MARKET INSIGHTS

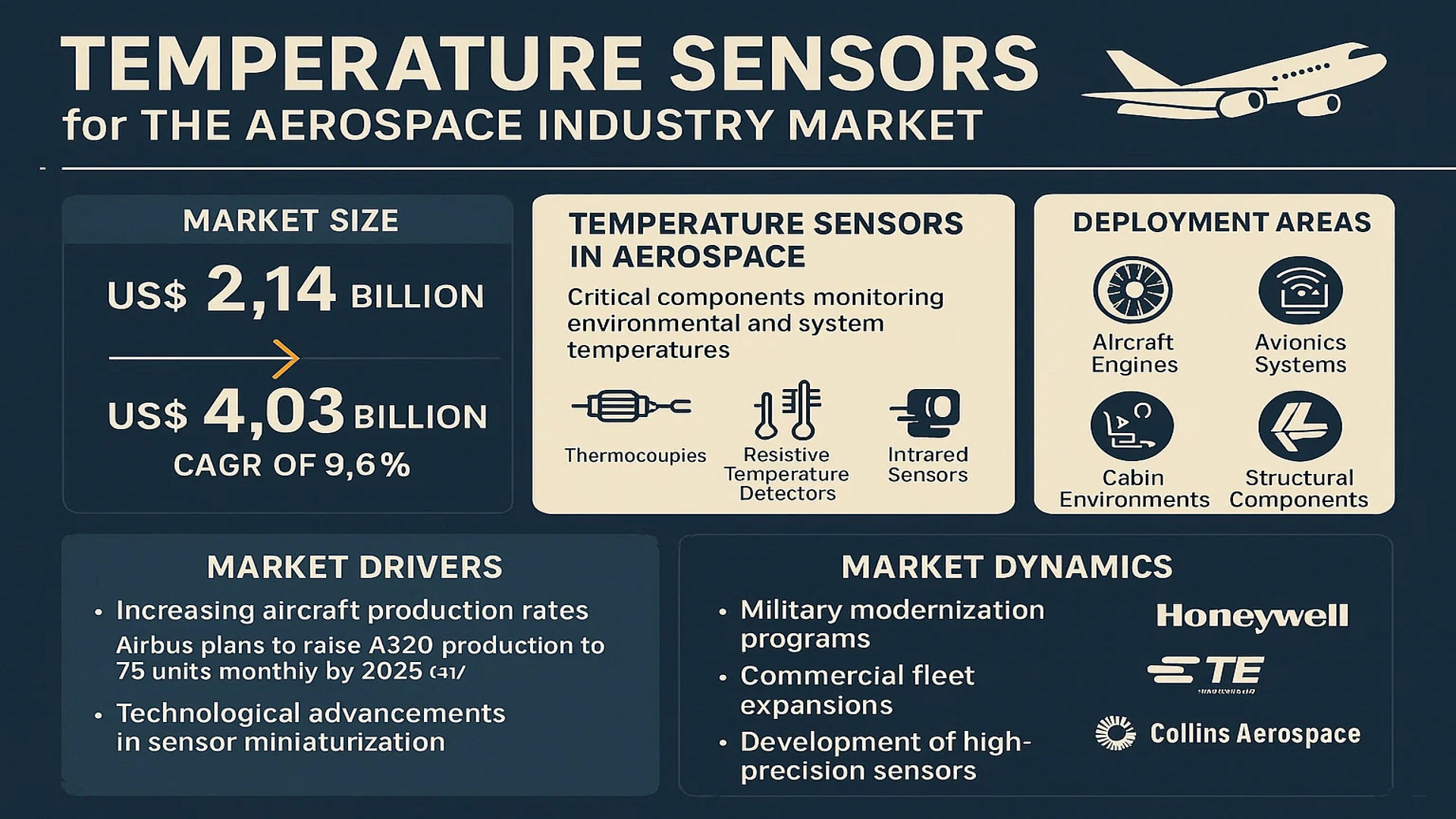

The global Temperature Sensors for The Aerospace Industry Market size was valued at US$ 2.14 billion in 2024 and is projected to reach US$ 4.03 billion by 2032, at a CAGR of 9.6% during the forecast period 2025-2032.

Temperature sensors in aerospace are critical components that monitor environmental and system temperatures to ensure operational safety and performance. These devices include thermocouples, resistive temperature detectors (RTDs), infrared sensors, and other specialized variants. They are deployed across aircraft engines, avionics systems, cabin environments, and structural components to provide real-time thermal data for flight control systems.

Market growth is driven by increasing aircraft production rates and technological advancements in sensor miniaturization. Airbus plans to increase A320 production to 75 units monthly by 2025, up from 60 in 2019, directly boosting sensor demand. The global aerospace industry generated USD 386.4 billion revenue in 2021 (4.1% YoY growth), with military modernization programs and commercial fleet expansions further accelerating adoption. Key players like Honeywell, TE Connectivity, and Collins Aerospace are developing high-precision sensors with enhanced durability for extreme aerospace conditions.

MARKET DYNAMICS

MARKET DRIVERS

Rising Aircraft Production and Fleet Expansion to Fuel Temperature Sensor Demand

The commercial aerospace sector is witnessing robust growth, with Airbus and Boeing ramping up production rates to meet pent-up demand post-pandemic. Airbus increased production of its A320 family to 65 units per month in 2023, with plans to reach 75 per month by 2025 – up from just 40 during the pandemic lows. This production surge directly correlates with increased demand for temperature sensors used in engine monitoring, environmental control systems, and avionics cooling. Each new generation aircraft requires 15-20% more sensors than previous models due to enhanced monitoring requirements, creating substantial market opportunities.

Aviation Safety Regulations Mandating Advanced Monitoring Systems

Strict aviation safety standards are compelling manufacturers to incorporate more sophisticated temperature monitoring solutions. The Federal Aviation Administration (FAA) and European Union Aviation Safety Agency (EASA) have introduced regulations requiring real-time temperature monitoring in critical aircraft systems. These regulations are driving adoption of smart temperature sensors with predictive analytics capabilities. Recent accidents attributed to thermal runaway in lithium-ion batteries have further accelerated regulatory focus, with the aerospace temperature sensor market expected to benefit from these mandated upgrades across commercial and military fleets.

The growing integration of IoT-enabled sensors in modern aircraft for condition-based maintenance is another key growth driver. Airlines are increasingly adopting these systems to reduce unscheduled maintenance and improve operational efficiency.

➤ Modern twin-aisle aircraft now incorporate over 500 temperature sensors throughout airframe and power systems, compared to about 300 in early 2000s models.

Furthermore, the space sector’s expansion, with over 1,800 satellites launched in 2022 alone, has created new demand for specialized high-reliability temperature sensors capable of withstanding extreme space environments.

MARKET RESTRAINTS

Stringent Certification Requirements Increasing Time-to-Market Challenges

The aerospace industry’s rigorous certification processes pose significant barriers to new temperature sensor technologies. Each sensor variant requires certification under DO-160 (Environmental Conditions and Test Procedures for Airborne Equipment) or equivalent standards, a process that typically takes 18-24 months and costs $500,000-$2 million per product. These extensive validation requirements make it difficult for smaller manufacturers to compete, limiting market innovation. The certification burden is particularly challenging for emerging technologies like fiber optic temperature sensors, despite their potential advantages in electromagnetic interference environments.

Additionally, the long product lifecycle of aerospace components (often 20-30 years) creates inertia against technology adoption. Airlines and OEMs are reluctant to replace proven sensor technologies due to requalification costs and potential system integration challenges.

MARKET CHALLENGES

Material and Supply Chain Constraints Impacting Sensor Manufacturing

The aerospace temperature sensor market faces significant supply chain vulnerabilities, particularly for specialized materials. Platinum resistance temperature detectors (RTDs), widely used in aircraft engines, rely on platinum group metals where prices have fluctuated 30-50% annually. Similarly, the semiconductor shortage has affected production of smart digital temperature sensors, forcing many manufacturers to implement 12-18 month lead times. These disruptions come at a time when OEMs are demanding just-in-time deliveries to support accelerated production schedules.

Other Critical Challenges

High Development Costs

Developing aerospace-grade temperature sensors requires substantial investment in cleanroom facilities, testing equipment, and specialized personnel. The typical R&D cost for a new aerospace temperature sensor line ranges between $5-10 million, creating high barriers to entry.

Technical Performance Limitations

Extreme operational environments in aerospace applications (-55°C to +2000°C range requirements) push current sensor technologies to their limits. Developing sensors that maintain accuracy across this range while resisting vibration, radiation, and chemical exposure remains an ongoing engineering challenge.

MARKET OPPORTUNITIES

Emerging Electric Aircraft Market Creating Demand for Next-Gen Sensors

The burgeoning electric vertical takeoff and landing (eVTOL) and hybrid-electric aircraft market represents a significant growth opportunity. These aircraft require specialized temperature monitoring systems for high-voltage battery packs, electric motors, and power electronics. Current estimates suggest each eVTOL aircraft will need 40-60% more temperature sensors than conventional helicopters, with the global eVTOL market projected to reach $30 billion by 2030. Sensor manufacturers investing in high-voltage compatible, lightweight solutions stand to gain substantial market share as these aircraft enter commercial service.

Additionally, the increasing adoption of additive manufacturing in aerospace enables new sensor integration approaches. Embedded temperature sensors in 3D-printed components are opening possibilities for distributed temperature monitoring that were previously impractical.

The growing emphasis on predictive maintenance in both commercial and military aviation also presents opportunities. Airlines are investing heavily in sensor networks that can provide early warning of thermal anomalies, reducing maintenance costs and improving aircraft availability.

TEMPERATURE SENSORS FOR THE AEROSPACE INDUSTRY MARKET TRENDS

Increasing Aircraft Production Rates to Drive Demand for Temperature Sensors

The aerospace industry is experiencing a significant rebound in aircraft production following pandemic-related slowdowns. Airbus plans to increase monthly production of its A320 family to 65 units by 2023 and potentially 75 units by 2025, which will directly stimulate demand for temperature sensors across engines, avionics, and environmental control systems. This resurgence occurs as temperature monitoring becomes increasingly critical for modern aircraft, where sensors must operate reliably in extreme conditions ranging from -55°C to over 1,000°C in turbine sections. The growing complexity of aerospace systems is driving adoption of advanced sensor technologies that combine high accuracy with minimal drift over time.

Other Trends

Miniaturization and Smart Sensor Integration

Aerospace manufacturers increasingly demand temperature sensors with reduced size and weight while maintaining or improving performance characteristics. This trend aligns with broader aircraft electrification initiatives where smart sensors with embedded diagnostics can communicate directly with maintenance systems. The integration of MEMS (Micro-Electro-Mechanical Systems) technology allows sensors to occupy less space while providing real-time data to predictive maintenance algorithms. These advancements help aircraft operators reduce weight and improve fuel efficiency while enhancing system monitoring capabilities.

Expanding Space Sector Investments Accelerate Sensor Innovation

Government and private sector investments in space exploration are creating new opportunities for temperature sensor manufacturers. With global aerospace industry revenues reaching $386.4 billion in 2021, representing 4.1% annual growth, demand has increased for specialized sensors capable of operating in the vacuum of space and extreme thermal cycling environments. Space applications require sensors with exceptional radiation hardness and long-term reliability, pushing manufacturers to develop innovative solutions using materials like platinum resistance elements and advanced thermocouple alloys. The growing satellite sector, which represents 73% of aerospace industry value, particularly drives demand for sensors with low power consumption and minimal calibration drift over multi-year missions.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Reliability Drive Market Leadership in Aerospace Temperature Sensing

The global temperature sensors market for the aerospace industry features a competitive mix of established manufacturers and emerging specialists. With aircraft production rates rebounding post-pandemic—Airbus plans to produce 75 A320-family aircraft monthly by 2025—demand for precision temperature monitoring solutions is accelerating. This dynamic has intensified competition among sensor providers to deliver products that meet stringent aviation safety standards while improving cost efficiency.

Honeywell International Inc. dominates the market, leveraging its vertically integrated aerospace solutions and decades of expertise in extreme-environment sensing. The company’s recent $100M investment in next-gen aerospace IoT sensors underscores its commitment to maintaining technological leadership. Close behind, TE Connectivity has gained significant market share through strategic acquisitions, including its 2023 purchase of Firstrate Sensor to expand its aerospace portfolio.

Meanwhile, Collins Aerospace differentiates itself through proprietary thin-film sensor technology, particularly in military aviation applications. The company reported 18% year-over-year growth in its sensor division during 2023, attributed to rising defense budgets across NATO countries. Smaller players like IST AG compete through niche innovations—their micro-miniature sensors are increasingly adopted in satellite thermal management systems as the space sector grows to $386 billion globally.

The competitive landscape continues evolving as manufacturers pursue three key strategies: 1) Developing wireless and self-powered sensors to reduce aircraft weight, 2) Enhancing predictive maintenance capabilities through AI integration, and 3) Expanding MRO (Maintenance, Repair, and Overhaul) networks to capture aftermarket opportunities. Recent partnerships, like Meggitt Sensing Systems’ collaboration with Lufthansa Technik, demonstrate how sensor providers are aligning with operators to co-develop customized solutions.

List of Key Temperature Sensor Providers for Aerospace

- Honeywell International Inc. (U.S.)

- TE Connectivity Ltd. (Switzerland)

- Collins Aerospace (U.S.)

- Meggitt Sensing Systems (U.K.)

- Conax Technologies (U.S.)

- TT Electronics (U.K.)

- IST AG (Switzerland)

- Thermocoax (France)

- Emerson Electric Co. (U.S.)

- Ametek Fluid Management Systems (U.S.)

- San Giorgio S.E.I.N. s.r.l. (Italy)

- Minco (U.S.)

Segment Analysis:

By Type

Thermocouple Segment Dominates Due to High Accuracy and Durability in Extreme Aerospace Conditions

The market is segmented based on type into:

- Thermocouple

- Subtypes: Type K, Type J, Type T, and others

- Resistive Type

- Subtypes: RTDs (Resistance Temperature Detectors), Thermistors, and others

- Infrared

- Others

By Application

Military Aircraft Segment Leads Due to Critical Temperature Monitoring Requirements

The market is segmented based on application into:

- Military Aircraft

- Civil Aircraft

- Spacecraft

- Unmanned Aerial Vehicles (UAVs)

- Others

By End User

OEMs Maintain Largest Market Share Due to Direct Integration in Aircraft Manufacturing

The market is segmented based on end user into:

- OEMs (Original Equipment Manufacturers)

- MRO (Maintenance, Repair and Overhaul) Providers

- Airlines

- Space Agencies

By Aircraft Type

Commercial Aviation Leads with Rising Passenger Traffic and Fleet Expansion

The market is segmented based on aircraft type into:

- Narrow-body Aircraft

- Wide-body Aircraft

- Regional Jets

- Business Jets

- Military Aircraft

Regional Analysis: Temperature Sensors for The Aerospace Industry Market

North America

The North American aerospace temperature sensor market is driven by strict FAA regulations and high adoption of advanced aircraft technologies. Commercial aviation giants like Boeing and defense contractors such as Lockheed Martin demand high-precision temperature monitoring systems to comply with safety standards. The region accounts for over 35% of global aerospace spending, with U.S. defense budgets allocating $842 billion in 2024. While legacy aircraft utilize thermocouples, next-gen platforms increasingly adopt infrared sensors for non-contact measurement. Supply chain consolidation among sensor manufacturers presents challenges, but ongoing R&D investments in IoT-enabled solutions create growth opportunities.

Europe

European aerospace temperature sensor demand is shaped by Airbus production scaling (targeting 75 A320s monthly by 2025) and ESA space program expansions. EU defense initiatives like the European Defence Fund incentivize localized sensor production, though reliance on U.S. suppliers persists for critical applications. Temperature sensor innovation focuses on lightweight designs to support fuel efficiency mandates, with Germany and France leading in MEMS-based solutions. Brexit complications continue to disrupt UK-EU aerospace partnerships, while Eastern European MRO facilities drive replacement demand. Environmental regulations push development of lead-free sensors, particularly for civil aviation applications.

Asia-Pacific

Asia-Pacific dominates aerospace sensor volume growth, with China’s COMAC C919 program and India’s UDAN regional connectivity scheme catalyzing demand. Local manufacturers like Firstrate Sensor capture 28% of the regional market by offering cost-competitive alternatives to Western suppliers. While military modernization programs in Japan and South Korea specify high-end sensors, price sensitivity in emerging markets favors resistive-type solutions. The region faces quality consistency challenges, with 17% of sensor-related aircraft incidents in 2023 traced to calibration issues. However, investments in semiconductor fabrication are enabling domestic production of advanced infrared array sensors.

South America

South America’s aerospace sensor market grows incrementally, constrained by economic instability but supported by fleet renewal initiatives. Brazil’s Embraer drives 62% of regional demand through business jet production, while Argentina’s FAdeA focuses on military aircraft upgrades. The lack of local sensor manufacturers creates import dependency, compounded by currency fluctuations. MRO facilities increasingly opt for refurbished sensors to control costs, though new widebody acquisitions by LATAM and Azul require modern monitoring systems. Regulatory harmonization with EASA standards is gradually improving sensor certification processes across the region.

Middle East & Africa

The MEA market shows polarized growth – Gulf states invest heavily in next-gen sensor technologies for military aviation (notably Saudi Arabia’s $50 billion Vision 2030 defense plan), while African nations rely on legacy systems due to budget constraints. Emirates and Qatar Airways’ fleet expansions drive premium sensor demand, with particular focus on thermal management for desert operations. South Africa remains the regional maintenance hub, though component sanctions on Russia have disrupted some supply channels. Israel’s sensor expertise in UAV applications presents export opportunities, while North African countries face challenges in establishing consistent aerospace supply chains.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Temperature Sensors for The Aerospace Industry market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at US$ 2.14 billion in 2024 and is projected to reach US$ 4.03 billion by 2032, growing at a CAGR of 9.6%.

- Segmentation Analysis: Detailed breakdown by product type (thermocouple, resistive, infrared), application (military aircraft, civil aircraft), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis of key markets like the US, China, and Germany.

- Competitive Landscape: Profiles of 25+ leading market participants including Honeywell, TE Connectivity, and Collins Aerospace, covering their product portfolios, market share (top 5 players hold 35% share), and strategic developments.

- Technology Trends: Analysis of emerging technologies like smart sensors, IoT integration, and miniaturization trends in aerospace temperature monitoring systems.

- Market Drivers: Evaluation of factors including increasing aircraft production (Airbus targeting 75 A320/month by 2025), growing aerospace industry (USD 386 billion in 2021), and stringent safety regulations.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, aircraft OEMs, MRO providers, and investors regarding market opportunities and challenges.

The research methodology combines primary interviews with industry experts and secondary data from verified sources, ensuring accuracy and reliability of market intelligence.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Temperature Sensors for The Aerospace Industry Market?

-> Temperature Sensors for The Aerospace Industry Market size was valued at US$ 2.14 billion in 2024 and is projected to reach US$ 4.03 billion by 2032, at a CAGR of 9.6% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Key players include Honeywell, TE Connectivity, Collins Aerospace, Meggitt Sensing Systems, and Ametek, among others.

What are the key growth drivers?

-> Growth is driven by increasing aircraft production, rising aerospace investments (USD 386 billion industry), and stringent safety regulations.

Which region dominates the market?

-> North America holds the largest share (38%), while Asia-Pacific shows the highest growth rate (6.2% CAGR).

What are the emerging trends?

-> Emerging trends include miniaturization of sensors, IoT integration for predictive maintenance, and development of high-temperature resistant materials.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...