MARKET INSIGHTS

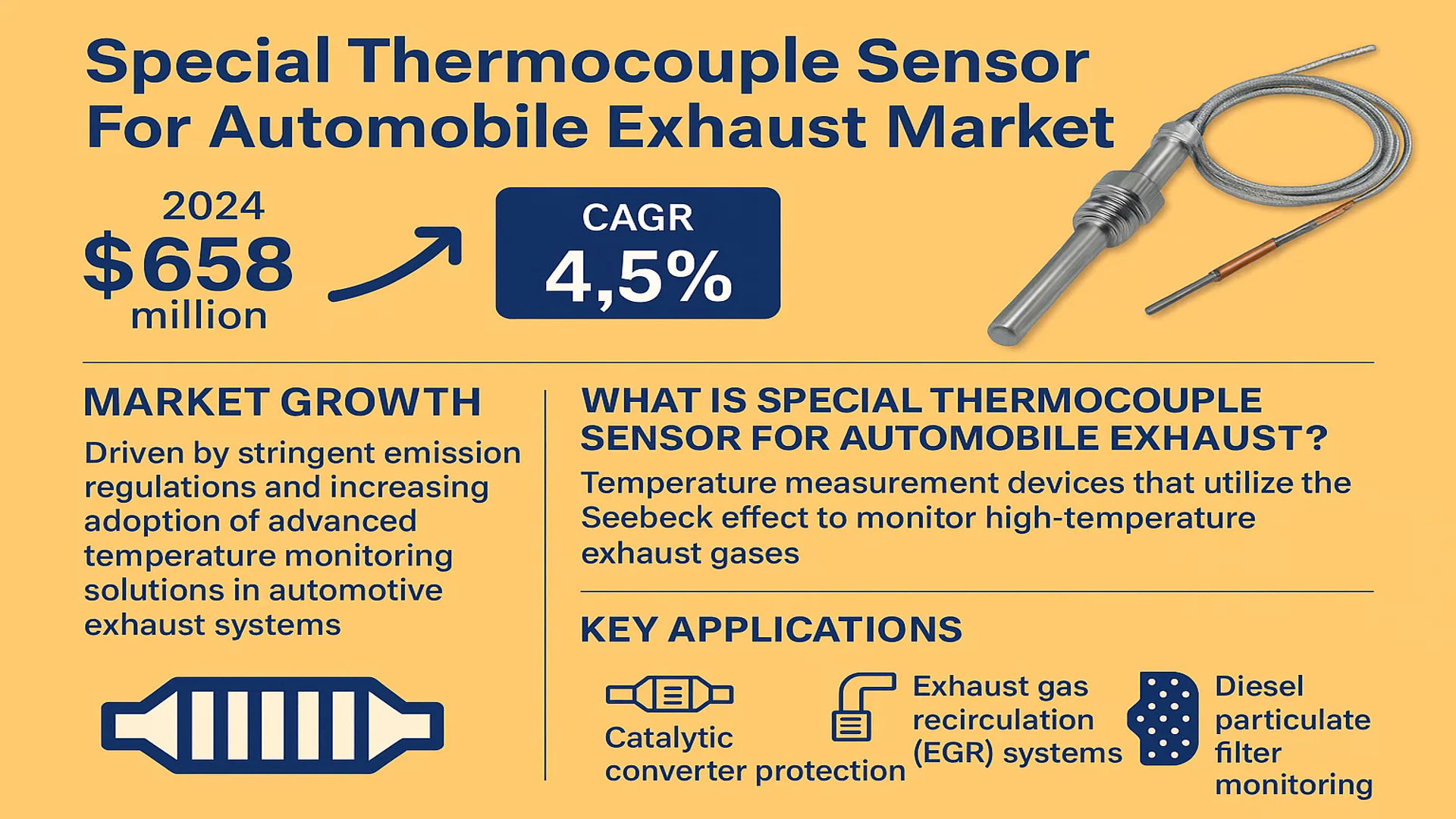

The global Special Thermocouple Sensor For Automobile Exhaust Market was valued at 658 million in 2024 and is projected to reach US$ 894 million by 2032, at a CAGR of 4.5% during the forecast period. The market growth is driven by stringent emission regulations and increasing adoption of advanced temperature monitoring solutions in automotive exhaust systems.

Special thermocouple sensors for automobile exhaust are temperature measurement devices that utilize the Seebeck effect to monitor high-temperature exhaust gases. These sensors consist of two dissimilar metal wires joined at one end to create a voltage proportional to temperature differences. Key applications include catalytic converter protection, exhaust gas recirculation (EGR) systems, and diesel particulate filter monitoring, ensuring compliance with emission standards like Euro 6 and EPA Tier 4.

The market expansion is further supported by the automotive industry’s shift toward electrification and hybrid vehicles, which still require exhaust temperature monitoring in internal combustion components. Among product types, K-Type thermocouples dominate the market due to their wide temperature range (-200°C to 1260°C) and cost-effectiveness. Regionally, Asia Pacific leads market growth, fueled by increasing vehicle production in China and India, where passenger vehicle sales reached 21.4 million units in 2023 according to industry reports.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Emission Regulations Propel Demand for Advanced Exhaust Monitoring Solutions

Global emissions standards continue to tighten, with major automotive markets implementing increasingly strict regulations. Emission control requires precise temperature monitoring in exhaust systems, making thermocouple sensors indispensable for modern vehicles. These sensors play a critical role in maintaining optimal catalytic converter temperatures, where deviations as small as 10-15°C can significantly impact emission reduction efficiency. The European Union’s Euro 7 standards and similar regulations worldwide are accelerating adoption of high-performance temperature sensing technologies. With emissions compliance becoming non-negotiable for automakers, the demand for reliable thermocouple sensors is experiencing sustained growth.

Electrification of Vehicle Fleets Creates New Measurement Challenges

While electric vehicle adoption grows, hybrid vehicles still dominate the transition phase, requiring sophisticated exhaust monitoring for their combustion engines. The hybrid vehicle market, projected to represent 35% of new car sales by 2030, creates unique thermal management requirements that drive sensor innovation. Thermocouples in these applications must handle rapid temperature cycling between electric and combustion modes, pushing manufacturers to develop more durable sensor solutions. Furthermore, range-extended electric vehicles continue to rely on exhaust temperature monitoring to optimize their small combustion engines, creating sustained demand across multiple powertrain architectures.

Advancements in Engine Performance Monitoring Boost Sensor Integration

Modern engine management systems increasingly incorporate exhaust temperature data to optimize performance and fuel efficiency. Thermocouple sensors now feed into complex algorithms that adjust fuel injection timing, turbocharger operation, and aftertreatment system controls. This integration has become particularly crucial for high-performance engines where exhaust temperatures can exceed 900°C. Recent developments in sensor materials and wireless data transmission enable real-time monitoring in these extreme conditions, supporting the automotive industry’s push toward smarter, more connected vehicles.

MARKET RESTRAINTS

High Development Costs for Next-Generation Sensor Solutions

The automotive sector’s relentless pursuit of higher temperature ranges and longer sensor lifespans creates significant R&D challenges. Developing thermocouple alloys that maintain accuracy beyond 1000°C while resisting thermal fatigue requires substantial investment in materials science. Many manufacturers face difficulties scaling up production of these advanced sensors while maintaining consistent quality, with yield rates for premium thermocouples often below industry averages for other automotive components. These cost pressures create barriers for smaller suppliers and may slow the pace of technological advancement in price-sensitive vehicle segments.

Intensifying Competitive Landscape Squeezes Profit Margins

The automotive sensor market has become increasingly crowded, with established players facing competition from regional suppliers and new entrants. This competition drives down unit prices while simultaneously raising expectations for features and reliability. Many manufacturers report shrinking profit margins on standard K-type thermocouples, the workhorses of exhaust monitoring. The situation worsens as vehicle manufacturers extend warranty periods, transferring more long-term reliability risk to component suppliers. These market dynamics force sensor companies to balance cost reduction with continued investment in quality and innovation.

Regulatory Uncertainty in Key Markets

Divergent regulatory timelines across major automotive markets create planning challenges for sensor manufacturers. While Europe pushes forward with aggressive emissions timelines, other regions display inconsistent enforcement of existing standards. This regulatory patchwork complicates product standardization and inventory management, particularly for global suppliers. The lack of harmonization in testing protocols and certification requirements adds development costs and may delay new product introductions in certain markets.

MARKET OPPORTUNITIES

Integration with Vehicle Connectivity Systems Opens New Data Markets

The rise of connected vehicle technologies creates opportunities to transform exhaust temperature data into valuable operational insights. Smart thermocouple systems can now integrate with telematics platforms, allowing fleet operators to monitor engine health in real-time. This capability is particularly valuable for commercial vehicle operators where exhaust system failures can lead to costly downtime. Sensor manufacturers who develop predictive analytics capabilities around their temperature data can establish new revenue streams beyond hardware sales, positioning themselves as partners in vehicle lifecycle management.

Aftermarket Growth Driven by Aging Vehicle Fleets

As average vehicle ages increase across most developed markets, the exhaust system component replacement cycle presents substantial aftermarket potential. Thermocouple sensors typically require replacement every 80,000-120,000 miles, creating a predictable replacement market. The rise of DIY repair culture coupled with online parts distribution makes aftermarket sensors increasingly accessible to consumers. Forward-thinking manufacturers are developing retrofit solutions that simplify sensor replacement procedures, making these components more serviceable outside dealership networks.

Material Science Breakthroughs Enable New Applications

Recent advancements in high-temperature ceramics and novel metal alloys are expanding the operational limits of thermocouple sensors. New materials capable of withstanding extreme thermal cycling without degradation enable sensor placement closer to combustion sources. These technological improvements open opportunities in performance vehicles and heavy-duty applications where conventional sensors previously failed prematurely. Additionally, the development of flexible thermocouple arrays allows for distributed temperature monitoring across larger surface areas, providing more comprehensive exhaust system diagnostics.

SPECIAL THERMOCOUPLE SENSOR FOR AUTOMOBILE EXHAUST MARKET TRENDS

Stricter Emission Regulations Drive Demand for Advanced Temperature Monitoring Solutions

The global automotive industry is undergoing a significant transformation, with emission control becoming a top priority for manufacturers worldwide. This shift is driving strong demand for special thermocouple sensors for automobile exhaust systems, as they play a crucial role in complying with increasingly stringent environmental regulations. The market for these sensors has been growing steadily, with global revenues reaching approximately 658 million in 2024 and projected to expand to 894 million by 2032 at a CAGR of 4.5%. K-Type thermocouples currently dominate the market due to their wide temperature range and durability in harsh exhaust environments.

Other Trends

Integration with Vehicle Electronics and IoT

Modern vehicles are becoming increasingly connected, and exhaust temperature sensors are no exception. There’s a growing trend towards integrating thermocouple sensors with advanced vehicle telemetry systems, enabling real-time monitoring and predictive maintenance capabilities. This integration allows for more precise engine management, optimizing fuel efficiency while minimizing emissions. Manufacturers are developing sensors with improved signal processing capabilities that can interface directly with engine control units (ECUs) and telematics systems.

Material Innovations for Enhanced Durability

The extreme conditions in automobile exhaust systems present significant challenges for sensor durability. In response, manufacturers are developing advanced materials and protective coatings that extend sensor lifespan while maintaining measurement accuracy. New ceramic-based insulation materials and platinum-rhodium alloy elements are showing particular promise in withstanding the high temperatures and corrosive environments found in modern exhaust systems. These advancements are crucial as vehicles continue to push for higher operating temperatures to meet efficiency targets while complying with strict NOx emission limits.

Regional Market Dynamics

While the market shows global growth, regional dynamics vary significantly based on local emission standards and automotive production trends. China’s market is expanding rapidly, driven by both domestic vehicle production growth and tightening emissions regulations similar to Euro 6 standards. In contrast, the U.S. market shows steady demand, particularly for sensors used in heavy-duty commercial vehicles where emissions compliance is strictly enforced. Europe remains at the forefront of demanding sensor technology, with premium automakers investing heavily in exhaust aftertreatment systems that require multiple high-precision temperature measurement points.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive Sensor Leaders Expand Exhaust Thermocouple Solutions Amid Emission Regulation Pressures

The global special thermocouple sensor for automobile exhaust market features a diversified competitive environment with established industrial sensor manufacturers and specialized automotive component suppliers. TE Connectivity and Emerson currently dominate the landscape, holding a combined market share of approximately 28% in 2024. Their leadership stems from decades of expertise in harsh-environment sensing solutions and direct OEM partnerships with major automakers worldwide.

The market structure shows moderate consolidation, where the top five players account for nearly 45% of the $658 million market. However, regional specialists like Germany’s Wika and Japan’s Keyence maintain strong positions in their domestic markets through tailored solutions for local emission standards. This creates a dynamic where global players must adapt their technologies to regional specifications while fending off competition from agile local providers.

Recent strategic movements indicate intensified competition, with multiple players expanding production capacity in Asia to serve growing electric vehicle markets. While thermocouples remain essential for conventional exhaust systems, industry leaders are also developing hybrid sensors compatible with emerging EV thermal management needs. This dual focus allows companies to maintain current revenue streams while future-proofing their portfolios.

Notably, mergers and acquisitions have reshaped the competitive framework, as seen when Danfoss Group acquired a controlling stake in TC GmbH last year to enhance its automotive sensor division. Such consolidation activities suggest the market is entering a phase where technological specialization and manufacturing scale will increasingly determine competitive advantage.

List of Key Special Thermocouple Sensor Manufacturers Profiled

- TE Connectivity (Switzerland)

- Emerson Electric Co. (U.S.)

- Omega Engineering (U.S.)

- Durex Industries (U.S.)

- Maxim Integrated (U.S.)

- Keyence Corporation (Japan)

- NXP Semiconductors (Netherlands)

- Danfoss Group (Denmark)

- Wika Alexander Wiegand SE & Co. KG (Germany)

- Chromalox (U.S.)

Segment Analysis:

By Type

K-Type Thermocouple Segment Dominates the Market Due to Wide Temperature Range and Robust Performance

The market is segmented based on type into:

- K-Type Thermocouple

- Most widely used due to broad temperature range (-200°C to +1250°C)

- High durability in exhaust environments

- S-Type Thermocouple

- Used for high-precision measurements

- Excellent stability in oxidizing atmospheres

- E-Type Thermocouple

- Higher sensitivity compared to other types

- Suitable for low-temperature applications

- N-Type Thermocouple

- Improved oxidation resistance

- Long-term stability in exhaust systems

- J-Type Thermocouple

- Cost-effective solution

- Suitable for vacuum environments

By Application

Passenger Vehicles Segment Leads Due to High Production Volumes and Stringent Emission Norms

The market is segmented based on application into:

- Passenger Vehicles

- Compact sensors for space-constrained installations

- Compliance with Euro 6 and similar emission standards

- Commercial Vehicles

- Heavy-duty sensors for larger exhaust systems

- Extended durability requirements

By Installation Type

Direct Mount Sensors Preferred for Accurate Temperature Measurement Close to Emission Sources

The market is segmented based on installation type into:

- Direct Mount

- Installed directly in exhaust stream

- Provides fastest response to temperature changes

- Remote Mount

- Connected via extension wires

- Used where space constraints prevent direct mounting

Regional Analysis: Special Thermocouple Sensor For Automobile Exhaust Market

Asia-Pacific

The Asia-Pacific region is the dominant market for automobile exhaust thermocouple sensors, driven by rapid automotive production growth in China, India, and Southeast Asia. China alone accounts for over 35% of global vehicle production, creating substantial demand for exhaust temperature monitoring systems. While price sensitivity favors K-type thermocouples, tightening emission regulations (China VI, Bharat Stage VI) are pushing automakers toward more precise sensor technologies. Local manufacturers like Holykell and Jalc Trading compete aggressively on cost, while global players establish joint ventures to access this high-volume market. Challenges include inconsistent regulatory enforcement across developing nations and supply chain fragmentation.

North America

Stringent EPA and California Air Resources Board (CARB) regulations mandate advanced exhaust monitoring, making North America a technology leader. The region sees strong adoption of S-type and N-type thermocouples in premium vehicles for their superior accuracy in catalytic converter temperature monitoring. Major Tier 1 suppliers like TE Connectivity and Emerson are investing in miniaturized sensors to meet evolving OEM requirements. However, fluctuating vehicle production volumes and the shift toward electric vehicles present long-term challenges for the exhaust sensor market. The U.S. remains the innovation hub with several patents filed for high-temperature resistant sensor materials.

Europe

Europe’s stringent Euro 7 norms and focus on real-driving emissions (RDE) testing are accelerating demand for high-precision exhaust thermocouples. Germany’s automotive engineering leadership drives innovation in sensor durability, with companies like Wika and Danfoss developing solutions for 1000°C+ operating temperatures. The region shows the highest adoption rate of ceramic-sheathed thermocouples, valued for chemical resistance in diesel aftertreatment systems. However, market growth faces headwinds from declining diesel vehicle production and extended vehicle replacement cycles. Collaboration between sensor manufacturers and emission control system providers is intensifying to develop integrated solutions.

South America

Market growth in South America is constrained by economic volatility but benefits from Brazil’s robust commercial vehicle sector. Mercosur emission standards drive basic thermocouple adoption, primarily J-type and K-type variants sourced from regional manufacturers. Argentina shows potential with new vehicle emission testing requirements, though currency fluctuations limit foreign investment. The lack of local semiconductor fabrication restricts advanced sensor production, creating import dependence. Opportunities exist in retrofit solutions for aging vehicle fleets, particularly in mining and agriculture sectors where exhaust system failures are common.

Middle East & Africa

This emerging market shows divergent trends: Gulf Cooperation Council (GCC) countries favor premium sensor-equipped vehicles to meet Euro-equivalent standards, while African markets rely on basic aftermarket solutions. The United Arab Emirates and Saudi Arabia are establishing automotive testing hubs, creating localized demand. Challenges include extreme climate conditions requiring specialized sensor materials and limited technical expertise in calibration. Turkish manufacturers like Sor Controls are expanding regionally with cost-competitive alternatives, though market penetration remains low outside major urban centers. Infrastructure development projects may spur commercial vehicle sensor demand in the long term.

Report Scope

This market research report provides a comprehensive analysis of the Global Special Thermocouple Sensor for Automobile Exhaust market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 658 million in 2024 and is projected to reach USD 894 million by 2032 at a CAGR of 4.5%.

- Segmentation Analysis: Detailed breakdown by product type (K-Type, S-Type, E-Type, N-Type, J-Type Thermocouples) and application (Passenger Vehicles, Commercial Vehicles) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis for major economies.

- Competitive Landscape: Profiles of leading market participants including Omega, TE Connectivity, Emerson, NXP Semiconductors and Danfoss Group, covering their product portfolios and strategic developments.

- Technology Trends & Innovation: Assessment of emerging sensor technologies, materials innovation, and integration with vehicle emission control systems.

- Market Drivers & Restraints: Evaluation of factors including stringent emission regulations, automotive production trends, and supply chain challenges.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, automotive OEMs, suppliers, and investors in the automotive components ecosystem.

The research employs primary and secondary methodologies, including interviews with industry experts and analysis of verified market data to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Special Thermocouple Sensor for Automobile Exhaust Market?

-> Special Thermocouple Sensor For Automobile Exhaust Market was valued at 658 million in 2024 and is projected to reach US$ 894 million by 2032, at a CAGR of 4.5% during the forecast period.

Which key companies operate in this market?

-> Leading players include Omega, TE Connectivity, Emerson, NXP Semiconductors, Danfoss Group, Wika, and Amphenol.

What are the key growth drivers?

-> Growth is driven by stringent emission regulations, increasing vehicle production, and demand for fuel-efficient vehicles.

Which region dominates the market?

-> Asia-Pacific leads in market share due to high automotive production, while North America shows strong growth in advanced emission control systems.

What are the emerging trends?

-> Trends include miniaturization of sensors, integration with IoT for predictive maintenance, and development of high-temperature resistant materials.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...