MARKET INSIGHTS

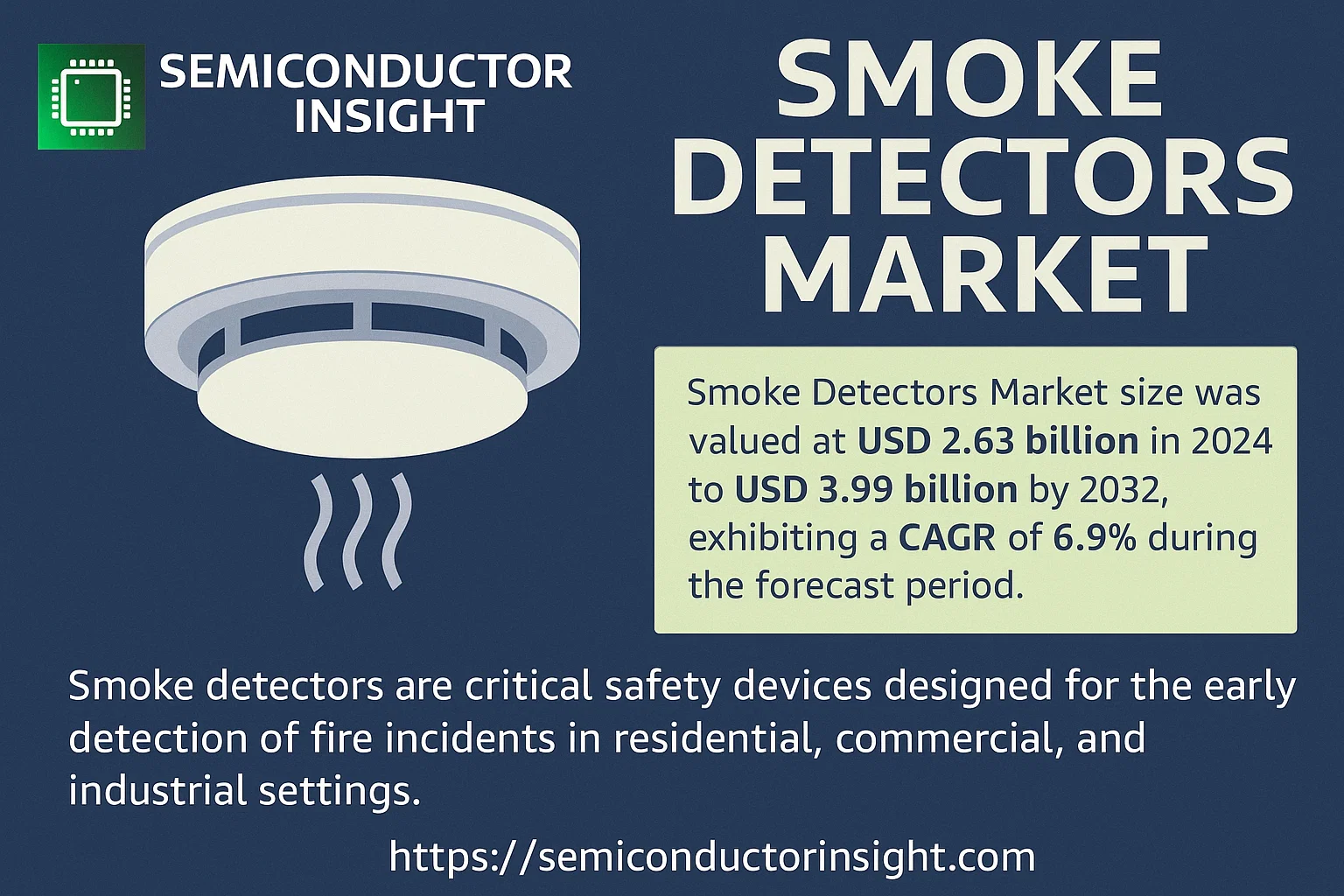

Global Smoke Detectors Market size was valued at USD 2.63 billion in 2024 to USD 3.99 billion by 2032, exhibiting a CAGR of 6.9% during the forecast period.

Smoke detectors are critical safety devices designed for the early detection of fire incidents in residential, commercial, and industrial settings. These devices function by sensing smoke particles in the air, triggering an audible and/or visual alarm to alert occupants of potential danger. The primary technologies used include photoelectric sensors, which detect visible smoke particles through light scattering, and ionization sensors, which detect invisible combustion particles through electrical current disruption. Dual-sensor alarms combine both technologies for comprehensive protection.

The market is experiencing steady growth due to several factors, including stringent government regulations mandating smoke detector installations in residential and commercial buildings, increasing awareness about fire safety, and rising construction activities worldwide. Additionally, technological advancements such as smart smoke detectors with Wi-Fi connectivity, battery monitoring, and integration with home automation systems are contributing to market expansion. Initiatives by key players in developing innovative products are also expected to fuel market growth. For instance, manufacturers are increasingly focusing on interconnected systems that allow all detectors in a building to sound an alarm when one detects smoke. Honeywell International Inc., Carrier Global Corporation, Johnson Controls International plc, and Siemens AG are some of the key players that operate in the market with diverse product portfolios.

MARKET DRIVERS

Stringent Safety Regulations and Building Codes

The global smoke detector market is primarily driven by the enforcement of stringent government regulations and building safety codes mandating the installation of smoke alarms in residential and commercial properties. Legislative bodies worldwide have continuously updated fire safety standards, compelling new constructions and renovations to incorporate advanced detection systems. This regulatory pressure creates a steady, non-discretionary demand cycle for smoke detector manufacturers and suppliers.

Increasing Urbanization and Infrastructure Development

Rapid urbanization, particularly in emerging economies, is leading to a surge in the construction of residential high-rises, commercial complexes, and industrial facilities. This expansion directly fuels the demand for fire safety equipment. The growing real estate sector, coupled with rising disposable incomes, is encouraging homeowners to invest in enhanced safety solutions, including interconnected and smart smoke detectors.

➤ The growing consumer awareness regarding the importance of early fire detection for life and property protection is a significant behavioral driver shaping market growth.

Furthermore, technological advancements are a key driver. The integration of IoT and wireless connectivity allows for smart detectors that provide remote alerts and integration with home automation systems. The development of dual-sensor and multi-criteria detectors, which reduce false alarms, is also pushing replacement and upgrade cycles in mature markets.

MARKET CHALLENGES

High Prevalence of False Alarms

A significant challenge facing the industry is the high rate of nuisance or false alarms, often caused by cooking smoke, steam, or dust. Frequent false alarms can lead to alarm fatigue, where occupants become desensitized and may ignore a real alarm, compromising safety. This issue drives the need for more sophisticated sensor technology, which can increase product costs and complexity.

Other Challenges

Price Sensitivity and Cost Constraints

In highly competitive and price-sensitive markets, particularly in the residential segment, the cost of advanced smoke detectors can be a barrier to adoption. Consumers and building managers often opt for basic, low-cost photoelectric or ionization units, delaying the uptake of more effective but expensive interconnected or smart detector systems.

Technical Complexity and Installation Barriers

The installation of interconnected systems, especially in existing buildings without pre-wiring, can be complex and costly. The need for professional installation for certain systems acts as a deterrent for some consumers, favoring simpler, standalone battery-operated units that may offer less comprehensive protection.

MARKET RESTRAINTS

Market Saturation in Developed Regions

The smoke detector market in developed regions like North America and Western Europe is highly mature and saturated. With high penetration rates in residential sectors, growth is largely dependent on replacement sales and technology upgrades rather than new installations. This limits the potential for high-volume growth in these key markets.

Long Product Lifecycle and Replacement Cycles

Smoke detectors are durable goods with a typical lifespan of 8-10 years. This long product lifecycle means that the replacement market operates on a slow cycle, restraining frequent sales opportunities. Consumers are often reluctant to replace functional units before their end-of-life, delaying the adoption of newer, safer technologies.

MARKET OPPORTUNITIES

Advent of Smart Homes and IoT Integration

The proliferation of smart home ecosystems presents a substantial growth opportunity. Smoke detectors with Wi-Fi or Bluetooth connectivity can send alerts to smartphones, integrate with other smart home devices (like turning on lights during an alarm), and provide system status updates. This added functionality is creating a premium segment and driving replacement demand among tech-savvy consumers.

Growth in Emerging Economies

There is significant untapped potential in emerging economies across Asia-Pacific, Latin America, and the Middle East. Improving economic conditions, rising safety awareness, and the development of modern infrastructure are expected to drive substantial demand for basic and advanced smoke detection systems in these regions over the coming decade.

Innovation in Sensor Technology

Continuous innovation, such as the development of advanced multi-sensor detectors that combine photoelectric, thermal, and carbon monoxide sensing, offers opportunities to create more reliable products that minimize false alarms. This technological differentiation allows companies to capture value in the competitive market and appeal to safety-conscious buyers.

Smoke Detectors Market Trends

Strong Market Growth Fueled by Regulation

The global Smoke Detectors market is on a steady growth trajectory, valued at US$ 2634 million in 2024 and projected to reach US$ 3987 million by 2032, reflecting a compound annual growth rate (CAGR) of 6.9%. This sustained expansion is heavily influenced by stringent government regulations, particularly in Europe. Countries including Norway, Denmark, Sweden, Finland, the UK, France, Ireland, Austria, Belgium, Germany, and the Netherlands have made smoke detector installation mandatory in residential housing. These government mandates, driven by the critical need for early fire detection to ensure occupant safety, are a primary driver for market penetration and new installations across the region.

Other Trends

Technological Segmentation and Multi-Sensor Adoption

The market is segmented by the type of detection technology, primarily into photoelectric smoke alarms, ionization smoke alarms, and dual-sensor alarms. Photoelectric detectors use a light beam and receptor, triggering an alarm when smoke particles disrupt the light. Ionization detectors contain a charged chamber where smoke particles disrupt an electric current to activate the alarm. Each technology has distinct performance characteristics in different fire scenarios, leading to a growing trend towards dual-sensor alarms and units that combine smoke detection with heat or carbon monoxide sensors, offering more comprehensive protection and driving product innovation.

Consolidated Competitive Landscape

The competitive environment features prominent global players such as Honeywell, Carrier, and Resideo. These leading giants often operate multiple sub-brands; for example, Honeywell’s portfolio includes Xtralis, Notifier, and System Sensor, while Carrier owns brands like Kidde and Edwards. In the European market specifically, key manufacturers include Ei Electronics, Hekatron, and Bosch, with the top five players holding a combined revenue share of approximately 47% in 2023. This indicates a relatively consolidated market where innovation, compliance with strict European norms, and strategic branding are key to maintaining competitive advantage.

COMPETITIVE LANDSCAPE

Key Industry Players

Globally Consolidated Market Led by Diversified Industrial Giants

The global smoke detectors market is characterized by a high degree of consolidation, dominated by large, diversified industrial corporations that have expanded into the fire safety and building technologies sectors. Global leaders such as Honeywell, Carrier Global Corporation (through its Kidde brand), and Johnson Controls command a significant share of the market. These players leverage extensive distribution networks, strong brand recognition, and comprehensive product portfolios that include not only individual smoke alarms but also integrated fire detection systems for commercial and industrial applications. The competitive environment is further intensified by the presence of major European players like Bosch, Siemens, and Schneider Electric. In Europe, the top five players collectively held approximately 47% of the market revenue in 2023, highlighting the concentrated nature of the market, particularly in regions with stringent regulatory mandates for residential smoke alarms.

Numerous smaller and specialized companies occupy significant niches, offering products tailored to specific regional requirements, technologies, or price points. European specialists such as Ei Electronics, Hekatron (part of Swiss Securitas Group), and FireAngel Safety Technology hold strong positions in their domestic markets, often benefiting from deep understanding of local standards. Beyond the industrial heavyweights, companies like Google Nest have entered the market with smart, connected devices, targeting the growing consumer demand for integrated home safety systems. Similarly, Asian manufacturers, including Panasonic Fire & Security, Hochiki, and Nittan Group, are prominent players, especially in the commercial and industrial segments. Independent brands like Resideo (First Alert) and new entrants from China, such as X-Sense Technology, compete effectively in the volume-driven residential sector with a focus on affordability and innovation.

List of Key Smoke Detectors Companies Profiled

- Honeywell

- Carrier Global Corporation

- Resideo (First Alert)

- Ei Electronics

- Google Nest

- Johnson Controls

- Swiss Securitas Group

- Bosch

- Schneider Electric

- Siemens

- Hochiki

- Nittan Group

- Nohmi Bosai Limited

- FireAngel Safety Technology

- Halma

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Dual Sensor Smoke Alarm is emerging as a highly preferred segment due to its comprehensive detection capabilities, combining the strengths of both photoelectric and ionization technologies. Photoelectric detectors are superior at sensing slow, smoldering fires, while ionization detectors respond faster to flaming fires with invisible combustion particles. The dual-sensor technology addresses the limitation of single-sensor units, offering broader protection and reducing the risk of nuisance alarms, which is a key purchasing consideration for both residential and commercial users. This trend reflects a growing consumer demand for more reliable and technologically advanced safety solutions. |

| By Application |

|

Residential/Home remains the dominant application segment, driven primarily by stringent government mandates for smoke detector installation in new and existing dwellings across many countries, particularly in Europe. The fundamental need for life safety in the home environment creates a consistent and high-volume demand. Beyond regulation, growing public awareness of fire safety, the integration of smoke detectors with smart home systems for remote alerts, and replacement cycles for older units further solidify this segment’s leadership. The commercial segment also shows robust growth, fueled by complex building safety codes and the need to protect high-value assets and ensure business continuity. |

| By End User |

|

Building Contractors & Developers constitute a leading end-user segment due to their role in fulfilling mandatory installation requirements in new construction projects. This segment demands products that meet specific building codes and standards, often purchasing in bulk and favoring established, certified brands. Their purchasing decisions are heavily influenced by compliance, reliability, and integration capabilities with other building systems. Meanwhile, the homeowner and tenant segment is increasingly seeking user-friendly, aesthetically pleasing, and interconnected devices that offer seamless integration with broader home automation platforms for enhanced convenience and control. |

| By Technology Integration |

|

Smart/Connected Detectors represent the fastest-evolving and most dynamic segment. These devices offer features far beyond basic alarm functionality, including mobile app notifications, integration with voice assistants, self-testing capabilities, and interconnection with other smart home devices like lights and door locks. This segment is driven by the proliferation of the Internet of Things (IoT) and consumer demand for integrated safety and convenience. While currently a premium offering, the value proposition of remote monitoring and automated responses is making smart detectors increasingly attractive, particularly in the residential upgrade market and new high-end commercial installations. |

| By Power Source |

|

Hardwired with Battery Backup is the leading segment, especially in new construction and major renovations, as it is often mandated by building codes for its superior reliability. This configuration ensures continuous operation even during power outages, a critical feature during a fire event. Battery-powered units maintain strong demand for their ease of installation in existing homes without dedicated wiring and for use as supplementary detectors. However, the trend is shifting towards hardwired systems with backup power due to their fail-safe nature and the growing integration with centralized home security and fire alarm panels, which require a constant power source for full functionality. |

Regional Analysis: Smoke Detectors Market

The market is heavily influenced by building codes from organizations like NFPA, which mandate specific types of smoke detectors (photoelectric, ionization, combination) in new constructions and renovations. This creates a non-discretionary demand cycle that ensures market stability and drives compliance-driven sales.

A key driver is the rapid integration of smoke detectors into the Internet of Things (IoT). Consumers increasingly seek devices that connect to smartphones and home assistants, providing real-time alerts and system status checks, which encourages the replacement of older, conventional units with advanced smart detectors.

The region hosts several globally recognized manufacturers who compete intensely on innovation, brand reputation, and product reliability. This competition leads to frequent new product launches with improved sensitivity, battery life, and user-friendly features, constantly raising the market standard.

High public awareness about fire safety, fueled by government campaigns and insurance incentives, ensures a robust replacement market. Homeowners are proactive about replacing outdated units, particularly with the recommended ten-year lifespan, creating a steady aftermarket demand independent of new construction cycles.

Europe

The European smoke detector market is a well-developed and steadily growing region, shaped by a harmonized yet diverse regulatory framework across member states. The introduction of EU-wide standards and directives has been a significant catalyst, pushing for higher safety benchmarks in residential properties. Markets in Western Europe, such as Germany, the UK, and France, are mature with high penetration rates, driven by strict national building regulations and a strong culture of risk mitigation. In contrast, Eastern European countries are experiencing faster growth as they align with EU norms, representing a key growth frontier. The region shows a clear preference for photoelectric smoke detectors due to their effectiveness in detecting smoldering fires, which are common in residential settings. Sustainability and product certifications like the CE mark are critical factors influencing consumer and professional purchasing decisions.

Asia-Pacific

The Asia-Pacific region is the fastest-growing market for smoke detectors globally, fueled by rapid urbanization, massive infrastructure development, and rising safety consciousness. Countries like China, Japan, and Australia have implemented stringent fire safety laws, mandating detectors in new buildings. The market is highly diverse, with mature markets in Australia and Japan coexisting with emerging giants like China and India, where growth potential is immense due to low penetration rates and increasing construction activities. Price sensitivity is a key characteristic, driving demand for cost-effective yet reliable solutions. Local manufacturers are becoming increasingly influential, competing with international players by offering affordable products tailored to regional needs. The adoption of wireless and smart detectors is also gaining traction in urban centers, following global trends.

South America

The South American smoke detector market is in a developing phase, characterized by growing awareness but varying levels of regulatory enforcement. Brazil and Argentina are the largest markets, where urbanization and the development of commercial real estate are primary growth drivers. Mandates for smoke detectors are increasingly being incorporated into building codes, particularly for commercial and high-income residential projects. However, market penetration in the broader residential sector remains relatively low due to economic volatility and a less mature regulatory environment compared to North America or Europe. The market is price-conscious, with a focus on basic, reliable ionization and photoelectric models. Growth is expected to be steady as economies stabilize and fire safety becomes a higher priority for governments and consumers alike.

Middle East & Africa

This region presents a mixed landscape for smoke detectors. The Gulf Cooperation Council (GCC) countries, such as the UAE and Saudi Arabia, represent the most advanced sub-market, driven by ambitious construction projects, high-quality infrastructure development, and strict fire safety codes for commercial and high-rise residential buildings. In contrast, the broader Middle East and Africa region has lower penetration, with growth primarily concentrated in urban commercial centers. The market is largely driven by new construction rather than replacement cycles. Economic disparities and political instability in parts of Africa hinder widespread adoption. There is a growing recognition of the importance of fire safety, but the market is still nascent, with significant long-term growth potential as regulations evolve and economic conditions improve.

Report Scope

This market research report provides a comprehensive analysis of the Smoke Detectors Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Smoke Detectors Market?

-> Smoke Detectors Market size was valued at USD 2.63 billion in 2024 to USD 3.99 billion by 2032, exhibiting a CAGR of 6.9% during the forecast period.

Which key companies operate in Smoke Detectors Market?

-> Key players include Honeywell, Carrier, Resideo (First Alert, Inc.), Ei Electronics, Google Nest, Johnson Controls, Swiss Securitas Group (Securiton and Hekatron), Bosch, Schneider Electric, Siemens, Hochiki, Nittan Group, and Nohmi Bosai Limited, among others.

What are the key growth drivers?

-> Key growth drivers include increasing government regulations mandating installation, rising focus on fire safety, and technological advancements in detection sensors.

Which region dominates the market?

-> Europe is a key market driven by government policies, with smoke detectors mandatory in countries including Norway, Denmark, Sweden, Finland, Estonia, the United Kingdom, France, Ireland, Austria, Belgium, Germany, and the Netherlands.

What are the emerging trends?

-> Emerging trends include multi-sensor alarms integrating heat or carbon monoxide detection, smart home integration, and adherence to strict European safety norms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...