Space Semiconductor Component Market Insights

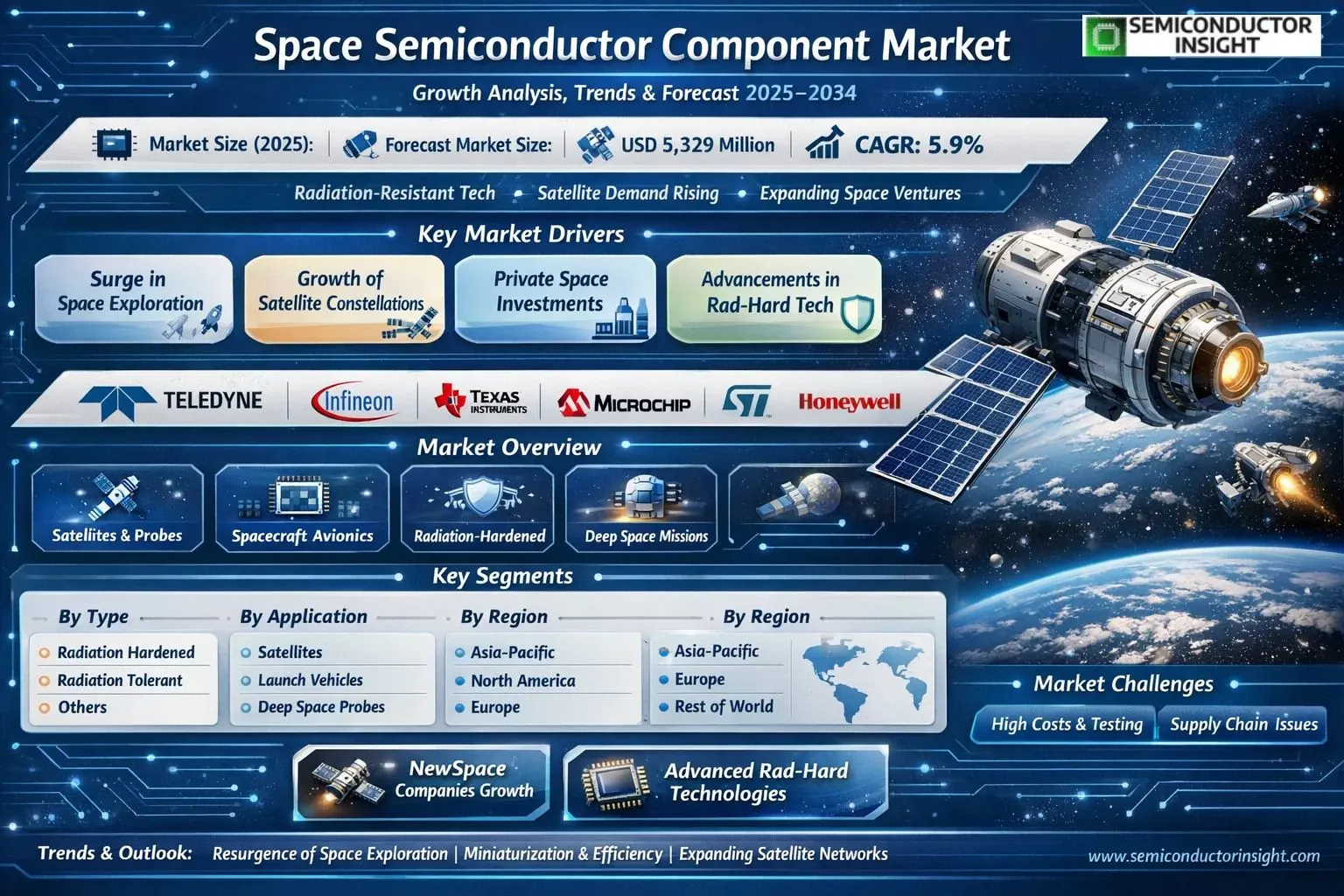

Global Space Semiconductor Component market size was valued at USD 3,606 million in 2025. The market is projected to reach USD 5,329 million by 2034, exhibiting a CAGR of 5.9% during the forecast period.

Space Semiconductor Component is the sector within the semiconductor industry that offers the manufacturing, development, and distribution of electronic components and integrated circuits specially intended for use in space applications. It is used in various space-related systems and equipment, such as scientific instruments, communication satellites, space probes, and spacecraft avionics. These semiconductors are able to resist the risky conditions of outer space, including high degree of radiation, extreme temperatures, and vacuum environments.

The market is experiencing rapid growth due to several factors, including the resurgence of space exploration, a surge in satellite constellations, and substantial investments from private space ventures like SpaceX and Blue Origin. Furthermore, advancements in radiation-hardened and tolerant technologies enable more reliable missions. Initiatives by key players continue to drive innovation. For instance, in early 2024, Microchip Technology Inc. enhanced its radiation-hardened FPGA portfolio to support next-generation deep space probes. Teledyne Technologies Incorporated, Infineon Technologies AG, Texas Instruments Incorporated, Microchip Technology Inc., and STMicroelectronics are some of the key players operating in the market with diverse portfolios.

MARKET DRIVERS

Rising Demand from Satellite Constellations

Space Semiconductor Component Market is propelled by the rapid expansion of low Earth orbit (LEO) satellite constellations, which require robust, radiation-hardened components for reliable operation. Major players like SpaceX’s Starlink initiative have launched thousands of satellites, driving demand for advanced processors, memory devices, and power management ICs tailored for harsh space environments. This surge is expected to contribute significantly to market growth, with annual satellite deployments exceeding 2,000 units in recent years.

Government and Private Space Missions

Government-led programs such as NASA’s Artemis and ESA’s exploration efforts, alongside private ventures like Blue Origin and Rocket Lab, are accelerating the need for high-performance semiconductors in spacecraft avionics and communication systems. These missions demand components withstanding extreme temperatures and cosmic radiation, fostering innovation in silicon carbide and gallium nitride technologies within Space Semiconductor Component Market.

➤ The market is projected to grow at a CAGR of 9.2% through 2030, fueled by over $50 billion in cumulative space investments.

Additionally, the push for reusable launch vehicles reduces overall mission costs, indirectly boosting procurement of durable semiconductor solutions and enhancing market accessibility for emerging players.

MARKET CHALLENGES

Technical and Environmental Hurdles

In Space Semiconductor Component Market, developing components resilient to total ionizing dose (TID) effects and single event upsets poses significant engineering challenges. Devices must operate flawlessly under prolonged radiation exposure, often requiring custom fabrication processes that extend development timelines.

Other Challenges

Supply Chain Vulnerabilities

Geopolitical tensions and reliance on limited foundries for rad-hard processes disrupt availability, with lead times stretching up to 18 months for critical parts like FPGAs and ASICs.

Moreover, miniaturization efforts to support CubeSats conflict with thermal management needs, complicating power efficiency in compact designs and increasing failure risks during long-duration missions.

MARKET RESTRAINTS

High Costs and Qualification Barriers

Space Semiconductor Component Market faces restraints from exorbitant R&D and qualification expenses, where full space certification can cost upwards of $10 million per component family. Stringent standards from agencies like NASA demand extensive testing, deterring smaller entrants.

Long lead times for radiation testing and process hardening further limit scalability, as manufacturers grapple with low-volume production economics despite rising demand.

Regulatory compliance across international space treaties adds layers of scrutiny, slowing innovation deployment and maintaining high entry barriers in this specialized sector.

MARKET OPPORTUNITIES

NewSpace Ecosystem Expansion

Space Semiconductor Component Market presents opportunities through the proliferation of commercial NewSpace companies, enabling cost-effective rideshare missions and fostering demand for COTS-modified rad-hard components.

Advancements in wide-bandgap semiconductors like SiC and GaN open avenues for higher efficiency power systems in electric propulsion, supporting deep-space probes and lunar gateways.

Integration of AI accelerators for onboard data processing in constellations unlocks real-time analytics, with the market poised for growth as 5G-enabled satellite networks expand global coverage.

Space Semiconductor Component Market Trends

Resurgence of Space Exploration Driving Demand

Space Semiconductor Component Market is experiencing robust growth fueled by the resurgence of space exploration initiatives worldwide. Space agencies and private enterprises are launching ambitious missions, including lunar expeditions, Mars voyages, and deep space probes, which necessitate highly reliable semiconductor components. These components must endure extreme radiation, temperature fluctuations, and vacuum conditions inherent to space environments. Essential for data processing, communication, navigation, and scientific instrumentation in satellites, launch vehicles, rovers, and landers, radiation-hardened and tolerant semiconductors ensure mission success. This trend underscores the critical role of advanced electronics in enabling complex space operations and fostering innovation within the sector.

Other Trends

Miniaturization and Power Efficiency Gains

In Space Semiconductor Component Market, ongoing advancements in miniaturization are transforming spacecraft design. Smaller, lighter components reduce payload mass, lowering launch costs and enhancing mission efficiency. Improved power efficiency allows for longer operational durations in resource-constrained environments, supporting applications across satellites, deep space probes, and planetary rovers. Industry leaders are prioritizing these developments to meet the demands of next-generation missions, integrating high-performance integrated circuits that balance size, weight, and functionality.

Expansion in Commercial and Diversified Applications

Space Semiconductor Component Market is witnessing a shift toward broader commercialization, with private companies driving demand alongside traditional space agencies. Key segments like radiation-hardened grade components dominate for high-risk missions such as deep space probes and launch vehicles, while radiation-tolerant variants gain traction in cost-sensitive satellite constellations. Regional dynamics, particularly in North America, Europe, and Asia, reflect increased investments in space infrastructure. Leading firms including Teledyne Technologies, Infineon Technologies, and Microchip Technology are innovating to address challenges in radiation resistance and thermal management, ensuring reliability across diverse applications from communication satellites to scientific landers. This multifaceted growth positions the market for sustained evolution amid global space ambitions.

COMPETITIVE LANDSCAPEKey Industry Players

Dominating Entities in Space Semiconductor Component Market

Space Semiconductor Component Market is characterized by a concentrated structure dominated by a few established leaders with specialized expertise in radiation-hardened and tolerant technologies. Teledyne Technologies Incorporated stands out as a primary frontrunner, leveraging its advanced capabilities in high-reliability components for satellites and deep space probes. Infineon Technologies AG and Texas Instruments Incorporated also command significant shares, providing critical integrated circuits resilient to extreme radiation and temperature fluctuations. This oligopolistic landscape reflects high entry barriers, including stringent qualification processes and substantial R&D investments required for space-grade semiconductors, enabling these giants to capture over 50% of the global revenue in 2025.

Beyond the top tier, several niche players contribute meaningfully by focusing on specific segments like radiation-tolerant grades for launch vehicles and rovers. Microchip Technology Inc excels in mixed-signal solutions, while STMicroelectronics International N.V. and BAE Systems Plc offer bespoke avionics semiconductors. Companies such as Cobham Advanced Electronic Solutions Inc, now part of larger entities, and Solid State Devices Inc provide specialized power management devices. Honeywell International Inc and Xilinx Inc (now AMD) enhance the ecosystem with FPGA and sensor technologies, respectively. Emerging dynamics include mergers like Maxim Integrated’s acquisition by Analog Devices, intensifying competition amid rising demand from commercial space ventures.

List of Key Space Semiconductor Component Companies Profiled

- Teledyne Technologies Incorporated

- Infineon Technologies AG

- Texas Instruments Incorporated

- Microchip Technology Inc

- Cobham Advanced Electronic Solutions Inc

- STMicroelectronics International N.V.

- Solid State Devices Inc

- Honeywell International Inc

- Xilinx Inc

- BAE Systems Plc

- TE Connectivity

- Maxim Integrated Products

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Radiation Hardened Grade leads due to its unmatched resilience in extreme space conditions.

|

| By Application |

|

Satellite dominates as the primary platform leveraging space semiconductors for diverse functionalities.

|

| By End User |

|

Commercial Space Companies are at the forefront, propelled by entrepreneurial ventures.

|

| By Orbit Type |

|

Low Earth Orbit (LEO) commands prominence with dynamic deployment trends.

|

| By Component Function |

|

Processors and Microcontrollers serve as the backbone for intelligent space systems.

|

Regional Analysis: Space Semiconductor Component Market

North America

North America excels in pioneering radiation-tolerant semiconductors, with innovations in wide-bandgap materials improving performance for satellite constellations. Focus on miniaturization supports smallsat deployments, enhancing data processing capabilities. Collaborative R&D ecosystems drive quantum-resistant encryption chips, vital for secure space communications in Space Semiconductor Component Market.

Leading firms like Analog Devices and Microchip Technology dominate, supplying specialized components for launch systems and rovers. Partnerships with SpaceX bolster production scalability. Their expertise in failure-proof designs positions North America as a hub for high-volume space semiconductor manufacturing.

Favorable policies from the FAA and ITAR framework expedite certifications for space-grade chips. Export controls safeguard intellectual property, while incentives for domestic production stimulate investments, reinforcing North America’s competitive edge in Space Semiconductor Component Market.

Venture capital flows into fabless semiconductor startups targeting space applications. Public-private partnerships fund advanced packaging technologies, enabling compact, efficient components. This influx supports sustained growth amid rising demand for mega-constellations.

Europe

Europe maintains a strong presence in Space Semiconductor Component Market through the European Space Agency’s initiatives and contributions from companies like Airbus Defence and Space. Emphasis on sustainable space technologies drives development of low-power semiconductors for Earth observation satellites and navigation systems like Galileo. Regional dynamics feature collaborative frameworks such as the Horizon Europe program, funding resilient chips for long-duration missions. Strengths in photonic integrated circuits enhance optical communications, while stringent quality standards ensure reliability. Challenges include dependency on U.S. technology transfers, prompting efforts to build indigenous supply chains. Growing focus on NewSpace ventures in the UK and France accelerates adoption of commercial-off-the-shelf adaptations for space use, fostering market expansion.

Asia-Pacific

Asia-Pacific emerges as a dynamic contender in Space Semiconductor Component Market, propelled by ambitious programs in China, India, and Japan. China’s lunar exploration and satellite mega-constellations demand high-density memory and processors, spurring local production of rad-hard components. India’s ISRO leverages cost-effective fabrication for small satellite swarms, emphasizing affordability. Japan excels in precision sensors for JAXA missions. Regional growth reflects government-backed semiconductor clusters, reducing import reliance. Supply chain diversification and talent pools in Taiwan and South Korea support advanced node technologies, positioning Asia-Pacific for rapid catch-up in deep-space applications.

South America

South America represents an nascent yet promising segment of Space Semiconductor Component Market, with Brazil and Argentina leading through space agencies like AEB. Focus on regional satellite networks for disaster monitoring drives demand for ruggedized communication chips. Collaborations with international partners provide technology access, enabling localization of assembly lines. Challenges include limited infrastructure, but growing private investments in launch capabilities foster gradual adoption of space-grade semiconductors. Emphasis on dual-use technologies for agriculture and telecom strengthens market potential.

Middle East & Africa

The Middle East & Africa region shows accelerating interest in Space Semiconductor Component Market, highlighted by UAE’s Mars mission and Saudi Arabia’s satellite ambitions. Investments in sovereign space programs necessitate secure, high-performance chips for remote sensing and connectivity. Africa’s growing Earth observation needs spur adoption of cost-optimized components. Dynamics involve partnerships with established players for knowledge transfer, building regional fabs. Focus on resilient designs for equatorial launches positions the area for expanded participation in global space semiconductor ecosystems.

Report Scope

This market research report provides a comprehensive analysis of Space Semiconductor Component Market, covering the forecast period 2025–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as satellites, space probes, spacecraft avionics, and scientific instruments.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Space Semiconductor Component Market?

-> Space Semiconductor Component Market was valued at USD 3606 million in 2025 and is expected to reach USD 5329 million by 2034, at a CAGR of 5.9% during the forecast period.

Which key companies operate in Space Semiconductor Component Market?

-> Key players include Teledyne Technologies Incorporated, Infineon Technologies AG, Texas Instruments Incorporated, Microchip Technology Inc, STMicroelectronics International N.V., and Honeywell International Inc, among others.

What are the key growth drivers?

-> Key growth drivers include resurgence of space exploration, demand for radiation-resistant components in satellites and probes, and miniaturization for launch cost reduction.

Which region dominates the market?

-> North America is the dominant region, while Asia remains the fastest-growing market.

What are the emerging trends?

-> Emerging trends include radiation hardened and tolerant grades, power-efficient designs, and advancements in spacecraft avionics.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...