MARKET INSIGHTS

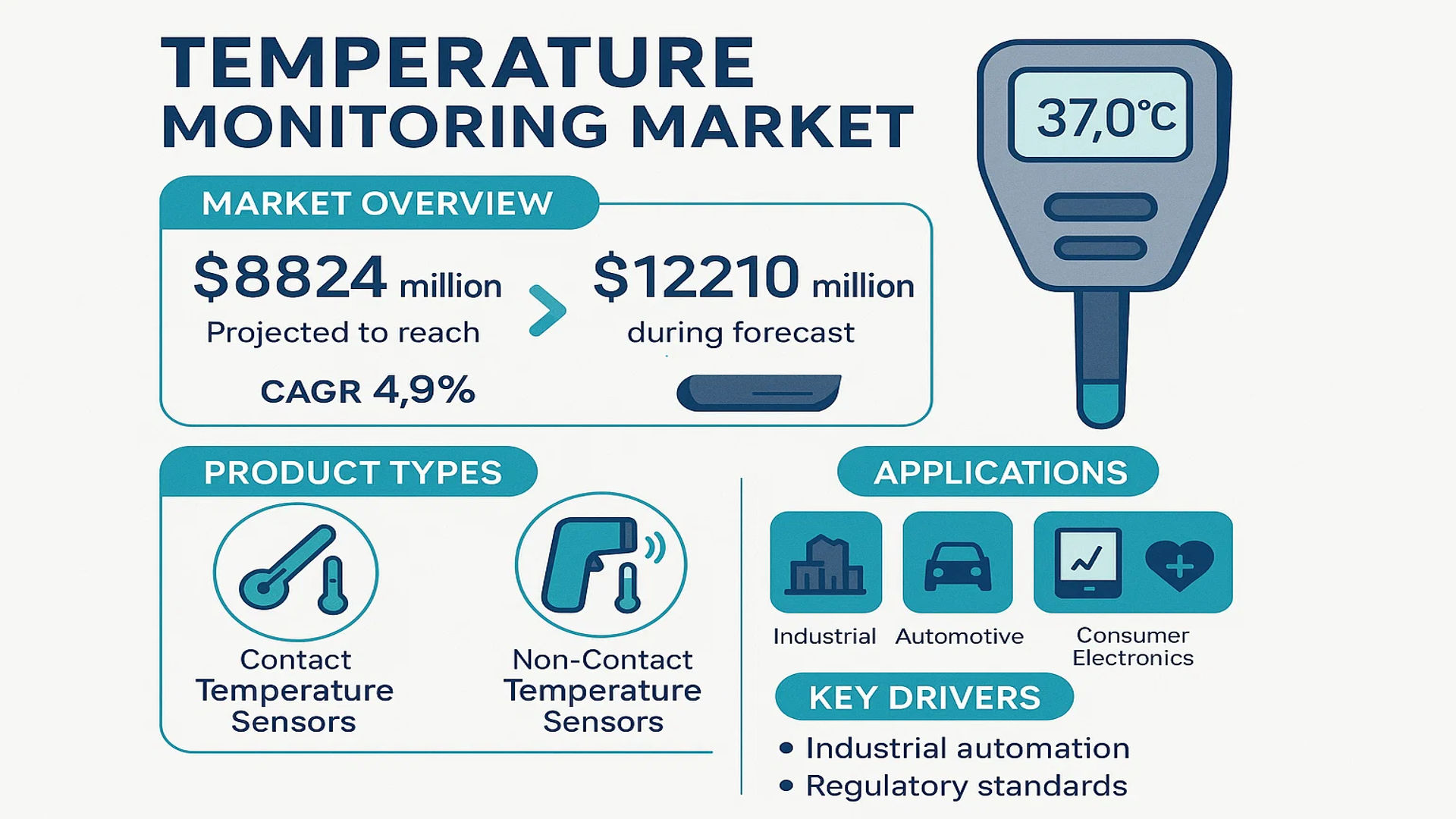

The global Temperature Monitoring Market was valued at 8824 million in 2024 and is projected to reach US$ 12210 million by 2032, at a CAGR of 4.9% during the forecast period.

Temperature monitoring products are specialized devices, primarily probes and sensors, designed to collect temperature data and present it in a human-understandable format. These critical components are categorized into two main types: contact temperature sensors, which require physical contact with the object being measured, and non-contact temperature sensors, which measure temperature from a distance. These sensors are fundamental to ensuring operational efficiency, safety, and quality control across a diverse range of sectors including industrial manufacturing, automotive, consumer electronics, and healthcare.

The market’s steady growth is underpinned by several key drivers, most notably the relentless push towards industrial automation and the implementation of stringent regulatory standards, particularly in the food and beverage and pharmaceutical sectors. Furthermore, the increasing integration of Internet of Things (IoT) technology and the rising demand for wireless and smart monitoring systems are creating significant new opportunities. The competitive landscape is fragmented, with the top five manufacturers—including Emerson, Sensata, and Amphenol—holding a combined market share of approximately 15%. Geographically, North America is the largest market, accounting for about 30% of global revenue, followed closely by Europe and China.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Industrial Automation and IoT Integration to Accelerate Market Growth

The global temperature monitoring market is experiencing robust growth driven by the rapid expansion of industrial automation and Internet of Things (IoT) integration across multiple sectors. Manufacturing facilities increasingly deploy smart temperature sensors to maintain optimal operating conditions, prevent equipment failure, and ensure product quality. The automotive industry, which accounts for approximately 28% of market applications, relies heavily on precision temperature monitoring for engine management, battery thermal regulation in electric vehicles, and climate control systems. The integration of Industry 4.0 technologies has created demand for connected temperature monitoring solutions that provide real-time data analytics and predictive maintenance capabilities. This technological evolution enables manufacturers to reduce downtime by up to 25% and improve energy efficiency by 15-20%, creating substantial value across production ecosystems.

Stringent Regulatory Requirements in Healthcare and Food Sectors to Boost Adoption

Healthcare and food industries are driving significant market growth due to increasingly stringent regulatory requirements for temperature-sensitive products. The medical sector requires precise temperature monitoring for vaccine storage, blood banks, pharmaceutical manufacturing, and laboratory applications, with compliance standards mandating continuous monitoring and documentation. Temperature deviations in pharmaceutical storage can render products ineffective, creating both safety concerns and substantial financial losses. Similarly, the food and beverage industry faces rigorous food safety regulations that mandate temperature control throughout the supply chain. Recent global health crises have further emphasized the importance of reliable temperature monitoring, with cold chain logistics for vaccines and perishable goods becoming critical infrastructure. These regulatory pressures are compelling organizations to invest in advanced monitoring systems that provide audit trails, real-time alerts, and compliance reporting capabilities.

Growing Emphasis on Energy Efficiency and Sustainability to Drive Market Expansion

The increasing global focus on energy efficiency and sustainability is creating substantial growth opportunities for advanced temperature monitoring solutions. Buildings account for approximately 40% of global energy consumption, with HVAC systems representing a significant portion of this usage. Smart temperature monitoring and control systems can reduce energy consumption in commercial buildings by 15-30% through optimized heating and cooling operations. Industrial facilities are implementing temperature monitoring to improve process efficiency, reduce waste, and minimize environmental impact. The transition toward renewable energy sources and electric vehicles further drives demand for sophisticated thermal management systems that ensure safety and performance. Government initiatives promoting energy efficiency and carbon reduction are accelerating adoption across multiple sectors, creating a favorable regulatory environment for temperature monitoring technologies.

MARKET CHALLENGES

High Implementation and Maintenance Costs to Constrain Market Penetration

The temperature monitoring market faces significant challenges related to implementation and maintenance costs, particularly for advanced IoT-enabled systems. While basic contact sensors remain relatively affordable, sophisticated monitoring solutions incorporating wireless connectivity, cloud platforms, and advanced analytics require substantial capital investment. Small and medium-sized enterprises often find the upfront costs prohibitive, especially when considering the total cost of ownership including software subscriptions, maintenance, and staff training. Additionally, retrofitting existing infrastructure with modern temperature monitoring systems can involve significant disruption and additional expenses. The need for periodic calibration and certification of precision instruments, particularly in regulated industries like healthcare and pharmaceuticals, adds ongoing operational costs that some organizations struggle to justify despite the potential benefits.

Other Challenges

Interoperability and Integration Complexities

The proliferation of different communication protocols and data formats creates interoperability challenges that hinder seamless integration of temperature monitoring systems with existing infrastructure. Many organizations operate legacy equipment that cannot easily communicate with modern IoT platforms, requiring additional gateways and middleware that increase complexity and cost. The lack of standardized protocols across manufacturers means that organizations often face vendor lock-in, limiting flexibility and increasing long-term dependency on specific technology providers.

Data Security and Privacy Concerns

As temperature monitoring systems become increasingly connected and data-driven, concerns about cybersecurity and data privacy are growing. Industrial facilities and healthcare organizations handle sensitive operational data that could be vulnerable to cyber attacks. The consequences of compromised temperature monitoring systems could include product spoilage, equipment damage, or even safety incidents in critical applications. These security concerns make organizations cautious about adopting cloud-based and connected solutions, particularly in highly regulated industries where data breaches could have severe compliance implications.

MARKET RESTRAINTS

Technical Limitations in Extreme Environments to Restrict Market Application

Temperature monitoring solutions face significant technical limitations when deployed in extreme environments, restricting their application across certain industries. In high-temperature industrial settings such as metal manufacturing, glass production, or energy generation, conventional sensors may fail or provide inaccurate readings due to material limitations. Similarly, cryogenic applications in medical storage or industrial gases present challenges for maintaining sensor accuracy and reliability at extremely low temperatures. These environmental constraints often require specialized and expensive sensor technologies that increase overall system costs. The development of sensors capable of withstanding extreme conditions while maintaining accuracy represents an ongoing engineering challenge that limits market expansion in certain industrial segments where conventional solutions prove inadequate.

Limited Technical Expertise and Skill Gaps to Hinder Market Development

The rapid technological advancement in temperature monitoring systems has created a significant skills gap that restrains market growth. Modern systems require expertise in sensor technologies, data analytics, network communications, and cybersecurity—skills that are in short supply across many industries. Organizations struggle to find qualified personnel capable of designing, implementing, and maintaining sophisticated temperature monitoring infrastructure. This skills shortage is particularly acute in emerging markets and smaller organizations that lack the resources to invest in extensive training programs. The complexity of integrating temperature monitoring data with other operational systems further exacerbates this challenge, as it requires cross-functional expertise that spans multiple technical domains. Without adequate technical capabilities, organizations may delay adoption or implement suboptimal solutions that fail to deliver expected benefits.

Economic Volatility and Budget Constraints to Slow Market Adoption

Global economic volatility and budget constraints present significant restraints for temperature monitoring market growth. During periods of economic uncertainty, organizations tend to postpone capital expenditures on non-essential equipment, including advanced monitoring systems. The perception of temperature monitoring as an operational expense rather than a strategic investment makes it vulnerable to budget cuts during economic downturns. Additionally, price sensitivity varies significantly across regions and industries, with developing markets and small businesses particularly constrained by budget limitations. The long return-on-investment period for some temperature monitoring implementations, especially those requiring infrastructure upgrades, makes justification difficult in organizations focused on short-term financial performance. These economic factors create adoption barriers that slow market growth despite the clear operational benefits that advanced temperature monitoring systems can provide.

MARKET OPPORTUNITIES

Emergence of AI and Predictive Analytics to Create New Growth Frontiers

The integration of artificial intelligence and predictive analytics with temperature monitoring systems presents substantial growth opportunities across multiple industries. Advanced algorithms can analyze historical temperature data to predict equipment failures, optimize energy consumption, and prevent product spoilage before it occurs. In manufacturing, AI-driven temperature monitoring can reduce unplanned downtime by up to 45% and improve product quality consistency. The healthcare sector benefits from predictive analytics that can anticipate refrigeration system failures in vaccine storage, potentially preventing costly spoilage of temperature-sensitive medications. These intelligent systems continuously learn from operational data, improving their predictive capabilities over time and creating increasingly valuable insights for organizations. The convergence of temperature monitoring with AI technologies represents a significant evolution beyond basic measurement into proactive management and optimization.

Expansion of Cold Chain Logistics to Drive Demand for Advanced Monitoring Solutions

The rapid growth of cold chain logistics, particularly driven by pharmaceutical and food industries, creates substantial opportunities for advanced temperature monitoring solutions. Global pharmaceutical cold chain logistics is experiencing double-digit growth due to increasing biologics and vaccine distribution, requiring precise temperature control throughout the supply chain. The food industry’s shift toward fresh and organic products further amplifies demand for reliable cold chain monitoring. Modern solutions incorporating GPS tracking, wireless connectivity, and cloud-based platforms enable real-time visibility into shipment conditions across global supply networks. These systems can automatically trigger alerts when temperatures deviate from specified ranges, allowing for immediate corrective action. The expansion of e-commerce and direct-to-consumer delivery models for temperature-sensitive products creates additional demand for monitoring solutions that ensure product integrity from manufacturer to end consumer.

Development of Miniaturized and Wireless Sensors to Enable New Applications

Technological advancements in sensor miniaturization and wireless communication are creating new application opportunities for temperature monitoring across previously inaccessible areas. Miniature sensors can be deployed in complex machinery, medical devices, and consumer products where space constraints previously limited monitoring capabilities. Wireless technology eliminates the need for extensive wiring infrastructure, reducing installation costs and enabling monitoring in remote or mobile applications. The development of energy-harvesting technologies that power sensors from ambient heat or vibration further expands application possibilities by eliminating battery replacement needs. These technological innovations enable temperature monitoring in applications ranging from wearable medical devices to smart agriculture systems, creating new market segments and driving overall industry growth. The continuous reduction in sensor size and cost while improving accuracy and connectivity capabilities represents a significant opportunity for market expansion into novel applications and industries.

TEMPERATURE MONITORING MARKET TRENDS

Integration of IoT and Wireless Connectivity to Emerge as a Pivotal Trend

The proliferation of the Internet of Things (IoT) is fundamentally reshaping the temperature monitoring landscape by enabling real-time, remote data acquisition and system control. This trend is accelerating the adoption of wireless sensors, which now represent a significant and rapidly growing segment of the market. These advanced systems facilitate predictive maintenance in industrial settings, allowing for the early detection of equipment anomalies before they lead to costly failures. Furthermore, in the medical sector, the demand for connected devices that can seamlessly transmit patient temperature data to electronic health records is surging, driven by the need for improved clinical workflows and patient outcomes. The global shift towards Industry 4.0 and smart manufacturing is a primary catalyst, with investments in industrial automation technologies creating a sustained demand for sophisticated, network-enabled monitoring solutions.

Other Trends

Stringent Regulatory Compliance and Quality Assurance

Heightened regulatory scrutiny across several key industries is a major driver for advanced temperature monitoring solutions. In the pharmaceutical and food & beverage sectors, maintaining strict environmental conditions is not just a matter of quality but a legal requirement. Regulations such as the FDA’s Title 21 CFR Part 11, which governs electronic records, mandate the use of validated and auditable monitoring systems. This has led to increased investment in compliant data loggers and monitoring platforms that ensure an unbroken chain of custody for temperature-sensitive products. The cold chain logistics market, in particular, relies heavily on these technologies to guarantee the integrity of vaccines, biologics, and perishable goods from manufacture to end-user, making regulatory compliance a powerful market force.

Miniaturization and Advancements in Sensor Technology

Continuous innovation in micro-electro-mechanical systems (MEMS) and semiconductor technology is leading to the development of smaller, more accurate, and energy-efficient temperature sensors. This trend of miniaturization is critical for applications in consumer electronics, wearable medical devices, and compact industrial equipment. The latest generation of sensors offers higher precision with minimal power consumption, enabling their integration into battery-powered and portable devices. Moreover, the development of non-contact infrared (IR) sensors has seen remarkable progress, with their accuracy and affordability improving significantly. This has expanded their use cases beyond traditional industrial settings into public health, such as the widespread deployment of thermal scanners for fever detection, a practice that gained immense traction globally and is now being integrated into long-term health and safety protocols.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Technological Innovation and Strategic Expansion to Maintain Competitive Edge

The global temperature monitoring market exhibits a fragmented yet competitive structure, characterized by the presence of numerous established multinational corporations and specialized niche players. Emerson Electric Co. stands as a dominant force, leveraging its extensive portfolio of industrial-grade contact and non-contact sensors and its formidable distribution network across North America, Europe, and Asia-Pacific. The company’s market leadership is further solidified by strategic acquisitions and a strong focus on IoT-integrated monitoring solutions for critical industries like oil & gas and manufacturing.

Sensata Technologies and Amphenol Corporation also command significant market shares, largely due to their deep-rooted presence in the automotive and industrial sectors. Their growth is propelled by continuous innovation in high-accuracy, miniaturized sensors and robust supply chain relationships with major OEMs. Furthermore, TE Connectivity and Texas Instruments are pivotal players, distinguished by their advanced semiconductor-based sensor technologies and significant investments in research and development for next-generation applications in consumer electronics and medical devices.

These leading entities are actively pursuing growth through geographic expansion into emerging markets and the launch of sophisticated, energy-efficient products. For instance, recent developments include the introduction of wireless, battery-less sensor platforms and AI-driven predictive maintenance systems. Meanwhile, other significant participants like Honeywell International Inc. and Siemens AG are strengthening their positions through substantial R&D expenditures, strategic partnerships with software firms for data analytics, and portfolio diversification into integrated building management and smart city solutions.

The competitive intensity is expected to increase further as companies strive to meet the evolving demands for precision, reliability, and connectivity. This dynamic ensures a continuous cycle of innovation and strategic maneuvering within the global landscape.

List of Key Temperature Monitoring Companies Profiled

- Emerson Electric Co. (U.S.)

- Sensata Technologies, Inc. (U.S.)

- Amphenol Corporation (U.S.)

- TE Connectivity Ltd. (Switzerland)

- Texas Instruments Incorporated (U.S.)

- Molex, LLC (U.S.)

- Honeywell International Inc. (U.S.)

- Siemens AG (Germany)

- ABB Ltd. (Switzerland)

- Panasonic Holdings Corporation (Japan)

- STMicroelectronics N.V. (Switzerland)

- Fluke Corporation (U.S.)

Segment Analysis:

By Type

Contact Temperature Sensors Segment Dominates the Market Due to Widespread Adoption Across Industrial and Automotive Applications

The market is segmented based on type into:

- Contact Temperature Sensors

- Subtypes: Thermocouples, Resistance Temperature Detectors (RTDs), Thermistors, and others

- Non-Contact Temperature Sensors

- Subtypes: Infrared (IR) Sensors, Fiber Optic Sensors, and others

By Application

Automotive Industry Segment Leads Due to Critical Need for Thermal Management in Electric Vehicles and Engine Systems

The market is segmented based on application into:

- Automotive Industry

- Electronics

- Industries

- Medical

- Food and Beverage

- Oil and Gas

- Other

By End User

Industrial Manufacturing Segment is a Key End User Driven by Process Control and Automation Requirements

The market is segmented based on end user into:

- Industrial Manufacturing

- Healthcare Providers

- Automotive OEMs

- Consumer Electronics Manufacturers

- Energy and Utilities

- Other

Regional Analysis: Temperature Monitoring Market

North America

North America holds the largest share of the global temperature monitoring market, accounting for approximately 30% of total revenue. This dominance is driven by stringent regulatory requirements across healthcare, pharmaceuticals, and food safety sectors, alongside advanced manufacturing and energy industries. The United States leads the region, with significant demand from the automotive and electronics sectors. Key players like Emerson, Honeywell, and Texas Instruments have a strong presence, fostering innovation in both contact and non-contact sensor technologies. The region’s focus on Industry 4.0 and IoT integration is accelerating the adoption of smart, connected temperature monitoring systems that offer real-time data analytics and predictive maintenance capabilities.

Europe

Europe represents a mature and highly regulated market, accounting for roughly 20% of global revenue. Strict EU directives governing medical devices, food storage, and industrial processes compel the use of high-accuracy, reliable temperature monitoring solutions. Germany, France, and the U.K. are the largest national markets, supported by robust automotive, chemical, and pharmaceutical industries. The region shows a growing preference for wireless and IoT-enabled sensors to enhance supply chain visibility and comply with environmental sustainability goals. However, market growth is tempered by economic pressures and the high cost of advanced sensor deployment in some Eastern European countries.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market for temperature monitoring, propelled by massive industrialization, expanding healthcare infrastructure, and rising consumer electronics production. China alone holds a share of about 20%, with Japan and South Korea also being significant contributors. The region’s growth is fueled by cost-effective manufacturing and increasing investments in smart city projects and automotive production. While contact sensors remain dominant due to their lower cost, there is a rising uptake of non-contact infrared sensors, particularly in medical and consumer applications post-pandemic. Local manufacturers are increasingly competitive, though international players like Panasonic and Omron maintain strong positions.

South America

The South American market is developing, characterized by gradual modernization of industrial and healthcare infrastructure. Brazil and Argentina are the primary markets, driven by the food and beverage and pharmaceutical sectors. Economic volatility and inconsistent regulatory enforcement, however, pose challenges to widespread adoption of advanced monitoring systems. Demand is largely concentrated in urban centers and export-oriented industries that must comply with international standards. The market shows potential for growth as regional stability improves and investment in industrial automation increases.

Middle East & Africa

This region presents an emerging market with growth opportunities centered around oil and gas operations, construction, and healthcare development in Gulf Cooperation Council (GCC) countries like Saudi Arabia and the UAE. The extreme climatic conditions necessitate robust temperature monitoring in sectors such as energy and logistics. However, the market’s expansion is uneven, hindered by limited technological adoption in less developed areas and funding constraints for advanced infrastructure. Long-term prospects are tied to economic diversification projects and increasing healthcare expenditure across the region.

Report Scope

This market research report provides a comprehensive analysis of the global Temperature Monitoring market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Temperature Monitoring Market?

-> Temperature Monitoring Market was valued at 8824 million in 2024 and is projected to reach US$ 12210 million by 2032, at a CAGR of 4.9% during the forecast period.

Which key companies operate in Global Temperature Monitoring Market?

-> Key players include Emerson, Sensata, Amphenol, TE Connectivity, Texas Instruments, Honeywell, Siemens, ABB, and STMicroelectronics, among others. The top five manufacturers hold a combined market share of approximately 15%.

What are the key growth drivers?

-> Key growth drivers include increasing automation across industries, stringent regulatory requirements in healthcare and food sectors, rising demand for consumer electronics, and the integration of IoT and AI in temperature monitoring systems.

Which region dominates the market?

-> North America is the largest market, holding approximately 30% of the global share, followed by Europe and China, each with about 20% market share.

What are the emerging trends?

-> Emerging trends include the development of wireless and non-contact temperature sensors, miniaturization of devices, adoption of Industry 4.0 technologies, and increasing use of smart sensors with predictive maintenance capabilities.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...