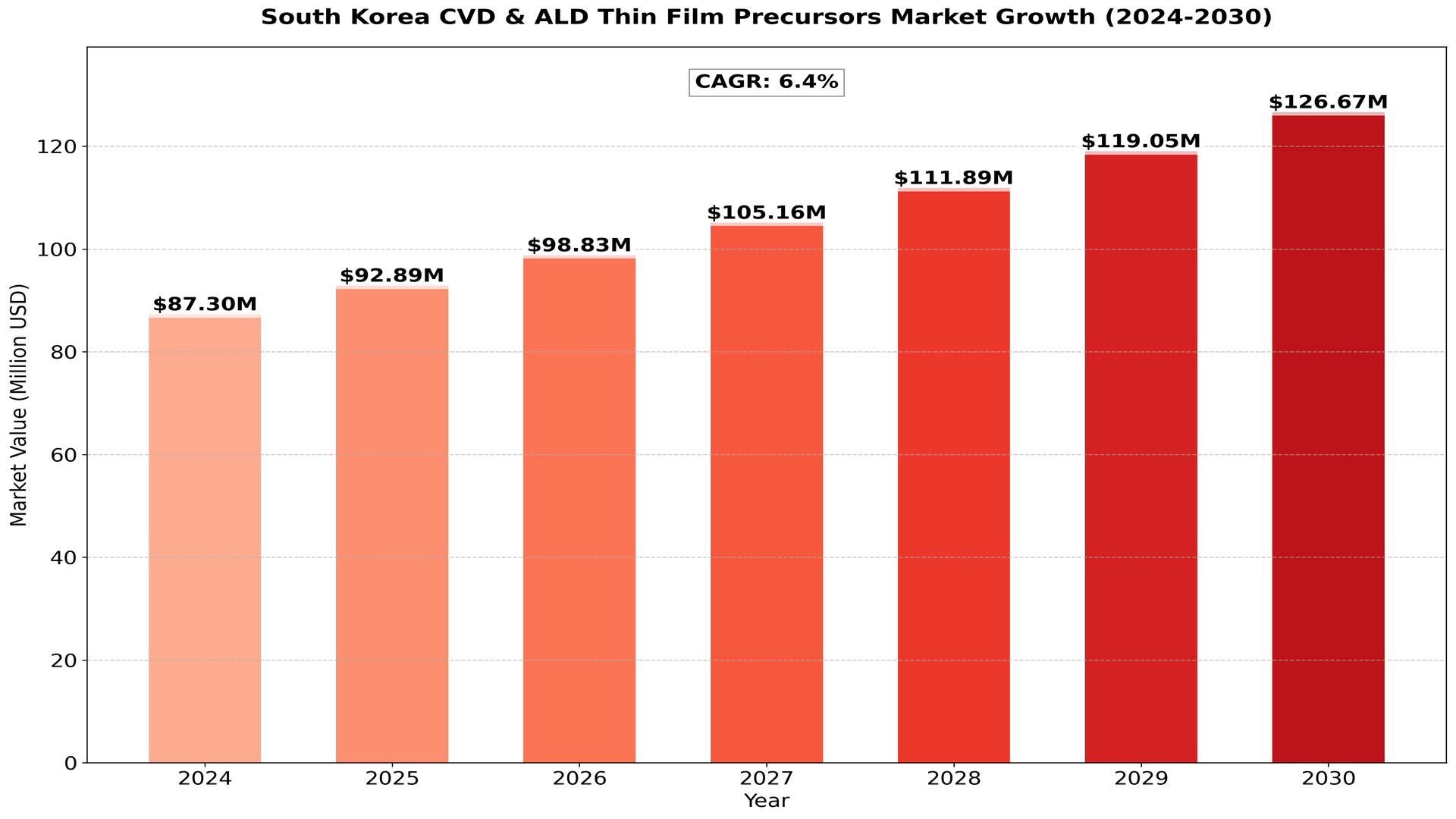

South Korea CVD & ALD Thin Film Precursors market size was valued at US$ 87.3 million in 2024 and is projected to reach US$ 126.8 million by 2030, at a CAGR of 6.4% during the forecast period 2024-2030.

Chemical compounds used in Chemical Vapor Deposition (CVD) and Atomic Layer Deposition (ALD) processes to create thin films for semiconductor and other advanced manufacturing applications.

The South Korean Audio Amplifier market is growing steadily, driven by the country’s strong consumer electronics sector and automotive industry. South Korea’s electronics industry, valued at $215 billion in 2023, provides a robust foundation for audio amplifier demand. Key trends include the development of high-efficiency Class-D amplifiers, integration of smart features and wireless connectivity, and increased adoption of amplifiers in smart home devices. The market faces challenges from the commoditization of basic amplifier technology and pressure to reduce power consumption in battery-operated devices. Opportunities lie in creating specialized amplifiers for emerging applications like true wireless stereo (TWS) earbuds and developing audio solutions for electric vehicles. With South Korea being home to major consumer electronics brands like Samsung and LG, there’s significant domestic production and innovation in audio technologies. The market benefits from South Korea’s vibrant music and entertainment industry, driving demand for high-quality audio equipment in professional and consumer applications. The country’s automotive sector, producing 3.5 million vehicles in 2023, also contributes to demand for automotive audio amplifiers.

This report contains market size and forecasts of CVD & ALD Thin Film Precursors in South Korea, including the following market information:

• South Korea CVD & ALD Thin Film Precursors Market Revenue, 2019-2024, 2024-2030, ($ millions)

• South Korea CVD & ALD Thin Film Precursors Market Sales, 2019-2024, 2024-2030,

• South Korea Top five CVD & ALD Thin Film Precursors companies in 2023 (%)

Report Includes

This report presents an overview of South Korea market for CVD & ALD Thin Film Precursors , sales, revenue and price. Analyses of the South Korea market trends, with historic market revenue/sales data for 2019 – 2023, estimates for 2024, and projections of CAGR through 2030.

This report focuses on the CVD & ALD Thin Film Precursors sales, revenue, market share and industry ranking of main manufacturers, data from 2019 to 2024. Identification of the major stakeholders in the South Korea CVD & ALD Thin Film Precursors market, and analysis of their competitive landscape and market positioning based on recent developments and segmental revenues.

This report will help stakeholders to understand the competitive landscape and gain more insights and position their businesses and market strategies in a better way.

This report analyzes the segments data by Type, and by Sales Channels, sales, revenue, and price, from 2019 to 2030. Evaluation and forecast the market size for Humidifier sales, projected growth trends, production technology, sales channels and end-user industry.

Segment by Type

• Silicon Precursors

• Metal Precursors

• High-k Precursors

• Low-k Precursors

Segment by Applications

• Integrated Circuits

• Flat Panel Display

• PV Industry

• Others

Key Companies covered in this report:

• Soulbrain

• Doosan Corporation

• Samsung SDI

• LG Chem

• Hyundai Motor Group

• SK Materials

• Hanwha Solutions

• Foosung Co., Ltd.

• Iljin Materials Co., Ltd.

• Wonik QnC Corporation

Including or excluding key companies relevant to your analysis.

Competitor Analysis

The report also provides analysis of leading market participants including:

• Key companies CVD & ALD Thin Film Precursors revenues in South Korean market, 2019-2024 (Estimated), ($ millions)

• Key companies CVD & ALD Thin Film Precursors revenues share in South Korean market, 2023 (%)

• Key companies CVD & ALD Thin Film Precursors sales in South Korean market, 2019-2024 (Estimated),

• Key companies CVD & ALD Thin Film Precursors sales share in South Korean market, 2023 (%)

Drivers:

- Thriving Semiconductor Industry:

South Korea is a global leader in semiconductor manufacturing, home to giants like Samsung Electronics and SK Hynix. The growth of these industries fuels the demand for advanced thin film deposition technologies, including CVD and ALD, as they are crucial for fabricating high-performance microchips and integrated circuits. - Advanced Electronics and Display Technologies:

South Korea’s dominance in electronics, especially in OLED and micro-LED displays, drives the need for precise and efficient thin film deposition techniques. CVD and ALD thin film precursors are essential in producing the ultra-thin, uniform coatings required for advanced displays. - Growing Investment in 5G and AI Technologies:

The rapid development of 5G networks and artificial intelligence (AI) technologies in South Korea requires cutting-edge semiconductor technologies, which rely on CVD and ALD thin film processes for miniaturization and performance enhancements. - Government Support and R&D:

The South Korean government offers strong support to the semiconductor industry, including funding for research and development (R&D). This has led to innovations in deposition processes and materials, fostering the growth of the thin film precursors market.

Restraints:

- High Production Costs:

The cost of raw materials and the complexity of manufacturing high-quality thin film precursors pose challenges. Developing cost-effective production methods remains a key restraint, especially for smaller manufacturers trying to compete with established players. - Stringent Environmental Regulations:

South Korea has stringent environmental laws regarding the use of hazardous chemicals, which can impact the production of certain thin film precursors. Compliance with these regulations increases the cost and complexity of manufacturing, potentially slowing down market growth. - Supply Chain Vulnerabilities:

The semiconductor industry has faced global supply chain disruptions, particularly during the COVID-19 pandemic. These disruptions have highlighted the fragility of the supply chain for raw materials and high-purity chemicals required for CVD and ALD processes.

Opportunities:

- Expansion of Green Technologies:

With the rise of renewable energy and electric vehicles (EVs), there’s growing demand for advanced battery technologies, solar panels, and other green technologies. Thin film deposition processes play a crucial role in these industries, creating new opportunities for CVD and ALD thin film precursor manufacturers. - Rising Demand for Smaller, More Efficient Devices:

As consumer electronics continue to evolve toward smaller, more powerful devices, there is increasing demand for miniaturized components with enhanced performance. ALD and CVD processes enable the production of thin films at the atomic level, creating significant opportunities for market growth. - Collaborations and Joint Ventures:

Strategic collaborations between South Korean companies and global firms specializing in thin film deposition technologies can drive innovation. Joint ventures allow companies to share expertise and resources, accelerating the development of new materials and processes.

Challenges:

- Technological Complexity:

Developing next-generation CVD and ALD thin film precursors requires significant technical expertise and investment in R&D. As the demand for more complex materials increases, so does the need for continuous innovation, which can be a barrier for companies with limited resources. - Global Competition:

While South Korea is a leading market for semiconductors and electronics, the global nature of the thin film precursors market means that local companies face stiff competition from international players, particularly from the U.S., China, and Japan. - Rapid Pace of Technological Change:

The fast pace of technological advancement in semiconductors and electronics requires companies in the thin film precursors market to stay ahead of the curve. Keeping up with these rapid changes can be challenging, especially for smaller or less-established firms.

Key Indicators Analysed

• Market Players & Competitor Analysis: The report covers the key players of the industry including Company Profile, Product Specifications, Production Capacity/Sales, Revenue, Price and Gross Margin 2019-2030 & Sales with a thorough analysis of the market’s competitive landscape and detailed information on vendors and comprehensive details of factors that will challenge the growth of major market vendors.

• South Korean Market Analysis: The report includes South Korean market status and outlook 2019-2030. Further the report provides break down details about each region & countries covered in the report. Identifying its sales, sales volume & revenue forecast. With detailed analysis by types and applications.

• Market Trends: Market key trends which include Increased Competition and Continuous Innovations.

• Opportunities and Drivers: Identifying the Growing Demands and New Technology

• Porters Five Force Analysis: The report provides with the state of competition in industry depending on five basic forces: threat of new entrants, bargaining power of suppliers, bargaining power of buyers, threat of substitute products or services, and existing industry rivalry.

Key Benefits of This Market Research:

• Industry drivers, restraints, and opportunities covered in the study

• Neutral perspective on the market performance

• Recent industry trends and developments

• Competitive landscape & strategies of key players

• Potential & niche segments and regions exhibiting promising growth covered

• Historical, current, and projected market size, in terms of value

• In-depth analysis of the CVD & ALD Thin Film Precursors Market

• Overview of the regional outlook of the CVD & ALD Thin Film Precursors Market

Key Reasons to Buy this Report:

• Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

• This enables you to anticipate market changes to remain ahead of your competitors

• You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations or other strategic documents

• The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

• Provision of market value (USD Billion) data for each segment and sub-segment

• Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

• Analysis by geography highlighting the consumption of the product/service in the region as well as indicating the factors that are affecting the market within each region

• Competitive landscape which incorporates the market ranking of the major players, along with new service/product launches, partnerships, business expansions, and acquisitions in the past five years of companies profiled

• Extensive company profiles comprising of company overview, company insights, product benchmarking, and SWOT analysis for the major market players

• The current as well as the future market outlook of the industry concerning recent developments which involve growth opportunities and drivers as well as challenges and restraints of both emerging as well as developed regions

• Includes in-depth analysis of the market from various perspectives through Porter’s five forces analysis

• Provides insight into the market through Value Chain

• Market dynamics scenario, along with growth opportunities of the market in the years to come

• 6-month post-sales analyst support

We offer additional regional and global reports that are similar:

• Global CVD & ALD Thin Film Precursors Market

• United States CVD & ALD Thin Film Precursors Market

• Japan CVD & ALD Thin Film Precursors Market

• Germany CVD & ALD Thin Film Precursors Market

• South Korea CVD & ALD Thin Film Precursors Market

• Indonesia CVD & ALD Thin Film Precursors Market

• Brazil CVD & ALD Thin Film Precursors Market

Customization of the Report: In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are meet.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...