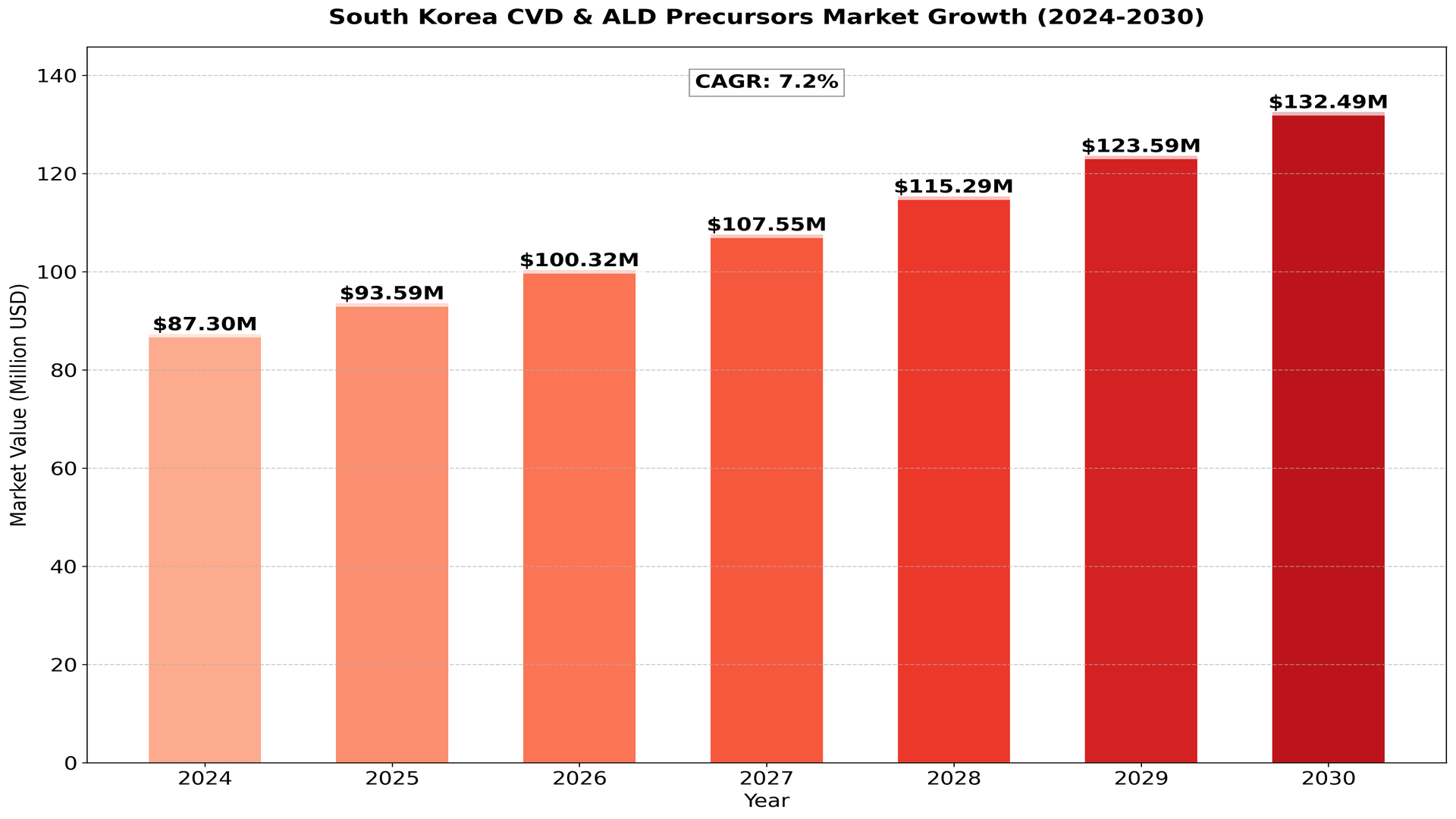

South Korea CVD & ALD Precursors Market size was valued at US$ 87.3 million in 2024 and is projected to reach US$ 132.49 million by 2030, at a CAGR of 7.2% during the forecast period 2024-2030.

Chemical compounds used in Chemical Vapor Deposition (CVD) and Atomic Layer Deposition (ALD) processes for depositing thin films in semiconductor manufacturing and other high-tech applications.

The South Korean CVD & ALD Precursors market is growing rapidly, supported by the country’s dominant position in the global semiconductor industry. South Korea’s semiconductor exports reached $128 billion in 2023, indicating the scale of chip manufacturing activities driving precursor demand. Key trends include the development of high-purity precursors for advanced node processes, increased adoption of ALD for memory chip production, and research into novel precursors for emerging materials like 2D semiconductors. The market faces challenges from stringent purity requirements and the need for constant innovation to keep pace with semiconductor scaling. Opportunities exist in creating precursors for new memory technologies like MRAM and developing eco-friendly precursor alternatives. With Samsung and SK Hynix, two of the world’s largest memory manufacturers, based in South Korea, there’s significant domestic demand for advanced CVD and ALD precursors. The market benefits from South Korea’s “K-Semiconductor Strategy,” which aims to invest $451 billion in the semiconductor industry by 2030, including substantial funding for materials and equipment development.

This report contains market size and forecasts of CVD & ALD Precursors in South Korea, including the following market information:

• South Korea CVD & ALD Precursors Market Revenue, 2019-2024, 2024-2030, ($ millions)

• South Korea CVD & ALD Precursors Market Sales, 2019-2024, 2024-2030,

• South Korea Top five CVD & ALD Precursors companies in 2023 (%)

Report Includes

This report presents an overview of South Korea market for CVD & ALD Precursors , sales, revenue and price. Analyses of the South Korea market trends, with historic market revenue/sales data for 2019 – 2023, estimates for 2024, and projections of CAGR through 2030.

This report focuses on the CVD & ALD Precursors sales, revenue, market share and industry ranking of main manufacturers, data from 2019 to 2024. Identification of the major stakeholders in the South Korea CVD & ALD Precursors market, and analysis of their competitive landscape and market positioning based on recent developments and segmental revenues.

This report will help stakeholders to understand the competitive landscape and gain more insights and position their businesses and market strategies in a better way.

This report analyzes the segments data by Type, and by Sales Channels, sales, revenue, and price, from 2019 to 2030. Evaluation and forecast the market size for Humidifier sales, projected growth trends, production technology, sales channels and end-user industry.

Segment by Type

• Silicon Precursors

• Metal Precursors

• High-k Precursors

• Low-k Precursors

Segment by Applications

• Integrated Circuits

• Flat Panel Display

• PV Industry

• Others

Key Companies covered in this report:

• Soulbrain

• Wonik QnC Corporation

• Hansol Chemical

• KC Tech Co.

• Doosan Corporation Electro-Materials

• TAIYO NIPPON SANSO Corporation

• SK Materials Co., Ltd.

• Hanwha Solutions/Chemical Corporation

• Jusung Engineering Co., Ltd.

• Samsung SDI Co., Ltd.

Including or excluding key companies relevant to your analysis.

Competitor Analysis

The report also provides analysis of leading market participants including:

• Key companies CVD & ALD Precursors revenues in South Korean market, 2019-2024 (Estimated), ($ millions)

• Key companies CVD & ALD Precursors revenues share in South Korean market, 2023 (%)

• Key companies CVD & ALD Precursors sales in South Korean market, 2019-2024 (Estimated),

• Key companies CVD & ALD Precursors sales share in South Korean market, 2023 (%)

1. Drivers:

- Growing Demand for Semiconductors: South Korea is a global leader in semiconductor manufacturing, driven by its strong presence in memory and logic chip production. The country’s semiconductor industry relies heavily on advanced materials and processes such as Chemical Vapor Deposition (CVD) and Atomic Layer Deposition (ALD) to meet the growing demand for high-performance and miniaturized devices. As semiconductor fabrication processes continue to advance toward smaller nodes (such as 5nm and below), the demand for high-quality CVD and ALD precursors is surging to enable the precise deposition of thin films and coatings used in advanced chips.

- Expansion of 5G and AI Applications: The rapid deployment of 5G networks and the growth of artificial intelligence (AI) applications in South Korea are key drivers for the CVD & ALD precursors market. Both 5G and AI technologies require advanced semiconductor chips with enhanced performance, low power consumption, and high-density integration. The precise thin-film deposition enabled by CVD and ALD processes is critical to achieving these requirements. As 5G and AI demand increases, the need for CVD and ALD precursors used in semiconductor manufacturing rises correspondingly.

- Advanced Display Technologies: South Korea is a leader in display technology innovation, particularly in the production of organic light-emitting diode (OLED) and quantum dot displays for televisions, smartphones, and other devices. The manufacturing of these advanced displays relies on CVD and ALD processes to deposit critical materials, such as metal oxides and nitrides, onto substrates with high precision and uniformity. As consumer demand for high-resolution, energy-efficient displays grows, the demand for CVD and ALD precursors for display production is also increasing.

- Electric Vehicle (EV) Growth: The rise of electric vehicles in South Korea is also contributing to the growth of the CVD & ALD precursors market. The development of EV batteries, power electronics, and sensor technologies requires advanced materials with improved energy efficiency, durability, and performance. CVD and ALD processes are used to deposit thin films in the production of components like lithium-ion batteries and power semiconductor devices, which are crucial for EVs. As South Korea continues to invest in its electric vehicle ecosystem, the need for CVD and ALD precursors in this sector is expected to increase.

- Government Support for Semiconductor and Display Industries: The South Korean government’s support for the semiconductor and display industries through subsidies, tax incentives, and R&D initiatives is fostering innovation in materials science, including CVD and ALD precursors. With a strong focus on maintaining the country’s leadership in advanced manufacturing, the government is actively investing in research and development for cutting-edge technologies, creating a conducive environment for the growth of the CVD & ALD precursors market.

2. Restraints:

- High Costs of CVD & ALD Processes: One of the major restraints for the CVD & ALD precursors market in South Korea is the high cost associated with these deposition processes. The materials used in CVD and ALD are often expensive, and the equipment required to perform these processes is highly specialized and costly. Additionally, maintaining precision and uniformity in deposition can be resource-intensive, requiring stringent quality control measures. These factors can limit the adoption of CVD and ALD technologies, especially among smaller manufacturers or industries with tighter margins.

- Environmental Concerns and Regulations: The use of certain CVD & ALD precursors can involve hazardous chemicals that pose environmental risks if not handled properly. South Korea, like many other countries, has stringent environmental regulations concerning the use and disposal of harmful chemicals in manufacturing processes. Ensuring compliance with these regulations adds to the operational costs for companies, which can be a deterrent for some manufacturers. The push toward greener and more sustainable manufacturing practices could also limit the use of certain traditional CVD and ALD precursors, requiring a shift to more eco-friendly alternatives.

- Supply Chain Disruptions: Global supply chain challenges, including shortages of raw materials and logistical disruptions, can affect the availability of critical CVD & ALD precursors. These disruptions have been exacerbated by factors such as the COVID-19 pandemic and geopolitical tensions. Given that South Korea’s semiconductor and display industries are highly reliant on uninterrupted supply chains for raw materials, any disruption can negatively impact production timelines and increase costs, posing a challenge for the CVD & ALD precursors market.

3. Opportunities:

- Emerging Applications in Quantum Computing: Quantum computing is an emerging field with the potential to revolutionize computing capabilities. The precise control and deposition of materials at the atomic level are critical for the development of quantum devices, making CVD and ALD technologies ideal for this purpose. As research and development in quantum computing accelerate in South Korea, there is an opportunity for the CVD & ALD precursors market to expand into this nascent field by providing advanced materials and deposition solutions tailored to quantum applications.

- Rising Adoption of ALD in Energy Storage: The use of ALD for energy storage devices, such as batteries and supercapacitors, is gaining traction due to its ability to improve the performance and longevity of these systems. In particular, ALD enables the deposition of ultra-thin protective layers on battery electrodes, which enhances their stability and lifespan. As South Korea continues to invest in clean energy and battery technology—especially in the context of electric vehicles and renewable energy storage—the market for ALD precursors in energy storage applications is poised for growth.

- Advancements in Flexible Electronics: The development of flexible and wearable electronics represents a growing market opportunity for CVD and ALD precursors in South Korea. These technologies require the deposition of highly uniform and flexible thin films that can maintain performance even under physical deformation. CVD and ALD processes are essential for producing the necessary materials for flexible displays, sensors, and other electronic components. As the demand for flexible and wearable electronics increases, the need for advanced deposition technologies and precursors will grow in tandem.

- Focus on Sustainable and Green Chemistry: As environmental concerns and sustainability become more prominent in South Korea, there is an increasing opportunity for the development of eco-friendly CVD & ALD precursors. Research into green chemistry solutions, such as non-toxic and biodegradable precursors, is underway to minimize the environmental impact of thin-film deposition processes. Companies that focus on creating sustainable alternatives for traditional precursors could tap into the growing demand for environmentally responsible manufacturing processes.

4. Challenges:

- Complexity of Deposition Processes: While CVD and ALD offer high precision in material deposition, the processes themselves are technically complex and require specialized expertise. Achieving the desired material properties—such as thickness, uniformity, and composition—requires fine-tuning of numerous process parameters, making it difficult for manufacturers without advanced technological capabilities. This complexity can be a barrier to adoption, particularly for companies transitioning from simpler deposition methods or those with limited experience in thin-film technologies.

- Market Competition from Alternative Deposition Methods: The CVD & ALD markets face competition from alternative deposition methods, such as physical vapor deposition (PVD) and molecular beam epitaxy (MBE), which may offer advantages in certain applications or cost structures. While CVD and ALD excel in precision and atomic-level control, alternative methods can be more suitable for large-scale production or less complex material requirements. This competition may limit the market share for CVD & ALD precursors, especially in industries where cost and speed are more critical than precision.

- Difficulty in Scaling to Mass Production: Although CVD and ALD are highly effective for producing high-performance thin films, scaling these processes to mass production can be challenging. The slow deposition rates inherent in ALD, in particular, make it difficult to use in large-scale manufacturing environments where throughput is a priority. Scaling these technologies without compromising on film quality or increasing costs is a key challenge that companies in the CVD & ALD precursors market need to address to capture larger market opportunities.

- Technological Obsolescence Risk: The rapid pace of innovation in semiconductor and display manufacturing technologies presents a risk of obsolescence for certain CVD & ALD precursors. As new materials and deposition techniques are developed, older precursor formulations may become less relevant or inefficient. To stay competitive, companies in the CVD & ALD precursors market must continuously innovate and adapt their product offerings to meet the evolving needs of advanced manufacturing processes, or risk being outpaced by competitors.

Key Indicators Analysed

• Market Players & Competitor Analysis: The report covers the key players of the industry including Company Profile, Product Specifications, Production Capacity/Sales, Revenue, Price and Gross Margin 2019-2030 & Sales with a thorough analysis of the market’s competitive landscape and detailed information on vendors and comprehensive details of factors that will challenge the growth of major market vendors.

• South Korean Market Analysis: The report includes South Korean market status and outlook 2019-2030. Further the report provides break down details about each region & countries covered in the report. Identifying its sales, sales volume & revenue forecast. With detailed analysis by types and applications.

• Market Trends: Market key trends which include Increased Competition and Continuous Innovations.

• Opportunities and Drivers: Identifying the Growing Demands and New Technology

• Porters Five Force Analysis: The report provides with the state of competition in industry depending on five basic forces: threat of new entrants, bargaining power of suppliers, bargaining power of buyers, threat of substitute products or services, and existing industry rivalry.

Key Benefits of This Market Research:

• Industry drivers, restraints, and opportunities covered in the study

• Neutral perspective on the market performance

• Recent industry trends and developments

• Competitive landscape & strategies of key players

• Potential & niche segments and regions exhibiting promising growth covered

• Historical, current, and projected market size, in terms of value

• In-depth analysis of the CVD & ALD Precursors Market

• Overview of the regional outlook of the CVD & ALD Precursors Market

Key Reasons to Buy this Report:

• Access to date statistics compiled by our researchers. These provide you with historical and forecast data, which is analyzed to tell you why your market is set to change

• This enables you to anticipate market changes to remain ahead of your competitors

• You will be able to copy data from the Excel spreadsheet straight into your marketing plans, business presentations or other strategic documents

• The concise analysis, clear graph, and table format will enable you to pinpoint the information you require quickly

• Provision of market value (USD Billion) data for each segment and sub-segment

• Indicates the region and segment that is expected to witness the fastest growth as well as to dominate the market

• Analysis by geography highlighting the consumption of the product/service in the region as well as indicating the factors that are affecting the market within each region

• Competitive landscape which incorporates the market ranking of the major players, along with new service/product launches, partnerships, business expansions, and acquisitions in the past five years of companies profiled

• Extensive company profiles comprising of company overview, company insights, product benchmarking, and SWOT analysis for the major market players

• The current as well as the future market outlook of the industry concerning recent developments which involve growth opportunities and drivers as well as challenges and restraints of both emerging as well as developed regions

• Includes in-depth analysis of the market from various perspectives through Porter’s five forces analysis

• Provides insight into the market through Value Chain

• Market dynamics scenario, along with growth opportunities of the market in the years to come

• 6-month post-sales analyst support

We offer additional regional and global reports that are similar:

• Global CVD & ALD Precursors Market

• United States CVD & ALD Precursors Market

• Japan CVD & ALD Precursors Market

• Germany CVD & ALD Precursors Market

• South Korea CVD & ALD Precursors Market

• Indonesia CVD & ALD Precursors Market

• Brazil CVD & ALD Precursors Market

Customization of the Report: In case of any queries or customization requirements, please connect with our sales team, who will ensure that your requirements are meet.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...