Smart Grid Power Semiconductor Market Insights

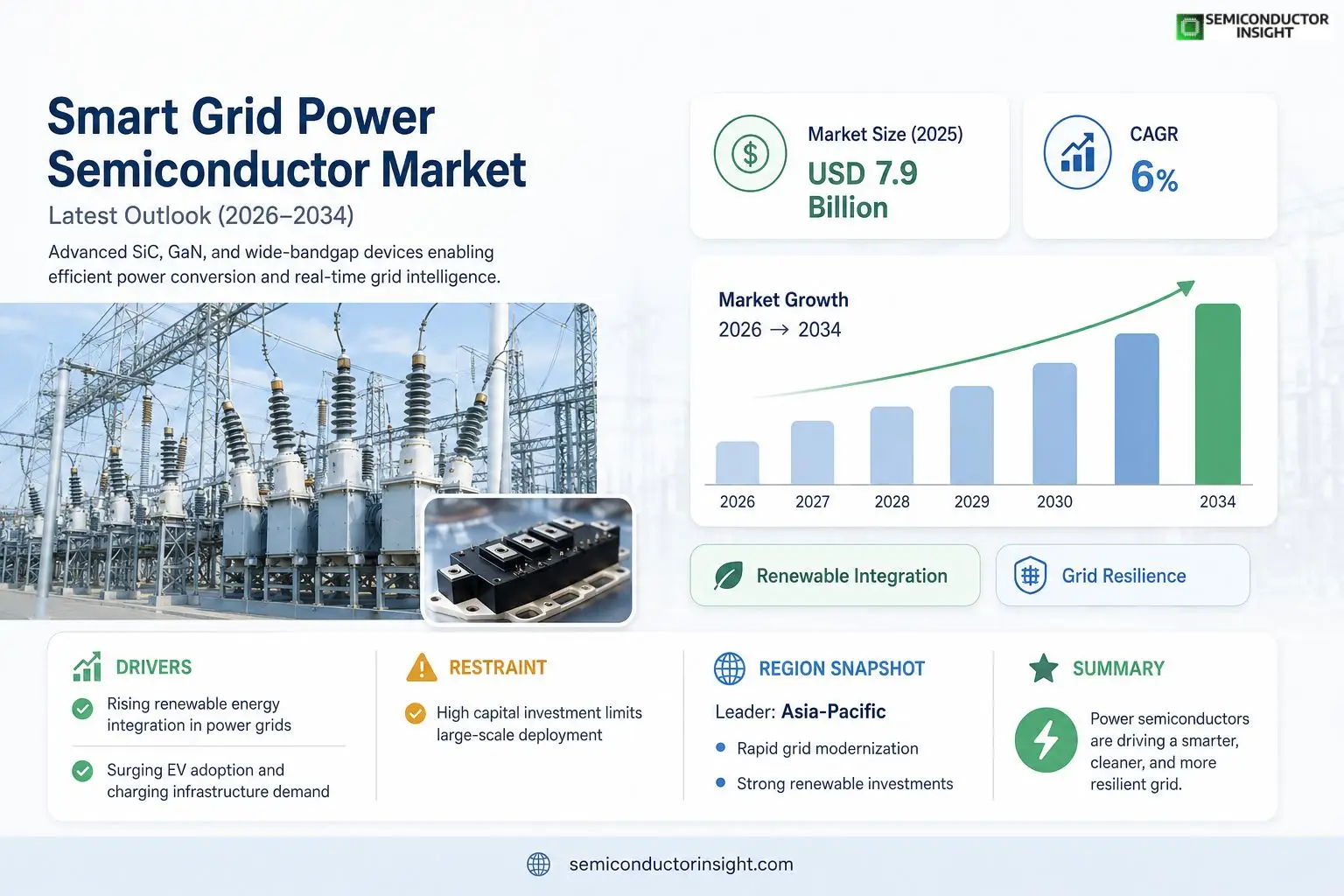

Global Smart Grid Power Semiconductor market size was valued at USD 7.9 billion in 2025. The market is projected to grow from USD 8 billion in 2026 to USD 14 billion by 2034, exhibiting a CAGR of 6% during the forecast period.

Smart Grid Power Semiconductors are advanced silicon‑carbide (SiC), gallium‑nitride (GaN) and wide‑bandgap devices that enable high‑efficiency voltage conversion, fault detection, and real‑time load balancing within modern electric grids.The market is experiencing rapid expansion because renewable energy penetration is accelerating, while utilities seek greater grid resilience under tighter regulatory mandates; furthermore, substantial R&D investments are driving next‑generation inverter technologies forward. Leading companies such as ABB Ltd., Siemens AG, Infineon Technologies AG, Texas Instruments Inc., and Mitsubishi Electric Corp are launching innovative solutions and forging strategic alliances.

MARKET DRIVERS

Increasing Renewable Energy Integration

Smart Grid Power Semiconductor Market is propelled by utilities seeking higher efficiency to accommodate the rapid rise in solar and wind capacity. Advanced silicon‑carbide (SiC) and gallium‑nitride (GaN) devices reduce conduction losses by up to 30%, enabling grid operators to balance variable generation while maintaining voltage stability.

Growth of Electric Vehicle Adoption

EV penetration is expected to exceed 15 million units globally by 2026, driving demand for high‑performance converters in charging infrastructure. Smart Grid Power Semiconductor Market benefits as manufacturers develop modular multilevel converters that support fast‑charging and bidirectional power flow, enhancing grid‑level load management.

➤ Analysts estimate that power semiconductor sales linked to smart grids will grow at a compound annual growth rate of 9% through 2032, outpacing overall semiconductor growth.

Combined, these trends create a robust revenue outlook, with projected market size approaching $7 billion by 2030, underscoring the strategic importance of semiconductor innovations in modern grid architectures.

MARKET CHALLENGES

Regulatory Complexity

Regional standards for grid interconnection and emissions vary widely, requiring manufacturers to certify each device for multiple jurisdictions. This fragmented compliance landscape adds testing costs and extends time‑to‑market for new semiconductor solutions.

Other Challenges

Supply Chain Constraints

Limited availability of high‑purity silicon and rare‑earth materials hampers production scaling. Recent geopolitical tensions have heightened lead times for critical wafers, pressuring manufacturers to diversify sourcing while preserving quality assurance.

MARKET RESTRAINTS

High Capital Expenditure

Deploying next‑generation smart grid infrastructure requires substantial upfront investment in both hardware and software platforms. Utilities often face budgetary constraints, which can delay large‑scale rollout of advanced power semiconductor devices despite clear long‑term efficiency gains.

MARKET OPPORTUNITIES

Emerging Wide‑Bandgap Technologies

The commercialization of SiC and GaN technologies opens new avenues for higher voltage operation and reduced cooling requirements. As efficiency targets tighten across renewable‑rich grids, these wide‑bandgap semiconductors are poised to capture a growing share of Smart Grid Power Semiconductor Market, especially in high‑density urban substations.

Smart Grid Power Semiconductor Market Trends

Accelerating Renewable Integration

Smart Grid Power Semiconductor Market is being reshaped by the rapid growth of renewable generation, which now supplies a large portion of electricity in many regions. Utilities are replacing conventional silicon converters with wide‑bandgap SiC and GaN devices that deliver higher efficiency, lower thermal losses, and faster switching speeds. These semiconductors enable inverter farms to handle variable output from solar and wind assets while maintaining voltage stability and reducing overall system losses by double‑digit percentages. The improved performance also supports tighter grid codes, allowing deeper penetration of clean energy without compromising reliability or increasing ancillary costs.

Other Trends

Strategic Alliances and R&D Investment

Major industry players such as ABB Ltd., Siemens AG, Infineon Technologies AG, Texas Instruments Inc., and Mitsubishi Electric Corp have formed joint ventures and technology‑sharing agreements aimed at accelerating product development cycles. Collective R&D budgets now exceed $1 billion annually, focusing on next‑generation inverter architectures, integrated gate drivers, and advanced packaging techniques that enhance thermal management. These collaborations shorten time‑to‑market for high‑power density modules, allowing utilities to adopt more compact and resilient solutions across transmission and distribution networks, a trend that is clearly evident in recent product launch announcements.

Regulatory‑Driven Grid Resilience

Regulators worldwide are tightening reliability and resiliency standards, compelling utility operators to modernize aging infrastructure. Within Smart Grid Power Semiconductor Market, this regulatory pressure translates into accelerated deployment of intelligent semiconductor converters that provide real‑time fault detection, automated load shedding, and rapid isolation of disturbed sections. The resulting improvements cut outage durations by roughly one‑third and enhance the grid’s ability to recover from extreme weather events. As utilities prioritize these capabilities, demand for robust, high‑performance semiconductor solutions continues to rise, reinforcing the market’s growth momentum.

COMPETITIVE LANDSCAPEKey Industry Players

Smart Grid Power Semiconductor Market – Competitive Overview

Smart Grid Power Semiconductor Market is dominated by a handful of multinational OEMs and semiconductor specialists that have leveraged extensive R&D investments in silicon‑carbide (SiC) and gallium‑nitride (GaN) technologies. ABB Ltd., Siemens AG, Infineon Technologies AG, Texas Instruments Inc., and Mitsubishi Electric Corp collectively account for the bulk of revenue, each offering integrated converter modules, high‑voltage SiC MOSFETs, and GaN power ICs tailored for grid‑level voltage conversion and fault detection. Their product portfolios are supported by strategic alliances with utilities and renewable‑energy firms, enabling rapid deployment of wide‑bandgap devices that improve grid efficiency and resilience. Market structure reflects a tiered approach where these leaders supply both standardized components and customized solutions, positioning them as the primary drivers of adoption across North America, Europe, and Asia‑Pacific.Beyond the core tier, a diverse set of niche players contributes significant innovation in specialized segments such as sensor‑driven load balancing, low‑loss power modules, and embedded protection circuits. Companies like ON Semiconductor, NXP Semiconductors, Rohm Semiconductor, STMicroelectronics, Renesas Electronics Corp., TDK EPCOS AG, and Hitachi Energy focus on application‑specific designs that address emerging needs in distributed generation, electric‑vehicle charging infrastructure, and micro‑grid management. Their emphasis on cost‑effective wide‑bandgap solutions and strategic partnerships with regional utilities has expanded market reach, especially in fast‑growing renewable‑energy markets of Latin America and the Middle East. This layered competitive landscape enhances overall market dynamism while fostering continuous technology advancement.

List of Key Smart Grid Power Semiconductor Companies Profiled

- ABB Ltd.

- Siemens AG

- Infineon Technologies AG

- Texas Instruments Inc.

- Mitsubishi Electric Corp.

- ON Semiconductor

- NXP Semiconductors

- Rohm Semiconductor

- STMicroelectronics

- Renesas Electronics Corp.

- TDK EPCOS AG

- Hitachi Energy

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Silicon‑Carbide (SiC) devices are emerging as the primary driver because they enable higher efficiency in conversion and robust operation under challenging grid conditions.

|

| By Application |

|

Renewable Energy Integration is the leading application segment as utilities seek to accommodate variable generation sources while maintaining grid stability.

|

| By End User |

|

Utility Companies dominate the end‑user landscape, driven by the need to modernize legacy infrastructure and comply with evolving regulatory frameworks.

|

| By Voltage Level |

|

High Voltage segment is gaining prominence as grid operators expand transmission capacities to accommodate distributed generation.

|

| By Grid Function |

|

Load Balancing is a critical function where power semiconductors offer real‑time responsiveness to fluctuating demand.

|

Regional Analysis: North America

United States

The utilities sector in the US is a primary driver of Smart Grid Power Semiconductor Market. Their ongoing efforts to upgrade grid infrastructure and incorporate renewable energy sources are fueling demand for power modules, inverters, and other power electronics components. The need for enhanced grid stability and fault ride-through capabilities is creating opportunities for advanced semiconductor technologies.

Industrial automation is another significant market segment in the US. The adoption of smart grid technologies in industrial facilities is driving demand for power semiconductors used in motor drives, power supplies, and energy management systems. The increasing adoption of industrial IoT (IIoT) further amplifies this demand.

The burgeoning electric vehicle (EV) market in the US is creating considerable demand for power semiconductors used in EV chargers and onboard chargers. The need for fast and efficient charging solutions is driving innovation in power electronics, particularly in silicon carbide (SiC) and gallium nitride (GaN) technologies.

The integration of renewable energy sources like solar and wind power into the grid requires advanced power semiconductors for efficient power conversion and grid synchronization. This segment presents significant growth opportunities for companies offering high-efficiency inverters and power conversion systems.

Europe

Europe exhibits a strong commitment to sustainable energy and grid modernization, making it a key player in Smart Grid Power Semiconductor Market. Stringent environmental regulations and ambitious renewable energy targets are driving demand for advanced power electronics. The focus on energy efficiency and the integration of smart meters are further contributing to market growth. The region is witnessing increasing adoption of SiC and GaN technologies for enhanced power density and efficiency. Smart Grid Power Semiconductor Market trends in Europe are heavily influenced by government initiatives promoting energy transition and the development of smart cities.

Asia-Pacific

Asia-Pacific is expected to be the fastest-growing market for Smart Grid Power Semiconductors. Rapid industrialization, increasing urbanization, and growing investments in grid infrastructure are driving demand across the region. China, in particular, is a major market with significant investments in smart grid projects. The proliferation of electric vehicles and the expansion of renewable energy capacity are further fueling market growth in this region. Smart Grid Power Semiconductor Market growth in Asia-Pacific is characterized by a focus on cost-effective solutions and the adoption of local manufacturing capabilities.

South America

South America presents a promising market for Smart Grid Power Semiconductors, with increasing investments in power infrastructure and renewable energy projects. Several countries in the region are focusing on grid modernization to improve reliability and efficiency. The growth of the electric vehicle market and the increasing adoption of distributed generation systems are also contributing to market expansion. Smart Grid Power Semiconductor Market opportunities in South America are linked to infrastructure development and the need for enhanced power management solutions.

Middle East & Africa

The Middle East & Africa region is witnessing growing investments in smart grid technologies and renewable energy projects. Several countries are implementing smart grid initiatives to improve grid stability and reduce energy losses. The expansion of the electric vehicle market and the increasing adoption of solar power are also contributing to market growth. Smart Grid Power Semiconductor Market in this region is driven by infrastructure development and the need for energy efficiency solutions.

Report Scope

This market research report provides a comprehensive analysis of the Smart Grid Power Semiconductor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Smart Grid Power Semiconductor Market?

-> Smart Grid Power Semiconductor Market was valued at USD 7.9 billion in 2025 and is expected to reach USD 14 billion by 2034, representing a CAGR of 6% over the forecast period.

Which key companies operate in Smart Grid Power Semiconductor Market?

-> Key players include ABB Ltd., Siemens AG, Infineon Technologies AG, Texas Instruments Inc., and Mitsubishi Electric Corp.

What are the key growth drivers?

-> Growth is driven by accelerating renewable‑energy penetration, heightened demand for grid resilience, stricter regulatory mandates, and substantial R&D investments in next‑generation inverter technologies.

Which region dominates the market?

-> The reference does not specify a dominant region; therefore no single region can be identified as the market leader.

What are the emerging trends?

-> Emerging trends include the adoption of advanced silicon‑carbide (SiC) and gallium‑nitride (GaN) wide‑bandgap devices, and the development of high‑efficiency inverter solutions for modern electric grids.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...