes: Two-stage, Three-stage, and others

By Application

Consumer Electronics Segment Dominates Owing to Increasing Demand for Compact Cooling Solutions

The market is segmented based on application into:

- Consumer Electronics

- Communication

- Medical

- Automotive

- Industrial

- Aerospace & Defense

- Others

By Cooling Capacity

Low-Capacity Modules Maintain Strong Position Due to Demand from Electronics Sector

The market is segmented based on cooling capacity into:

- Low-capacity (below 50W)

- Medium-capacity (50W-200W)

- High-capacity (above 200W)

By Material Type

Bismuth Telluride-based Modules Continue to Dominate the Thermoelectric Cooler Market

The market is segmented based on material type into:

- Bismuth Telluride (Bi2Te3)

- Lead Telluride (PbTe)

- Silicon-Germanium (SiGe)

- Others

Regional Analysis: Thermoelectric Cooler Module Market

Asia-Pacific

The Asia-Pacific region dominates the global thermoelectric cooler module (TEC) market, accounting for over 50% of global demand, with China leading in both production and consumption. This prominence is driven by rapid industrialization, expansion of 5G infrastructure, and booming consumer electronics manufacturing across China, Japan, and South Korea. The region benefits from strong government support for semiconductor and electric vehicle industries, which heavily utilize TECs for thermal management. Local manufacturers like Guangdong Fuxin Technology and Zhejiang Wangu Semiconductor are expanding capacities to meet domestic demand, though high-end applications still rely on imported modules from global leaders. The proliferation of IoT devices and EV adoption are expected to sustain a double-digit CAGR through 2030.

North America

North America’s TEC market thrives on cutting-edge applications in medical devices, aerospace, and telecommunications. The U.S. accounts for nearly 80% of regional demand, supported by major players like Laird Thermal Systems and Phononic developing advanced multi-stage modules for laser systems and portable medical equipment. The Inflation Reduction Act’s $369 billion clean energy investment is indirectly boosting demand for energy-efficient cooling solutions in battery thermal management systems. However, higher production costs compared to Asian competitors have led many OEMs to source standard modules from abroad while focusing domestic capabilities on R&D-intensive applications.

Europe

European markets emphasize precision engineering and sustainability in TEC adoption, with Germany and France leading deployment in industrial automation and laboratory equipment. The region sees growing application in renewable energy systems, particularly for cooling power electronics in solar inverters. EU regulations like the Ecodesign Directive push manufacturers toward lead-free and RoHS-compliant modules. Though local production is limited, companies like Kryotherm Industries (Russia) and European subsidiaries of Ferrotec maintain strong footholds in niche medical and defense sectors, where reliability outweighs cost considerations.

Middle East & Africa

This emerging market presents unique growth opportunities in harsh environment applications, particularly for cooling telecommunications base stations and oil/gas monitoring equipment. The UAE and Saudi Arabia are investing in localized TEC assembly to support their diversification into high-tech industries. While current adoption is limited by lower industrialization levels, the region’s extreme climate conditions create natural demand for robust thermal management solutions, especially as datacenter construction accelerates. Partnerships with Asian manufacturers are helping bridge technology gaps.

South America

The South American market remains nascent but shows potential in medical refrigeration and industrial process cooling. Brazil leads regional demand, with automotive and food processing sectors beginning to adopt TECs for localized temperature control. Economic volatility and import dependency constrain market growth, though increasing renewable energy investments may drive future demand for power electronics cooling solutions. Local players like Brazilian subsidiaries of global brands focus primarily on distribution rather than manufacturing due to infrastructure limitations.

Report Scope

This market research report provides a comprehensive analysis of the Global Thermoelectric Cooler Module Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 795 million in 2024 and is projected to reach USD 1,475 million by 2032 at a CAGR of 9.5%.

- Segmentation Analysis: Detailed breakdown by product type (Single-stage, Multi-stage), application (Consumer Electronics, Communication, Medical, Automotive, Industrial, Aerospace & Defense), and end-user industries.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Asia-Pacific dominates with over 50% market share (USD 500 million in 2024), led by China, Japan, and South Korea.

- Competitive Landscape: Profiles of 25+ key players including Ferrotec (20% market share), Laird Thermal Systems, Coherent Corp, and KELK Ltd., with analysis of their product portfolios, R&D investments, and strategic partnerships.

- Technology Trends: Assessment of emerging innovations in semiconductor materials, miniaturization, and integration with IoT/AI-driven thermal management systems.

- Market Drivers: Growth in 5G infrastructure (250+ million unit shipments in 2024), electric vehicles, and medical devices. Restraints include lower efficiency compared to compressor-based systems.

- Stakeholder Analysis: Strategic insights for OEMs, component suppliers, and investors regarding high-growth applications like automotive thermal management (projected 10%+ CAGR).

The research employs primary interviews with industry leaders and analysis of verified market data from regulatory bodies, company filings, and trade associations to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Thermoelectric Cooler Module Market?

-> Thermoelectric Cooler Module Market was valued at 795 million in 2024 and is projected to reach US$ 1475 million by 2032, at a CAGR of 9.5% during the forecast period.

Which companies lead the Thermoelectric Cooler Module Market?

-> Top players include Ferrotec, Laird Thermal Systems, Coherent Corp, KELK Ltd., and Phononic, with the top 5 holding 55% market share collectively.

What drives market growth?

-> Key drivers are 5G infrastructure expansion, EV adoption, and demand for compact cooling in medical devices. Consumer electronics account for 25% of 2024 applications.

Which region shows highest growth potential?

-> Asia-Pacific (USD 500 million in 2024) leads with China as the largest consumer, while North America and Europe dominate high-value medical/automotive segments.

What are emerging technology trends?

-> Innovations focus on higher-efficiency semiconductor materials, IoT integration for smart cooling, and miniaturized modules for wearable devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...