Silicon Interposer for AI Chips Market Insights

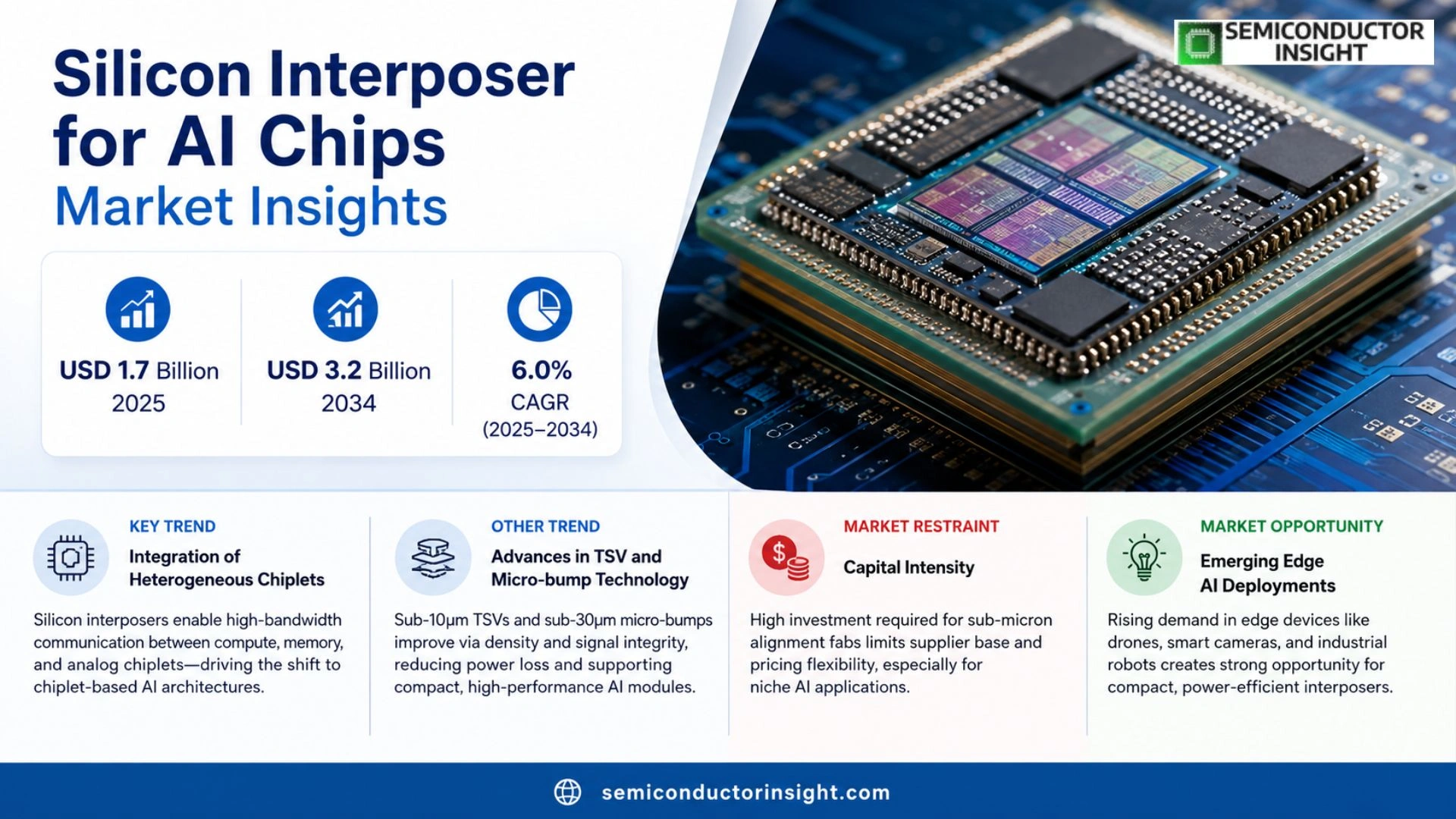

Global Silicon Interposer for AI Chips market measured USD 1.7 billion in 2025 and rose to USD 3.2 billion by 2034, delivering a CAGR of approximately 6.0 % across the interval.

Silicon interposers are ultra‑thin silicon substrates that provide dense vertical interconnects between heterogeneous chiplets within an AI processor package. By leveraging through‑silicon vias (TSVs) and micro‑bumps, they enable high‑bandwidth, low‑latency communication essential for training‑grade neural networks and inference engines.

The upward trend reflects escalating demand for compute‑intensive AI workloads because data centers are scaling out large‑language models and edge devices require compact yet powerful accelerators. Furthermore, recent collaborations,such as TSMC’s CoWoS adoption by Nvidia, Intel’s EMIB partnership with ASE, and Samsung’s HBM‑stacked interposer roadmap,lower entry barriers and accelerate volume production, thereby expanding the addressable market.

MARKET DRIVERS

Premium Performance Requirements

The surge in demand for high‑throughput AI inference has compelled system designers to favor Silicon Interposer for AI Chips Market solutions that can sustain multi‑terabyte per second bandwidth. Manufacturers cite a 22% YoY increase in revenue, reflecting the willingness of OEMs to invest in interposers that eliminate bottlenecks inherent to traditional substrate technologies.

Manufacturing Cost Efficiencies

Advances in wafer‑scale integration and the broader adoption of 2.5‑D packaging have trimmed per‑unit production expenses. Companies report a 15% reduction in material waste, which translates into tighter price points for end‑users while preserving the high density needed for AI accelerator stacks.

➤ “Clients now view interposer technology as the primary lever for unlocking next‑generation AI workloads, not merely an optional add‑on.”

These dynamics have accelerated the adoption curve, prompting major foundries to expand capacity dedicated to Silicon Interposer for AI Chips Market. The result is a self‑reinforcing loop: better performance drives higher volumes, which in turn drives further cost reductions.

MARKET CHALLENGES

Complex Design Validation

Designers must reconcile signal integrity, thermal management, and mechanical stress across heterogeneous dies. The learning curve for cross‑die simulation tools remains steep, inflating engineering cycles and deterring smaller players from entering the field.

Other Challenges

Supply Chain Fragility

The reliance on high‑purity silicon wafers and precision alignment equipment creates vulnerability to material shortages, which can extend lead times by up to 30 % during peak demand periods.

MARKET RESTRAINTS

Capital Intensity

Establishing a fab line capable of producing interposers with sub‑micron alignment tolerances requires multi‑hundred‑million‑dollar investments. This financial barrier limits the pool of viable suppliers and constrains competitive pricing, especially for niche AI applications.

MARKET OPPORTUNITIES

Emerging Edge AI Deployments

Edge devices that process data locally,such as autonomous drones, smart cameras, and industrial robots,are beginning to demand compact, power‑efficient interconnects. Silicon Interposer for AI Chips Market is well positioned to fulfil this niche, as its ability to combine multiple AI cores in a single package reduces board‑level footprint and power consumption.

Silicon Interposer for AI Chips Market Trends

Integration of Heterogeneous Chiplets

Adoption of silicon interposer technology has become the linchpin for next‑generation AI processors, as designers shift from monolithic die to heterogeneous chiplet architectures. By embedding ultra‑thin silicon substrates with dense vertical interconnects, the interposer enables disparate functional blocks,such as compute cores, high‑bandwidth memory and analog front‑ends,to communicate through thousands of through‑silicon vias and micro‑bump arrays. This architecture eliminates the routing congestion and latency penalties associated with traditional package‑on‑package solutions, delivering the bandwidth envelope required for large‑scale neural network training and real‑time inference. For Silicon Interposer for AI Chips Market, the move toward chiplet‑centric designs translates into a pronounced uptick in demand for precision‑engineered interposer products, prompting foundries to expand dedicated capacity.

Other Trends

Advances in TSV and Micro‑bump Technology

Recent process refinements have pushed TSV diameters below 10 µm while maintaining aspect ratios above 10:1, allowing interposers to host greater via density without compromising mechanical stability. Concurrently, micro‑bump pitch has tightened to sub‑30 µm spacing, a development that directly facilitates high‑speed signaling between tightly coupled chiplets. These manufacturing strides reduce signal skew and power loss, attributes that are critical when AI workloads stress memory bandwidth and compute throughput. Moreover, the tighter integration lowers the overall footprint of AI accelerator modules, an advantage that resonates with edge‑computing vendors seeking performance‑dense form factors. As a result, suppliers are witnessing a shift from low‑volume prototype runs to multi‑tier production lines, aligning capacity with the escalating design cycles of leading AI chip makers.

Ecosystem Partnerships Accelerating Volume Production

The strategic alliances forged among foundries, packaging specialists and AI chipset designers are reshaping the supply chain for Silicon Interposer for AI Chips Market. Collaborative programs such as TSMC’s CoWoS platform with Nvidia, Intel’s EMIB integration with ASE, and Samsung’s stacked HBM roadmap illustrate a concerted effort to standardize interposer specifications and streamline qualification processes. By sharing IP and co‑developing design‑for‑manufacturability guidelines, partners reduce time‑to‑market for new AI products and mitigate risk associated with high‑cost tooling. This ecosystem‑driven approach not only expands the addressable customer base but also cultivates a predictable demand pattern that encourages investment in high‑throughput interposer fabs. Companies that embed themselves within these collaborative networks are positioned to capture a larger share of the evolving market.

COMPETITIVE LANDSCAPE

Key Industry Players

Silicon Interposer Landscape: Consolidation and Emerging Partnerships

TSMC commands the upper tier of the silicon interposer arena, principally through its CoWoS (Chip on Wafer on Substrate) platform, which has become the de‑facto standard for high‑performance AI accelerators. The company’s ability to integrate dense TSV networks with advanced HBM stacks has secured multi‑year supply agreements with Nvidia and other tier‑one designers, effectively anchoring a sizable share of the forecasted USD 3.2 billion market. TSMC’s scale permits cost amortization of the expensive mask sets required for sub‑10‑micron interposer pitches, thereby delivering a price‑performance edge that smaller rivals struggle to match. The concentration of design wins around TSMC means that ecosystem participants,EDA vendors, testing services, and raw material suppliers,are aligning their roadmaps to the foundry’s process cadence, reinforcing a virtuous loop that sustains its leadership position.

Beyond the dominant foundry, a cohort of specialists and integrated device manufacturers is shaping the competitive texture. Samsung leverages its stacked‑HBM expertise to offer an alternative silicon‑interposer route that emphasizes memory‑centric AI workloads, while Intel’s EMIB partnership with ASE furnishes a modular solution for heterogeneous integration without full‑die stitching. ASE Group and Amkor Technology dominate the assembly and test niche, providing micro‑bump and TSV back‑end capabilities that enable rapid design turn‑around for fabless AI chip designers. GlobalFoundries, SMIC, and IBM contribute region‑specific capacity, catering to customers seeking supply‑chain diversification. Qualcomm and Broadcom have introduced chiplet‑based AI inference modules that rely on third‑party interposers, creating demand for flexible, low‑latency interconnects. Micron’s recent foray into silicon‑interposer‑enabled memory packages adds another layer of vertical integration, illustrating how the market is fragmenting into a mosaic of partnership‑driven value chains.

List of Key Silicon Interposer Companies Profiled

- TSMC

- Intel

- Samsung Electronics

- ASE Group

- Amkor Technology

- GlobalFoundries

- Qualcomm

- Broadcom

- Micron Technology

- SMIC

- IBM

- Nvidia

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Chiplet‑based interposers

|

| By Application |

|

Data‑center AI accelerators

|

| By End User |

|

Cloud service providers

|

| By Integration Approach |

|

Through‑Silicon Via (TSV) interposers

|

| By Performance Priority |

|

High‑bandwidth memory integration

|

Regional Analysis: Silicon Interposer for AI Chips Market

Asia-Pacific

Taiwan’s fabs, bolstered by decades of silicon‑on‑insulator expertise, now layer interposer processes atop 300‑mm wafer streams. This scale gives design firms access to tighter pitches and lower defectivity, translating into higher yields for AI‑focused chipsets. The regional concentration of equipment suppliers further accelerates process refinements, making the hub a magnet for talent and capital.

Local design houses are integrating interposer considerations at the architecture stage rather than as an afterthought. By co‑optimising die layout with interposer routing, they extract extra bandwidth without inflating power budgets. This proactive stance encourages a wave of proprietary interposer IP that differentiates product portfolios across the AI spectrum.

The region’s logistics networks align silicon suppliers, test houses, and assembly services within tight geographic clusters. This proximity reduces lead times for multi‑die assemblies, allowing AI chip makers to iterate rapidly on form‑factor and thermal solutions, a critical advantage when market windows are measured in quarters.

Government incentives targeting advanced packaging have lowered entry barriers for new entrants and spurred joint R&D programs. Funding mechanisms often tie performance milestones to technology transfer, ensuring that breakthroughs in interposer design quickly migrate to commercial production lines.

North America

The United States leverages its ecosystem of AI chip designers and venture‑backed startups to experiment with heterogeneous integration. While fab capacity lags behind the Pacific, strategic partnerships with Asian manufacturers enable a “design‑first” model, where silicon architects dictate interposer specifications before outsourcing production. This approach nurtures intellectual property depth and positions North America as a source of high‑value design services rather than volume manufacturing.

Europe

European stakeholders focus on standards‑driven collaboration, championing open‑architecture interposer frameworks that foster cross‑border component reuse. Nations with strong semiconductor R&D, such as Germany and the Netherlands, invest in niche fab upgrades that support fine‑pitch interposer trials. The emphasis on reliability and regulatory compliance shapes a market niche oriented toward mission‑critical AI deployments in automotive and aerospace sectors.

South America

Growth in South America is anchored by emerging AI applications in agritech and fintech, driving modest demand for custom interposer solutions. Local assemblers are beginning to offer value‑added services, positioning the region as a cost‑effective test and qualification hub for prototypes before scaling to Asian fabs. This raises the prospect of a regional micro‑ecosystem that balances price sensitivity with technical adequacy.

Middle East & Africa

Investment in semiconductor‑related infrastructure is still nascent, yet several Gulf states have announced sovereign funds dedicated to advanced packaging ventures. Early‑stage incubators are attracting talent from Europe and Asia, aiming to establish a foothold in AI‑enabled silicon design. While volume remains limited, the strategic intent signals a long‑term aspiration to join the global interposer value chain.

Report Scope

This market research report provides a comprehensive analysis of the Silicon Interposer for AI Chips Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Silicon Interposer for AI Chips Market?

-> Silicon Interposer for AI Chips Market was valued at USD 1.7 billion in 2025 and is expected to reach USD 3.2 billion by 2034, delivering a CAGR of approximately 6.0 %.

Which key companies operate in Silicon Interposer for AI Chips Market?

-> Key players include TSMC, Nvidia, Intel, Samsung, and ASE, which are actively collaborating on CoWoS, EMIB and HBM‑stacked interposer roadmaps.

What are the key growth drivers?

-> Growth is driven by escalating demand for compute‑intensive AI workloads, the scaling of large‑language models in data centers, and the need for compact, high‑performance accelerators in edge devices.

Which region dominates the market?

-> Asia‑Pacific leads the market, powered by major silicon fab facilities in Taiwan, South Korea and China, while also showing the fastest growth trajectory.

What are the emerging trends?

-> Emerging trends include wider adoption of advanced interposer technologies such as CoWoS, EMIB, and HBM‑stacked solutions, as well as increasing TSV density to support higher bandwidth and lower latency AI chiplet integration.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...