MARKET INSIGHTS

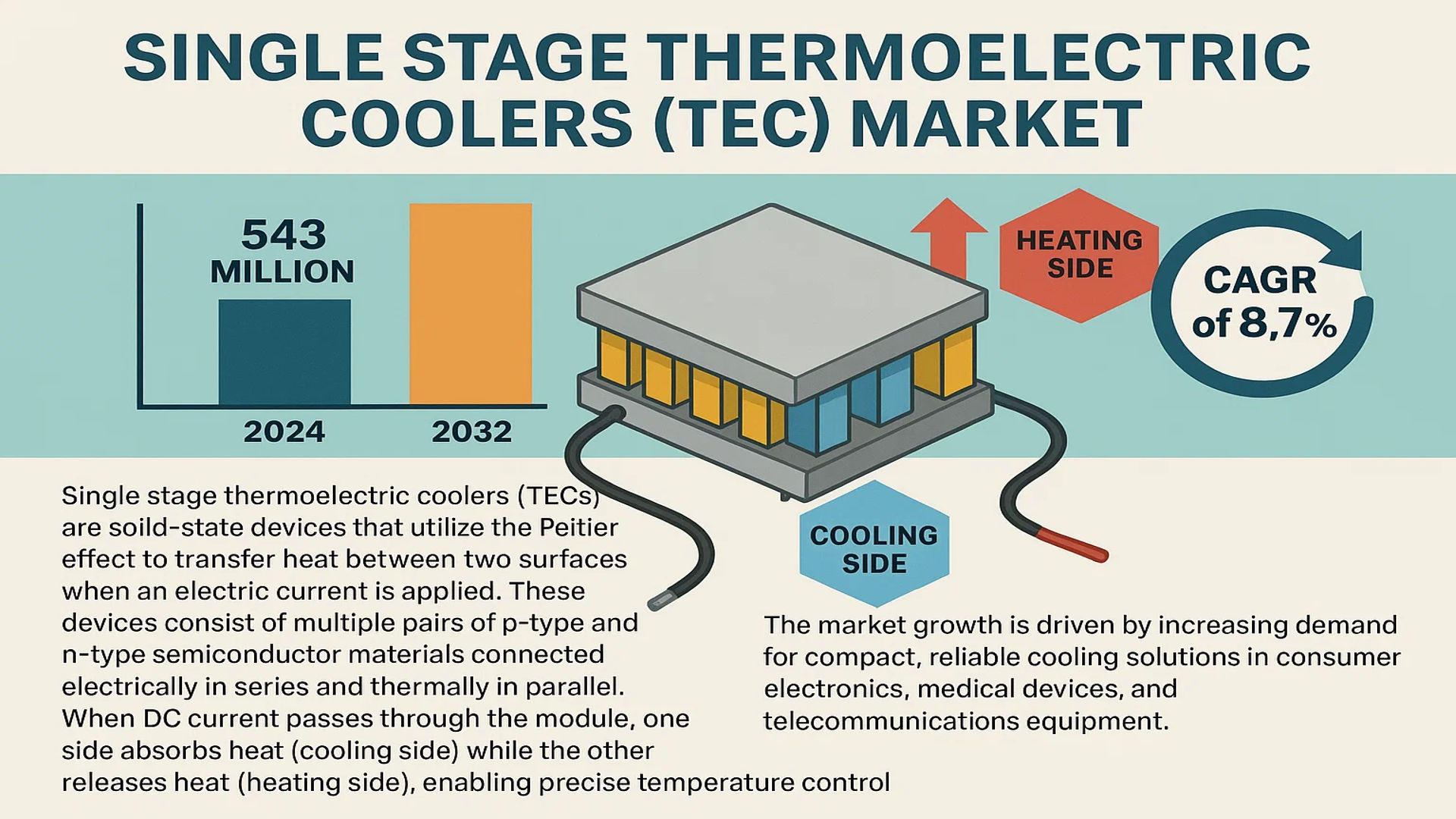

The global Single Stage Thermoelectric Coolers (TEC) market was valued at 543 million in 2024 and is projected to reach US$ 958 million by 2032, at a CAGR of 8.7% during the forecast period.

Single stage thermoelectric coolers (TECs) are solid-state devices that utilize the Peltier effect to transfer heat between two surfaces when an electric current is applied. These devices consist of multiple pairs of p-type and n-type semiconductor materials connected electrically in series and thermally in parallel. When DC current passes through the module, one side absorbs heat (cooling side) while the other releases heat (heating side), enabling precise temperature control without moving parts.

The market growth is driven by increasing demand for compact, reliable cooling solutions in consumer electronics, medical devices, and telecommunications equipment. The Asia-Pacific region dominates the market with over 50% share in 2024, fueled by rapid electronics manufacturing growth in China, Japan, and South Korea. Key players including Ferrotec, Laird Thermal Systems, and Coherent Corp are expanding their product portfolios to capitalize on emerging opportunities in 5G infrastructure and electric vehicles.

MARKET DYNAMICS

MARKET DRIVERS

Growth in Electronics Miniaturization Fuels Adoption of Single-Stage TECs

The relentless trend toward smaller, more powerful electronic devices is accelerating demand for compact thermal management solutions. Single-stage thermoelectric coolers (TECs) are increasingly adopted in smartphones, wearables, and IoT devices where conventional cooling methods prove impractical. With consumer electronics accounting for 25% of the global TEC market in 2024, manufacturers are developing thinner TEC modules with improved heat flux density. For instance, leading suppliers now offer units under 2mm thickness capable of maintaining precise temperature control in constrained spaces, making them indispensable for thermal regulation in 5G chipsets and high-performance processors.

Medical Technology Advancements Create New Applications

The healthcare sector’s shift toward portable diagnostic equipment and wearable medical devices presents significant growth opportunities for single-stage TECs. Their ability to maintain strict temperature ranges (±0.1°C) makes them ideal for PCR devices, DNA analyzers, and portable ultrasound systems. The global medical TEC market segment is projected to grow at 10.2% CAGR through 2030, driven by increasing demand for point-of-care testing in emerging economies. Recent innovations include medical-grade TEC modules with enhanced reliability for continuous operation in life-support equipment, where consistent thermal performance is critical.

Automotive Electrification Expands Thermal Management Needs

Electric vehicle adoption is reshaping thermal management requirements, with single-stage TECs playing a crucial role in battery temperature regulation and cabin climate control systems. Automakers are integrating TEC-based solutions for localized cooling of sensitive LiDAR and vision systems in autonomous vehicles. The automotive TEC segment is expected to grow at 11.5% annually through 2032, as EV production volumes increase globally. Recent developments include ruggedized TEC assemblies that withstand automotive vibration profiles while maintaining energy efficiency in temperature-critical applications.

MARKET RESTRAINTS

Material Costs and Supply Chain Constraints Limit Market Expansion

The single-stage TEC market faces significant pressure from rising raw material costs, particularly for bismuth telluride – the key semiconductor material in thermoelectric modules. Price volatility for rare earth elements increased production costs by 18-22% between 2020-2024, squeezing manufacturer margins. Geopolitical factors have further disrupted supply chains, with lead times for specialized ceramic substrates extending beyond 16 weeks in some cases. These constraints particularly impact small-to-medium manufacturers lacking long-term supplier contracts, potentially slowing market growth in price-sensitive segments.

Energy Efficiency Concerns in High-Power Applications

While single-stage TECs excel in precision cooling applications, their relatively low coefficient of performance (COP) compared to compressor-based systems limits adoption in high-heat-flux scenarios. The average COP for commercial single-stage modules remains below 0.6, meaning they require significant electrical input relative to cooling capacity achieved. This energy inefficiency becomes increasingly problematic as environmental regulations tighten globally, prompting some industries to evaluate alternative cooling technologies for large-scale thermal management needs.

MARKET CHALLENGES

Design Complexity in High-Density Electronics Applications

As electronic components shrink, thermal management becomes increasingly challenging. Single-stage TEC manufacturers must balance conflicting requirements of minimal thickness, high heat-pumping capacity, and reliable long-term performance. The industry reports a 23% increase in design-related failures when TEC modules are implemented in sub-3mm applications, primarily due to thermal stress and delamination issues. Developing robust solutions for next-generation chip packaging remains an ongoing challenge, requiring advanced materials and novel fabrication techniques to maintain reliability in harsh operating environments.

Technical Workforce Shortages Impact Innovation Pace

The specialized nature of thermoelectric system design has created a talent gap, with estimates suggesting a 35% shortage of qualified thermal engineers globally. This shortage slows product development cycles and hampers the implementation of advanced manufacturing techniques needed to improve TEC performance. Companies are increasingly investing in training programs and automated design tools to mitigate this constraint, but the knowledge-intensive nature of thermoelectric applications continues to present recruitment challenges across the value chain.

MARKET OPPORTUNITIES

Emerging IoT Applications Create New Growth Frontiers

The proliferation of edge computing and 5G infrastructure presents substantial opportunities for single-stage TEC deployment. Network equipment providers are increasingly adopting TEC-based cooling for outdoor small cell units and edge servers, where traditional cooling methods prove unreliable. The telecommunications TEC segment is projected to grow at 12.8% CAGR through 2030 as operators deploy denser networks requiring robust thermal management. Recent product developments include weather-resistant TEC assemblies optimized for extreme temperature environments in smart city applications.

Advanced Material Developments Enable Performance Breakthroughs

Ongoing research in thermoelectric materials promises significant efficiency improvements for single-stage TECs. Novel nanocomposite materials have demonstrated ZT values exceeding 1.5 in laboratory settings – nearly double the performance of commercial bismuth telluride alloys. While manufacturing scale-up remains challenging, these advancements could revolutionize the market by enabling TEC modules with 30-40% better energy efficiency. Industry leaders are actively pursuing strategic partnerships with material science innovators to capitalize on these developments and gain competitive advantage in high-value market segments.

SINGLE STAGE THERMOELECTRIC COOLERS (TEC) MARKET TRENDS

Accelerated Miniaturization in Electronics Drives Market Expansion

The global push for smaller, more efficient electronic devices has significantly increased demand for single-stage thermoelectric coolers (TECs). With the consumer electronics industry accounting for 25% of the total TEC market in 2024, manufacturers are prioritizing compact cooling solutions for smartphones, wearables, and IoT devices. Recent advancements in semiconductor materials have improved cooling efficiency by approximately 15-20% compared to earlier generations, enabling TECs to maintain optimal temperatures in increasingly dense electronic configurations. While traditional cooling methods struggle with space constraints, single-stage TECs offer unmatched reliability in compact form factors below 4mm thickness.

Other Trends

Electrification of Automotive Systems

The automotive sector’s transition toward electric vehicles (EVs) has created substantial opportunities for TEC applications. Battery thermal management systems now incorporate single-stage coolers to maintain lithium-ion batteries within their ideal 15-35°C operating range, extending battery life by up to 30%. Furthermore, advanced driver-assistance systems (ADAS) require precise temperature stabilization for LiDAR and image sensors, where TECs provide sub-degree accuracy without vibration interference. As EV production grows at a projected 24% CAGR through 2030, this vertical is becoming a key growth driver for the TEC market.

Medical Technology Breakthroughs Create New Applications

Medical device manufacturers are increasingly adopting single-stage TECs for portable diagnostic equipment and wearable health monitors. The ability to maintain ±0.1°C temperature stability makes them ideal for PCR devices, blood analyzers, and infrared thermography systems. Recent developments include integration with photonics modules for laser diode cooling in surgical instruments, achieving heat flux densities exceeding 5W/cm². With the global medical TEC segment expected to surpass $180 million by 2026, ongoing R&D focuses on enhancing compatibility with biocompatible materials and sterilization processes.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Drive Market Leadership in TEC Space

The global single stage thermoelectric cooler (TEC) market features a mix of established leaders and emerging specialists, with the top five manufacturers holding approximately 55% revenue share in 2024. Market dynamics reflect increasing competition as companies invest heavily in material science breakthroughs and application-specific designs to meet diverse cooling requirements across industries.

Ferrotec Corporation dominates the market with over 20% share, leveraging its vertically integrated semiconductor manufacturing and global distribution network. The company’s recent $35 million expansion of its Jiangsu production facility reinforces its leadership position, particularly in high-power cooling solutions for 5G infrastructure and electric vehicles.

Japanese precision engineering firms KELK Ltd. (Komatsu) and KYOCERA maintain strong positions in industrial and automotive applications, benefiting from decades of experience in thermal management systems. Their focus on ultra-reliable TEC modules for harsh environments has secured long-term contracts with automotive OEMs and industrial equipment manufacturers.

Meanwhile, North American players like Laird Thermal Systems and TE Technology are gaining traction through specialized medical and aerospace cooling solutions. Laird’s collaboration with NASA on Mars rover thermal systems exemplifies the technological sophistication driving this segment, while TE Technology’s patented high-ΔT designs are becoming industry standards for precision instrumentation cooling.

The competitive landscape shows increasing regional specialization, with Chinese manufacturers like Guangdong Fuxin Technology capturing cost-sensitive consumer electronics segments through mass production capabilities, while European firms such as Kryotherm Industries focus on customized solutions for defense and scientific applications where performance outweighs cost considerations.

List of Key Single Stage Thermoelectric Cooler Manufacturers

- Ferrotec Corporation (Japan/USA)

- KELK Ltd. (Komatsu) (Japan)

- Coherent Corp (USA)

- Laird Thermal Systems (USA/UK)

- Z-MAX Co., Ltd. (Japan)

- KYOCERA Corporation (Japan)

- Thermonamic Electronics (China)

- TE Technology, Inc. (USA)

- Kryotherm Industries (Russia)

- Guangdong Fuxin Technology Co., Ltd. (China)

- Phononic (USA)

- Wakefield Thermal Solutions (USA)

Segment Analysis:

By Type

Standard Rectangular TEC Segment Dominates Due to Widespread Integration in Consumer Electronics and Industrial Systems

The market is segmented based on type into:

- Standard rectangular TEC

- Linear TEC

- Round TEC

- Others

By Application

Consumer Electronics Segment Leads Owing to Increasing Demand for Miniature Cooling Solutions

The market is segmented based on application into:

- Consumer electronics

- Subtypes: Smartphones, laptops, gaming consoles

- Communication

- Medical

- Subtypes: Medical imaging, laboratory equipment

- Automotive

- Industrial

- Aerospace & defense

- Others

By Cooling Capacity

Medium Cooling Capacity Segment Holds Significant Share for Optimal Performance in Core Applications

The market is segmented based on cooling capacity into:

- Low capacity (Under 50W)

- Medium capacity (50W-150W)

- High capacity (Above 150W)

By End-User Industry

Electronics Manufacturing Sector Represents Largest Adoption Due to Thermal Management Needs

The market is segmented based on end-user industry into:

- Electronics manufacturing

- Healthcare

- Automotive

- Aerospace & defense

- Others

Regional Analysis: Single Stage Thermoelectric Coolers (TEC) Market

Asia-Pacific

Asia-Pacific dominates the global TEC market with a 50% revenue share in 2024, primarily driven by China’s electronics manufacturing boom and India’s expanding telecom infrastructure. This region consumes over 75 million units annually, with Japan and South Korea leading in high-precision applications for medical devices and automotive components. The rapid adoption of 5G base stations, which require precise thermal management, has accelerated demand for compact TEC solutions. Local manufacturers like Guangdong Fuxin Technology are gaining traction in consumer electronics, though the region still relies on imports for advanced medical and aerospace-grade modules.

North America

The U.S. accounts for 70% of North America’s TEC demand, with strong adoption in defense (e.g., laser cooling systems) and medical equipment like portable MRI machines. Strict FDA guidelines for medical devices and DOE energy efficiency standards push manufacturers toward high-reliability TEC designs. Major players like Laird Thermal Systems and Phononic benefit from R&D investments in solid-state cooling for data centers, though high production costs limit widespread consumer adoption. The region shows growing interest in thermoelectric-waste heat recovery systems for electric vehicles, with pilot projects underway by Tesla and GM.

Europe

Germany and France lead Europe’s €120 million TEC market, where environmental regulations favor lead-free and RoHS-compliant modules. The region excels in niche applications: Italian manufacturers supply TECs for luxury wine chillers, while Swedish firms focus on industrial process cooling. EU-funded projects like HEAT4COOL promote thermoelectric integration in building HVAC systems. However, competition from Asian suppliers has pressured local producers to specialize in custom high-end solutions. A notable trend is the pairing of TECs with IoT sensors for real-time temperature monitoring in pharmaceutical logistics.

South America

Brazil represents 60% of regional TEC consumption, mainly for automotive seat coolers and beverage dispensers. The lack of local semiconductor fabrication forces reliance on imports, with Chinese suppliers capturing 80% of the budget segment. Argentina shows potential in medical refrigeration for vaccine storage, but currency volatility discourages long-term investments. Emerging applications include TEC-based dehumidifiers for tropical climates and cooling systems for cryptocurrency mining rigs. Market growth remains constrained by inadequate R&D infrastructure and fragmented distribution networks.

Middle East & Africa

The GCC countries drive demand for TECs in portable food chillers and military communication gear, with UAE and Israel as key import hubs. Harsh desert climates create opportunities for solar-powered thermoelectric cooling, though adoption lags due to high upfront costs. South Africa’s mining sector utilizes TECs for electronic equipment cooling in underground operations. The region faces challenges including counterfeit low-efficiency modules and limited technical expertise. Long-term growth potential lies in telecom tower cooling as 5G networks expand across Saudi Arabia and Nigeria.

Report Scope

This market research report provides a comprehensive analysis of the Global Single Stage Thermoelectric Coolers (TEC) Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 543 million in 2024 and is projected to reach USD 958 million by 2032 at a CAGR of 8.7%.

- Segmentation Analysis: Detailed breakdown by product type (Standard Rectangular TEC, Linear TEC, Round TEC), application (Consumer Electronics, Communication, Medical, Automotive, Industrial), and end-user industries.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Asia-Pacific dominated with >50% market share in 2024, led by China.

- Competitive Landscape: Profiles of 25+ key players including Ferrotec (20% market share), Laird Thermal Systems, Coherent Corp, and emerging Chinese manufacturers like Guangdong Fuxin Technology.

- Technology Trends: Advancements in semiconductor materials, miniaturization trends, and integration with 5G/IoT applications driving efficiency improvements.

- Market Drivers: Growing demand from electric vehicles, medical devices (25% market share), and telecommunications infrastructure expansion.

- Stakeholder Analysis: Strategic insights for OEMs, thermal solution providers, and investors on emerging opportunities in high-growth segments.

The analysis combines primary interviews with industry leaders and verified secondary data from financial reports, trade associations, and patent filings to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Single Stage TEC Market?

-> Single Stage Thermoelectric Coolers (TEC) market was valued at 543 million in 2024 and is projected to reach US$ 958 million by 2032, at a CAGR of 8.7% during the forecast period.

Which companies lead the Single Stage TEC market?

-> Top 5 players (Ferrotec, KELK Ltd., Coherent Corp, Laird, Z-MAX) hold 55% market share. Ferrotec leads with 20% revenue share.

What drives market growth?

-> Key drivers include 5G infrastructure rollout, EV thermal management demands, and medical device miniaturization.

Which region shows highest growth?

-> Asia-Pacific dominates with >50% share, while North America leads in medical/defense applications.

What are emerging technology trends?

-> Trends include high-efficiency semiconductor materials, integrated cooling solutions for AI chips, and automotive-grade TEC modules.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...