MARKET INSIGHTS

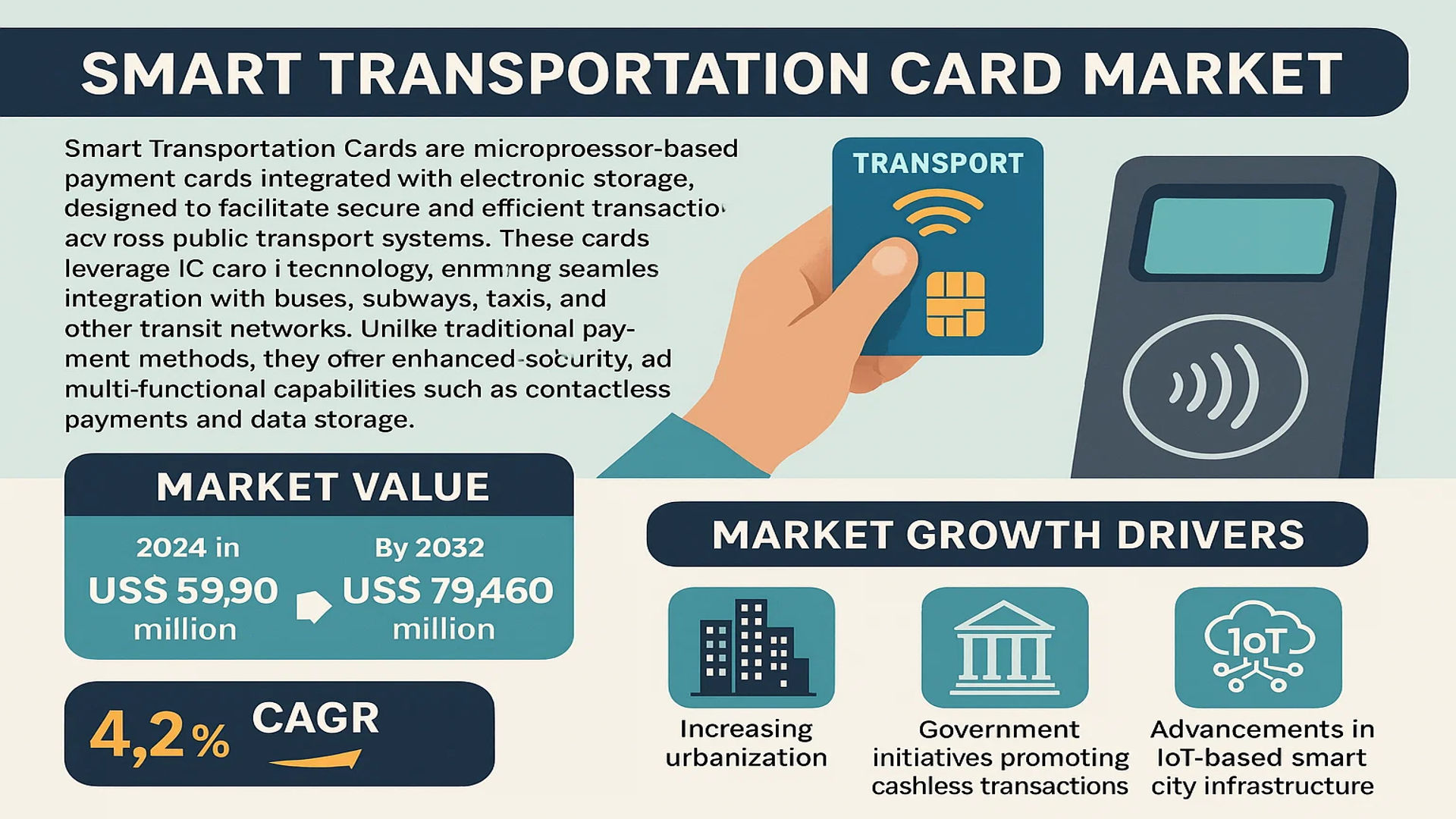

The global Smart Transportation Card Market was valued at 59900 million in 2024 and is projected to reach US$ 79460 million by 2032, at a CAGR of 4.2% during the forecast period.

Smart Transportation Cards are microprocessor-based payment cards integrated with electronic storage, designed to facilitate secure and efficient transactions across public transport systems. These cards leverage IC card technology, enabling seamless integration with buses, subways, taxis, and other transit networks. Unlike traditional payment methods, they offer enhanced security, speed, and multi-functional capabilities such as contactless payments and data storage.

The market growth is driven by increasing urbanization, government initiatives promoting cashless transactions, and advancements in IoT-based smart city infrastructure. For instance, major cities like London (Oyster Card) and Tokyo (Suica Card) have demonstrated the scalability of these systems. Key players such as NXP Semiconductors, Gemalto, and Sony Corporation dominate the market, offering solutions that align with evolving transit demands, including biometric integration and mobile wallet compatibility.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Urbanization and Smart City Initiatives Accelerate Adoption of Smart Transportation Cards

Global urban population growth is driving the need for efficient transportation solutions, with smart cards emerging as a critical infrastructure component. Over 62% of the world’s projected 9.7 billion population will live in urban areas by 2050, creating immense pressure on public transit systems. Smart transportation cards provide seamless multi-modal integration, reducing congestion and improving commuter experience. Leading smart city projects across Asia, Europe, and North America are prioritizing contactless payment systems as part of their digital transformation strategies. Governments are investing heavily in upgrading legacy ticketing systems to accommodate growing passenger volumes, with Asia-Pacific accounting for 48% of total market share in 2024 due to rapid infrastructure development.

Contactless Payment Revolution Fuels Market Expansion

The global shift toward cashless transactions is fundamentally transforming transportation payment systems. Contactless smart card shipments grew by 23% year-over-year in 2023 as consumers increasingly prefer tap-and-go convenience. Transportation authorities report 30-40% faster boarding times with contactless solutions compared to traditional ticketing methods. The pandemic accelerated this transition, with health concerns prompting over 68% of transit operators to prioritize touch-free payment options. Major financial institutions are partnering with transit agencies to enable open-loop payments, allowing commuters to use bank-issued contactless cards directly at fare gates. This convergence of banking and transit payment ecosystems creates new growth avenues for smart card manufacturers.

➤ The integration of Near Field Communication (NFC) technology has reduced card transaction time to under 500 milliseconds, making it 5x faster than magnetic stripe alternatives.

Emerging markets present significant untapped potential, with Latin America and Africa expected to show the highest growth rates as they leapfrog legacy systems to adopt smart card technologies directly.

MARKET RESTRAINTS

High Implementation Costs and Legacy System Integration Challenges

While smart transportation cards offer long-term operational efficiencies, the initial deployment costs remain a significant barrier for many transit authorities. A full system upgrade for mid-sized cities can cost between $50-$100 million, including infrastructure, software, and hardware requirements. The challenge compounds when integrating with existing legacy systems, requiring extensive modifications to fare collection equipment and back-end IT architectures. Over 40% of transit agencies cite budget constraints as their primary obstacle to smart card adoption. Additionally, the average lifespan of transportation card readers is 7-10 years, creating recurring capital expenditure requirements that strain municipal budgets.

Other Restraints

Cybersecurity Vulnerabilities

The increasing connectivity of fare collection systems exposes transportation networks to sophisticated cyber threats. Security breaches in transit payment systems increased by 137% between 2020-2023, with hackers targeting personal commuter data and payment information. This has led to stricter compliance requirements that add complexity and cost to system implementations.

Interoperability Limitations

Lack of standardization across regions creates fragmentation, with different cities adopting incompatible technologies. Approximately 35% of smart card users report inconvenience when traveling between cities with different payment systems. This reduces the overall utility of transportation cards and slows adoption rates.

MARKET OPPORTUNITIES

Mobile Wallet Integration Opens New Revenue Streams

The proliferation of smartphone-based payments creates transformative opportunities for the smart transportation card market. Over 2.8 billion mobile wallet users worldwide are increasingly expecting transit systems to support digital payment options. Forward-thinking cities are developing hybrid solutions that work with both physical cards and mobile apps, expanding customer choice. This convergence allows transit agencies to collect valuable commuter data for optimized route planning and dynamic pricing strategies. Pilot programs testing account-based ticketing have shown 28% higher customer satisfaction scores compared to card-only systems.

The emergence of Mobility-as-a-Service (MaaS) platforms presents another lucrative opportunity. These integrated platforms combine multiple transportation modes under single payment solutions, with smart cards serving as the physical access point. Early adopters report 15-20% increases in public transit ridership after implementing MaaS ecosystems supported by smart card technology.

MARKET CHALLENGES

Data Privacy Concerns and Regulatory Complexity

Smart transportation systems collect vast amounts of user data, raising significant privacy concerns among commuters and regulators alike. Over 60% of consumers express unease about location tracking through their transit cards, creating pushback against data collection initiatives. Compliance with evolving data protection regulations like GDPR requires substantial investment in security infrastructure and legal resources. The average transit agency spends 12-18% of its technology budget on privacy compliance measures, diverting funds from system improvements.

Other Challenges

Consumer Behavior Modification

Transitioning passengers from cash or legacy tickets to smart cards requires extensive education campaigns and incentive programs. Cities typically need 3-5 years to achieve 80% adoption rates, during which they must maintain dual payment systems at increased operational costs.

Technology Obsolescence Risk

The rapid pace of payment technology innovation creates uncertainty about long-term system viability. Many agencies struggle with technology lock-in, having made significant investments in solutions that may become outdated within a decade due to emerging alternatives like biometric payments.

SMART TRANSPORTATION CARD MARKET TRENDS

Adoption of Contactless Payment Technologies Accelerates Market Growth

The global smart transportation card market is witnessing rapid evolution with the increasing adoption of contactless payment technologies, driven by the demand for seamless and efficient urban mobility solutions. Contactless smart cards, which use Near Field Communication (NFC) and Radio-Frequency Identification (RFID), have gained traction due to their speed and convenience in public transportation systems. Cities worldwide are integrating these cards into buses, subways, and even bike-sharing systems to enhance commuter experience. Additionally, the COVID-19 pandemic has accelerated the shift toward touchless transactions, further boosting market demand. By 2032, contactless smart cards are projected to account for over 60% of transit card payments globally, indicating a significant market transformation.

Other Trends

Integration with Digital Wallets and Mobile Applications

The convergence of smart transportation cards with mobile wallets and transit apps is reshaping urban commuting. Many major cities are enabling users to load their travel cards directly onto smartphones or wearable devices, eliminating the need for physical cards. This trend aligns with the rise of smart city initiatives, where governments aim for interoperable payment ecosystems. For instance, transit authorities in Europe and Asia are integrating smart cards with mobile applications that provide real-time updates on fares, schedules, and route planning. This shift not only enhances user convenience but also reduces operational costs for transportation providers.

Expansion of Multi-Modal Transport Networks

The development of multi-modal transport systems is a key driver for the smart transportation card market. Cities are increasingly investing in unified payment solutions that allow commuters to use a single card or digital pass across different transit modes, including buses, subways, trams, and ferries. This strategy promotes seamless connectivity and reduces reliance on private vehicles, contributing to sustainability goals. In North America and Europe, governments are collaborating with private vendors to create interoperable systems, while Asia-Pacific leads in adoption due to its extensive urban rail networks. By 2030, over 40% of transit systems are expected to offer multi-modal smart card solutions, reflecting a growing emphasis on integrated urban mobility.

Rising Security and Data Privacy Concerns

While the smart transportation card market thrives, concerns around data security and fraud prevention remain critical challenges. Cyber threats targeting transit payment systems have prompted governments and manufacturers to invest in advanced encryption technologies and biometric authentication. Recent innovations include tokenization and blockchain-based verification to safeguard user transactions. However, balancing security with ease of use remains a hurdle, particularly in regions with high cybercrime rates. Market players are increasingly focusing on developing robust anti-fraud mechanisms to maintain consumer trust while ensuring regulatory compliance in data protection.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Expand Their Footprint in the Evolving Smart Transportation Card Market

The global smart transportation card market remains highly competitive, with both established multinational corporations and regional specialists vying for market share. NXP Semiconductors and Gemalto (now part of Thales Group) currently dominate the market, collectively holding over 30% revenue share as of 2024. Their leadership stems from comprehensive product portfolios covering contactless IC chips, security solutions, and complete system integration capabilities.

Asian players are making significant strides in the market, with Shanghai Fudan Microelectronics and Watchdata capturing growing shares in their domestic markets and expanding internationally. These companies benefit from government support for smart city initiatives and competitive pricing strategies that appeal to cost-sensitive transportation authorities.

The competitive dynamic is intensifying as companies pursue partnerships with transit operators and payment networks. This ecosystem approach has become critical because smart cards increasingly serve as multi-application platforms beyond basic fare collection. Recent collaborations between Sony Corporation’s FeliCa technology and Southeast Asian transit systems exemplify this trend.

Meanwhile, Oberthur Technologies and G+D are differentiating through enhanced security features as cyber threats become more sophisticated. Both companies have launched next-generation cards with biometric authentication capabilities, addressing growing concerns about fraud in contactless transactions.

Looking ahead, the competitive landscape will likely witness further consolidation as major players acquire specialized firms to bolster their IoT and mobile payment capabilities. Mid-sized providers such as CardLogix and Bartronics could become acquisition targets given their niche expertise in custom card solutions.

List of Key Smart Transportation Card Companies Profiled

- NXP Semiconductors (Netherlands)

- Gemalto (Thales Group) (France)

- NEC Corporation (Japan)

- Samsung Electronics Co. Ltd. (South Korea)

- Sony Corporation (Japan)

- LG CNS (South Korea)

- Oberthur Technologies (France)

- Infineon Technologies (Germany)

- CardLogix (U.S.)

- Giesecke+Devrient (G+D) (Germany)

- Bartronics (India)

- Shanghai Fudan Microelectronics Group Co., Ltd. (China)

- Watchdata (China)

Segment Analysis:

By Type

Contactless Smart Transportation Cards Lead the Market Due to Faster Transactions and Enhanced User Convenience

The market is segmented based on technology type into:

- Contact Smart Cards

- Require physical insertion into a reader for data transfer

- Contactless Smart Cards

- Use RFID/NFC technology for tap-and-go functionality

- Hybrid Cards

- Combine both contact and contactless technologies

By Application

Public Transit Systems Represent the Largest Application Segment for Smart Transportation Cards

The market is segmented based on application into:

- Bus Transit Systems

- Subway/Metro Systems

- Taxi Services

- Parking Payment Systems

- Multi-Modal Transportation Hubs

By Technology

RFID-based Solutions Dominate the Market with Widespread Adoption in Urban Transit Systems

The market is segmented based on underlying technology into:

- RFID-based Cards

- NFC-enabled Cards

- Proximity Cards

- Smart Chip Cards

By End User

Urban Commuters Represent the Primary User Base for Smart Transportation Cards

The market is segmented based on end users into:

- Daily Commuters

- Tourists & Visitors

- Corporate Employees

- Government Employees

Regional Analysis: Smart Transportation Card Market

Asia-Pacific

The Asia-Pacific region dominates the global smart transportation card market, accounting for over 45% of market share as of 2024. China leads this growth with its extensive adoption of contactless smart cards across metro systems in cities like Beijing and Shanghai. India shows promising expansion through initiatives like the National Common Mobility Card (NCMC), which aims to unify payment systems across transit networks. Japan and South Korea remain technologically advanced markets with high penetration of contactless solutions. The region’s growth is propelled by rapid urbanization, government digitization policies, and the need for efficient transit management in densely populated cities.

North America

North America’s smart transportation card market is characterized by progressive technology adoption and public-private partnerships. The U.S. leads with major metropolitan areas implementing open-loop payment systems (like OMNY in New York) that integrate contactless bank cards. Canada’s Presto system serves as a benchmark for regional interoperability, while Mexico is gradually upgrading its transit payment infrastructure. The region benefits from strong technology providers and consumer preference for seamless multimodal transit experiences. However, the transition from legacy magnetic stripe cards to contactless RFID solutions faces challenges due to infrastructure upgrade costs.

Europe

Europe’s mature smart transportation card market is driven by EU-wide interoperability initiatives and strong regulatory support for cashless transit. The United Kingdom’s Oyster card system and Germany’s multi-purpose BahnCard set regional standards. Nordic countries lead in digital fare collection innovation, with mobile app integrations supplementing physical cards. The EU’s push for sustainable urban mobility creates opportunities for multimodal smart cards that combine transit with micro-mobility services. However, market saturation in Western Europe contrasts with growing demand in Eastern European cities where transport modernization is ongoing.

South America

The South American market shows uneven adoption, with Brazil’s Bilhete Único in São Paulo and Argentina’s SUBE card demonstrating successful implementations. These contactless card systems serve as models for other cities in the region. Challenges include economic instability affecting infrastructure investments, and the need to balance affordability with technological upgrades. The market holds potential as governments prioritize urban mobility solutions, but growth remains dependent on stable funding and coordinated regional standards.

Middle East & Africa

This emerging market is seeing targeted growth in Gulf Cooperation Council (GCC) countries where smart city initiatives drive adoption. Dubai’s Nol card leads with features integrating metro, buses, and toll payments. South Africa’s Gautrain system demonstrates successful smart card implementation in sub-Saharan Africa. While the overall region lags in adoption due to funding constraints and infrastructure limitations, increasing urbanization and preparations for major events (like Saudi Arabia’s 2030 vision projects) are accelerating investment in digital transit solutions.

Report Scope

This market research report provides a comprehensive analysis of the Global Smart Transportation Card Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Smart Transportation Card market was valued at USD 59,900 million in 2024 and is projected to reach USD 79,460 million by 2032, growing at a CAGR of 4.2%.

- Segmentation Analysis: Detailed breakdown by product type (contact vs. contactless), application (bus, subway, taxi, others), and end-user industry to identify high-growth segments and investment opportunities. In 2024, contactless cards accounted for 72% of the market share.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia-Pacific dominates with 48% market share, driven by China and Japan’s advanced transportation systems.

- Competitive Landscape: Profiles of leading market participants including NEC, Samsung Electronics, Sony, NXP Semiconductors, and Gemalto, covering their product offerings, R&D focus, and recent M&A activities.

- Technology Trends & Innovation: Assessment of emerging technologies including NFC integration, biometric authentication, and multi-application smart cards for seamless urban mobility.

- Market Drivers & Restraints: Evaluation of factors such as urbanization, smart city initiatives, and government mandates versus challenges like cybersecurity risks and high implementation costs.

- Stakeholder Analysis: Strategic insights for card manufacturers, transit operators, payment processors, and government agencies regarding ecosystem development and partnership opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from transportation authorities, and analysis of 120+ smart card implementations worldwide to ensure data accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Smart Transportation Card Market?

-> Smart Transportation Card Market was valued at 59900 million in 2024 and is projected to reach US$ 79460 million by 2032, at a CAGR of 4.2% during the forecast period.

Which key companies operate in this market?

-> Major players include NEC, Samsung Electronics, Sony Corporation, NXP Semiconductors, Gemalto, Infineon Technologies, and Shanghai Fudan Microelectronics.

What are the key growth drivers?

-> Key drivers include urbanization (68% global population in cities by 2050), government smart city initiatives, and demand for cashless transit systems.

Which region dominates the market?

-> Asia-Pacific leads with 48% market share, followed by Europe (28%) and North America (18%). China alone accounts for 32% of global usage.

What are the emerging trends?

-> Emerging trends include mobile wallet integration (growing at 22% CAGR), biometric payment cards, and multi-modal transportation platforms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...