SWIR Image Sensors for Industrial Cameras MARKET INSIGHTS

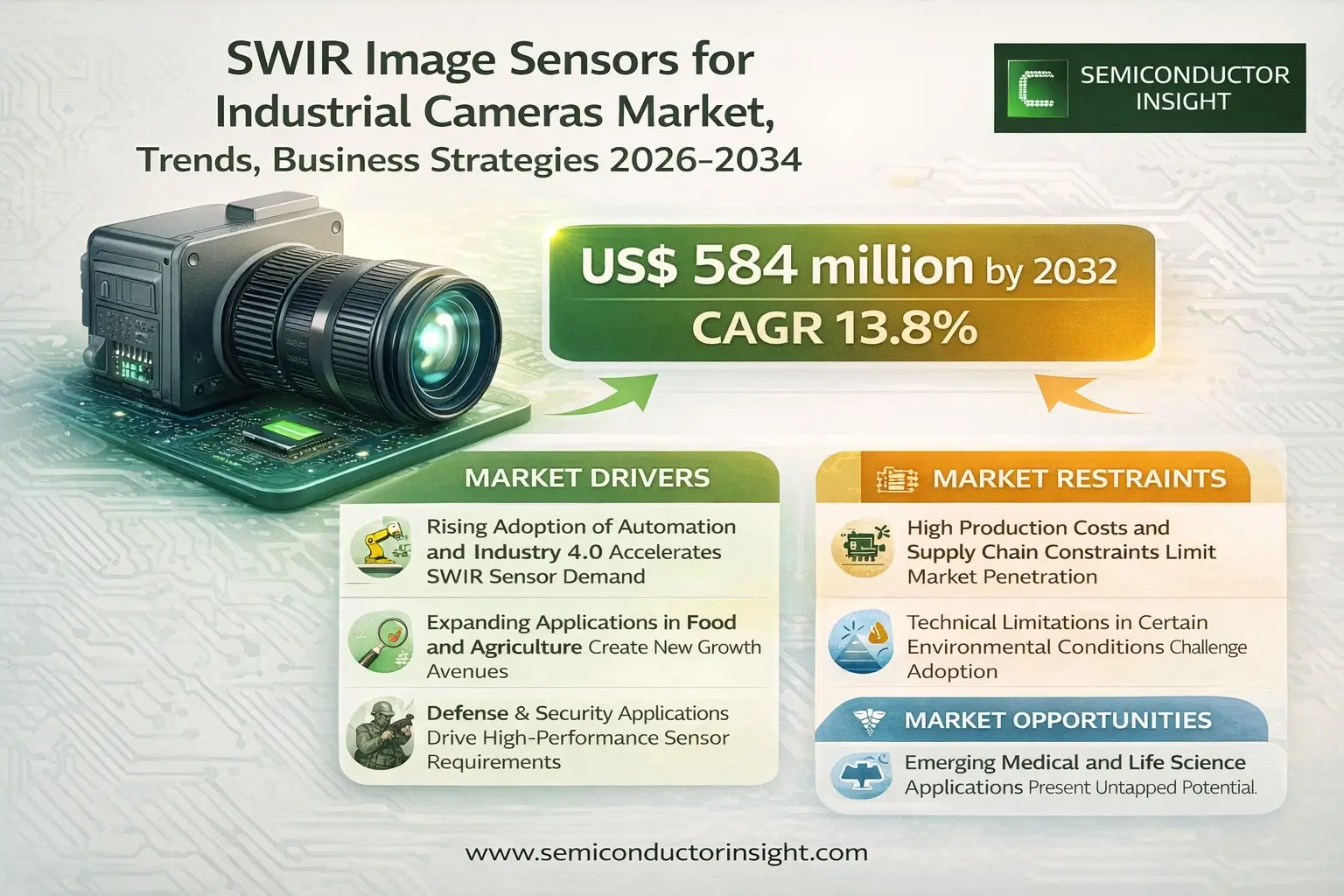

Global SWIR Image Sensors for Industrial Cameras Market was valued at 248 million in 2024 and is projected to reach USD 584 million by 2032, at a CAGR of 13.8% during the forecast period.

SWIR (short-wave infrared) image sensors are specialized semiconductor devices capable of detecting light in the wavelength range of 900 nm to 2500 nm. Unlike traditional visible light sensors, SWIR technology can penetrate materials like silicon, plastics, and smoke while capturing high-resolution images in low-light conditions. These sensors are primarily used in industrial cameras for applications requiring non-destructive testing, quality control, and spectral analysis.

The market growth is driven by increasing industrial automation, stringent quality inspection requirements, and advancements in infrared imaging technologies. The InGaAs sensor segment currently dominates the market due to its superior performance in detecting SWIR wavelengths. Key players like Sony Semiconductor Solutions, Hamamatsu Photonics, and Teledyne are investing heavily in R&D to develop more cost-effective and high-performance SWIR sensors, further accelerating market expansion.

SWIR Image Sensors for Industrial Cameras MARKET DYNAMICS

SWIR Image Sensors for Industrial Cameras MARKET DRIVERS

Rising Adoption of Automation and Industry 4.0 Accelerates SWIR Sensor Demand

The industrial sector’s rapid shift toward automation and smart manufacturing is significantly driving the adoption of SWIR image sensors. With Global Industry 4.0 market expected to grow at over 16% annually until 2030, manufacturers increasingly rely on advanced imaging solutions for quality inspection and process monitoring. SWIR sensors excel in detecting material defects invisible to conventional cameras, with capabilities to identify moisture content, chemical compositions, and thermal variations. In semiconductor manufacturing alone, SWIR-based inspection systems achieve defect detection rates exceeding 98%, far superior to visible-light alternatives. This precision directly translates to reduced waste and higher production yields.

Expanding Applications in Food and Agriculture Create New Growth Avenues

SWIR technology is revolutionizing food safety and agricultural monitoring through its unique material penetration capabilities. The sensors can detect bruising in fruits up to 3mm beneath the surface and identify foreign contaminants in food processing lines with 99.5% accuracy. With global food safety testing expenditures surpassing D 20 billion annually, food processors are rapidly adopting SWIR-based sorting systems. In precision agriculture, these sensors enable real-time crop health monitoring by analyzing water stress and nutrient levels, helping farms optimize irrigation and reduce water usage by 20-30%. This dual industry expansion creates sustained demand for industrial SWIR cameras.

Defense and Security Applications Drive High-Performance Sensor Requirements

Military and security applications account for nearly 35% of the industrial SWIR sensor market due to their superior performance in low-light and obscured conditions. Unlike visible-light cameras, SWIR sensors can see through smoke, fog, and certain camouflage materials while providing high-definition imagery. Border surveillance systems using SWIR technology have demonstrated 40% improvement in intrusion detection rates compared to thermal imaging. Furthermore, the growing global defense expenditure, particularly in unmanned systems and night vision capabilities, continues to fuel demand for advanced SWIR imaging solutions across military and homeland security applications.

SWIR Image Sensors for Industrial Cameras MARKET RESTRAINTS

High Production Costs and Supply Chain Constraints Limit Market Penetration

The specialized materials and manufacturing processes required for SWIR sensors create significant cost barriers. InGaAs-based sensors, which dominate the market, require rare earth elements with complex purification processes, resulting in unit costs 5-8 times higher than conventional CMOS sensors. Recent geopolitical tensions have exacerbated supply chain vulnerabilities, with lead times for critical components extending beyond 12 months in some cases. These factors collectively maintain SWIR systems as premium solutions, restricting adoption among small and mid-sized manufacturers with tighter budgets.

Technical Limitations in Certain Environmental Conditions Challenge Adoption

While SWIR sensors outperform visible-light cameras in many scenarios, they face inherent physical limitations that constrain certain applications. Performance degrades significantly in heavy precipitation, with detection ranges decreasing by 50-60% during rainfall compared to optimal conditions. Additionally, some common industrial materials like certain plastics and glasses exhibit minimal SWIR absorption, creating blind spots in material sorting applications. These technical constraints require careful system design and sometimes hybrid sensor approaches, increasing complexity and cost for end-users.

SWIR Image Sensors for Industrial Cameras MARKET OPPORTUNITIES

Emerging Medical and Life Science Applications Present Untapped Potential

The healthcare sector represents a high-growth frontier for SWIR imaging, with recent studies demonstrating its effectiveness in non-invasive diagnostics. SWIR-based vein visualization systems achieve 92% first-attempt success rates for difficult venous access cases, compared to 65% for traditional methods. Pharmaceutical companies are also adopting SWIR hyperspectral imaging for tablet coating analysis, reducing quality control time by 75%. As medical technology continues advancing toward non-contact diagnostics, SWIR sensors are positioned to enable breakthrough applications in early disease detection and surgical guidance.

Advancements in Sensor Miniaturization Enable New Embedded Applications

Recent breakthroughs in SWIR sensor packaging and integration are creating opportunities in compact industrial systems. New wafer-level packaging techniques have reduced sensor footprints by 40% while improving thermal performance, enabling direct integration into handheld devices and UAVs. This miniaturization trend aligns perfectly with growing demand for portable inspection tools in field service applications and autonomous mobile robots. Industry leaders have already demonstrated prototype systems with SWIR sensors small enough for smartphone integration, suggesting potential for massive consumer-scale adoption in the coming decade.

SWIR Image Sensors for Industrial Cameras MARKET CHALLENGES

Intense Competition from Alternative Technologies Threatens Market Position

SWIR sensors face increasing competition from advancing visible-light and thermal imaging technologies. Recent developments in AI-enhanced visible spectrum cameras now achieve 85% of SWIR performance in material classification tasks at a fraction of the cost. Meanwhile, uncooled thermal sensors have narrowed the resolution gap while offering superior performance in complete darkness. This competitive pressure forces SWIR manufacturers to continually innovate while justifying their premium pricing, particularly in price-sensitive industrial segments where alternative technologies meet minimum requirements.

Regulatory and Standardization Hurdles Impede Market Growth

The lack of unified standards for SWIR imaging creates adoption barriers, particularly in regulated industries. Medical applications face stringent FDA approval processes that can delay commercialization by 12-18 months. In industrial settings, the absence of standardized SWIR-based quality metrics forces manufacturers to develop proprietary inspection criteria, increasing implementation costs. Recent proposals for international SWIR imaging standards show promise but will require multi-year industry collaboration to achieve widespread adoption.

SWIR IMAGE SENSORS FOR INDUSTRIAL CAMERAS MARKET TRENDS

Increasing Adoption of InGaAs Sensors to Emerge as a Dominant Trend

Global SWIR Image Sensors for Industrial Cameras Market for industrial cameras is witnessing significant traction due to the rising adoption of InGaAs (Indium Gallium Arsenide) sensors, which hold the largest market share. These sensors offer high sensitivity in the short-wave infrared spectrum (900-1700 nm) and are increasingly preferred for applications requiring superior resolution and low-light performance. The segment is projected to grow at a compound annual growth rate (CAGR) of over 15% from 2024 to 2032. Recent improvements in InGaAs sensor manufacturing, such as reduced dark current and lower fabrication costs, are further accelerating their deployment in industrial machine vision and quality inspection systems. Additionally, manufacturers are focusing on developing compact and cost-effective InGaAs-based cameras to meet the evolving needs of automation and robotics.

Other Trends

Integration With AI and Machine Learning

The integration of artificial intelligence (AI) and machine learning (ML) algorithms with SWIR imaging systems is revolutionizing industrial automation. AI-powered SWIR cameras enable real-time defect detection, predictive maintenance, and material sorting with higher accuracy than traditional visible-light imaging. Industries such as semiconductor manufacturing and food processing are leveraging these advancements to minimize waste and improve yield rates. For instance, hyperspectral imaging combined with SWIR sensors allows AI models to distinguish between materials with similar visual properties, enhancing sorting efficiency by up to 25%. The increasing availability of edge computing solutions has further strengthened the role of AI in SWIR-based industrial inspections.

Growth in Industrial Automation and Smart Manufacturing

The expansion of Industry 4.0 and smart manufacturing initiatives is a major driver for SWIR image sensors. As factories adopt IoT-connected systems, there is a growing need for sensors capable of operating in challenging environments where dust, smoke, or low visibility may hinder traditional cameras. SWIR sensors are uniquely positioned to address these challenges due to their ability to penetrate certain obscurants. The automotive sector, in particular, is investing heavily in SWIR-based inspection systems for weld quality checks and paint defect detection, with some manufacturers reporting defect detection improvements of up to 40%. Furthermore, the rising deployment of autonomous guided vehicles (AGVs) in warehouses is creating new opportunities for SWIR cameras in obstacle detection and navigation.

Technological Advancements in SWIR Imaging

Technological innovations are broadening the applicability of SWIR image sensors beyond traditional industrial use cases. Enhanced quantum efficiency and pixel size reduction in SWIR sensors are enabling applications in medical imaging and precision agriculture. For example, SWIR cameras are increasingly used in non-invasive diagnostics, such as vein imaging and tissue analysis, where high-resolution infrared imaging provides advantages over conventional methods. In the agricultural sector, SWIR-equipped drones are being deployed for crop health monitoring, with some systems capable of detecting water stress and nutrient deficiencies up to two weeks earlier than visible-spectrum cameras. These advancements are expected to drive demand across diversified industries, contributing to the projected market growth to D 584 million by 2032.

COMPETITIVE LANDSCAPE

Key Industry Players

Technology Leaders Drive Innovation in SWIR Imaging Solutions

Global SWIR Image Sensors for Industrial Cameras Market for industrial cameras features a moderately concentrated competitive environment, dominated by semiconductor giants and specialized imaging technology providers. Sony Semiconductor Solutions Group leads the market with an estimated 28% revenue share in 2024, leveraging its advanced InGaAs sensor technology and strong presence across key industrial markets. The company’s latest IMX990 and IMX991 SWIR sensors have set new benchmarks for resolution and sensitivity in industrial inspection applications.

Hamamatsu Photonics and Teledyne Technologies collectively account for approximately 35% of the market, benefiting from their decades of experience in infrared imaging solutions. Hamamatsu’s G15193 series and Teledyne’s Linea HS32 SWIR cameras are particularly popular in high-speed manufacturing environments where precision is critical.

While these established players dominate the high-performance segment, emerging companies like TriEye are disrupting the market with cost-effective CMOS-based SWIR solutions. TriEye’s proprietary technology reduces production costs by up to 90% compared to traditional InGaAs sensors, potentially democratizing SWIR imaging for broader industrial adoption.

Recently, the competitive intensity has increased as companies expand into adjacent application areas. STMicroelectronics recently partnered with several European machine vision companies to develop integrated SWIR solutions for autonomous quality control systems, while New Imaging Technologies announced a breakthrough in room-temperature SWIR sensor performance that could redefine price-performance ratios in the industrial segment.

List of Key SWIR Image Sensor Companies Profiled

- Sony Semiconductor Solutions Group (Japan)

- STMicroelectronics (Switzerland)

- Hamamatsu Photonics (Japan)

- Teledyne Technologies (U.S.)

- TriEye (Israel)

- New Imaging Technologies (France)

- Sensors Unlimited (U.S.)

- Xenics (Belgium)

- Princeton Infrared Technologies (U.S.)

Segment Analysis:

By Type

InGaAs Sensor Segment Leads the Market Due to Superior Performance in Low-Light Conditions

The market is segmented based on type into:

- InGaAs Sensor

- HgCdTe Sensor

By Application

Manufacturing Segment Dominates Owing to Widespread Use in Quality Control and Inspection

The market is segmented based on application into:

- Manufacturing

- Security

- Medical

- Intelligent Transportation Systems

- Other

Regional Analysis: SWIR Image Sensors for Industrial Cameras Market

Asia-Pacific

The Asia-Pacific region leads Global SWIR Image Sensors for Industrial Cameras Market , driven by rapid industrialization and technological advancements. China, Japan, and South Korea dominate the market due to strong semiconductor manufacturing capabilities and extensive adoption of automation in industries like electronics manufacturing and automotive. The region benefits from significant government investments in Industry 4.0 initiatives, further accelerating demand for SWIR-based industrial cameras. However, cost sensitivity in emerging economies like India and Southeast Asian countries creates price competition among suppliers. The shift toward smart manufacturing and quality control applications continues to fuel market expansion, with China alone accounting for over 35% of the regional market share.

North America

North America remains a high-growth market for SWIR image sensors, particularly in defense, aerospace, and medical imaging applications. The U.S. leads adoption due to stringent industrial inspection standards and R&D investments in advanced sensing technologies. Government contracts in surveillance and military applications contribute significantly to market growth, with companies like Teledyne and FLIR Systems driving innovation. However, the high cost of InGaAs-based sensors restrains broader adoption in price-sensitive industries. The region shows strong potential for AI-integrated SWIR imaging solutions, aligning with the growing demand for industrial automation and predictive maintenance systems.

Europe

European demand for SWIR image sensors is largely driven by automotive manufacturing and environmental monitoring applications. Germany leads the region with its strong industrial base and focus on precision engineering. Strict EU regulations on industrial emissions monitoring create sustained demand for hyperspectral imaging solutions. While the market remains technologically advanced, growth is somewhat constrained by the fragmentation of industrial standards across member states. Key players like STMicroelectronics and Xenics are actively developing lower-cost SWIR solutions to penetrate small and medium enterprises in the manufacturing sector.

Middle East & Africa

This emerging market shows promising growth potential, particularly in oil and gas pipeline inspection and border security applications. Countries like Israel and Saudi Arabia are adopting SWIR technology for military and infrastructure monitoring purposes. However, limited local manufacturing capabilities and reliance on imported components create supply chain challenges. The market is gradually evolving with increasing foreign investments in industrial automation, though widespread adoption remains constrained by budget limitations and lack of technical expertise in advanced imaging systems.

South America

The South American market presents niche opportunities, primarily in mining and agricultural inspection applications. Brazil and Argentina show gradual adoption of SWIR sensors for food quality monitoring and mineral exploration. Economic instability and currency fluctuations continue to hinder large-scale investments in advanced imaging technologies. While the market exhibits long-term potential, growth is expected to remain modest compared to other regions due to limited industrial modernization initiatives and weaker technology infrastructure.

Report Scope

This market research report provides a comprehensive analysis of Global SWIR Image Sensors for Industrial Cameras Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. Global market was valued at USD 248 million in 2024 and is projected to reach USD 584 million by 2032, growing at a CAGR of 13.8%.

- Segmentation Analysis: Detailed breakdown by product type (InGaAs Sensor, HgCdTe Sensor), application (Manufacturing, Security, Medical, Intelligent Transportation Systems, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. The U.S. and China are key markets with significant growth potential.

- Competitive Landscape: Profiles of leading market participants including Sony Semiconductor Solutions Group, STMicroelectronics, Hamamatsu Photonics, Teledyne, TriEye, and New Imaging Technologies, covering their product portfolios and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging SWIR sensor technologies, integration with AI/ML for industrial imaging, and advancements in semiconductor materials.

- Market Drivers & Restraints: Analysis of factors such as increasing industrial automation, demand for quality inspection, and challenges like high production costs.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, industrial camera OEMs, system integrators, and investors.

The research methodology combines primary interviews with industry experts and analysis of verified market data from reliable sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global SWIR Image Sensors for Industrial Cameras Market?

-> SWIR Image Sensors for Industrial Cameras Market was valued at 248 million in 2024 and is projected to reach USD 584 million by 2032, at a CAGR of 13.8% during the forecast period.

Which key companies operate in this market?

-> Key players include Sony Semiconductor Solutions Group, STMicroelectronics, Hamamatsu Photonics, Teledyne, TriEye, and New Imaging Technologies.

What are the key growth drivers?

-> Key growth drivers include increasing industrial automation, demand for advanced inspection systems, and adoption in security & surveillance applications.

Which region dominates the market?

-> Asia-Pacific shows the highest growth potential, while North America currently holds significant market share.

What are the emerging trends?

-> Emerging trends include miniaturization of sensors, higher resolution SWIR imaging, and integration with AI for industrial quality control.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...