Solid-state DC Breaker Market Insights

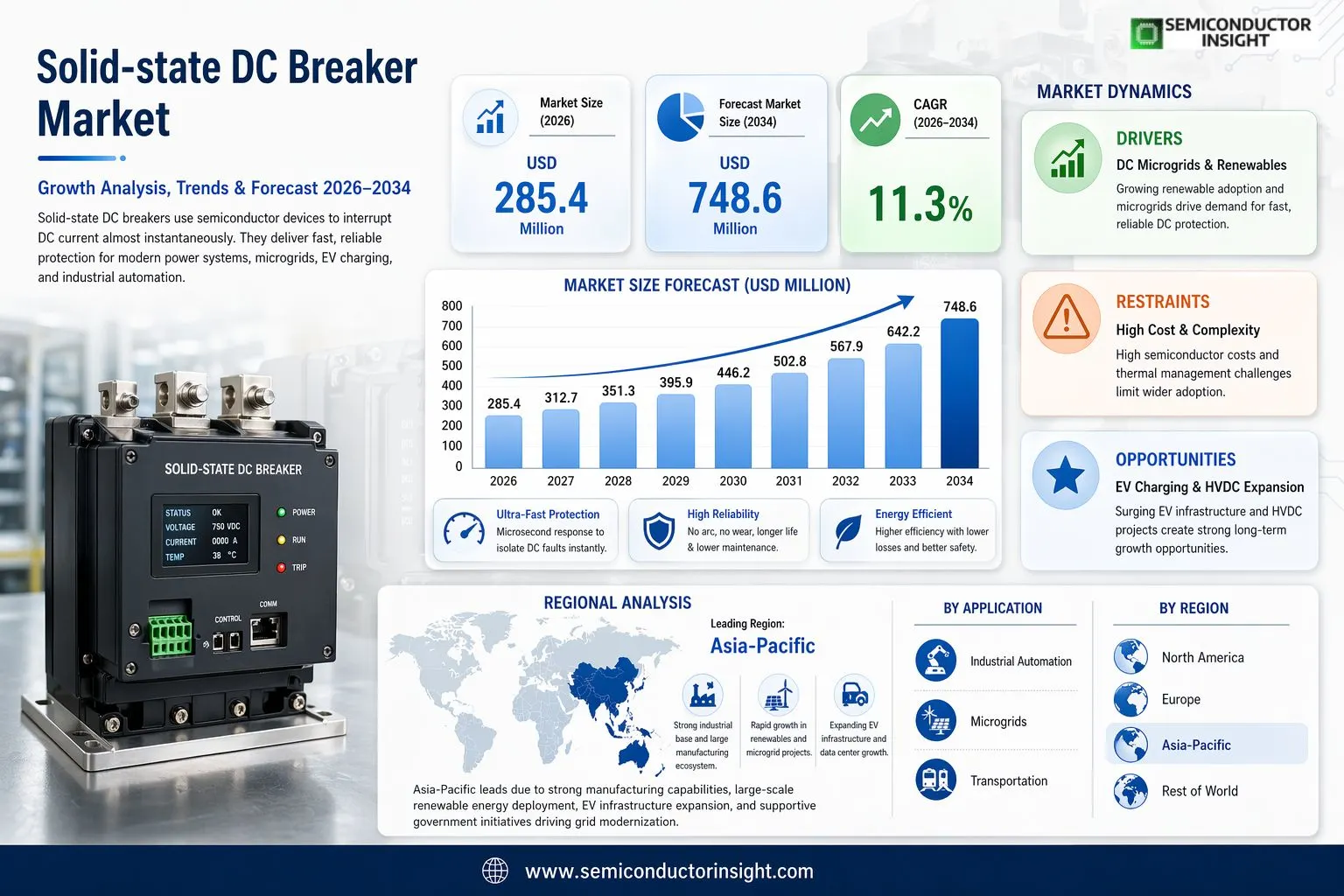

Global Solid-state DC Breaker market size was valued at USD 285.4 million in 2026. The market is projected to grow from USD 312.7 million in 2026 to USD 748.6 million by 2034, exhibiting a CAGR of 11.3% during the forecast period.

The solid-state DC breaker is a highly efficient, fast-acting circuit breaker designed specifically for DC systems, utilizing semiconductor devices to interrupt the current flow. Unlike traditional mechanical DC breakers, which rely on moving parts to physically separate the contacts and extinguish arcs, solid-state DC breakers use power semiconductors such as Insulated Gate Bipolar Transistors (IGBTs), Metal-Oxide-Semiconductor Field-Effect Transistors (MOSFETs), or thyristors. These components enable the breaker to respond almost instantaneously to fault conditions, making them ideal for modern power systems with high-speed demands. The product range spans across low voltage, medium voltage, and high voltage configurations, serving applications in industrial automation, microgrids, and transportation sectors.

The market is experiencing robust growth driven by the accelerating global transition toward DC-based power infrastructure, rapid expansion of renewable energy installations, and the increasing deployment of electric vehicle (EV) charging networks. The proliferation of microgrid projects and HVDC transmission systems has created a strong demand for faster, more reliable fault protection solutions that traditional mechanical breakers cannot adequately provide. Furthermore, the rising adoption of solid-state DC breakers in data centers and industrial automation environments underscores the technology’s expanding commercial footprint. Key players actively shaping the competitive landscape include ABB, Siemens, Fuji Electric, Eaton, Atom Power, Shanghai KingSi Power, Fullde Electric, and Sun.King Technology, among others, each contributing to product innovation and global market penetration.

MARKET DRIVERS

Accelerating Adoption of DC Microgrids and Renewable Energy Integration

Global transition toward decentralized and renewable energy systems has become one of the most significant forces propelling Solid State DC Breaker Market forward. As solar photovoltaic installations and battery energy storage systems continue to expand at scale, the demand for reliable, fast-acting DC protection devices has intensified. Unlike conventional mechanical breakers, solid-state DC breakers offer switching speeds in the microsecond to millisecond range, which is critical for protecting sensitive power electronics in modern DC architectures. Governments across North America, Europe, and Asia-Pacific have introduced ambitious renewable energy targets, further reinforcing infrastructure investments that require advanced DC circuit protection solutions.

Growth of Electric Vehicle Charging Infrastructure and EV Ecosystem

The rapid global expansion of electric vehicle adoption has created a substantial downstream demand for robust DC protection technology. High-power DC fast-charging stations operating at voltages between 400V and 1,000V require breakers capable of interrupting fault currents without generating arcs , a fundamental limitation of traditional electromechanical devices. The solid-state DC breaker addresses this requirement through semiconductor-based switching elements such as IGBTs and MOSFETs, which enable arc-free interruption and extend operational lifespan significantly. Major automotive markets including China, Germany, and the United States are actively scaling their charging networks, making high-performance DC protection a prerequisite for safe and reliable infrastructure deployment.

➤ Solid-state DC breakers are increasingly being specified in utility-scale battery storage projects and EV charging hubs due to their ability to operate reliably in high-cycling environments with minimal maintenance requirements compared to mechanical counterparts.

Beyond renewable energy and mobility, the proliferation of high-voltage direct current (HVDC) transmission networks across intercontinental and offshore grid projects represents another powerful market driver. HVDC systems are inherently vulnerable to DC fault propagation, which can cause cascading failures across entire transmission corridors. Solid-state DC breakers, with their ability to isolate faults within microseconds, are increasingly regarded as an enabling technology for multi-terminal HVDC grids. Strategic investments by grid operators and utilities in Europe and Asia are expected to sustain strong demand within this segment throughout the forecast period.

MARKET CHALLENGES

High Manufacturing Costs and Complexity of Power Semiconductor Components

Despite the clear technical advantages of solid-state DC breakers, high unit costs remain the most immediate challenge limiting broader market penetration. The core switching elements , including wide bandgap semiconductors such as silicon carbide (SiC) and gallium nitride (GaN) , are significantly more expensive to manufacture than conventional silicon-based components or the copper contacts used in mechanical breakers. For many distribution-level applications, the total cost of ownership can be difficult to justify in the near term, particularly in price-sensitive markets across developing economies. Additionally, the thermal management requirements associated with continuous conduction losses in power semiconductors add further complexity and cost to the overall system design.

Other Challenges

Lack of Standardization Across Voltage Classes

Solid State DC Breaker Market currently operates across a fragmented landscape of voltage ratings, communication protocols, and protection coordination standards. The absence of universally adopted IEC or IEEE standards specific to solid-state DC protection devices creates integration barriers for system designers and utilities. This challenge is particularly evident in multi-vendor microgrid and HVDC projects, where interoperability between protection, control, and monitoring equipment from different manufacturers cannot always be guaranteed without extensive custom engineering.

Limited Field Track Record and Utility Acceptance

While solid-state DC breakers have demonstrated strong performance in laboratory and pilot environments, many utility operators and industrial end-users remain cautious due to the relatively limited long-term field deployment history compared to decades of proven mechanical breaker performance. Gaining acceptance within conservative procurement and engineering approval frameworks requires sustained demonstration projects, third-party certification, and long-term reliability data , all of which take considerable time and investment to accumulate in the marketplace.

MARKET RESTRAINTS

Conduction Losses and Thermal Management Limitations in Continuous Operation

One of the most technically consequential restraints facing Solid State DC Breaker Market is the inherent on-state conduction loss associated with semiconductor switching devices. Unlike mechanical breakers, which present virtually zero resistance when closed, solid-state devices exhibit a forward voltage drop that results in continuous power dissipation during normal operation. In high-current applications, this thermal burden can be substantial, necessitating sophisticated heat sink designs, forced cooling systems, or active thermal management strategies that add both cost and physical footprint to the installation. For applications requiring continuous high-current ratings above several kiloamperes, these thermal constraints can limit the competitiveness of solid-state solutions against hybrid alternatives.

Regulatory Uncertainty and Evolving Protection Coordination Frameworks

The regulatory environment surrounding DC distribution and transmission protection remains in an active state of evolution in most major markets. Existing grid codes and protection standards were largely developed with AC systems in mind, and the adaptation of these frameworks to accommodate solid-state DC breaker technology has progressed at an uneven pace across different jurisdictions. In certain regions, the absence of clear regulatory pathways for approving and certifying DC protection equipment at utility scale creates project delays and increases the perceived risk for investors and grid operators. Until harmonized international standards are fully established and enforced, regulatory ambiguity will continue to act as a meaningful restraint on market expansion, particularly for large-scale HVDC and offshore wind integration projects.

MARKET OPPORTUNITIES

Wide Bandgap Semiconductor Advancements Opening New Application Horizons

The ongoing commercialization of silicon carbide (SiC) and gallium nitride (GaN) power semiconductors presents a transformative opportunity for Solid State DC Breaker Market. These wide bandgap materials offer significantly higher breakdown voltages, lower on-state resistance, and superior thermal conductivity compared to conventional silicon, directly addressing the conduction loss and thermal management challenges that have historically constrained solid-state DC breaker adoption. As manufacturing volumes for SiC and GaN devices scale upward and unit costs continue to decline, a growing range of medium-voltage and high-voltage DC applications will become economically viable for solid-state protection solutions, expanding the addressable market considerably over the coming decade.

Offshore Wind and Multi-Terminal HVDC Grid Expansion

The accelerating development of offshore wind energy corridors, particularly across the North Sea, Baltic Sea, and emerging markets in Asia-Pacific, represents one of the most substantial near-term growth opportunities for solid-state DC breaker technology. Offshore HVDC collector networks and multi-terminal interconnectors require protection devices capable of isolating DC faults with extreme speed to prevent damage to expensive subsea cable infrastructure and converter stations. Solid-state DC breakers are uniquely positioned to fulfill this role, and several large-scale offshore interconnection projects currently in planning or early construction phases are expected to serve as flagship deployments that validate the technology’s performance at scale. Successful execution of these projects will likely catalyze broader utility adoption across both offshore and onshore HVDC applications globally.

Data Center and Industrial DC Power Distribution Modernization

Global data center industry’s gradual migration toward 400V DC power distribution architectures offers an emerging and commercially significant opportunity for solid-state DC breaker manufacturers. DC distribution within data centers eliminates multiple AC-DC conversion stages, improving overall energy efficiency , a priority driven by sustainability mandates and rising energy costs. As hyperscale and colocation data center operators evaluate DC-native power infrastructure, the requirement for reliable, intelligent, and compact DC protection devices will grow in parallel. Similarly, industrial facilities adopting DC bus topologies for motor drives, robotics, and electrified process equipment represent an expanding customer base for Solid-state DC Breaker Market participants seeking diversified revenue streams beyond utility-scale applications.

Trends

Rising Adoption of Semiconductor-Based Protection Devices Reshaping DC Power Infrastructure

Solid State DC Breaker Market is experiencing a notable shift driven by the accelerating transition toward advanced DC power systems across industrial and energy sectors. Unlike conventional mechanical breakers, solid-state DC breakers leverage semiconductor components such as IGBTs, MOSFETs, and thyristors to deliver near-instantaneous fault interruption. This technological superiority is increasingly recognized by grid operators, industrial facility managers, and transportation system designers who require high-speed, reliable protection for sensitive DC networks. The demand for faster response times and reduced maintenance requirements continues to position solid-state DC breakers as a preferred choice in modern power infrastructure planning.

Other Trends

Expansion Across Microgrid and Renewable Energy Applications

One of the most prominent trends shaping Solid State DC Breaker Market is the rapid proliferation of microgrids and distributed renewable energy systems. As solar photovoltaic installations and battery energy storage systems expand globally, the need for effective DC-side protection has grown considerably. Solid-state DC breakers are increasingly integrated into microgrid architectures to manage fault conditions with precision and speed that mechanical alternatives cannot match. This trend is particularly evident across North America, Europe, and Asia, where regulatory support for clean energy infrastructure is reinforcing investment in advanced protection technologies.

Industrial Automation Driving Low Voltage Segment Demand

The industrial automation sector represents a key application area contributing to sustained momentum in Solid State DC Breaker Market. Manufacturing facilities deploying automated production lines, robotics, and DC-powered motor drives require circuit protection solutions that can respond to fault events without disrupting sensitive control systems. The low voltage segment, in particular, is witnessing strong adoption as automation investments intensify across sectors including automotive, electronics, and process manufacturing. Leading market participants such as ABB, Siemens, Eaton, and Fuji Electric have continued to refine their solid-state DC breaker product lines to address the evolving requirements of industrial end users.

Transportation Electrification Emerging as a High-Growth Application Segment

The electrification of transportation systems is emerging as a significant trend influencing Solid State DC Breaker Market. Electric vehicles, rail networks, and maritime electrification projects are generating considerable demand for DC circuit protection devices capable of operating reliably under high-current, high-speed conditions. As governments and private operators accelerate electrification programs, solid-state DC breakers are increasingly specified for traction power systems, EV charging infrastructure, and onboard power distribution. The participation of companies such as Atom Power, Shanghai KingSi Power, Fullde Electric, and Sun.King Technology reflects a competitive and innovation-driven market landscape responding to these emerging application demands across multiple geographies.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Solid-State DC Breaker Market: Competitive Dynamics, Leading Manufacturers, and Strategic Positioning

Global solid-state DC breaker market is characterized by a moderately consolidated competitive landscape, with a handful of established power electronics and electrical equipment giants commanding a significant share of revenues. ABB and Siemens stand out as the dominant forces, leveraging decades of expertise in power protection systems, extensive R&D capabilities, and broad global distribution networks. These companies have been at the forefront of integrating advanced semiconductor technologies , including IGBTs and MOSFETs , into next-generation DC protection solutions tailored for industrial automation, microgrids, and transportation infrastructure. In 2026, Global top five players collectively accounted for a substantial portion of total market revenue, underscoring the degree to which technological leadership and established customer relationships serve as key competitive differentiators in this space.

Beyond the tier-one incumbents, a growing cohort of specialized and regional players is intensifying competition across niche voltage segments. Companies such as Atom Power have distinguished themselves through innovative all-digital solid-state breaker platforms targeting low and medium voltage applications, while Asian manufacturers including Shanghai KingSi Power, Fullde Electric, and Sun.King Technology are gaining traction by offering cost-competitive solutions tailored to the rapidly expanding renewable energy and microgrid sectors across Asia-Pacific. Fuji Electric and Eaton further strengthen the mid-tier competitive field with diversified product portfolios spanning low, medium, and high voltage solid-state DC breakers. As demand accelerates across electric vehicle charging infrastructure, offshore wind, and data center power systems, competition is expected to intensify, with both established players and emerging specialists investing heavily in product innovation, strategic partnerships, and geographic expansion to capture incremental market share.

List of Key Solid-State DC Breaker Companies Profiled

- ABB

- Siemens

- Fuji Electric

- Eaton

- Atom Power

- Shanghai KingSi Power

- Fullde Electric

- Sun.King Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Low Voltage solid-state DC breakers represent the leading segment within the type classification, driven by their broad applicability across a diverse range of commercial and industrial settings. Key qualitative insights include:

Medium and High Voltage segments are gaining traction in utility-scale renewable energy projects and high-power transmission applications, where the elimination of arc-related hazards and mechanical wear represents a compelling operational advantage over conventional breaker technologies. |

| By Application |

|

Industrial Automation stands out as the dominant application segment for solid-state DC breakers, reflecting the ongoing transformation of manufacturing environments toward highly automated, digitally integrated production lines. Key qualitative insights include:

The Microgrids segment is emerging as a high-growth application area, fueled by global investments in renewable energy integration and the expansion of islanded and community energy systems. Transportation applications, particularly in electric rail, marine electrification, and electric vehicles, also represent an increasingly significant demand source driven by decarbonization mandates. |

| By End User |

|

Commercial & Industrial end users represent the leading end-user segment in Solid State DC Breaker Market, underpinned by robust capital investment in modernized electrical infrastructure, energy efficiency programs, and the rapid deployment of on-site renewable energy generation. Key qualitative insights include:

Utilities and power generation entities are progressively adopting solid-state DC breakers in HVDC transmission corridors and grid-scale battery storage installations, driven by grid modernization programs worldwide. |

| By Technology |

|

IGBT-Based solid-state DC breakers hold the leading position within the technology segment, owing to their well-established performance characteristics and proven reliability across a wide spectrum of voltage and current ratings. Key qualitative insights include:

|

| By Installation Type |

|

New Installation represents the dominant installation type segment, reflecting the accelerating pace of greenfield infrastructure development across renewable energy, data center, and electrified transportation sectors globally. Key qualitative insights include:

|

Regional Analysis: Solid-state DC Breaker Market

Asia-Pacific

Asia-Pacific’s ambitious solar and wind energy deployment programs have created a pressing need for reliable DC protection solutions. As utility-scale photovoltaic farms and offshore wind installations multiply across China, India, and Southeast Asia, solid-state DC breakers are becoming indispensable components in ensuring safe and efficient energy conversion, storage, and distribution across complex multi-directional DC networks.

The rapid proliferation of electric vehicles across China, Japan, and South Korea is generating robust demand for advanced DC circuit protection in fast-charging networks. Solid-state DC breakers provide the ultra-fast fault interruption required to safeguard sensitive EV charging equipment and battery systems, making them a preferred choice as regional governments mandate the expansion of high-power public and commercial charging infrastructure.

Asia-Pacific’s vast industrial base, spanning semiconductor fabrication, consumer electronics, heavy machinery, and precision manufacturing, demands highly reliable DC protection solutions. Solid-state DC breakers are increasingly integrated into factory automation systems, robotics, and process control equipment across the region, where even momentary power disruptions carry significant production and financial consequences, driving strong sustained market demand.

Supportive regulatory frameworks and substantial government investment in smart grid modernization across Asia-Pacific are accelerating solid-state DC breaker adoption. National energy security priorities in China, India, and ASEAN nations are driving procurement of advanced grid protection technologies. Incentive programs targeting grid resilience, energy storage integration, and low-carbon transition further underpin long-term regional market growth prospects through 2034.

North America

North America represents a highly significant and technologically mature market for solid-state DC breakers, underpinned by extensive grid modernization efforts, a rapidly growing renewable energy sector, and strong adoption of electric mobility solutions. The United States leads regional demand, with federal infrastructure investments channeling substantial funding toward upgrading aging electrical grids with advanced protection technologies. The proliferation of utility-scale battery energy storage systems and solar installations across the Sun Belt states is creating direct demand for high-performance DC circuit protection. Canada’s expanding clean energy ambitions and increasing cross-border HVDC transmission developments further reinforce the regional market. The presence of leading semiconductor manufacturers, power electronics innovators, and established utility companies with strong procurement capabilities positions North America as a critical hub for both solid-state DC breaker development and deployment through the forecast period.

Europe

Europe occupies a prominent position in Global solid-state DC breaker market, propelled by the region’s landmark energy transition commitments and comprehensive electrification strategies. The European Union’s Green Deal and REPowerEU initiatives have catalyzed unprecedented investment in offshore wind energy, pan-European HVDC interconnects, and distributed renewable generation, all of which require sophisticated DC fault protection solutions. Germany, the United Kingdom, the Netherlands, and the Nordic countries are particularly active in deploying solid-state DC breaker technologies across both transmission and distribution applications. The region’s strong regulatory environment, which mandates grid reliability and sustainability standards, encourages utilities and industrial operators to adopt next-generation protection technologies. Europe’s advanced automotive industry, undergoing rapid electrification, is also a meaningful contributor to regional solid-state DC breaker demand, particularly in EV powertrain and charging infrastructure applications.

South America

South America is an emerging market for solid-state DC breakers, with growth prospects closely tied to the region’s expanding renewable energy sector and gradual grid infrastructure modernization. Brazil leads regional activity, benefiting from substantial hydropower resources being complemented by rapidly growing wind and solar capacity, which requires advanced DC protection for reliable integration. Chile and Colombia are also demonstrating increasing interest in solid-state DC breaker solutions as they pursue clean energy diversification strategies. While market development in South America remains at an earlier stage compared to Asia-Pacific and North America, rising foreign direct investment in power infrastructure, improving grid interconnection projects, and growing awareness of the operational benefits of solid-state protection technologies are collectively establishing a positive growth trajectory for Solid State DC Breaker Market across the region through 2034.

Middle East & Africa

The Middle East and Africa region presents a developing yet progressively important landscape for Solid State DC Breaker Market. Gulf Cooperation Council nations, particularly Saudi Arabia and the UAE, are making substantial investments in large-scale solar power projects and smart grid infrastructure as part of ambitious national energy diversification programs, generating growing demand for advanced DC protection technologies. Africa’s vast untapped renewable energy potential, especially in solar irradiance-rich sub-Saharan regions, is attracting increasing international investment in off-grid and mini-grid electrification projects where solid-state DC breakers offer distinct reliability advantages over conventional mechanical alternatives. While infrastructure constraints and budget limitations continue to moderate near-term market penetration in parts of Africa, the long-term outlook remains constructive as electrification rates improve, regional energy cooperation deepens, and awareness of solid-state DC breaker benefits grows among utilities and independent power producers across the Middle East and Africa.

Report Scope

This market research report provides a comprehensive analysis of Solid State DC Breaker Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Solid State DC Breaker Market?

-> Global Solid-state DC Breaker Market was valued at USD million in 2026 and is projected to reach USD million by 2032, growing at a CAGR of % during the forecast period.

Which key companies operate in Solid State DC Breaker Market?

-> Key players include ABB, Siemens, Fuji Electric, Eaton, Atom Power, Shanghai KingSi Power, Fullde Electric, and Sun.King Technology, among others. In 2026, Global top five players held approximately % share in terms of revenue.

What are the key growth drivers?

-> Key growth drivers include increasing adoption of DC-based power systems, rapid expansion of microgrids, growing demand for industrial automation, and the need for high-speed fault protection in modern power infrastructure. The use of advanced semiconductor devices such as IGBTs, MOSFETs, and thyristors enables near-instantaneous response to fault conditions, making solid-state DC breakers essential for next-generation power systems.

Which region dominates the market?

-> Asia-Pacific is a key growth region, with China projected to reach USD million by the end of the forecast period. North America also holds a significant share, with the U.S. market estimated at USD million in 2026.

What are the emerging trends?

-> Emerging trends include widespread deployment of solid-state DC breakers in microgrids and transportation sectors, rising integration with industrial automation systems, and growing shift from mechanical to semiconductor-based circuit protection solutions. The Low Voltage segment is also anticipated to witness notable growth, projected to reach USD million by 2032 with a CAGR of % over the next six years.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...