MARKET INSIGHTS

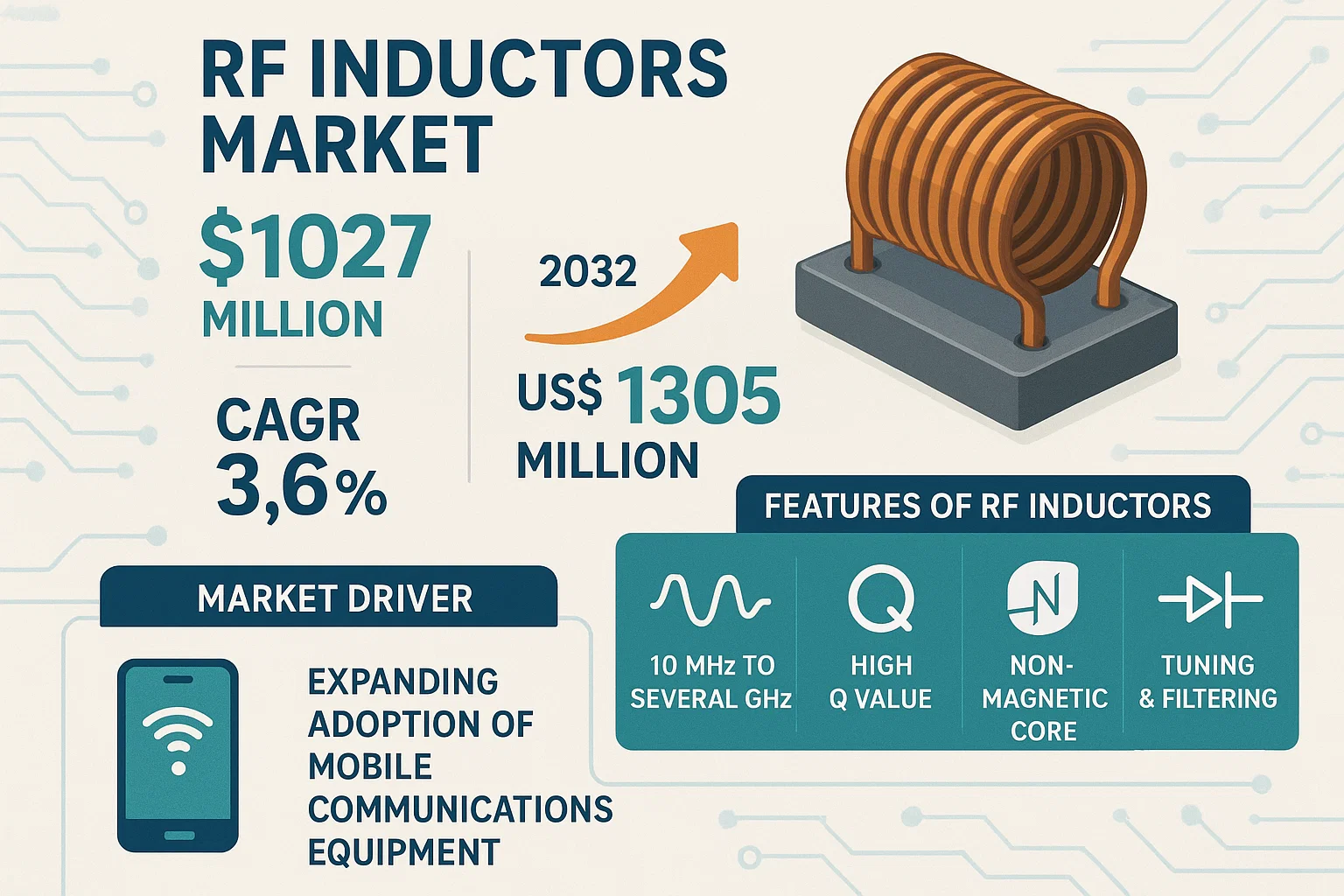

The global RF Inductors market was valued at 1027 million in 2024 and is projected to reach US$ 1305 million by 2032, at a CAGR of 3.6% during the forecast period.

RF inductors are passive electronic components specifically designed for high-frequency circuits operating in the range from 10 MHz to several GHz. These components are characterized by their high Quality factor (Q value) and predominantly feature a non-magnetic core structure to minimize energy losses. They are fundamental in tuning, filtering, impedance matching, and noise suppression within radio frequency applications.

The market’s steady growth is primarily driven by the expanding adoption of mobile communications equipment, including smartphones and wireless LAN devices. Furthermore, the rapid deployment of 5G infrastructure and the increasing electronic content in automotive and consumer electronics are significant contributors. The market is highly concentrated, with the top six players, including Murata, TDK, and Taiyo Yuden, collectively holding approximately 60% of the global market share. Geographically, China dominates as the largest market, accounting for over 50% of global demand, fueled by its massive electronics manufacturing sector.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of 5G Infrastructure and Smart Devices to Accelerate Market Expansion

The global rollout of 5G technology represents a primary catalyst for the RF inductors market. 5G networks require a significantly higher density of base stations and small cells compared to previous generations, each demanding advanced RF components for signal filtering, impedance matching, and noise suppression. The transition to higher frequency bands, including millimeter-wave spectrum, necessitates components with superior high-frequency performance, where RF inductors are critical. This infrastructure build-out, coupled with the increasing integration of 5G modems into smartphones, IoT devices, and automotive systems, creates sustained demand. The number of 5G subscriptions worldwide is projected to exceed 5 billion by the end of the decade, underscoring the massive scale of this driver and its direct impact on component markets.

Growing Automotive Electronics and Electrification to Fuel Demand

The automotive industry’s rapid transformation towards electrification, advanced driver-assistance systems (ADAS), and in-vehicle connectivity is a significant growth engine for RF inductors. Modern vehicles incorporate a vast array of electronic control units, infotainment systems, radar, LiDAR, and V2X communication modules, all of which rely on high-frequency circuits. The shift to electric vehicles further amplifies this demand, as power management systems and battery monitoring require robust RF filtering to ensure electromagnetic compatibility and prevent interference. With global sales of electric vehicles consistently breaking records and the average electronic content per vehicle rising substantially, the automotive segment has become a major and growing consumer of high-performance RF inductors.

Expansion of Internet of Things and Wearable Technology to Boost Market Growth

The explosive growth of the Internet of Things (IoT) ecosystem and wearable technology is providing a substantial and diverse demand stream for RF inductors. Billions of connected devices, from smart home sensors and industrial monitors to health and fitness trackers, require compact, efficient, and high-performance RF components for wireless communication via protocols like Wi-Fi, Bluetooth, Zigbee, and LoRa. The miniaturization trend in these applications pushes the development of smaller, surface-mount inductor designs with maintained Q factors. The sheer volume of units shipped annually in these categories ensures a high-volume, cost-sensitive market that continues to drive innovation and production scale for component manufacturers.

MARKET RESTRAINTS

Intense Price Pressure and Miniaturization Challenges to Limit Profitability

The RF inductors market operates under constant and intense price pressure, particularly for high-volume consumer electronics applications. Manufacturers are compelled to continuously reduce costs while simultaneously enhancing performance characteristics like Q factor, self-resonant frequency, and current handling capacity. This pressure is exacerbated by the trend towards extreme miniaturization, as designing and producing components like multilayer chip inductors at sub-0201 sizes requires advanced manufacturing techniques and materials, which can increase production costs. Achieving high performance in a smaller footprint often involves more expensive materials and more complex processes, creating a challenging economic environment where balancing performance, size, and cost becomes a critical restraint on profitability and market expansion.

Complex Supply Chain and Material Availability to Hinder Production Stability

The manufacturing of high-quality RF inductors is dependent on a stable supply of specialized raw materials, including specific ferrite compositions, ceramic substrates, and precious metals for electrodes and terminations. Global supply chain disruptions, geopolitical tensions affecting material sourcing, and price volatility for these inputs can significantly impact production lead times and costs. Furthermore, the advanced equipment required for precision winding, layering, and sintering represents a substantial capital investment. Any disruption in the availability of key manufacturing machinery or its maintenance can constrain production capacity. This reliance on a complex and sometimes fragile supply ecosystem acts as a significant restraint, making the market vulnerable to external shocks and limiting the ability to quickly scale production to meet surging demand.

Technical Design Complexity for High-Frequency Applications to Deter Market Penetration

As wireless systems advance into higher frequency bands, the design and integration of RF inductors become exponentially more complex. At frequencies above several gigahertz, parasitic effects such as parasitic capacitance and skin effect become pronounced, degrading the performance of the inductor and the overall circuit. Designing inductors that maintain a high Q factor and precise inductance values at these frequencies requires sophisticated electromagnetic simulation tools and highly experienced RF design engineers. This high barrier to entry in terms of technical expertise and design resources can deter smaller companies from developing cutting-edge products and can slow down the adoption of new technologies, acting as a restraint on the overall growth and innovation pace within the market.

MARKET CHALLENGES

Meeting Stringent Performance Specifications for Next-Generation Applications

The market faces the ongoing challenge of developing RF inductors that meet the increasingly stringent performance requirements of next-generation communication standards. Applications in 5G millimeter-wave bands and automotive radar systems demand components with exceptionally high Q factors, very tight inductance tolerances, and ultra-low equivalent series resistance (ESR) to minimize signal loss and heat generation. Achieving these specifications consistently in mass production, while also adhering to demanding automotive-grade reliability standards like AEC-Q200, requires immense precision in material science and manufacturing control. Even minor variations in material composition or processing parameters can lead to batch failures, making quality control a paramount and costly challenge for manufacturers aiming to serve these high-performance segments.

Other Challenges

Rapid Technological Obsolescence

The fast-paced evolution of wireless standards and device form factors presents a persistent challenge of rapid technological obsolescence. Product life cycles are shortening, and inductor manufacturers must continuously invest in research and development to create new products that are compatible with emerging protocols and fit into ever-smaller spaces. This requires not only financial investment but also the agility to pivot production lines quickly, risking inventory becoming outdated if market adoption of a new technology slows or changes direction.

Intense Global Competition

The market is characterized by intense global competition from both established multinational giants and emerging low-cost manufacturers. This competition puts continuous pressure on pricing and forces companies to differentiate through performance, reliability, and customer service rather than cost alone. Navigating different regional market demands, regulatory environments, and competitive landscapes requires a sophisticated global strategy, which can be a significant challenge for mid-sized players.

MARKET OPPORTUNITIES

Emergence of 6G Research and Satellite Communication to Open New Frontiers

While 5G deployment is ongoing, early research and development into 6G technology and the rapid growth of low-earth orbit (LEO) satellite communication networks like Starlink present groundbreaking opportunities. These next-generation systems are expected to operate in terahertz frequency ranges and require entirely new classes of RF components with unprecedented performance metrics. RF inductor manufacturers that invest in foundational research for these future applications can position themselves as technology leaders. Furthermore, the infrastructure for global satellite internet requires ground terminals, user equipment, and the satellites themselves, all of which will need robust and reliable RF components, creating a new and high-value market segment beyond traditional terrestrial networks.

Advancements in Integrated Passive Devices and Embedded Components to Offer Growth Avenues

The trend towards greater integration and miniaturization in electronics is driving the development of Integrated Passive Devices (IPDs) and embedded components, where inductors, resistors, and capacitors are fabricated directly into the substrate of a package or printed circuit board. This approach saves valuable board space, improves electrical performance by reducing parasitic interconnections, and enhances reliability. For RF inductor providers, this represents a significant opportunity to move up the value chain by offering integrated solutions rather than discrete components. Mastering the technologies to embed high-Q inductors into organic or silicon-based substrates allows companies to cater to the most advanced and space-constrained applications in smartphones, wearables, and medical implants.

Strategic Expansion into High-Growth Regional Markets and Verticals to Diversify Revenue

Significant opportunities exist for companies to strategically expand their presence in high-growth regional markets and emerging industry verticals. The Asia-Pacific region, particularly China, already dominates consumption and manufacturing, but Southeast Asian countries are rapidly developing their electronics manufacturing capabilities. Establishing production or strong distribution channels in these evolving markets can capture new growth. Similarly, beyond consumer electronics and automotive, new verticals like industrial IoT, renewable energy systems, and advanced medical equipment are increasingly utilizing wireless connectivity, creating fresh demand streams for reliable RF components. Companies that can successfully diversify their customer base across these new geographies and industries can build a more resilient and growing business model.

RF INDUCTORS MARKET TRENDS

Proliferation of 5G Infrastructure and Mobile Devices Driving Market Expansion

The global rollout of 5G networks represents a primary catalyst for the RF inductors market, as these components are essential for filtering, impedance matching, and signal integrity in high-frequency circuits. The increasing number of 5G base stations worldwide, coupled with the rising adoption of 5G-enabled smartphones, directly fuels demand. For instance, global 5G smartphone shipments surpassed 600 million units in 2023, requiring advanced RF front-end modules that utilize multiple high-performance inductors. Furthermore, the expansion of IoT and smart devices operating on cellular and Wi-Fi 6/6E standards necessitates compact, efficient RF inductors with high quality factors (Q) to minimize signal loss and power consumption. This trend is further amplified by the ongoing miniaturization of electronic components, pushing manufacturers to develop smaller form factors without sacrificing performance.

Other Trends

Automotive Electronics and Electrification

The automotive sector is emerging as a significant growth area for RF inductors, driven by the increasing integration of advanced driver-assistance systems (ADAS), vehicle-to-everything (V2X) communication, and infotainment systems. Modern vehicles now incorporate numerous wireless modules for GPS, cellular connectivity, and radar systems, each requiring stable RF performance in harsh operating environments. The transition towards electric vehicles (EVs) also contributes to this demand, as these vehicles rely heavily on sophisticated electronics for battery management and connectivity. With the global automotive electronics market projected to maintain strong growth, the need for reliable, high-temperature-rated RF inductors is expected to rise correspondingly.

Technological Advancements in Component Design and Materials

Innovation in materials science and manufacturing processes is a key trend shaping the competitive landscape of the RF inductors market. There is a continuous push towards developing inductors with higher self-resonant frequencies and improved Q factors to meet the demands of next-generation communication standards, such as 5G mmWave and upcoming 6G technologies. Manufacturers are increasingly utilizing novel core materials and advanced multilayer techniques to achieve better performance in smaller packages. This is particularly critical for applications in space-constrained portable devices and infrastructure equipment. Additionally, the industry is focusing on enhancing the power handling capacity and temperature stability of these components to cater to high-power RF applications and automotive use cases, ensuring reliability under strenuous conditions.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Focus on Technological Innovation and Geographic Expansion to Maintain Market Position

The global RF inductors market exhibits a semi-consolidated structure, dominated by a handful of major players while accommodating numerous medium and smaller specialized manufacturers. Murata Manufacturing Co., Ltd. stands as the undisputed market leader, commanding a significant share due to its extensive product portfolio covering multilayer, film, and wire-wound inductors, coupled with its robust manufacturing presence across Asia, North America, and Europe. The company’s technological leadership in miniaturization and high-frequency performance solidifies its position in key applications like smartphones and wireless communication modules.

TDK Corporation and Taiyo Yuden Co., Ltd. are other pivotal players, collectively holding a substantial portion of the global market. Their growth is propelled by continuous investments in R&D for advanced materials and manufacturing processes, enabling them to meet the evolving demands for higher quality factors (Q) and smaller form factors. These companies maintain strong relationships with major consumer electronics and automotive OEMs, ensuring consistent demand.

Furthermore, strategic initiatives such as capacity expansions in high-growth regions like China and Southeast Asia, along with new product launches tailored for 5G infrastructure and Internet of Things (IoT) devices, are expected to further augment their market shares. Coilcraft, Inc. distinguishes itself through a strong focus on high-performance, custom-designed inductors for specialized applications, carving out a significant niche in the North American and European markets.

Meanwhile, companies like Vishay Intertechnology, Inc. and Samsung Electro-Mechanics are strengthening their competitive stance through strategic acquisitions, partnerships with technology firms, and significant enhancements to their production capabilities. Their efforts are concentrated on developing inductors with improved efficiency and thermal stability, particularly for the automotive and telecommunications sectors, ensuring their relevance in a rapidly advancing technological landscape.

List of Key RF Inductors Companies Profiled

- Murata Manufacturing Co., Ltd. (Japan)

- TDK Corporation (Japan)

- Taiyo Yuden Co., Ltd. (Japan)

- Coilcraft, Inc. (U.S.)

- Delta Electronics, Inc. (Taiwan)

- Chilisin Electronics Corp. (Taiwan)

- Vishay Intertechnology, Inc. (U.S.)

- Sunlord Electronics Co., Ltd. (China)

- Samsung Electro-Mechanics (South Korea)

- AVX Corporation (U.S.)

- TOKEN Electronics Co., Ltd. (Taiwan)

- Eaton Corporation plc (Ireland)

- Würth Elektronik GmbH & Co. KG (Germany)

- Laird Performance Materials (U.K.)

- Viking Tech Corporation (Taiwan)

- Johanson Technology, Inc. (U.S.)

- API Delevan, Inc. (U.S.)

- Agile Magnetics, Inc. (U.S.)

- Precision Incorporated (U.S.)

Segment Analysis:

By Type

Multilayer RF Inductors Segment Dominates the Market Due to Superior Performance in High-Frequency Applications

The market is segmented based on type into:

- Wire Wound RF Inductors

- Film RF Inductors

- Multilayer RF Inductors

By Application

Mobile Phone Segment Leads Due to Pervasive Integration in Modern Smartphones and 5G Devices

The market is segmented based on application into:

- Mobile Phone

- Consumer Electronics

- Automotive

- Communication Systems

- Others

By Core Type

Non-Magnetic Core Segment Holds Significant Share Owing to Essential High Q Factor Requirements

The market is segmented based on core type into:

- Air Core

- Ferrite Core

- Ceramic Core

- Non-Magnetic Core

By Frequency Range

High-Frequency Segment (Above 1 GHz) Gains Traction Driven by 5G and Advanced Wireless Communication Needs

The market is segmented based on frequency range into:

- Low Frequency (Below 100 MHz)

- Medium Frequency (100 MHz to 1 GHz)

- High Frequency (Above 1 GHz)

Regional Analysis: RF Inductors Market

Asia-Pacific

The Asia-Pacific region dominates the global RF inductors market, accounting for over 50% of total consumption, with China being the single largest market globally. This dominance is driven by the region’s massive electronics manufacturing ecosystem, particularly for mobile phones, consumer electronics, and communication systems. China’s position as the world’s factory for consumer electronics, coupled with significant domestic demand, creates immense volume requirements for RF components. Countries like Japan and South Korea contribute through their advanced technological capabilities and presence of key players like Murata, TDK, and Taiyo Yuden. While cost sensitivity remains a factor, driving demand for multilayer and film-type inductors, there is a clear trend toward higher-performance components to support 5G infrastructure, IoT devices, and advanced automotive electronics. The region benefits from strong government support for technology development and extensive supply chain integration.

North America

North America represents a technologically advanced and high-value market for RF inductors, characterized by strong demand from the telecommunications, automotive, and aerospace sectors. The region’s focus on innovation and early adoption of next-generation technologies, such as 5G networks and advanced driver-assistance systems (ADAS), drives demand for high-performance, miniaturized inductors with superior quality factors. The presence of leading technology companies and robust R&D investments supports the adoption of advanced multilayer and film-type RF inductors. While manufacturing volume is lower compared to Asia-Pacific, the region emphasizes quality, reliability, and compliance with stringent technical standards. The United States is the largest market within the region, with significant contributions from Canada and Mexico, particularly in automotive and industrial applications.

Europe

Europe maintains a strong position in the RF inductors market, supported by its advanced automotive industry, industrial automation, and telecommunications infrastructure. The region’s emphasis on quality and precision engineering aligns with the demand for high-reliability components used in automotive electronics, medical devices, and industrial communication systems. Germany, France, and the U.K. are key markets, driven by their automotive sectors and ongoing investments in Industry 4.0 and IoT. Environmental regulations and sustainability initiatives also influence product development, encouraging the use of eco-friendly materials and processes. While the region faces competition from Asian manufacturers on cost, it differentiates through technological innovation, adherence to strict quality standards, and strong focus on R&D.

South America

The South American RF inductors market is emerging, with growth primarily driven by increasing mobile phone penetration, consumer electronics adoption, and gradual industrialization. Brazil and Argentina are the largest markets, though economic volatility and currency fluctuations occasionally impact investment and procurement cycles. Demand is largely cost-driven, with a preference for standard multilayer and wire-wound inductors. The automotive sector shows potential for growth as regional manufacturing expands, but overall adoption of high-frequency, high-performance components remains limited compared to more developed regions. Infrastructure challenges and limited local production capabilities mean that most RF inductors are imported, primarily from Asia, which affects supply chain stability and cost structures.

Middle East & Africa

The Middle East & Africa region represents a developing market for RF inductors, with growth opportunities linked to telecommunications expansion, urbanization, and increasing consumer electronics adoption. The Gulf Cooperation Council (GCC) countries, particularly the UAE and Saudi Arabia, are investing in smart city initiatives and 5G infrastructure, driving demand for communication-grade RF components. However, the market remains constrained by limited local manufacturing, reliance on imports, and economic diversification challenges. In Africa, mobile communication growth is a key driver, but infrastructural and economic barriers slow the adoption of advanced components. While the market is growing, it remains a smaller segment globally, with potential long-term growth tied to increased digitalization and industrial development.

Report Scope

This market research report provides a comprehensive analysis of the global RF Inductors market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global RF Inductors market was valued at USD 1,027 million in 2024 and is projected to reach USD 1,305 million by 2032, growing at a CAGR of 3.6%.

- Segmentation Analysis: Detailed breakdown by product type (Wire Wound, Film, Multilayer RF Inductors) and application (Mobile Phone, Consumer Electronics, Automotive, Communication Systems, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Asia-Pacific dominates with over 50% market share, led by China.

- Competitive Landscape: Profiles of 18 key players including Murata, TDK, Taiyo Yuden, Coilcraft, and Vishay. The top six players hold ~60% market share.

- Technology Trends & Innovation: Assessment of high-frequency circuit applications (10MHz to GHz range), non-magnetic core structures, and evolving quality factor (Q) requirements.

- Market Drivers & Restraints: Evaluation of factors including 5G deployment, IoT expansion, and mobile communication growth versus supply chain constraints and material costs.

- Stakeholder Analysis: Strategic insights for component manufacturers, OEMs, and investors in the RF components ecosystem.

The research methodology combines primary interviews with industry experts and analysis of verified market data, ensuring report reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global RF Inductors Market?

-> RF Inductors market was valued at 1027 million in 2024 and is projected to reach US$ 1305 million by 2032, at a CAGR of 3.6% during the forecast period.

Which key companies operate in Global RF Inductors Market?

-> Major players include Murata, TDK, Taiyo Yuden, Coilcraft, Vishay, Samsung Electro-Mechanics, AVX, and Wurth Elektronik, among others.

What are the key growth drivers?

-> Primary drivers include 5G network expansion, increasing smartphone adoption, growth in IoT devices, and automotive electronics demand.

Which region dominates the market?

-> Asia-Pacific leads with over 50% market share, driven by China’s electronics manufacturing sector.

What are the emerging trends?

-> Emerging trends include miniaturization of components, higher frequency requirements for 5G/6G, and advanced materials for improved Q factors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...

Be the first to review “RF Inductors Market Size, Share, Trends, Market Growth and Business Strategies 2025-2032”