MARKET INSIGHTS

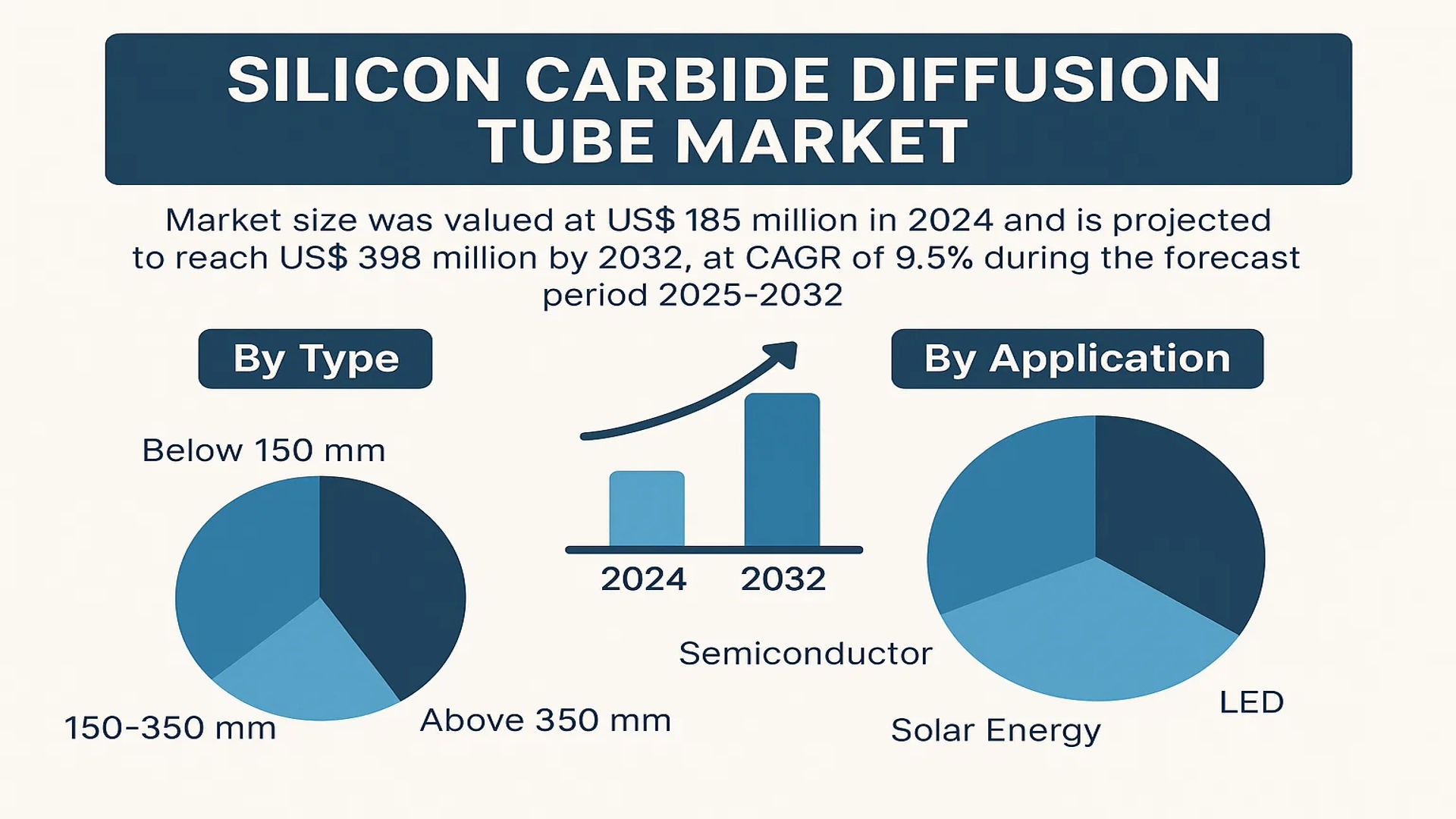

The global Silicon Carbide Diffusion Tube Market size was valued at US$ 185 million in 2024 and is projected to reach US$ 398 million by 2032, at a CAGR of 9.5% during the forecast period 2025-2032.

Silicon Carbide Diffusion Tubes are high-performance ceramic components widely used in semiconductor manufacturing, solar energy, and LED production. These tubes offer exceptional thermal stability, corrosion resistance, and mechanical strength, making them ideal for high-temperature diffusion processes. They come in various sizes, including below 150 mm, 150-350 mm, and above 350 mm, to meet diverse industrial requirements.

The market is driven by the growing semiconductor industry, advancements in renewable energy technologies, and increasing demand for energy-efficient lighting solutions. Key players such as Ferrotec Material Technologies Corporation, Coorstek, and Worldex Industry dominate the market, collectively holding a significant revenue share. Recent expansions in semiconductor fabrication facilities, particularly in Asia-Pacific, are expected to further propel market growth in the coming years.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Semiconductor Manufacturing to Accelerate Market Growth

The silicon carbide diffusion tube market is witnessing robust growth due to the rapid expansion of semiconductor fabrication facilities globally. Silicon carbide’s exceptional thermal conductivity and chemical inertness make it indispensable for high-temperature semiconductor processes. Over 30 new semiconductor fabs are currently under construction worldwide, with investments exceeding $200 billion. This surge in production capacity directly correlates with increased demand for critical components like diffusion tubes that can withstand extreme process conditions while maintaining purity standards essential for chip manufacturing.

Renewable Energy Sector Expansion to Fuel Adoption

Growing investments in solar energy infrastructure represent a significant driver for silicon carbide diffusion tubes. These components play a vital role in the production of photovoltaic cells, particularly in diffusion furnaces that require materials capable of enduring prolonged high-temperature operations. The global solar panel market is projected to maintain a compound annual growth rate exceeding 8% through 2030, creating sustained demand for specialized processing equipment. Manufacturers are developing larger diameter tubes (above 350mm) to accommodate next-generation wafer sizes, with several industry leaders announcing capacity expansions specifically targeting solar applications.

The push towards energy efficiency in industrial processes further amplifies this trend, as silicon carbide’s superior thermal properties can reduce energy consumption in high-temperature operations by up to 25% compared to traditional materials. This operational efficiency makes the material increasingly attractive despite higher upfront costs.

➤ Recent supply chain data indicates order backlogs for silicon carbide components have extended to 8-10 months across major manufacturers, highlighting the intense market demand.

MARKET RESTRAINTS

High Production Costs and Complex Manufacturing to Limit Market Penetration

The superior performance characteristics of silicon carbide diffusion tubes come with significant manufacturing challenges that restrain market growth. The material requires specialized sintering processes conducted at temperatures exceeding 2000°C, demanding advanced furnace technology and skilled operators. Production yields typically range between 60-70% even for established manufacturers, creating bottlenecks in meeting the current demand surge. These technical complexities contribute to silicon carbide tubes costing approximately 3-5 times more than conventional quartz alternatives, making adoption difficult for cost-sensitive applications.

Material Supply Chain Vulnerabilities

The market faces constraints from concentrated raw material sourcing, with over 75% of high-purity silicon carbide powder originating from a limited number of producers. Recent geopolitical tensions have exposed vulnerabilities in this supply chain, with lead times for critical raw materials extending beyond 6 months in some cases. Additionally, the energy-intensive production process makes manufacturers particularly susceptible to regional power shortages and rising energy costs.

Technical Limitations

While silicon carbide offers excellent thermal properties, its brittle nature poses handling challenges during installation and maintenance. Field data indicates that approximately 15-20% of premature tube failures result from mechanical damage during transportation or furnace loading rather than operational wear. This fragility increases total cost of ownership and creates hesitancy among some end-users to transition from more forgiving materials.

MARKET CHALLENGES

Intense Competition from Alternative Materials to Pressure Market Share

The silicon carbide diffusion tube market faces growing competition from advanced quartz and ceramic composite materials that offer comparable performance at lower price points. Recent developments in quartz doping technologies have produced variants capable of withstanding temperatures up to 1300°C – sufficient for many mid-range semiconductor processes. These alternatives currently capture about 35% of the diffusion tube market for processes below 1200°C, creating pricing pressure on silicon carbide solutions.

Technology Transition Risks

The semiconductor industry’s transition to larger wafer sizes presents both opportunities and challenges for silicon carbide tube manufacturers. While the shift to 300mm and 450mm wafers drives demand for larger diameter tubes, it also requires complete retooling of production lines. Industry estimates suggest the transition to next-generation wafer sizes could require capital investments exceeding $50 million per production line, potentially slowing adoption rates as manufacturers evaluate return on investment.

Quality Consistency Concerns

Maintaining material purity and dimensional tolerances across large-scale production runs remains an ongoing challenge. Even minor variations in silicon carbide composition or tube wall thickness can significantly impact diffusion process uniformity. Recent quality control data reveals that approximately 12% of tubes fail to meet the stringent specifications required for advanced semiconductor nodes below 10nm, creating bottlenecks for manufacturers serving this high-value segment.

MARKET OPPORTUNITIES

Emerging Applications in Wide Bandgap Semiconductor Production to Open New Revenue Streams

The rapid adoption of silicon carbide and gallium nitride semiconductors for electric vehicles and power electronics presents substantial growth opportunities for diffusion tube manufacturers. These next-generation semiconductors require even higher processing temperatures (up to 1800°C) where silicon carbide becomes the only viable containment material. With the wide bandgap semiconductor market projected to grow at over 30% CAGR through 2030, specialized diffusion tubes tailored for these applications could represent a $500 million addressable market within five years.

Aftermarket Services Expansion

The installed base of silicon carbide diffusion tubes has grown significantly in recent years, creating opportunities for maintenance, refurbishment, and recycling services. Analysis suggests the aftermarket for silicon carbide components could grow to represent 25% of total industry revenue by 2028 as manufacturers develop proprietary recoating and repair processes that extend tube lifespan by up to 40%. Several leading players have recently launched dedicated service divisions to capitalize on this recurring revenue opportunity.

Regional Manufacturing Expansion

Government incentives for semiconductor equipment localization in North America and Europe are prompting strategic investments in regional production. The market could see 5-7 new silicon carbide component manufacturing facilities established outside traditional Asian production hubs within the next three years, reducing lead times and improving supply chain resilience for end-users in these regions.

SILICON CARBIDE DIFFUSION TUBE MARKET TRENDS

Expansion of Semiconductor Manufacturing to Drive Market Growth

The global silicon carbide diffusion tube market is experiencing robust growth, primarily fueled by the rapid expansion of semiconductor manufacturing. Silicon carbide (SiC) tubes, known for their superior thermal conductivity and chemical resistance, have become indispensable in high-temperature diffusion processes used in chip fabrication. With semiconductor foundries expanding capacity to meet surging demand for advanced electronics, the market is projected to grow at a compound annual growth rate (CAGR) of approximately 7-9% over the next decade. Asia-Pacific, led by China, Taiwan, and South Korea, accounts for over 60% of global consumption due to concentrated semiconductor production. The increasing adoption of SiC tubes in epitaxial deposition and oxidation processes further strengthens this trend.

Other Trends

Renewable Energy Applications Gaining Traction

The solar energy sector is emerging as a significant consumer of silicon carbide diffusion tubes, particularly in photovoltaic cell manufacturing. These tubes play a critical role in the diffusion furnaces used for doping silicon wafers. As global solar installations continue to break records, with annual additions exceeding 250 GW in recent years, demand for high-performance diffusion tubes has skyrocketed. Manufacturers are increasingly focusing on developing tubes with enhanced purity levels (>99.999%) to meet the exacting standards of solar cell production. This segment is expected to grow at nearly double the industry average CAGR through 2032.

Technological Advancements in Tube Design

Recent innovations in silicon carbide diffusion tube technology are reshaping the competitive landscape. Leading manufacturers are investing heavily in improved sintering techniques that enhance tube durability while maintaining thermal stability. The introduction of gradient density SiC tubes has shown particular promise, offering up to 30% longer service life in harsh operating conditions. Furthermore, the integration of advanced coatings has significantly reduced particle contamination – a critical factor in semiconductor yield rates. These technological improvements are driving premiumization in the market, with high-performance tubes commanding 15-20% price premiums over standard offerings.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Expansion Drive Competition in Silicon Carbide Diffusion Tube Market

The global Silicon Carbide Diffusion Tube market exhibits a moderately consolidated structure, with a mix of established manufacturers and emerging players vying for market share. Ferrotec Material Technologies Corporation emerges as a dominant force, leveraging its expertise in advanced ceramics and diversified product offerings to maintain its leading position. With facilities spanning multiple continents, the company demonstrates strong supply chain resilience – a critical advantage in the current market environment.

Coorstek and Worldex Industry follow closely, collectively accounting for a significant portion of global revenues. These companies differentiate themselves through proprietary manufacturing techniques and strategic partnerships with semiconductor equipment manufacturers. Their ability to meet stringent purity and thermal stability requirements gives them an edge in serving high-end applications across the semiconductor and LED sectors.

The competitive intensity is further amplified by Chinese manufacturers like Shandong Huamei and Xian Zhongwei, who are aggressively expanding their production capacities. While traditionally focused on domestic markets, these players are increasingly targeting international customers through competitive pricing strategies and improving product quality standards.

Supply chain optimization has become a key differentiator, with leading players vertically integrating their operations from raw material procurement to final product testing. CE-MAT and Kallex Company have particularly excelled in this aspect, allowing them to maintain stable pricing despite fluctuations in silicon carbide feedstock costs.

A notable trend among top competitors is the shift toward larger diameter tubes (above 350mm) to cater to next-generation semiconductor fab requirements. This technological evolution requires significant capital investment, potentially reshaping the competitive landscape as smaller players may struggle to keep pace with these advancements.

List of Key Silicon Carbide Diffusion Tube Manufacturers

- Ferrotec Material Technologies Corporation (Japan)

- Coorstek (U.S.)

- Worldex Industry (China)

- CE-MAT (Germany)

- Kallex Company (China)

- Shandong Huamei (China)

- Xian Zhongwei (China)

- Tangshan FCT (China)

- Ningbo VET Energy Technology (China)

Segment Analysis:

By Type

Below 150 mm Segment Leads the Market Due to Widespread Adoption in Semiconductor Fabrication

The Silicon Carbide Diffusion Tube market is segmented based on type into:

- Below 150 mm

- 150-350 mm

- Above 350 mm

By Application

Semiconductor Segment Dominates Owing to High Demand for High-Temperature Processing Solutions

The market is segmented based on application into:

- Semiconductor

- Solar Energy

- LED

By Material Grade

High-Purity Silicon Carbide Gains Importance for Critical Semiconductor Applications

The market is segmented based on material grade into:

- Standard Grade

- High Purity Grade

Regional Analysis: Silicon Carbide Diffusion Tube Market

North America

The Silicon Carbide Diffusion Tube market in North America is driven by its advanced semiconductor and solar energy industries, particularly in the U.S., where demand is bolstered by substantial R&D investments and strict quality standards. The region benefits from a well-established supply chain and collaborations between manufacturers like Coorstek and Ferrotec. Government initiatives supporting next-generation electronics and renewable energy further stimulate growth. However, high production costs and competition from Asian suppliers pose challenges. The market is expected to rise steadily, leveraging technological advancements in SiC-based power electronics and LED applications.

Europe

Europe’s market thrives on stringent regulatory frameworks that emphasize eco-friendly production and energy-efficient semiconductor manufacturing. Countries like Germany and France lead in adopting SiC diffusion tubes for automotive and industrial applications, thanks to strong collaborations between research institutions and manufacturers. Despite being a mature market, Europe faces constraints from high raw material costs and reliance on imports. The shift toward sustainable energy solutions, including solar and power electronics, continues to drive demand. Emerging innovations in wide-bandgap semiconductors present long-term opportunities for market expansion.

Asia-Pacific

The Asia-Pacific region dominates the global Silicon Carbide Diffusion Tube market, accounting for the highest consumption volume. China, Japan, and South Korea lead due to their thriving semiconductor and LED industries, supported by aggressive government policies and local manufacturing hubs. The cost-competitive production ecosystem attracts global players, though quality disparities persist in some markets. Countries like India are gradually increasing their adoption of SiC technology, fueled by rising renewable energy projects. The region’s market is expected to maintain rapid growth, driven by expanding 5G infrastructure and electric vehicle manufacturing, though supply chain disruptions occasionally hinder progress.

South America

South America’s market remains nascent but promising, with Brazil showing gradual uptake in semiconductor and solar panel production. Limited local manufacturing capabilities and economic instability slow widespread adoption, forcing reliance on imports. However, increasing investments in renewable energy infrastructure and partnerships with global suppliers offer growth potential. Manufacturers must navigate trade barriers and logistical challenges to capitalize on this emerging demand. The market’s trajectory largely depends on policy reforms and technological advancements in material sciences.

Middle East & Africa

This region presents long-term potential, particularly in Gulf countries like Saudi Arabia and the UAE, where diversification efforts are boosting semiconductor and solar energy projects. However, the market is constrained by limited industrial infrastructure and a lack of local expertise. Africa’s growth is slower due to funding gaps and fragmented supply chains, though South Africa shows modest demand for LED and energy applications. Partnerships with global manufacturers and technology transfers could accelerate market development, provided geopolitical and economic hurdles are addressed.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Silicon Carbide Diffusion Tube markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Silicon Carbide Diffusion Tube market was valued at US$ 185 million in 2024 and is projected to reach US$ 398 million by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Below 150 mm, 150-350 mm, Above 350 mm), application (Semiconductor, Solar Energy, LED), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. market size is estimated at USD million in 2024, while China is projected to reach USD million.

- Competitive Landscape: Profiles of leading market participants including Ferrotec Material Technologies Corporation, Coorstek, Worldex Industry, CE-MAT, and Kallex Company, covering their product offerings, R&D focus, manufacturing capacity, and recent developments.

- Technology Trends & Innovation: Assessment of emerging semiconductor fabrication techniques, material advancements, and evolving industry standards in diffusion tube technology.

- Market Drivers & Restraints: Evaluation of factors driving market growth including semiconductor industry expansion, along with challenges such as raw material constraints and high manufacturing costs.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Silicon Carbide Diffusion Tube Market?

-> Silicon Carbide Diffusion Tube Market size was valued at US$ 185 million in 2024 and is projected to reach US$ 398 million by 2032, at a CAGR of 9.5% during the forecast period 2025-2032.

Which key companies operate in Global Silicon Carbide Diffusion Tube Market?

-> Key players include Ferrotec Material Technologies Corporation, Coorstek, Worldex Industry, CE-MAT, Kallex Company, Shandong Huamei, and Xian Zhongwei, among others.

What are the key growth drivers?

-> Key growth drivers include expansion of semiconductor manufacturing, increasing solar energy adoption, and growing LED production.

Which region dominates the market?

-> Asia-Pacific is the dominant market, driven by semiconductor manufacturing in China, Japan, and South Korea, while North America shows significant growth potential.

What are the emerging trends?

-> Emerging trends include development of larger diameter tubes, improved thermal stability solutions, and integration with advanced semiconductor fabrication processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...