Sub-harmonic mixer for 60 GHz down-conversion Market Insights

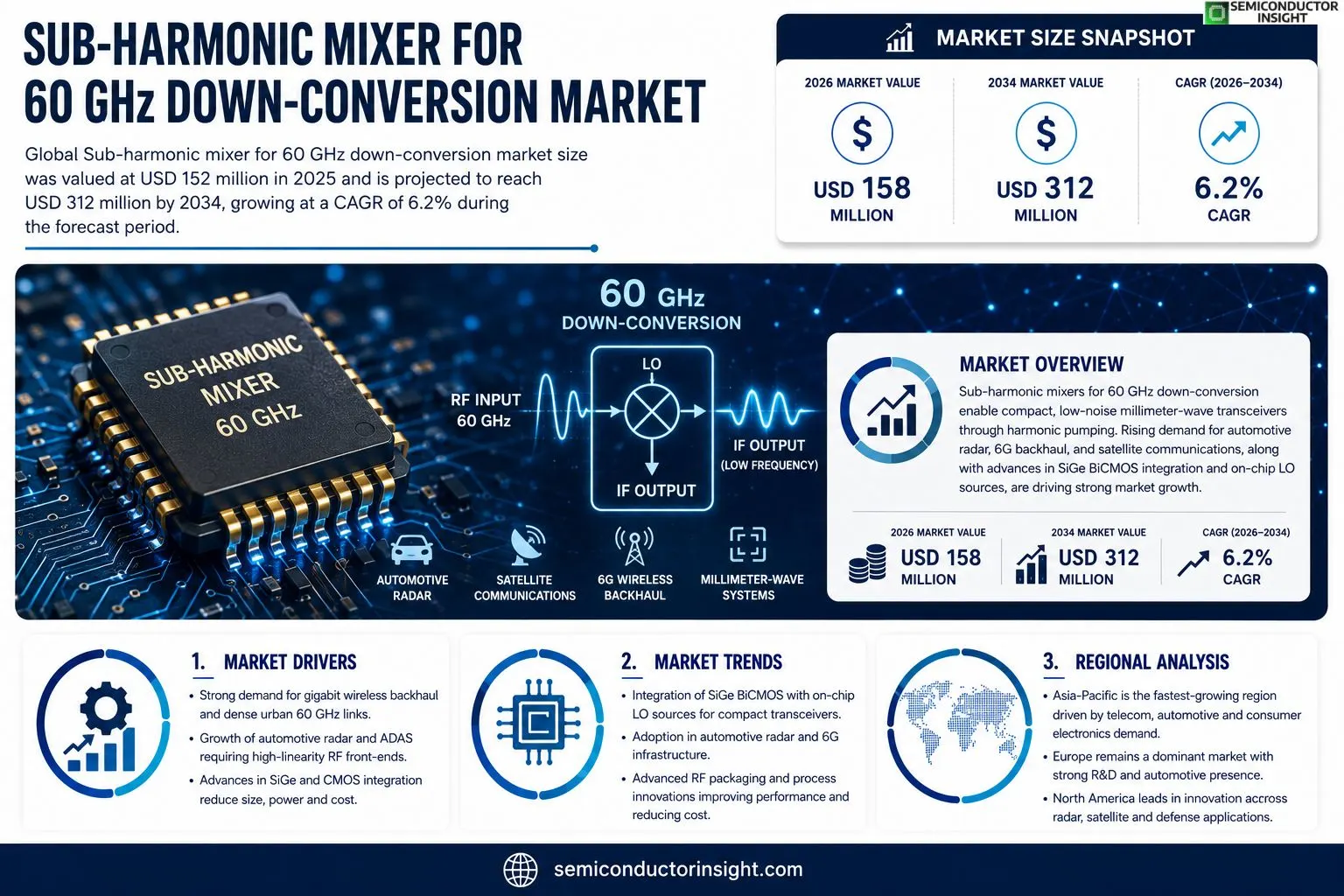

Sub-harmonic mixer for 60 GHz down-conversion market size was valued at USD 152 million in 2025. The market is projected to grow from USD 158 million in 2026 to USD 312 million by 2034, exhibiting a CAGR of 6.2% during the forecast period.

Sub‑harmonic mixers for 60 GHz down‑conversion are specialized RF components that translate high‑frequency signals to lower intermediate frequencies using harmonic pumping. This technique enables compact millimeter‑wave transceiver architectures essential for automotive radar, satellite communications, and emerging 6G backhaul links.The market is experiencing rapid growth because demand for high‑resolution automotive radar and gigabit wireless backhaul is increasing; however, challenges such as stringent phase‑noise requirements persist. Furthermore, advances in SiGe BiCMOS processes and integration of on‑chip local‑oscillator sources are driving cost reductions, while key players like Analog Devices, Qorvo, NXP Semiconductors, and Skyworks are expanding their portfolios through strategic collaborations and technology roadmaps.

MARKET DRIVERS

Increasing Demand for High‑Frequency Wireless Backhaul

Sub‑harmonic mixer for 60 GHz down‑conversion Market is being propelled by telecom operators upgrading to millimeter‑wave backhaul links that support multi‑gigabit per second data rates. Network planners cite a 30 % year‑over‑year growth in 60 GHz deployments for dense urban environments, driving immediate procurement of reliable mixers.

Advances in Silicon‑Based RF Integration

Recent breakthroughs in SiGe and CMOS processes have lowered the cost of integrating sub‑harmonic mixers with other RF front‑end components. This consolidation reduces board space by up to 40 % and improves thermal performance, making the technology attractive for both 5G base stations and satellite terminal manufacturers.

➤ The rapid adoption of 5G and low‑Earth‑orbit satellite constellations accelerates mixer development cycles, creating a compounding effect on market demand.

Furthermore, automotive manufacturers are exploring 60 GHz radar for advanced driver‑assistance systems, adding a new vertical that relies on high‑linearity sub‑harmonic mixers to achieve precise range detection under challenging conditions.

MARKET CHALLENGES

Manufacturing Complexity at Millimeter‑Wave Frequencies

Producing mixers that operate efficiently at 60 GHz requires sub‑micron lithography and tight control of parasitic elements. Small variations in line width can cause > 5 dB degradation in conversion loss, leading to higher reject rates and increased unit costs.

Other Challenges

Supply Chain Constraints

The recent semiconductor wafer shortage has limited the availability of high‑quality GaAs and SiGe substrates, extending lead times for key components and pressuring OEMs to hold larger safety stocks.

MARKET RESTRAINTS

Stringent Regulatory Requirements

Regulators in North America and Europe impose strict out‑of‑band emission limits for devices operating near 60 GHz, necessitating additional filtering and testing. Compliance costs can add up to 15 % of a product’s total bill of materials, discouraging some low‑margin manufacturers.Moreover, certification processes for automotive radar modules often require multiple iterative assessments, prolonging time‑to‑market and reducing the attractiveness of new mixer designs for fast‑moving consumer segments.These regulatory hurdles, combined with the need for high‑precision calibration, act as a restraint on rapid market expansion despite strong demand signals.

MARKET OPPORTUNITIES

Emerging Applications in Autonomous Vehicles

Autonomous driving systems are beginning to integrate 60 GHz radar for high‑resolution object detection, creating a niche where sub‑harmonic mixers can deliver superior linearity and low noise. Forecasts suggest a 12 % CAGR for radar‑centric mixer sales over the next five years.In addition, satellite broadband providers targeting high‑throughput links are evaluating compact mixer modules to reduce payload weight. The resulting demand for lightweight, power‑efficient mixers opens a clear growth avenue for specialized silicon‑based designs.Finally, research collaborations between universities and chipset manufacturers are exploring novel materials such as graphene, which could further enhance mixer performance and unlock new market segments beyond traditional telecom.

Sub-harmonic mixer for 60 GHz down-conversion Market Trends

Accelerated Adoption in Automotive Radar and 6G Backhaul

Sub‑harmonic mixer for 60 GHz down‑conversion Market is witnessing a notable acceleration as vehicle manufacturers push for higher‑resolution radar systems. Millimeter‑wave radar architectures that rely on sub‑harmonic mixing enable compact, low‑power transceivers, which satisfy the stringent size and weight constraints of modern automotive designs. At the same time, telecom operators are deploying gigabit‑class backhaul links that operate in the 60 GHz band, creating parallel demand for reliable frequency‑conversion solutions. Industry analysts observe that the convergence of automotive safety requirements and emerging 6G infrastructure is forming a dual‑market catalyst that sustains steady demand growth.

Other Trends

Technology Integration Advances

Advances in SiGe BiCMOS processes are simplifying the integration of sub‑harmonic mixers with on‑chip local‑oscillator sources. This integration reduces bill‑of‑materials cost and improves phase‑noise performance, addressing a key technical hurdle for high‑frequency applications. Moreover, the shift toward heterogeneous integration allows designers to combine passive and active RF blocks on a single substrate, further shrinking the footprint of 60 GHz transceivers. These technological strides are expected to lower entry barriers for new entrants and stimulate broader ecosystem participation.

Competitive Landscape and Strategic Partnerships

Major semiconductor firms such as Analog Devices, Qorvo, NXP Semiconductors, and Skyworks are reinforcing their market positions through targeted collaborations with foundries and system‑level OEMs. Joint roadmaps focusing on next‑generation SiGe platforms and standardized RF module specifications are emerging as a common strategy. By aligning product development cycles with automotive OEM timelines and telecom rollout schedules, these players are able to deliver differentiated mixer solutions that meet both performance and cost objectives. The competitive environment is thus characterized by a blend of technology‑driven differentiation and partnership‑enabled market expansion.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Landscape of Sub‑harmonic Mixer for 60 GHz Down‑Conversion Market

The Sub‑harmonic mixer segment for 60 GHz down‑conversion is anchored by a handful of large‑scale semiconductor firms that command the majority of revenue. Analog Devices, Qorvo, and NXP Semiconductors lead the market through extensive RF product portfolios, deep SiGe BiCMOS expertise, and strategic alliances with automotive OEMs. Their offerings integrate on‑chip local‑oscillator sources and advanced packaging, enabling cost‑effective, high‑performance mixers that satisfy the stringent phase‑noise and linearity requirements of automotive radar and emerging 6G backhaul links. This concentration of capability creates a tiered structure where Tier‑1 players supply complete mixer solutions, while a selective group of Tier‑2 suppliers provide specialty components or niche process technologies.Beyond the dominant trio, a diverse set of niche innovators enriches the ecosystem. Skyworks Solutions and Infineon Technologies focus on compact, low‑power designs for satellite communications, while Texas Instruments leverages its broad RF foundry services to support custom mixer development. MACOM, STMicroelectronics, and Broadcom contribute differentiated technologies such as gallium‑arsenide and silicon‑photonic integration. Murata Manufacturing, MediaTek, and Renesas Electronics round out the competitive field by delivering highly integrated modules and system‑on‑chip solutions that address specific automotive radar segments and high‑frequency wireless backhaul use cases. Collectively, these players drive incremental performance gains, sustain supply‑chain resilience, and expand the addressable market for 60 GHz sub‑harmonic mixers.

List of Key Sub‑harmonic Mixer for 60 GHz Down‑Conversion Companies Profiled

- Analog Devices

- Qorvo

- NXP Semiconductors

- Skyworks Solutions

- Infineon Technologies

- Texas Instruments

- MACOM

- STMicroelectronics

- Broadcom

- Murata Manufacturing

- MediaTek

- Renesas Electronics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

SiGe BiCMOS drives market momentum because it balances low noise performance with scalable integration.

|

| By Application |

|

Automotive radar remains the leading application as manufacturers pursue higher resolution and longer detection ranges.

|

| By End User |

|

Automotive OEMs drive the segment because of regulatory push toward advanced driver assistance and autonomous systems.

|

| By Manufacturing Process |

|

Monolithic integration is gaining traction as design teams aim for size, weight and power efficiency.

|

| By System Architecture |

|

Balanced architectures are preferred for high‑performance radar and backhaul because they deliver superior conversion gain and suppression of undesired spurs.

|

Regional Analysis: Sub-harmonic mixer for 60 GHz down-conversion Market

North America

The push for higher bandwidth in wireless backhaul and autonomous vehicle sensors drives demand for stable, low‑noise mixers. Industry collaborations target seamless integration of 60 GHz modules, emphasizing thermal management and linearity, which in turn accelerates product roll‑outs across telecom and defense sectors.

FCC allocations for millimeter‑wave spectrum provide a clear framework that encourages investment. Ongoing spectrum harmonization efforts across North America simplify cross‑border deployment, reducing time‑to‑market for Sub‑harmonic mixer solutions and fostering a unified standards environment.

Silicon‑on‑insulator (SOI) and CMOS processes are increasingly leveraged to deliver cost‑effective mixers without sacrificing performance. Early adoption by network equipment vendors highlights the region’s readiness to transition from prototype to volume production.

A handful of established players dominate, yet emerging start‑ups focus on niche applications such as aerospace telemetry. Strategic acquisitions and joint ventures are common, reinforcing North America’s role as the primary arena for competitive innovation in this market.

Europe

Europe’s Sub‑harmonic mixer for 60 GHz down‑conversion Market is shaped by strong governmental funding for 6G research and a mature automotive ecosystem. Collaborative projects under the Horizon Europe programme foster cross‑border technology sharing, while stringent EMC regulations drive designers toward high‑precision, low‑spurious solutions. Key hubs in Germany, France, and the UK host supplier clusters that specialize in RF front‑end components, enabling rapid prototyping for satellite communications and industrial IoT use cases. Market participants benefit from a well‑established supply chain and a focus on sustainability, prompting the development of energy‑efficient mixers that align with EU Green Deal objectives.

Asia‑Pacific

Asia‑Pacific exhibits rapid growth potential as manufacturers accelerate mass production of millimeter‑wave devices for telecom infrastructure and consumer electronics. Countries such as China, South Korea, and Japan invest heavily in advanced semiconductor fabrication, driving cost reductions and enabling broader adoption of Sub‑harmonic mixers. Market dynamics are influenced by aggressive rollout of 5G networks and early trials of 6G, creating demand for compact, high‑performance mixers in dense urban environments. Supplier ecosystems benefit from strong export orientation, positioning the region as a key source of both component innovation and volume supply.

South America

South America’s market remains nascent, with growth anchored in regional telecom operators upgrading to high‑frequency backhaul solutions. Brazil leads initiatives to localize component design, supported by university research programs focused on millimeter‑wave technologies. While capital investment is modest compared to other regions, partnerships with North American firms facilitate technology transfer, gradually building a domestic capability for Sub‑harmonic mixer development and integration into emerging smart city projects.

Middle East & Africa

In the Middle East & Africa, market activity centers on satellite communications and defense applications that demand reliable frequency conversion at 60 GHz. Emerging economies such as the United Arab Emirates and South Africa are establishing test‑beds for high‑frequency radar and telemetry, driving modest demand for specialized mixers. Collaborative agreements with vendors enable local engineering teams to acquire expertise, laying the groundwork for future expansion as regional infrastructure projects adopt advanced wireless solutions.

Report Scope

This market research report provides a comprehensive analysis of the Sub-harmonic mixer for 60 GHz down-conversion Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Sub-harmonic mixer for 60 GHz down-conversion Market?

-> Sub-harmonic mixer for 60 GHz down-conversion Market was valued at USD 152 million in 2025 and is expected to reach USD 312 million by 2034, exhibiting a CAGR of 6.2% during the forecast period.

Which key companies operate in Sub-harmonic mixer for 60 GHz down-conversion Market?

-> Key players include Analog Devices, Qorvo, NXP Semiconductors, Skyworks, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for high‑resolution automotive radar, gigabit wireless backhaul, and emerging 6G millimeter‑wave applications.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include integration of SiGe BiCMOS processes, on‑chip local‑oscillator sources, and advanced RF packaging to reduce cost and improve performance.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...