Market Insights

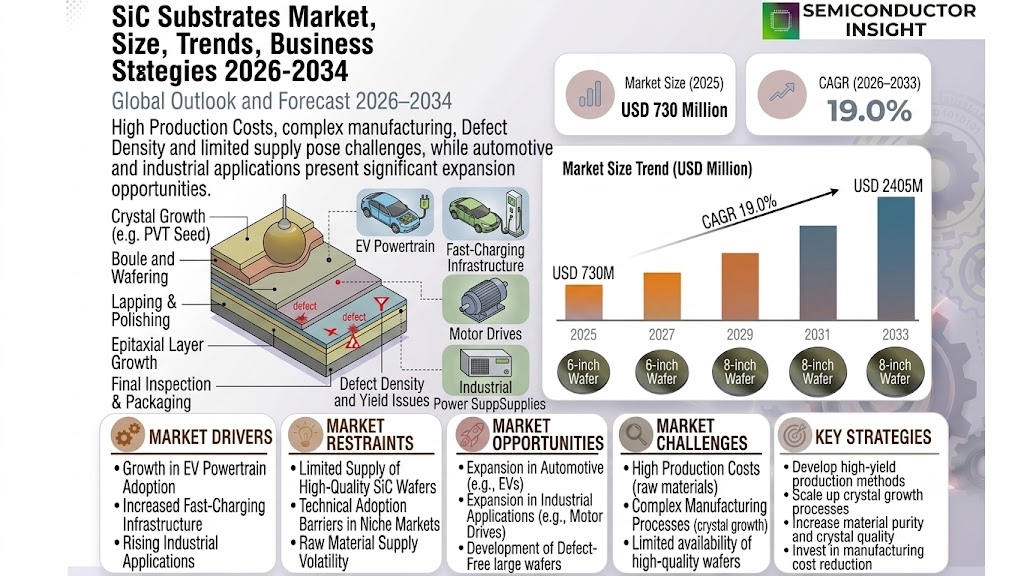

Global SiC Substrates Market size was valued at USD 730 million in 2025. The market is projected to grow from USD 730 million in 2025 to USD 2405 million by 2033, exhibiting a CAGR of 19.0% during the forecast period.

Silicon carbide (SiC) substrates are semiconductor materials known for their superior electrical and thermal properties compared to traditional silicon or gallium arsenide wafers. These substrates are particularly suited for high-temperature and high-power applications, making them essential in industries such as power electronics, RF devices, and optoelectronics. Available in polytypes like 4-H and 6-H, SiC Substrates are typically nitrogen-doped and polished for optimal performance.

The market is experiencing robust growth due to increasing demand for energy-efficient power devices and advancements in electric vehicle (EV) technologies. Furthermore, the adoption of SiC Substrates in renewable energy systems and telecommunications infrastructure is accelerating market expansion. Key players such as Cree (Wolfspeed), II-VI Advanced Materials, and ROHM dominate the industry, collectively holding over 56% of the global market share. North America leads the market with a 34% share, followed closely by China and Europe at approximately 26% each.

MARKET DRIVERS

Increasing Demand for Energy-Efficient Power Electronics

Global SiC Substrates Market is driven by rising demand for energy-efficient semiconductor materials in power electronics. Silicon carbide offers superior thermal conductivity and high breakdown voltage, making it ideal for electric vehicles (EVs) and renewable energy systems. The growing adoption of EVs has accelerated the need for efficient power modules, with SiC Substrates enabling higher energy conversion efficiency compared to silicon.

Growth in 5G and RF Applications

Silicon carbide substrates are increasingly used in 5G infrastructure due to their high-frequency performance and thermal stability. The expansion of 5G networks globally is creating substantial demand for SiC-based RF devices, supporting efficient power amplification and signal processing.

Additionally, government initiatives promoting renewable energy projects are further supporting market expansion, as SiC-based solutions enhance efficiency in solar inverters and grid systems.

MARKET CHALLENGES

High Production Costs and Complex Manufacturing Processes

The fabrication of SiC Substrates involves high-cost raw materials and complex crystal growth techniques, which increase overall production expenses. Limited availability of high-quality silicon carbide wafers also poses supply chain challenges for manufacturers.

Other Challenges

Defect Density and Yield Issues

Maintaining low defect density in SiC Substrates remains a significant technical hurdle, impacting production yields. Manufacturers face difficulties in scaling up production while maintaining high material purity and crystal quality.

MARKET RESTRAINTS

Limited Supply of High-Quality SiC Wafers

SiC Substrates Market faces constraints due to the limited number of suppliers capable of producing defect-free, large-diameter wafers. This scarcity restricts the adoption rate in high-performance applications where reliability is critical, such as aerospace and defense.

MARKET OPPORTUNITIES

Expansion in Automotive and Industrial Applications

The automotive industry represents a major growth opportunity for SiC Substrates , particularly in EV powertrains and fast-charging infrastructure. Industrial applications, including motor drives and power supplies, are also embracing SiC technology to improve energy efficiency and reduce operational costs.

SiC Substrates Market Trends

Rapid Market Growth Driven by High-Power Applications

Global SiC Substrates Market is projected to grow from USD 730 million in 2025 to USD 2405 million by 2033, exhibiting a robust 19% CAGR. This expansion is fueled by increasing adoption of SiC Substrates in power components and RF devices for electric vehicles, renewable energy systems, and 5G infrastructure. The material’s superior thermal conductivity and high breakdown voltage make it ideal for these demanding applications.

Other Trends

Technology Advancements in Crystal Growth

Manufacturers are making significant progress in 8-inch wafer production, with Cree (Wolfspeed) leading the transition from 6-inch substrates. This shift promises substantial cost reductions through economies of scale, potentially lowering SiC device prices by 20-30% in the medium term.

Geographical Market Shifts

While North America currently holds 34% market share, China is rapidly catching up with substantial investments in domestic production. The Chinese government’s semiconductor self-sufficiency policies have accelerated local companies like TankeBlue Semiconductor, which now control about 80% of China’s SiC substrate market.

Supply Chain Diversification

Global players are establishing multiple production bases to mitigate geopolitical risks, with II-VI Advanced Materials and ROHM expanding facilities in both the US and Europe. This strategy aims to ensure stable supply as demand from automotive and industrial sectors grows.

Emerging Application Areas

Beyond traditional power electronics, SiC Substrates are gaining traction in aerospace and defense applications where radiation hardness and high-temperature stability are critical. The market is also seeing increased adoption in fast-charging infrastructure for electric vehicles.

COMPETITIVE LANDSCAPE

Key Industry Players

Global SiC Substrates Market Dominated by US and Japanese Players

Global SiC Substrates Market remains highly concentrated, with Cree (Wolfspeed) and II-VI Advanced Materials maintaining technological leadership and holding approximately 30% combined market share. North American manufacturers dominate production capabilities, particularly in 6-inch and larger diameter wafers, while Japanese firms like ROHM and Showa Denko specialize in high-purity substrates for automotive applications. These established players benefit from decade-long R&D investments and extensive patent portfolios covering crystal growth techniques.

Chinese manufacturers including TankeBlue Semiconductor and SICC Materials are rapidly expanding capacity with government support, focusing on 4-inch substrates for domestic power electronics markets. Emerging players like Beijing Cengol Semiconductor and Hebei Synlight Crystal are making strides in improving defect density and throughput, though still lag in large-diameter wafer production. Europe’s Norstel (acquired by STMicroelectronics) continues to advance in low-defect substrates for industrial applications.

List of Key SiC Substrates Companies Profiled

- Cree (Wolfspeed)

- II-VI Advanced Materials

- TankeBlue Semiconductor

- SICC Materials

- Beijing Cengol Semiconductor

- Showa Denko (NSSMC)

- Hebei Synlight Crystal

- Norstel (STMicroelectronics)

- ROHM

- SK Siltron

- Dow Corning (Now part of Dow Inc.)

- Nippon Steel

- Ascatron

- GeneSiC Semiconductor

- SemiQ Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

6 Inch Substrates

|

| By Application |

|

Power Components

|

| By End User |

|

Automotive Sector

|

| By Crystal Structure |

|

4H-SiC Structure

|

| By Doping Type |

|

Nitrogen-doped (N-type)

|

Regional Analysis: Global SiC Substrates Market

Asia-Pacific

China’s aggressive fab expansion and vertical integration strategies position it as the largest SiC Substrates consumer. Domestic firms are achieving yield improvements through government-backed pilot production lines and collaborations with international equipment suppliers.

Japanese producers maintain technological leadership in low-defect SiC crystal growth, with patented thermal management solutions enabling superior substrate performance. Their expertise supports premium pricing strategies for automotive-grade materials.

Strong partnerships between Korean SiC substrate suppliers and domestic power semiconductor giants create a captive demand pipeline. Investments focus on throughput optimization to serve mass-market EV applications.

Taiwan leverages its semiconductor ecosystem to bridge substrate production with advanced SiC device fabrication. Leading foundries drive substrate specification standardization to accelerate design-in processes for global customers.

North America

The North American SiC Substrates Market thrives on defense and aerospace applications requiring radiation-hardened solutions. U.S. initiatives like the CHIPS Act strategically prioritize domestic SiC supply chain development, supporting wafer production scale-up. Automotive OEM collaboration with substrate producers accelerates qualification for next-generation EV powertrains. Silicon Valley startups introduce novel crystalline growth techniques to challenge established suppliers.

Europe

Europe’s SiC substrate industry benefits from cross-border research consortia and stringent industrial power efficiency regulations. German automotive tier-1s drive demand for locally-sourced materials, while Italian and French equipment manufacturers provide specialized crystal growth technologies. EU funding initiatives foster substrate innovations targeting renewable energy infrastructure needs.

Middle East & Africa

Emerging investments in SiC substrate auxiliary industries mark the region’s entry into the value chain. Strategic partnerships with Asian and European technology providers aim to establish local test and characterization capabilities, particularly for high-temperature applications suited to regional environmental conditions.

South America

Brazil shows early-stage SiC substrate industry development focused on power electronics for industrial motor drives and energy transmission. Collaborative agreements with North American technology licensors help overcome technical barriers, while tax incentives attract wafer processing equipment investments.

Report Scope

This market research report provides a comprehensive analysis of the SiC Substrates Market , covering the forecast period 2025–2033. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of SiC Substrates Market?

-> SiC Substrates Market size was valued at USD 730 million in 2025. The market is projected to grow from USD 730 million in 2025 to USD 2405 million by 2033, exhibiting a CAGR of 19.0% during the forecast period.

Which key companies operate in SiC Substrates Market?

-> Key players include Cree (Wolfspeed), II-VI Advanced Materials, ROHM, TankeBlue Semiconductor, and SICC Materials, among others. The top 5 companies hold about 56% market share.

What are the key growth drivers?

-> Key growth drivers include increasing demand for high-power and high-temperature devices, advancements in LED technology, and rising adoption in automotive and telecommunications sectors.

Which region dominates the market?

-> North America is the largest market with 34% share, followed by China and Europe with 26% and 29% shares respectively.

What are the emerging trends?

-> Emerging trends include development of larger wafer sizes (from 2″ to 8″), increasing focus on domestic production capabilities, and technological advancements in crystal manufacturing processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...