Smart Antenna Semiconductor Market Insights

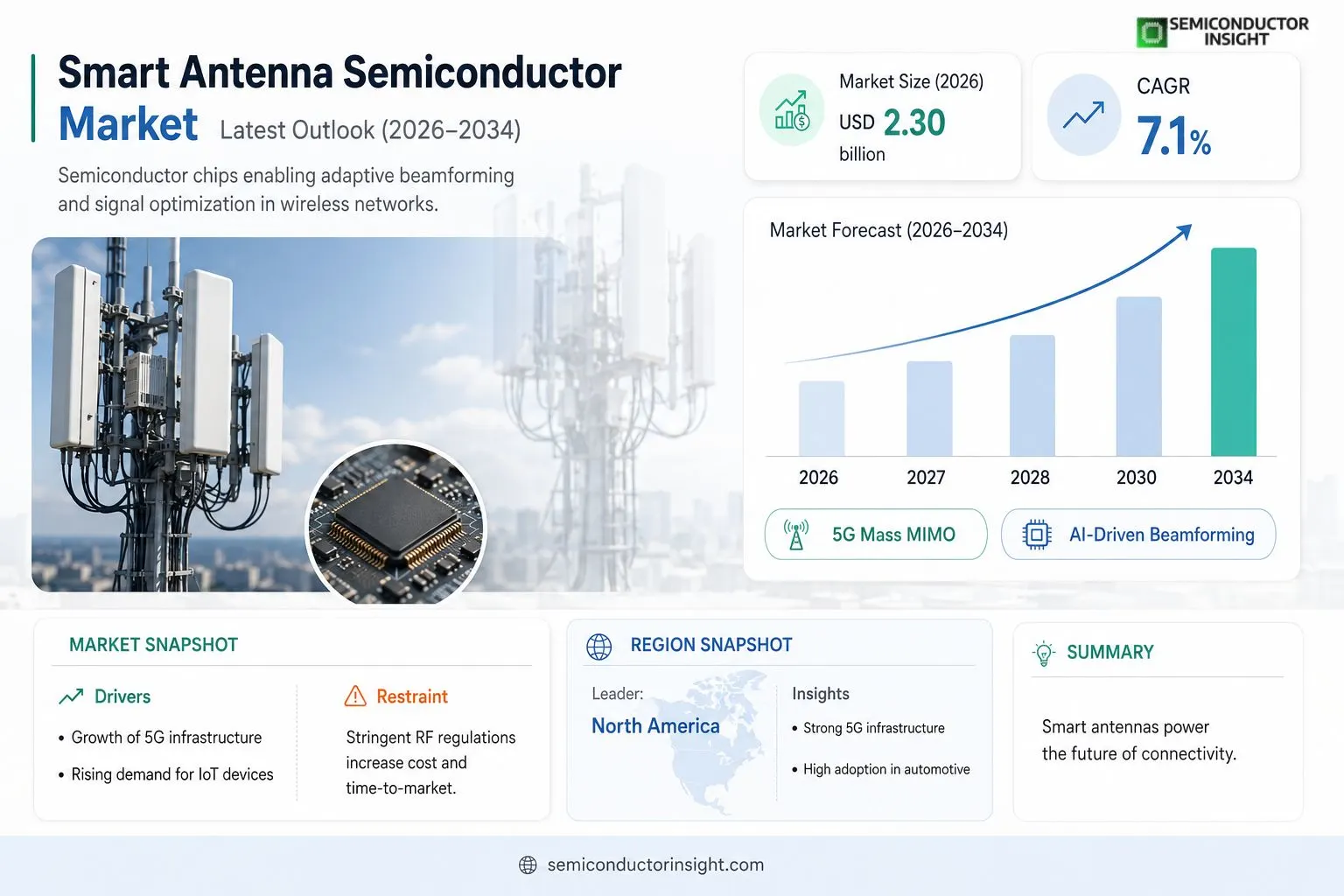

Global smart antenna semiconductor market is projected to grow from USD 2.30 billion in 2026 to USD 3.90 billion by 2034, exhibiting a CAGR of 7.1% during the forecast period.

Smart antenna semiconductors are integrated‑circuit components that enable adaptive beamforming, direction‑finding, and signal‑optimization functions for wireless communication systems such as LTE‑Advanced, Wi‑Fi 6/6E, and emerging 5G/6G networks; they combine RF front‑end modules with digital signal‑processing algorithms to dynamically steer beams toward users while suppressing interference.The market is experiencing rapid growth because telecom operators are expanding network capacity and deploying massive MIMO infrastructure; however, challenges remain around high‑frequency material costs and stringent regulatory standards. Furthermore, rising demand for IoT devices and autonomous vehicles drives adoption of intelligent antenna solutions, while leading players like Qualcomm, NXP Semiconductors, Skyworks Solutions, and Qorvo continue investing in R&D and strategic partnerships.

MARKET DRIVERS

Growth of 5G Infrastructure

The rapid rollout of 5G networks is accelerating demand for high‑performance Smart Antenna Semiconductor Market solutions. Operators require antenna arrays that can dynamically steer beams, which drives semiconductor manufacturers to innovate faster.

Expansion of IoT Devices

By 2027, connected IoT devices are projected to exceed 30 billion units, creating a massive need for compact, low‑power smart antenna chips that support multiple frequency bands.

➤ Smart antenna semiconductor adoption is expected to rise at a CAGR of 12% through 2030, outpacing the broader semiconductor sector.

In addition, automotive telematics and advanced driver‑assistance systems (ADAS) are integrating smart antennas to improve vehicle‑to‑infrastructure communication, further bolstering market growth.

MARKET CHALLENGES

High Development Costs

Designing multi‑band, beam‑forming chips requires substantial R&D investment, and Smart Antenna Semiconductor Market faces pressure to reduce time‑to‑market while maintaining profitability.

Other Challenges

Supply‑Chain Vulnerabilities

Global semiconductor shortages have disrupted component availability, leading to longer lead times for manufacturers and OEMs.

MARKET RESTRAINTS

Regulatory Barriers

Stringent RF emission standards across regions require extensive certification, adding cost and time to product launches within Smart Antenna Semiconductor Market.Moreover, spectrum allocation disputes in densely populated areas can limit the usable frequency bands for smart antenna solutions, constraining market expansion.Finally, intellectual‑property complexities around beam‑forming algorithms pose additional legal hurdles for new entrants.

MARKET OPPORTUNITIES

Edge Computing Integration

Embedding smart antenna chips with edge AI processors enables real‑time beam adaptation, opening lucrative opportunities in data‑center interconnects and private 5G networks.Emerging markets in Africa and South‑East Asia are investing in 5G infrastructure, presenting a fertile ground for Smart Antenna Semiconductor Market players to capture early market share.Additionally, the convergence of satellite‑based internet services and terrestrial networks drives demand for versatile antenna semiconductors capable of seamless handover, creating a new growth frontier.

Smart Antenna Semiconductor Market Trends

Network Capacity Expansion and Massive MIMO Deployment

Telecom operators are aggressively expanding network capacity to meet the exponential growth in mobile data traffic. This expansion drives the deployment of massive MIMO infrastructure, which relies on sophisticated smart antenna semiconductor components to perform adaptive beamforming and interference suppression. The integration of RF front‑end modules with digital signal‑processing algorithms enables dynamic beam steering, improving spectral efficiency across LTE‑Advanced, Wi‑Fi 6/6E, and emerging 5G/6G networks. As operators roll out higher‑frequency bands, the demand for these semiconductors rises, positioning Smart Antenna Semiconductor Market as a critical enabler of next‑generation wireless services.

Other Trends

Cost and Regulatory Landscape

While growth is strong, the market faces pressure from high‑frequency material costs and increasingly stringent regulatory standards. Advanced substrate materials required for millimeter‑wave operation command premium pricing, influencing the bill‑of‑materials for base‑station equipment. Concurrently, regulatory bodies are tightening compliance requirements for emissions and safety, prompting manufacturers to invest in design‑for‑compliance processes. These cost and compliance dynamics compel vendors to pursue economies of scale and collaborative development models to sustain profitability without compromising performance.

Emerging Applications in IoT and Autonomous Vehicles

The proliferation of Internet of Things devices and the advent of autonomous vehicle platforms are opening new demand corridors for smart antenna solutions. In IoT deployments, dense device clusters benefit from the directional gain and reduced interference that intelligent antenna arrays provide, extending battery life and network reliability. Autonomous vehicles, meanwhile, require robust high‑frequency connectivity for real‑time sensor data exchange, a use case that aligns with the beam‑forming capabilities of modern semiconductor designs. Leading players such as Qualcomm, NXP Semiconductors, Skyworks Solutions, and Qorvo are channeling R&D resources toward these segments, forming strategic partnerships to accelerate product readiness and capture emerging market share.

COMPETITIVE LANDSCAPEKey Industry Players

Smart Antenna Semiconductor Market – Competitive Overview

Smart Antenna Semiconductor Market is currently led by a few large integrated‑circuit manufacturers that combine RF front‑end expertise with advanced digital signal‑processing capabilities. Qualcomm, Skyworks Solutions, and Qorvo together command a sizable share of the global revenue, leveraging deep R&D investments and strategic alliances with telecom equipment vendors to supply adaptive‑beamforming solutions for 5G massive MIMO deployments. Their product portfolios span mmWave front‑end modules, tunable power amplifiers, and AI‑enabled beam‑steering chips, enabling operators to meet the aggressive capacity targets required for dense urban networks. The market structure reflects a classic oligopoly where economies of scale, patent portfolios, and access to high‑frequency silicon processes create high entry barriers for new entrants.Beyond the dominant trio, a diverse set of niche and mid‑size players adds depth to the ecosystem. NXP Semiconductors and Infineon Technologies focus on automotive‑grade smart antenna ICs that support vehicle‑to‑infrastructure communication and autonomous‑driving scenarios. Murata Manufacturing and STMicroelectronics specialize in compact, multi‑band modules for IoT devices, while Analog Devices and Broadcom provide high‑performance beam‑forming solutions for enterprise Wi‑Fi 6/6E and private‑network deployments. MediaTek and Intel are expanding their 5G radio‑access portfolio to include integrated smart antenna blocks, and Samsung Electronics contributes foundry services that accelerate silicon‑on‑insulator (SOI) production for next‑generation frequencies. These companies collectively drive innovation across verticals, ensuring a competitive supply chain that can satisfy the projected CAGR of 7.1 % through 2034.

List of Key Smart Antenna Semiconductor Companies Profiled

- Qualcomm

- Skyworks Solutions

- Qorvo

- NXP Semiconductors

- Infineon Technologies

- Murata Manufacturing

- STMicroelectronics

- Analog Devices

- Broadcom Inc.

- MediaTek

- Intel Corporation

- Samsung Electronics

- Renesas Electronics

- Texas Instruments

- Apple (custom RF solutions)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Adaptive Beamforming Antennas are the primary growth driver because they enable precise signal steering that maximizes capacity in dense urban deployments.

|

| By Application |

|

5G Base‑Station Infrastructure commands the leading position as network operators roll out massive MIMO arrays.

|

| By End User |

|

Telecom Operators dominate the end‑user landscape because they dictate network architecture and upgrade cycles.

|

| By Frequency Range |

|

mmWave Solutions are gaining prominence as they unlock unprecedented bandwidth for next‑generation networks.

|

| By Deployment Scenario |

|

Outdoor Macro‑Cell Sites emerge as the leading scenario due to their broad coverage impact.

|

Regional Analysis: North America

United States

The telecommunications industry in North America is undergoing a rapid transformation, with 5G rollout being a primary catalyst for smart antenna adoption. Service providers are investing heavily in upgrading their networks to support higher data rates and lower latency, creating substantial demand for advanced antenna solutions.

The automotive sector is increasingly integrating smart antenna technology for enhanced connectivity and safety features, particularly in the context of autonomous driving and advanced driver-assistance systems. This trend is driving innovation in compact and high-performance antenna designs.

The defense and aerospace industries represent a significant market segment for smart antennas, requiring robust and reliable solutions for secure communication and radar systems. Ongoing technological advancements are focusing on improving stealth capabilities and signal processing efficiency.

The growth of the Industrial Internet of Things (IIoT) is creating new opportunities for smart antennas in applications like asset tracking, remote monitoring, and process automation, demanding reliable connectivity in diverse industrial environments.

Europe

The European Smart Antenna Semiconductor Market is poised for substantial expansion, driven by government initiatives promoting digital infrastructure and increasing adoption of 5G technologies. Several key players in the automotive and industrial sectors are contributing to demand growth. The focus is on energy-efficient antenna designs and integration with advanced wireless communication standards. Regional strategies often emphasize collaboration between industry, academia, and research institutions to foster innovation in smart antenna technologies. Environmental regulations and a strong emphasis on data privacy are also shaping business approaches within the European market. The quest for seamless connectivity across diverse European landscapes presents both opportunities and challenges for market participants.

Asia-Pacific

The Asia-Pacific region, particularly China, Japan, and South Korea, is the largest and fastest-growing market for Smart Antenna Semiconductor Market. This growth is propelled by massive investments in 5G infrastructure, a burgeoning consumer electronics market, and strong manufacturing capabilities. The region is a hotbed for technological innovation, with numerous companies developing cutting-edge antenna solutions. Business strategies here often focus on cost-effectiveness, high-volume production, and catering to the specific needs of local industries. The rapid expansion of the IoT and automotive sectors further fuels demand, making Asia-Pacific a crucial region for global market players.

South America

South America presents a promising, albeit less mature, market for Smart Antenna Semiconductor Market. Increasing investments in telecommunications infrastructure and a growing adoption of mobile technologies are the primary drivers of growth. The automotive sector is also beginning to explore the potential of smart antenna technology. Regional strategies are focused on addressing the infrastructure gaps and developing cost-effective solutions for the local market. Government initiatives aimed at expanding broadband access are expected to further stimulate demand in the coming years.

Middle East & Africa

The Middle East & Africa region is witnessing a gradual but steady growth in Smart Antenna Semiconductor Market. Expanding mobile networks, particularly 4G and the early stages of 5G deployment, are key growth drivers. The automotive industry and government investments in smart city initiatives are also contributing to demand. Business strategies in this region often involve adapting to the specific regulatory environment and focusing on providing solutions suited to the unique challenges of the local infrastructure. The region holds significant long-term potential as connectivity continues to expand.

Report Scope

This market research report provides a comprehensive analysis of the Smart Antenna Semiconductor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Smart Antenna Semiconductor Market?

-> Smart Antenna Semiconductor Market was valued at USD 2.10 billion in 2025 and is expected to reach USD 3.90 billion by 2034.

Which key companies operate in Smart Antenna Semiconductor Market?

-> Key players include Qualcomm, NXP Semiconductors, Skyworks Solutions, and Qorvo, among others.

What are the key growth drivers?

-> Key growth drivers include expansion of telecom network capacity, deployment of massive MIMO, rising demand for IoT devices and autonomous vehicles, and the need for adaptive beamforming in 5G/6G networks.

Which region dominates the market?

-> The provided reference does not specify a dominant region for Smart Antenna Semiconductor Market.

What are the emerging trends?

-> Emerging trends include integration of AI-driven signal processing, development of higher‑frequency antenna modules for 6G, and increasing adoption of smart antenna solutions in autonomous vehicle platforms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...