MARKET INSIGHTS

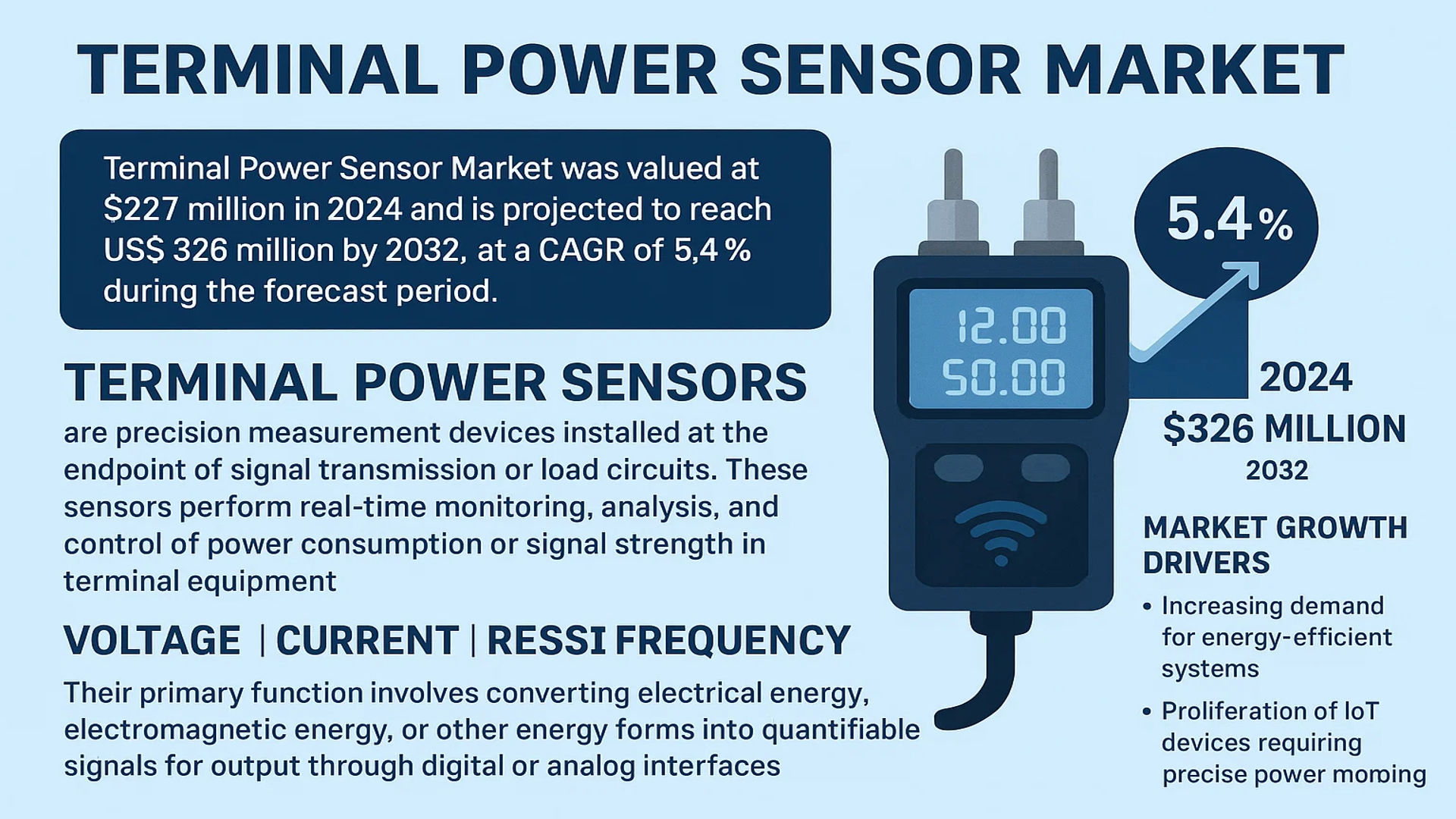

The global Terminal Power Sensor Market was valued at 227 million in 2024 and is projected to reach US$ 326 million by 2032, at a CAGR of 5.4% during the forecast period.

Terminal Power Sensors are precision measurement devices installed at the endpoint of signal transmission or load circuits. These sensors perform real-time monitoring, analysis, and control of power consumption or signal strength in terminal equipment. Their primary function involves converting electrical energy, electromagnetic energy, or other energy forms into quantifiable signals (voltage, current, resistance, or frequency) for output through digital or analog interfaces.

The market growth is driven by increasing demand for energy-efficient systems and the proliferation of IoT devices requiring precise power monitoring. While North America currently dominates with advanced manufacturing sectors, Asia-Pacific shows the highest growth potential due to expanding electronics production. Key segments include thermoelectric, Hall effect, and calorific sensors, with thermoelectric sensors projected to maintain significant market share. Leading manufacturers such as Keysight Technologies and Rohde & Schwarz continue to innovate, with recent developments focusing on higher frequency ranges and improved accuracy for 5G applications.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Energy-Efficient Systems to Propel Market Growth

The global shift toward energy-efficient systems across industries is accelerating the adoption of terminal power sensors. With industrial automation and smart manufacturing requiring precise power monitoring, these sensors enable real-time energy optimization. The industrial IoT sector alone is projected to grow at a compound annual rate exceeding 8%, creating significant demand for advanced power measurement solutions. Terminal power sensors play a critical role in minimizing energy waste while maintaining operational efficiency, particularly in high-power applications where even minor improvements can yield substantial cost savings.

Expansion of 5G Infrastructure to Drive Sensor Deployment

5G network expansion is creating unprecedented demand for terminal power sensors in communication infrastructure. Each 5G base station requires multiple power sensors to monitor transmission efficiency, with estimates suggesting up to 15 sensors per urban macro cell site. As telecom operators worldwide invest over $200 billion annually in 5G deployment, the need for reliable power monitoring solutions continues to grow. These sensors ensure optimal performance of RF components while preventing power-related failures in critical communication equipment.

Furthermore, the increasing complexity of multi-band 5G systems necessitates more sophisticated power measurement capabilities:

➤ Modern 5G antennas with beamforming technology require power sensors capable of handling frequencies up to 40 GHz while maintaining measurement accuracy within ±0.5 dB.

The rollout of millimeter wave technologies in 5G+ networks will further expand the application scope for high-frequency terminal power sensors in coming years.

MARKET RESTRAINTS

High Development Costs to Limit Market Penetration

While terminal power sensors offer significant benefits, their development presents substantial financial barriers. Advanced sensors capable of measuring high-frequency signals require expensive components such as gallium arsenide semiconductors and precision calibration equipment. The design and testing process for a single sensor model can exceed six months with costs ranging from $500,000 to $2 million depending on frequency range and accuracy requirements. These high development costs create challenges for manufacturers seeking to expand their product portfolios across different frequency bands and power levels.

Additional Restraints

Technical Complexity

Developing sensors that maintain accuracy across wide temperature ranges (-40°C to +85°C) while compensating for signal reflection losses remains technically challenging. Many manufacturers struggle to achieve consistent performance metrics across all operating conditions.

Miniaturization Demands

The industry push for smaller form factors conflicts with the need for robust shielding against electromagnetic interference, requiring costly engineering solutions to maintain sensor reliability in compact designs.

MARKET OPPORTUNITIES

Emerging Applications in Electric Vehicles to Create New Growth Avenues

The rapid electrification of automotive systems presents significant opportunities for terminal power sensor manufacturers. Modern electric vehicles incorporate over 50 power monitoring points across battery management, motor control, and charging systems. With global EV production expected to triple by 2030, the demand for automotive-grade power sensors that withstand harsh operating environments while maintaining ±0.1% measurement accuracy will grow substantially. Sensor providers that can meet the automotive industry’s stringent quality and reliability standards stand to capture a significant share of this emerging market segment.

Other promising applications include onboard charging systems where power sensors help optimize energy transfer efficiency during both AC and DC charging scenarios. Wireless charging infrastructure development will further expand the need for specialized power measurement solutions in coming years.

MARKET CHALLENGES

Intense Competition from Alternative Technologies to Pressure Market Growth

The terminal power sensor market faces growing competition from integrated power measurement solutions that combine multiple functions into single chipsets. Semiconductor companies are developing System-on-Chip designs that embed power measurement capabilities directly into power management ICs, potentially reducing the need for discrete sensors in some applications. While these integrated solutions currently lack the precision of dedicated sensors for high-frequency applications, continuous improvements in semiconductor technology may narrow this performance gap over time.

Additional Challenges

Supply Chain Vulnerabilities

Dependence on specialty semiconductor materials makes the industry susceptible to geopolitical factors affecting the supply of critical components such as gallium nitride wafers and precision resistors.

Standardization Issues

The absence of universal calibration standards across different frequency ranges creates compatibility challenges for users operating multi-vendor systems, potentially slowing adoption in some sectors.

TERMINAL POWER SENSOR MARKET TRENDS

Rising Demand for Energy Efficiency to Drive Terminal Power Sensor Adoption

The growing emphasis on energy efficiency across industries is accelerating the adoption of terminal power sensors, which provide real-time monitoring of power consumption in communication networks, industrial automation, and smart devices. With global electricity demand projected to increase by 2.5% annually through 2032, businesses are investing in precise measurement tools to optimize energy usage and reduce operational costs. Terminal power sensors offer high accuracy (±0.5 dB) and wide frequency range capabilities, making them indispensable in sectors requiring stringent power management. Additionally, government regulations mandating energy-efficient infrastructure further bolster market expansion.

Other Trends

5G Network Expansion

The rollout of 5G infrastructure worldwide is creating substantial demand for terminal power sensors, particularly those capable of handling high-frequency signals (up to 40 GHz). These sensors enable telecom operators to maintain optimal signal integrity across base stations and transmission equipment. With over 2.2 billion 5G subscribers expected by 2026, manufacturers are focusing on developing compact sensors with multi-band compatibility and enhanced thermal stability for outdoor deployments.

Integration of IoT in Industrial Automation

Industrial IoT applications are driving innovation in terminal power sensor technology, with features like wireless connectivity (Zigbee, LoRaWAN) and cloud-based analytics gaining traction. Smart factories utilize these sensors for predictive maintenance, detecting anomalies in motor drives, robotics, and power distribution units. The market for IIoT sensors in manufacturing is projected to grow at 12.3% CAGR through 2030, with terminal power sensors capturing over 28% share of industrial monitoring solutions. Recent product launches featuring galvanic isolation (1000V+ protection) specifically target harsh industrial environments.

Advancements in Semiconductor Technology Reshaping Product Offerings

Leading manufacturers are leveraging GaN (Gallium Nitride) and SiC (Silicon Carbide) semiconductor technologies to develop next-generation terminal power sensors with faster response times (<1μs) and wider dynamic range (60dB+). These innovations address the needs of emerging applications like electric vehicle charging infrastructure and renewable energy systems. Modular sensor designs are gaining popularity, allowing field-replaceable detection heads while maintaining calibration accuracy within ±0.2%. The thermoelectric sensor segment, currently holding 42% market share, benefits most from these technological improvements.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Competition in Terminal Power Sensor Market

The global terminal power sensor market features a dynamic competitive environment, where established technology providers and emerging innovators compete to capture market share. Keysight Technologies leads the industry with its comprehensive range of high-precision sensors and measurement solutions, particularly in RF and microwave applications. Their dominance stems from continuous R&D investments, with over 12% of annual revenue dedicated to developing next-generation power measurement technologies.

Rohde & Schwarz and Anritsu Corporation maintain strong positions in the communications segment, providing critical testing solutions for 5G infrastructure deployment. Both companies have significantly expanded their portfolio through strategic acquisitions – Rohde & Schwarz recently integrated iberts test solutions, while Anritsu enhanced its millimeter-wave capabilities through partnerships with chipset manufacturers.

Meanwhile, Texas Instruments and Honeywell are leveraging their semiconductor expertise to develop integrated power monitoring solutions for industrial IoT applications. Texas Instruments’ recent launch of its INA233 power monitor with digital interface demonstrates the growing convergence of sensing and control functionalities in terminal applications.

Market Differentiation Strategies

While large corporations compete through scale and vertical integration, mid-sized players like Vaunix Technology and Mini-Circuits focus on niche applications. Vaunix has gained traction in defense and aerospace sectors with its ruggedized sensors, capturing approximately 8% market share in military communications. Mini-Circuits, known for its RF components, has successfully extended into power measurement through modular sensor solutions that offer configuration flexibility.

The competitive intensity is further amplified by regional players such as Beijing Zhongwei Technology and Murata Manufacturing, who are rapidly closing the technology gap through localized R&D centers. Beijing Zhongwei’s recent $15 million investment in its Chengdu facility underscores the growing capability of Chinese manufacturers to serve both domestic and export markets.

List of Key Terminal Power Sensor Companies Profiled

- Keysight Technologies (U.S.)

- Rohde & Schwarz (Germany)

- Anritsu Corporation (Japan)

- Teledyne Technologies (U.S.)

- Bird Technologies (U.S.)

- Tektronix (U.S.)

- Vaunix Technology (U.S.)

- Mini-Circuits (U.S.)

- Texas Instruments (U.S.)

- Honeywell International (U.S.)

- Murata Manufacturing (Japan)

- Beijing Zhongwei Technology (China)

- Rohm Semiconductor (Japan)

The landscape continues evolving as companies balance organic innovation with strategic partnerships. Recent collaborations between sensor manufacturers and cloud platform providers indicate the industry’s shift toward connected power monitoring solutions, setting the stage for the next phase of competition in smart infrastructure applications.

Segment Analysis:

By Type

Thermoelectric Sensors Lead the Market Due to High Precision and Wide Application Scope

The market is segmented based on type into:

- Thermoelectric

- Hall Effect

- Calorific

By Application

Communication Terminal Segment Holds Major Share Due to Proliferation of Wireless Networks

The market is segmented based on application into:

- Communication Terminal

- Industrial Control

- Medical Equipment

- Consumer Electronics

- Others

By End User

Telecommunications Sector Emerges as Key Adopter for Network Infrastructure Monitoring

The market is segmented based on end user into:

- Telecommunications

- Manufacturing

- Healthcare

- Consumer Electronics

- Others

Regional Analysis: Terminal Power Sensor Market

Asia-Pacific

Dominating the global Terminal Power Sensor market with the largest revenue share, the Asia-Pacific region is experiencing robust growth fueled by rapid industrialization and extensive deployment of 5G infrastructure. China leads the regional market, accounting for over 40% of APAC’s demand, driven by massive investments in telecom infrastructure and smart manufacturing. The thermoelectric sensor segment is particularly strong here due to its cost-effectiveness in high-volume applications. Japan and South Korea follow closely, with advanced adoption in precision measurement applications for semiconductors and automotive electronics. While price sensitivity remains a key market characteristic, increasing quality standards in electronics manufacturing are driving upgrades to more sophisticated sensor solutions.

North America

The highly mature North American market prioritizes technological sophistication and reliability in terminal power measurement. With major players like Keysight Technologies and Tektronix headquartered in the region, innovation drives market differentiation – particularly in RF power measurement for aerospace/defense applications. The U.S. Department of Defense’s increasing budget for electronic warfare systems (projected to reach $17.8 billion in 2024) is creating specialized demand. However, market growth faces headwinds from trade restrictions on advanced sensor technologies and gradual saturation in traditional measurement applications. The medical equipment sector shows particular promise for high-accuracy terminal power sensors.

Europe

Characterized by stringent quality standards and environmental regulations, the European market emphasizes precision and energy efficiency in terminal power sensing solutions. Germany’s strong industrial automation sector accounts for nearly 30% of regional demand, particularly for Hall Effect sensors in motor control applications. The EU’s push for energy-efficient electronics under the Ecodesign Directive is accelerating adoption of smart power monitoring solutions. However, market fragmentation across countries and relatively slow infrastructure modernization compared to Asia temper growth potential. Emerging opportunities exist in renewable energy systems integration and electric vehicle charging infrastructure.

Middle East & Africa

Though currently a smaller market, MEA shows accelerating growth in terminal power sensor adoption, particularly in Gulf nations modernizing their oil/gas infrastructure and telecom networks. UAE’s smart city initiatives and Saudi Arabia’s Vision 2030 industrial diversification are driving demand for advanced power monitoring in critical infrastructure. The region exhibits a unique demand pattern where ultra-ruggedized sensors for harsh environments coexist with cutting-edge solutions for urban infrastructure. Market growth is constrained by technical skill gaps in sensor implementation and valuation of price over technical specifications in procurement decisions.

South America

The South American market remains price-driven with basic terminal power sensors dominating industrial and consumer applications. Brazil accounts for nearly half of regional demand, particularly in basic power monitoring for agricultural equipment and consumer electronics. Market maturity varies significantly by country, with Chile and Colombia showing more sophisticated demand patterns aligned with North American standards. Political and economic instability continue to deter major investments in advanced sensing solutions, though increasing automation in mining operations presents a promising niche for growth.

Report Scope

This market research report provides a comprehensive analysis of the global Terminal Power Sensor market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Terminal Power Sensor market was valued at USD 227 million in 2024 and is projected to reach USD 326 million by 2032, growing at a CAGR of 5.4%.

- Segmentation Analysis: Detailed breakdown by product type (Thermoelectric, Hall Effect, Calorific), application (Communication Terminal, Industrial Control, Medical Equipment, Consumer Electronics), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. and China are key growth markets, with Asia-Pacific showing the fastest growth.

- Competitive Landscape: Profiles of leading market participants including Keysight Technologies, Rohde & Schwarz, Anritsu, Teledyne Technologies, and Texas Instruments, covering their product portfolios, market share, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging sensor technologies, integration with IoT platforms, and advancements in power measurement accuracy.

- Market Drivers & Restraints: Analysis of factors such as increasing demand for energy-efficient devices, growth in telecommunications infrastructure, and challenges related to high precision requirements.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, OEMs, system integrators, and investors regarding market opportunities and competitive positioning.

The report employs both primary and secondary research methodologies, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Terminal Power Sensor Market?

-> Terminal Power Sensor Market was valued at 227 million in 2024 and is projected to reach US$ 326 million by 2032, at a CAGR of 5.4% during the forecast period.

Which key companies operate in Global Terminal Power Sensor Market?

-> Key players include Keysight Technologies, Rohde & Schwarz, Anritsu, Teledyne Technologies, Bird Technologies, Tektronix, and Texas Instruments.

What are the key growth drivers?

-> Key growth drivers include increasing demand for power efficiency in electronics, growth in 5G infrastructure, and expanding industrial automation.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is expected to show the highest growth rate during the forecast period.

What are the emerging trends?

-> Emerging trends include miniaturization of sensors, integration with AI for predictive maintenance, and development of ultra-high frequency power sensors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...