Smart Grid Embedded Market Insights

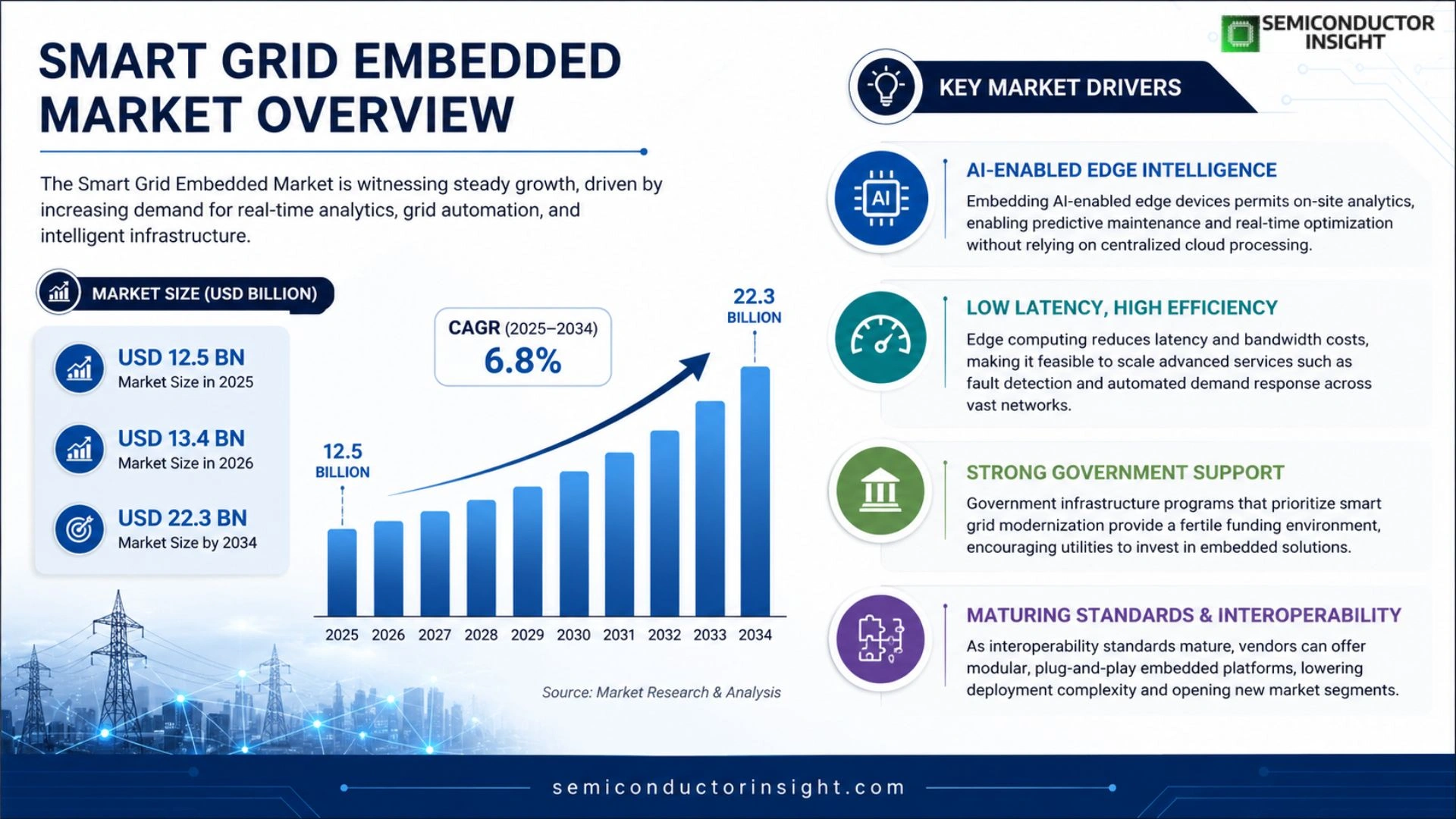

Global Smart Grid Embedded Market size was valued at USD 12.5 billion in 2025. The market is projected to grow from USD 13.4 billion in 2026 to USD 22.3 billion by 2034, exhibiting a CAGR of 6.8% during the forecast period.

Smart grid embedded systems are integrated hardware and software platforms that embed advanced sensors, communication modules, and analytics into electrical distribution infrastructure. They enable real‑time monitoring, automated fault detection, demand response, and optimal energy flow across generation‑to‑load networks.

The market is experiencing rapid expansion because utilities are accelerating renewable integration and governments are mandating grid modernization. Furthermore, the proliferation of IoT devices and big‑data analytics fuels adoption. Key players such as Siemens AG, Schneider Electric, ABB Ltd., General Electric and Hitachi Energy are investing heavily in R&D and strategic partnerships to broaden their portfolios.

MARKET DRIVERS

Enhanced Energy Efficiency and Demand Response

The integration of embedded controllers within distribution networks enables real‑time load balancing, reducing peak demand and minimizing transmission losses. Smart Grid Embedded Market solutions automate demand‑response programs, allowing utilities to shift consumption without compromising consumer comfort.

Growth of Renewable Energy Sources

As solar and wind installations surge, embedded platforms provide the necessary voltage regulation and frequency control to maintain grid stability. This capability accelerates renewable adoption and supports national decarbonization targets.

➤ Industry analysts expect Smart Grid Embedded Market to outpace traditional grid upgrades, driven by policy incentives and technology convergence.

Overall, the combination of efficiency gains, renewable integration, and advanced automation creates a robust growth engine for the sector.

MARKET CHALLENGES

Cybersecurity Threats

Embedded devices increase the attack surface of power networks. Protecting communication channels and firmware from intrusion requires continuous investment in security protocols and skilled personnel.

Other Challenges

Regulatory and Standardization Hurdles

Differing regional standards complicate cross‑border deployments, and evolving regulatory frameworks can delay project approvals.

MARKET RESTRAINTS

High Initial Capital Expenditure

Deploying embedded intelligence across extensive feeder lines requires substantial upfront investment in hardware, communication infrastructure, and integration services, which can deter smaller utilities.

Furthermore, the cost of retrofitting legacy substations with modern embedded solutions adds to the financial burden, often extending the payback period beyond initial expectations.

Limited access to financing options in emerging markets further restrains the pace of adoption, despite the long‑term operational savings.

MARKET OPPORTUNITIES

Advanced Data Analytics and AI Integration

Embedding AI‑enabled edge devices permits on‑site analytics, enabling predictive maintenance and real‑time optimization without relying on centralized cloud processing.

Edge computing reduces latency and bandwidth costs, making it feasible to scale advanced services such as fault detection and automated demand response across vast networks.

Government infrastructure programs that prioritize smart grid modernization provide a fertile funding environment, encouraging utilities to invest in embedded solutions.

As interoperability standards mature, vendors can offer modular, plug‑and‑play embedded platforms, lowering deployment complexity and opening new market segments.

Smart Grid Embedded Market Trends

Accelerated Renewable Integration Fuels Market Momentum

Smart Grid Embedded Market is experiencing a pronounced shift as utilities prioritize renewable energy sources. Grid operators are retrofitting distribution networks with embedded sensors and communication modules that allow real‑time balancing of variable generation. This capability reduces reliance on conventional peaking plants and supports compliance with emerging government mandates for carbon reduction. As a result, the deployment of embedded platforms is expanding across North America, Europe, and select Asian jurisdictions, creating a broader base for advanced demand‑response programs and automated fault isolation. The trend reflects a strategic alignment between grid resilience objectives and the economic incentives tied to cleaner power portfolios.

Other Trends

IoT and Big‑Data Analytics Enable Proactive Grid Management

Integration of Internet‑of‑Things devices and high‑volume data streams is reshaping how Smart Grid Embedded Market delivers value. Edge‑located sensors continuously capture voltage, current, and environmental parameters, feeding analytics engines that predict load spikes and equipment degradation before they manifest as outages. Utilities are leveraging machine‑learning models to fine‑tune voltage regulation and to orchestrate distributed energy resources in a coordinated manner. The resulting operational efficiency gains translate into lower maintenance costs and higher power quality for end users. Companies that embed scalable data pipelines within their hardware offerings are gaining a competitive edge, as they can offer turnkey solutions that address both monitoring and optimization in a single package.

Strategic R&D Investments by Industry Leaders

Major players such as Siemens, Schneider Electric, ABB, General Electric, and Hitachi Energy are channeling substantial research and development budgets into next‑generation embedded architectures. Their focus areas include hardened cybersecurity modules, plug‑and‑play communication standards, and modular hardware designs that simplify field upgrades. Collaborative partnerships with regional utilities and technology startups are accelerating prototype validation and reducing time‑to‑market. These strategic moves reinforce Smart Grid Embedded Market’s trajectory toward higher automation levels, tighter integration with distributed generation assets, and enhanced interoperability across legacy infrastructure. The cumulative effect is a more resilient, data‑rich grid that can adapt to evolving load patterns and regulatory expectations.

COMPETITIVE LANDSCAPE

Key Industry Players

Smart Grid Embedded Market Overview

Smart Grid Embedded market was valued at USD 12.5 billion in 2025 and is projected to reach USD 22.3 billion by 2034, growing at a CAGR of 6.8 %. Market leadership is concentrated among a handful of multinational engineering firms that combine deep utility expertise with advanced hardware‑software integration capabilities. Siemens AG, Schneider Electric, ABB Ltd., General Electric and Hitachi Energy dominate the top tier, leveraging extensive R&D investments and strategic partnerships to deliver end‑to‑end embedded platforms that incorporate real‑time sensing, communications, and analytics. Their sizable portfolios enable utilities to accelerate renewable integration, meet regulatory mandates for grid modernization, and capitalize on the expanding IoT and big‑data ecosystem. These incumbents benefit from scale, global service networks, and long‑standing relationships with utilities, which reinforce a relatively consolidated market structure despite rapid growth.

Beyond the core incumbents, a diverse set of niche and regional players enriches the competitive landscape by focusing on specialized modules, software analytics, and emerging market segments. Companies such as Eaton Corporation, Itron Inc., Landis+Gyr, S&C Electric, Mitsubishi Electric, Cisco Systems, and Honeywell International bring differentiated capabilities in power management, metering intelligence, industrial communication, and cybersecurity. Start‑up innovators and mid‑size firms are also entering the space, targeting high‑growth opportunities in micro‑grid control, demand‑response optimization, and edge‑computing solutions. This broader ecosystem introduces competitive pressure that drives continuous innovation, price erosion, and collaborative ventures across the smart‑grid value chain.

List of Key Smart Grid Embedded Companies Profiled

- Siemens AG

- Schneider Electric

- ABB Ltd.

- General Electric

- Hitachi Energy

- Eaton Corporation

- Itron Inc.

- Landis+Gyr

- S&C Electric Company

- Mitsubishi Electric

- Cisco Systems

- Honeywell International

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Hardware Integration

|

| By Application |

|

Renewable Energy Integration

|

| By End User |

|

Utility Companies

|

| By Technology |

|

IoT Sensors

|

| By Deployment Model |

|

Hybrid

|

Regional Analysis: North America

The primary drivers include government initiatives promoting renewable energy integration, the need for enhanced grid reliability, and the decreasing cost of embedded intelligence.

Innovations in IoT, AI, and data analytics are fueling the development of more sophisticated and efficient Smart Grid Embedded Market solutions.

The market is characterized by a mix of established players and emerging startups, fostering intense competition and innovation.

The integration of blockchain technology and the growing focus on cybersecurity are expected to be key trends shaping Smart Grid Embedded Market moving forward.

North America

The North American region is witnessing a significant transformation of its energy infrastructure, with a strong emphasis on adopting Smart Grid Embedded Market technologies. The region’s diverse regulatory landscape and varying levels of infrastructure development present both opportunities and challenges for market players. Investment in smart meters, grid automation, and DER management systems is gaining momentum, driven by a desire to improve energy efficiency and enhance grid resilience. Business strategies in North America often involve collaborating with local utilities, tailoring solutions to specific regional needs, and navigating complex regulatory frameworks. The increasing adoption of electric vehicles (EVs) further necessitates the development of smart charging infrastructure, creating new avenues for growth within Smart Grid Embedded Market.

Europe

Europe is at the forefront of the global transition towards a sustainable energy system, with strong government support for smart grid initiatives and Smart Grid Embedded Market. The region’s focus on energy efficiency, renewable energy integration, and decarbonization is driving significant investments in grid modernization. Business strategies in Europe often involve leveraging European Union regulations and funding opportunities, fostering innovation through collaborative research projects, and prioritizing cybersecurity to ensure grid security. The deployment of smart grids and the integration of DERs are key components of Europe’s energy transition, creating substantial opportunities for Smart Grid Embedded Market.

Asia-Pacific

The Asia-Pacific region presents the largest and fastest-growing market for Smart Grid Embedded Market technologies. Rapid economic growth, increasing urbanization, and rising energy demand are driving significant investments in grid infrastructure across the region. Business strategies in Asia-Pacific often involve establishing local partnerships, adapting solutions to diverse regional needs, and competing on cost-effectiveness. The adoption of smart grids, smart meters, and DER management systems is crucial for meeting the growing energy demands of the region while improving grid efficiency and reliability. Smart Grid Embedded Market is poised for substantial growth in Asia-Pacific, driven by government initiatives and private sector investments.

South America

South America is experiencing a growing interest in Smart Grid Embedded Market technologies, driven by the need to modernize aging grid infrastructure and improve energy access. Government initiatives aimed at promoting renewable energy and decentralization are fostering demand for smart grid solutions. Business strategies in South America often involve working with local utilities and governments to address specific energy challenges and tailor solutions to regional needs. The adoption of smart meters and DER management systems is key to enhancing grid reliability and efficiency in the region. Smart Grid Embedded Market has significant potential for growth in South America as the region continues to invest in grid modernization and renewable energy deployment.

Middle East & Africa

The Middle East and Africa region presents a unique opportunity for Smart Grid Embedded Market, driven by increasing energy demand, government initiatives for grid modernization, and the growing adoption of renewable energy sources. The region’s focus on energy efficiency and water conservation is further driving demand for smart grid solutions. Business strategies in the Middle East and Africa often involve partnering with local governments and utilities to address specific energy challenges and tailor solutions to regional needs. The deployment of smart meters, DER management systems, and grid automation technologies is crucial for enhancing grid resilience and efficiency in the region. Smart Grid Embedded Market is expected to witness significant growth in the Middle East and Africa as the region continues to invest in energy infrastructure and embrace smart grid technologies.

Report Scope

This market research report provides a comprehensive analysis of the Smart Grid Embedded Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Smart Grid Embedded Market?

-> Smart Grid Embedded Market size was valued at USD 12.5 billion in 2025. The market is projected to grow from USD 13.4 billion in 2026 to USD 22.3 billion by 2034.

Which key companies operate in Smart Grid Embedded Market?

-> Key players include Siemens AG, Schneider Electric, ABB Ltd., General Electric, and Hitachi Energy, among others.

What are the key growth drivers?

-> Key growth drivers include accelerated renewable integration, governmental grid‑modernization mandates, proliferation of IoT devices, and big‑data analytics.

Which region dominates the market?

-> The market is globally distributed, with strong presence in North America, Europe, and Asia‑Pacific, reflecting worldwide grid modernization efforts.

What are the emerging trends?

-> Emerging trends include advanced sensor integration, AI‑enabled analytics, and seamless communication modules for real‑time grid management.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...