MARKET INSIGHTS

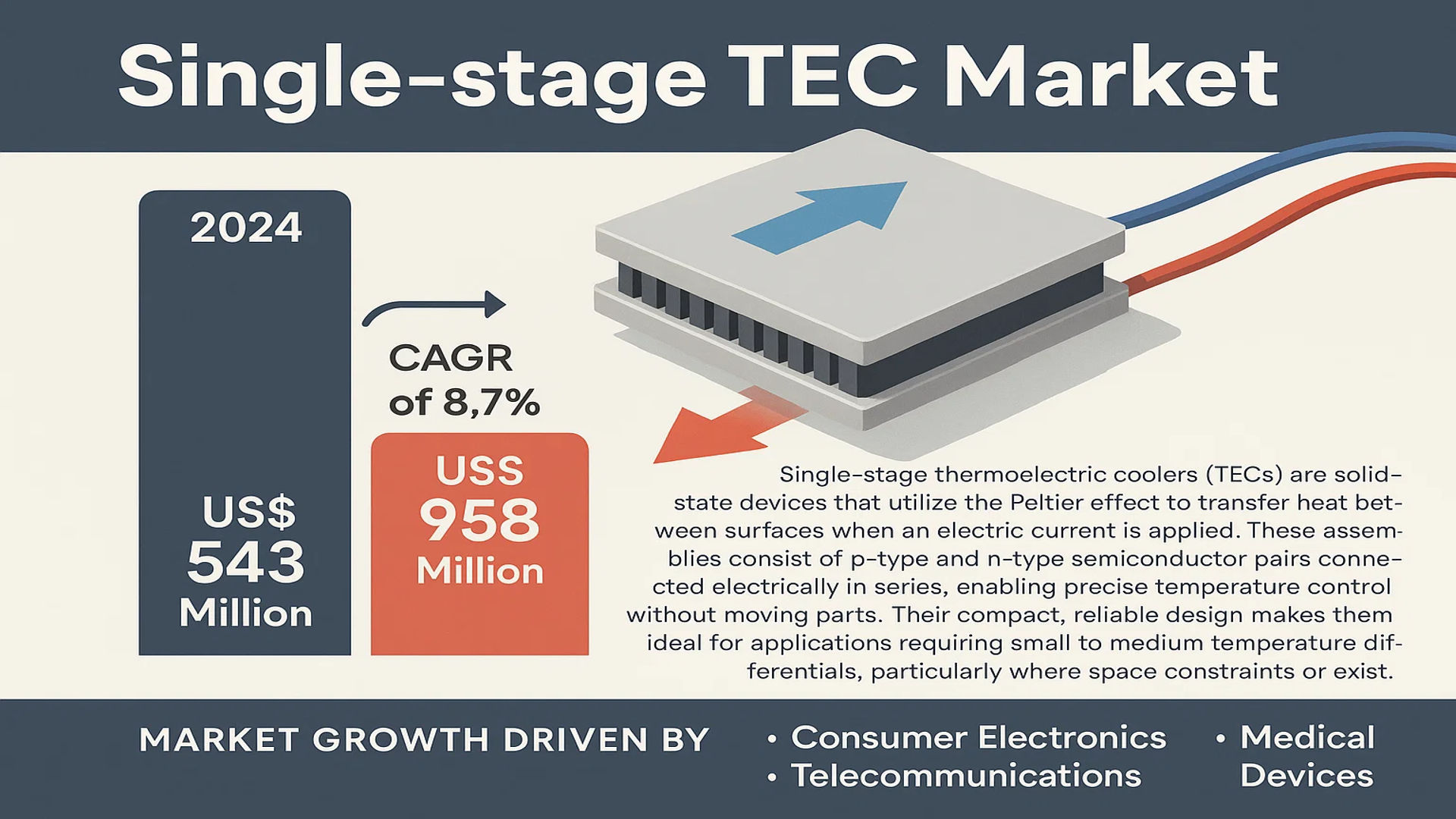

The global Single-stage TEC Market was valued at 543 million in 2024 and is projected to reach US$ 958 million by 2032, at a CAGR of 8.7% during the forecast period.

Single-stage thermoelectric coolers (TECs) are solid-state devices that utilize the Peltier effect to transfer heat between surfaces when an electric current is applied. These assemblies consist of p-type and n-type semiconductor pairs connected electrically in series, enabling precise temperature control without moving parts. Their compact, reliable design makes them ideal for applications requiring small to medium temperature differentials, particularly where space constraints or noise sensitivity exist.

The market growth is driven by increasing demand in consumer electronics, telecommunications, and medical devices, where precise thermal management is critical. The Asia-Pacific region dominates the market, accounting for over 50% of global demand in 2024, primarily due to robust electronics manufacturing in China, Japan, and South Korea. While consumer electronics currently lead applications (25% market share), emerging 5G infrastructure and electric vehicle adoption are accelerating growth in communication and automotive segments.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of Miniaturized Electronics to Accelerate Single-Stage TEC Adoption

The global trend toward miniaturization in electronics is creating robust demand for single-stage thermoelectric coolers. As semiconductor components shrink while computational power increases, thermal management becomes increasingly critical. Single-stage TECs provide precise temperature control in compact form factors ideal for smartphones, wearables, and IoT devices. With over 1.8 billion smartphones shipped annually, each potentially requiring multiple TEC modules for camera sensors and processors, this represents a massive addressable market. The automotive sector is similarly driving demand as electric vehicles incorporate more advanced driver assistance systems (ADAS) requiring thermal stabilization.

Advancements in Medical Device Technologies Fuel Market Expansion

Medical applications are emerging as significant drivers for single-stage TEC adoption, particularly in portable diagnostic equipment and laboratory instrumentation. These coolers enable precise thermal regulation for sensitive diagnostic components such as PCR machines and portable ultrasound systems. The global medical device market is projected to exceed $850 billion by 2030, with cooling solutions constituting an increasingly vital component. Single-stage TECs offer distinct advantages in medical settings due to their vibration-free operation and ability to maintain temperature stability within ±0.1°C, critical for both diagnostic accuracy and sample preservation.

Furthermore, the growing pharmaceutical cold chain logistics sector presents new opportunities. Temperature-sensitive drug transportation requires reliable cooling solutions where single-stage TECs provide advantages over conventional compressor-based systems in certain applications, particularly for last-mile delivery of biologics and vaccines.

MARKET RESTRAINTS

Thermal Efficiency Limitations Constrain High-Power Applications

While single-stage TECs excel in compact applications, their relatively low coefficient of performance (COP) compared to multi-stage systems presents a significant restraint. A typical single-stage TEC achieves COP values between 0.3-0.7, meaning they consume more power than the heat they move. This inefficiency becomes problematic in applications requiring significant heat pumping capacity or operating in high ambient temperatures. The energy penalty restricts adoption in power-hungry systems where alternatives like vapor-compression cooling remain superior.

Additionally, the materials science limitations of current thermoelectric compounds hinder performance improvements. Bismuth telluride remains the dominant material despite decades of research into alternatives with better thermoelectric properties, creating an innovation bottleneck that slows market expansion into new applications.

MARKET CHALLENGES

Supply Chain Vulnerabilities Impacting Rare Material Availability

The single-stage TEC market faces mounting challenges from supply chain reliability, particularly concerning rare earth materials critical for thermoelectric manufacturing. Bismuth and tellurium supply remains concentrated in a few countries, creating vulnerability to geopolitical disruptions. Tellurium availability is particularly constrained as it’s primarily obtained as a byproduct of copper refining, with annual global production limited to approximately 500-600 metric tons.

Additional Challenges

Thermal Cycling Durability

Repeated thermal cycling can degrade TEC performance over time through thermal expansion mismatches and intermetallic diffusion at junctions. Manufacturers are investing in advanced bonding techniques and material formulations to improve product lifetimes beyond the current 50,000-100,000 cycle standard.

Standardization Gaps

The lack of universal performance testing standards across the industry creates inconsistencies in product specifications and performance claims, making it difficult for buyers to compare solutions across vendors.

MARKET OPPORTUNITIES

Emerging 5G Infrastructure Creates New Cooling Demands

The global rollout of 5G networks presents a significant growth opportunity for single-stage TEC manufacturers. 5G base stations and small cells require precise thermal management for sensitive RF components and power amplifiers. With projections of over 7 million 5G base stations to be deployed by 2030, each potentially incorporating multiple TEC modules, this infrastructure buildout could drive substantial market expansion. The unique requirements of outdoor telecom equipment – including reliability across wide temperature ranges and minimal maintenance needs – align well with single-stage TEC capabilities.

Another promising opportunity lies in the developing field of quantum computing. While still emerging, quantum processors operating at cryogenic temperatures may benefit from precision thermoelectric solutions for temperature stabilization and gradient control during the warming stages of operation.

SINGLE-STAGE TEC MARKET TRENDS

Rising Demand for Compact Thermal Management Solutions Drives Market Growth

The global single-stage thermoelectric cooler (TEC) market is experiencing significant growth, fueled by increasing demand for compact, solid-state cooling solutions across multiple industries. Valued at $543 million in 2024, the market is projected to reach $958 million by 2032, expanding at a CAGR of 8.7%. The push toward miniaturization in consumer electronics and the need for precise temperature control in medical and telecom equipment have accelerated adoption. While traditional compressor-based cooling systems struggle with size and noise constraints, single-stage TECs offer silent operation, high reliability, and adaptability to space-constrained environments. Manufacturers are increasingly integrating these modules into 5G base stations, optoelectronic devices, and portable medical instruments.

Other Trends

Electrification of Automotive Systems

Electric vehicle (EV) manufacturers are adopting single-stage TECs for battery thermal management, cabin climate control, and sensor temperature stabilization. With global EV sales surpassing 10 million units annually, the automotive sector has emerged as a high-growth segment. These coolers efficiently regulate lithium-ion battery temperatures, improving performance and lifespan while operating without refrigerants—aligning with stringent environmental regulations. Furthermore, advancements in semiconductor materials have enhanced heat transfer efficiency by up to 15% compared to earlier generations, making them viable for demanding automotive applications.

Asia-Pacific Dominance and Supply Chain Localization

Asia-Pacific commands over 50% of the global market share, driven by concentrated electronics production in China, Japan, and South Korea. Regional suppliers like Guangdong Fuxin Technology are scaling production to meet export and domestic demand, particularly for cooling high-performance computing hardware and optical communication modules. Meanwhile, North American and European manufacturers are focusing on high-reliability applications—such as aerospace and medical imaging—where precision and longevity justify premium pricing. However, geopolitical tensions and semiconductor material shortages have prompted firms to diversify supply chains, with 40% of surveyed companies investing in regional production facilities to mitigate disruptions.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Innovation to Capitalize on Expanding Thermal Management Applications

The global single-stage TEC market features a competitive ecosystem dominated by established players with strong technical expertise, while smaller regional companies are gaining traction in niche segments. Ferrotec Corporation maintains its leadership position with approximately 21% market share in 2024 through its vertically integrated semiconductor manufacturing capabilities and extensive product portfolio. The company’s recent investments in AI-powered thermal solutions for 5G infrastructure have strengthened its position in high-growth segments.

Laird Thermal Systems and KELK Ltd. (Komatsu) collectively account for nearly 18% of the market, leveraging their precision engineering capabilities for medical and industrial applications. Both companies have accelerated R&D efforts to develop energy-efficient TEC modules that comply with growing sustainability requirements across industries.

Meanwhile, Chinese manufacturers like Guangdong Fuxin Technology and Zhejiang Wangu Semiconductor are rapidly expanding their market presence through competitive pricing strategies and government-supported semiconductor initiatives. While currently focused on consumer electronics applications, these companies are making strategic moves into automotive and telecommunications verticals.

List of Key Single-stage TEC Manufacturers

- Ferrotec Corporation (Japan)

- KELK Ltd. (Komatsu) (Japan)

- Laird Thermal Systems (U.S.)

- Coherent Corp (formerly II-VI Incorporated) (U.S.)

- TE Technology, Inc. (U.S.)

- KYOCERA Corporation (Japan)

- Guangdong Fuxin Technology (China)

- Thermonamic Electronics (China)

- Z-MAX (Japan)

- Phononic (U.S.)

- Same Sky (formerly CUI Devices) (U.S.)

- Kryotherm Industries (Russia)

- Zhejiang Wangu Semiconductor (China)

- Pelonis Technologies (U.S.)

- Wakefield Thermal (U.S.)

Segment Analysis:

By Type

Circle Type Segment Leads the Market Due to Widespread Usage in Compact Devices

The market is segmented based on type into:

- Circle Type

- Subtypes: Standard cooling modules, high-power cooling modules

- Rectangle Type

- Subtypes: Standard rectangular modules, custom rectangular arrays

- Others

By Application

Consumer Electronics Segment Dominates Due to Growing Demand for Miniaturized Cooling Solutions

The market is segmented based on application into:

- Consumer Electronics

- Subtypes: Smartphone cooling solutions, wearable devices, gaming consoles

- Communication

- Medical

- Automotive

- Industrial

- Aerospace & Defense

- Others

By Cooling Capacity

Low-Capacity Modules Lead in Portable Electronics Segment

The market is segmented based on cooling capacity into:

- Low Capacity (0-50W)

- Medium Capacity (51-150W)

- High Capacity (151W and above)

By End-User Industry

Electronics Manufacturing Sector Shows Highest Adoption

The market is segmented based on end-user industry into:

- Electronics Manufacturing

- Healthcare

- Automotive

- Telecommunications

- Aerospace & Defense

- Others

Regional Analysis: Single-stage TEC Market

Asia-Pacific

The Asia-Pacific region dominates the global Single-stage TEC market, accounting for over 50% of total demand in 2024. China spearheads this growth due to its thriving electronics manufacturing sector and rapid adoption of 5G infrastructure, requiring precision thermal management solutions. Japan and South Korea contribute significantly through advanced semiconductor applications in consumer electronics and electric vehicles. Cost-effective production capabilities and government initiatives like China’s 14th Five-Year Plan for high-tech manufacturing further accelerate market expansion. However, the region shows bifurcated demand—while China focuses on mass production for consumer applications, Japan specializes in high-performance TECs for automotive and industrial uses.

North America

Characterized by technological innovation, North America holds 28% of the global Single-stage TEC market share. The U.S. leads with robust demand from medical device manufacturers and data center cooling applications, where precise temperature control is critical. Regulatory support through initiatives like the CHIPS and Science Act bolsters semiconductor-based cooling solutions. Major players like Laird Thermal Systems and TE Technology drive R&D in energy-efficient designs. A notable trend is the integration of TECs in electric vehicle battery thermal management systems, spurred by the Biden administration’s push for EV adoption. However, higher production costs compared to Asian counterparts restrain price-sensitive applications.

Europe

Europe’s market emphasizes sustainability, with stringent RoHS and WEEE regulations promoting eco-friendly thermoelectric materials. Germany and France are key contributors, leveraging TECs in industrial automation and renewable energy systems. The region shows growing adoption in biomedical applications like portable dialysis machines, supported by universal healthcare systems. Collaborative projects such as the EU’s Horizon Europe program fund research into high-efficiency thermoelectric materials. While environmental compliance increases production costs, it also creates differentiation opportunities for manufacturers emphasizing recyclability and low-carbon footprints.

South America

This emerging market is witnessing gradual growth, primarily in Brazil and Argentina, where telecommunications infrastructure upgrades drive demand for cooling 5G base stations. The automotive sector shows potential with increasing hybrid vehicle production. However, economic instability and reliance on imports for high-end TECs limit market expansion. Local players focus on aftermarket consumer electronics repairs rather than industrial applications. Governments are beginning to incentivize local semiconductor production, which could stimulate future TEC demand for domestic manufacturing.

Middle East & Africa

The region presents niche opportunities in telecommunications and oil/gas monitoring equipment. UAE and Saudi Arabia lead demand through smart city initiatives requiring precision cooling for IoT devices. South Africa shows potential in medical refrigeration for vaccine storage. Challenges include limited local manufacturing capabilities and dependence on Asian imports. However, strategic investments like Saudi Arabia’s Vision 2030 are gradually improving technological infrastructure, creating long-term prospects for specialized TEC applications in harsh desert environments.

Technology Adoption Variance: Asia-Pacific’s dominance stems from integration in high-volume electronics, whereas Western markets prioritize specialized applications. This dichotomy will persist, with Asia driving volume growth and Western regions focusing on performance optimization.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Single-stage TEC (Thermoelectric Cooler) markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Single-stage TEC market was valued at USD 543 million in 2024 and is projected to reach USD 958 million by 2032, growing at a CAGR of 8.7%.

- Segmentation Analysis: Detailed breakdown by product type (Circle Type, Rectangle Type, Others), technology, application (Consumer Electronics, Communication, Medical, Automotive, Industrial, Aerospace & Defense), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Asia-Pacific dominates with >50% market share in 2024, led by China.

- Competitive Landscape: Profiles of 25+ leading participants including Ferrotec (20%+ market share), KELK Ltd., Laird Thermal Systems, and Coherent Corp, covering product portfolios, R&D, manufacturing, and M&A activities.

- Technology Trends: Assessment of Peltier effect innovations, material science advancements, and integration with 5G/IoT/AI applications driving 9%+ CAGR in unit shipments.

- Market Drivers & Restraints: Evaluation of factors like 5G/EV adoption versus challenges such as lower efficiency compared to multi-stage TECs.

- Stakeholder Analysis: Strategic insights for semiconductor suppliers, OEMs, investors, and policymakers regarding the 130+ million unit global market.

Research methodology combines primary interviews with industry experts and validated secondary data from financial reports, trade associations, and patent analysis to ensure accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Single-stage TEC Market?

-> Single-stage TEC Market was valued at 543 million in 2024 and is projected to reach US$ 958 million by 2032, at a CAGR of 8.7% during the forecast period.

Which key companies operate in Global Single-stage TEC Market?

-> Key players include Ferrotec, KELK Ltd., Coherent Corp, Laird Thermal Systems, Guangdong Fuxin Technology, and KYOCERA, with top 5 players holding 55% market share.

What are the key growth drivers?

-> Growth is driven by 5G infrastructure, medical devices, electric vehicles, and demand for compact cooling solutions in consumer electronics.

Which region dominates the market?

-> Asia-Pacific commands over 50% share, with China as the largest consumer, while North America leads in high-end applications.

What are the emerging trends?

-> Trends include advanced semiconductor materials, miniaturization, and integration with IoT-enabled temperature control systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...