MARKET INSIGHTS

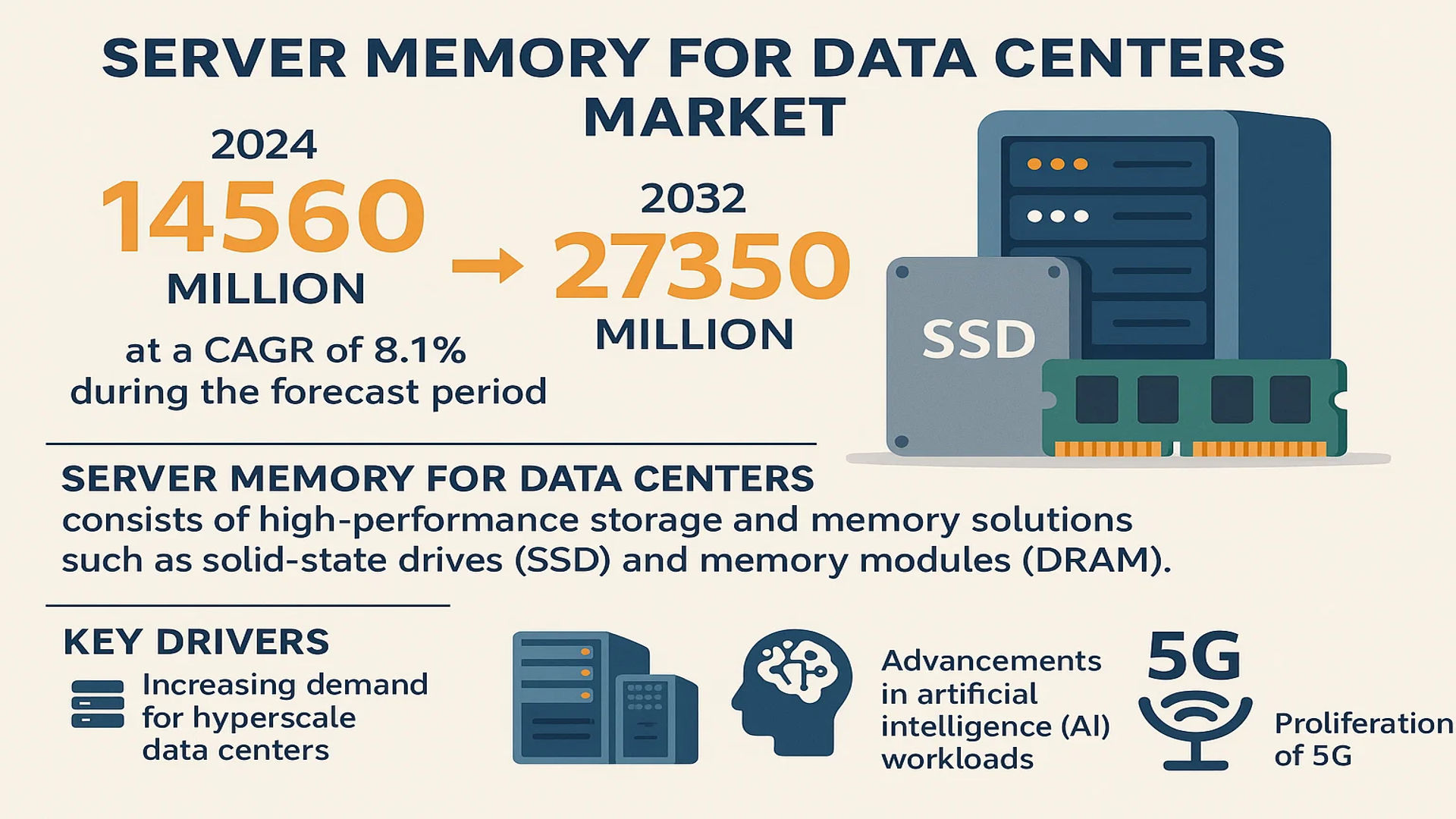

The global Server Memory for Data Centers market was valued at 14560 million in 2024 and is projected to reach US$ 27350 million by 2032, at a CAGR of 8.1% during the forecast period.

Server memory for data centers consists of high-performance storage and memory solutions such as solid-state drives (SSD) and memory modules (DRAM), which are critical for enterprise and cloud-based infrastructure. SSDs leverage NAND flash memory for persistent, low-latency data storage, while DRAM modules ensure rapid access to frequently used data, enabling real-time processing and scalability for modern applications.

The market is driven by increasing demand for hyperscale data centers, advancements in artificial intelligence (AI) workloads, and the proliferation of 5G networks. For instance, in 2024, Samsung introduced its latest 32GB DDR5 memory modules, designed for energy efficiency and high-speed data processing. Meanwhile, Micron Technology expanded its SSD portfolio with PCIe Gen5 solutions, targeting enterprise workloads. Key players like SK Hynix and Western Digital continue to innovate in response to rising demand from both internet data centers (IDCs) and enterprise data centers (EDCs).

MARKET DYNAMICS

MARKET DRIVERS

Exponential Growth of Hyperscale Data Centers to Fuel Server Memory Demand

The global surge in hyperscale data center construction is creating unprecedented demand for high-performance server memory solutions. Hyperscale facilities, which power cloud computing giants and AI platforms, prioritize high-density memory configurations to handle massive workloads. Recent industry analysis indicates that the average memory capacity per server in hyperscale environments has surpassed 500GB, with projections reaching 1TB by 2026. This growth is directly tied to the expansion of cloud services, where annual spending on infrastructure is growing at nearly 20% compound annual growth rate. Memory innovations such as DDR5 and PCIe Gen5 SSDs are becoming standard in these environments due to their superior bandwidth and energy efficiency.

AI and Machine Learning Workloads Accelerating Adoption of High-Bandwidth Memory

The artificial intelligence revolution represents perhaps the single most significant driver for advanced server memory solutions. Training complex neural networks requires memory bandwidth exceeding 1TB/s – far beyond what traditional DRAM can provide. This has led to rapid adoption of High Bandwidth Memory (HBM) solutions, with market adoption growing at over 45% annually. Generative AI applications particularly highlight this trend, where a single large language model training session can utilize server memory configurations amounting to hundreds of petabytes. Memory manufacturers are responding with 3D-stacked designs offering bandwidth up to 4.8Gbps per pin, while enterprise SSD adoption in AI training environments has tripled in the past two years.

Enterprise Digital Transformation Initiatives Creating Sustained Demand

Global enterprises across sectors are undertaking comprehensive digital transformation programs that significantly increase their server memory requirements. The migration of critical workloads to private and hybrid cloud environments has caused enterprise data center operators to upgrade their memory infrastructure substantially. Financial institutions now commonly deploy servers with 1-2TB RAM configurations for in-memory databases, while healthcare providers require high-performance SSDs to handle medical imaging datasets that often exceed hundreds of terabytes. Market data shows enterprise investments in server memory upgrades grew by 18% year-over-year, with particular strength in the financial services and healthcare verticals.

MARKET RESTRAINTS

Supply Chain Fragility and Geopolitical Factors Impacting Memory Availability

The server memory market faces significant challenges from complex global supply chains and geopolitical tensions. Over 85% of advanced memory components originate from a concentrated production region, creating volatility in availability and pricing. Recent trade restrictions have caused price fluctuations exceeding 30% for certain high-performance memory modules. Semiconductor manufacturing facilities require billions in capital investment and years to establish, limiting the industry’s ability to rapidly respond to demand surges or supply disruptions. These factors create substantial planning challenges for data center operators who must balance performance requirements with budgetary constraints and component availability.

Thermal and Power Constraints in High-Density Deployments

As server memory densities continue increasing to meet performance demands, thermal management has emerged as a critical constraint. High-performance DDR5 modules consume up to 20% more power than previous generations during peak operation, while enterprise-grade SSDs in RAID configurations can generate substantial thermal load. Data center operators report that memory-related cooling expenses now represent nearly 15% of total facility operational costs, up from 8% five years ago. This creates difficult tradeoff decisions between performance requirements and operational efficiency, particularly in colocation environments where power and cooling capacities are contractually limited.

MARKET OPPORTUNITIES

Emerging Memory Technologies Creating New Performance Paradigms

The industry stands at the cusp of multiple breakthrough memory technologies that promise to redefine data center performance. Compute Express Link (CXL) memory pooling architectures enable unprecedented memory disaggregation and utilization efficiencies, with pilot deployments showing 40% improvements in resource utilization. Meanwhile, storage-class memory solutions blending DRAM and NAND characteristics are entering the market, offering persistent memory with near-DRAM performance. The total addressable market for these next-generation solutions is projected to exceed $12 billion by 2027, representing both a technological and economic opportunity for memory manufacturers and data center operators alike.

Sustainability Innovations Opening New Market Segments

Environmental concerns are driving demand for energy-efficient memory solutions that reduce data center carbon footprints. Low-power DDR5 modules now achieve 20% better performance-per-watt than previous generations, while advanced NAND flash architectures reduce erase/write energy consumption by up to 35%. The green data center market, valued at over $50 billion, increasingly prioritizes these memory innovations as part of comprehensive sustainability strategies. Memory manufacturers responding to this trend gain competitive advantage in enterprise and government procurement processes where environmental impact has become a key evaluation criterion.

MARKET CHALLENGES

Accelerating Obsolescence Cycles Increasing Refresh Costs

The server memory industry faces mounting pressure from increasingly rapid technology obsolescence cycles. Where enterprises previously maintained server fleets for 5-7 years, memory-intensive workloads now drive refresh cycles as short as 2-3 years. This creates significant capital expenditure challenges, particularly for organizations with large server deployments. The financial impact is compounded by the steep price premiums for cutting-edge memory technologies – first-adopter costs for new memory standards can exceed established solutions by 50-70%. These dynamics force difficult budgeting decisions between performance requirements and total cost of ownership.

Increasing Complexity in Memory Hierarchy Management

Modern server architectures now incorporate complex memory hierarchies including DRAM, persistent memory, SSD caching, and storage-class memory – each requiring specialized management. Data center operators report spending up to 30% more engineering time optimizing memory configurations compared to three years ago. The challenge is particularly acute for cloud service providers managing heterogenous workloads across their server fleets. Without effective automation tools, this complexity can lead to suboptimal memory utilization and performance bottlenecks, potentially eroding the value proposition of premium memory investments.

SERVER MEMORY FOR DATA CENTERS MARKET TRENDS

Adoption of High-Speed and High-Capacity Memory Solutions Accelerates Growth

The global server memory market is witnessing accelerated growth due to increasing demand for high-speed and high-capacity storage solutions in data centers worldwide. The shift toward cloud computing, artificial intelligence (AI), and machine learning (ML) workloads requires faster data processing, driving the adoption of DDR5 and advanced SSDs. DDR5 memory technology, which offers nearly double the bandwidth of DDR4, is becoming a standard in enterprise applications. Meanwhile, the rise of PCIe Gen 5 SSDs ensures ultra-fast data transfer speeds of up to 128 GT/s, catering to latency-sensitive workloads. Additionally, investments in hyperscale data centers, expected to exceed $150 billion by 2025, further boost memory module and SSD demand.

Other Trends

Rapid Expansion of AI-Powered Data Centers

The surge in AI-driven computing necessitates memory solutions that can handle massive parallel workloads. Server memory manufacturers are optimizing DRAM and SSDs for AI infrastructure, offering enhanced bandwidth and low-latency storage. High-Bandwidth Memory (HBM), integrated in AI accelerators, is gaining traction due to its ability to process large datasets efficiently. The growing AI chip market, projected to surpass $83 billion by 2027, underscores the need for advanced server memory that supports real-time analytics and deep learning models. Moreover, enterprise adoption of generative AI tools is accelerating investments in memory infrastructure to handle unstructured data processing.

Energy Efficiency and Sustainability Take Center Stage

Data centers account for nearly 1-1.5% of global electricity consumption, pushing vendors to develop energy-efficient memory solutions. Innovations like low-power DDR5 (LPDDR5) and NAND flash with reduced power consumption are gaining prominence as enterprises seek sustainable operations. Governments and regulatory bodies have also imposed stricter energy efficiency requirements, prompting data centers to upgrade legacy memory hardware. Additionally, liquid-cooled storage devices are emerging as an innovation to reduce heat dissipation in high-performance computing environments. Such advancements align with the global push toward carbon-neutral data centers by 2030, shaping the next generation of server memory technologies.

COMPETITIVE LANDSCAPE

Key Industry Players

Memory Manufacturers Expand Capacities and Innovation to Meet Data Center Demands

The global server memory for data centers market presents a semi-consolidated competitive landscape, dominated by semiconductor giants with vertically integrated manufacturing capabilities alongside specialized memory solution providers. Samsung leads the market with its comprehensive portfolio of high-performance SSDs and DRAM modules, holding the largest NAND flash market share of approximately 33% as of 2024. The company’s technological leadership in 3D NAND and DDR5 memory gives it strategic advantages in meeting hyperscale data center requirements.

SK Hynix and Micron Technology follow closely, together accounting for about 45% of the server DRAM market. Their recent joint development of the industry’s first 321-layer NAND flash demonstrates the rapid innovation cycle in this sector. These companies are increasingly focusing on energy-efficient memory solutions to address data center sustainability goals, with SK Hynix recently announcing a 30% reduction in power consumption for their latest server DDR5 modules.

The competitive intensity is further heightened by emerging Chinese players like Changxin Memory Technologies (CXMT), which has been gaining traction through aggressive pricing strategies and government-backed capacity expansions. While currently holding a smaller market share, Chinese manufacturers are expected to significantly influence price dynamics and regional supply chains over the forecast period.

Specialty manufacturers such as Kingston Technology and SMART Modular Technologies maintain strong positions in the enterprise segment through customized solutions and robust quality control. Their ability to provide legacy support and specialized configurations allows them to compete effectively against larger players in certain vertical markets. Meanwhile, controller and interface technology companies like Rambus play a crucial supporting role through licensing and chipset innovations that enhance overall memory performance.

List of Key Server Memory for Data Centers Market Players

- Samsung Electronics (South Korea)

- SK Hynix (South Korea)

- Micron Technology (U.S.)

- Western Digital (U.S.)

- Kioxia (Japan)

- Changxin Memory Technologies (China)

- Kingston Technology (U.S.)

- SMART Modular Technologies (U.S.)

- ADATA Technology (Taiwan)

- Rambus (U.S.)

- Innodisk (Taiwan)

- Apacer Technology (Taiwan)

Segment Analysis:

By Type

Solid-State Drive (SSD) Segment Leads Due to High Performance and Reliability in Modern Data Centers

The market is segmented based on type into:

- Solid-State Drive (SSD)

- Memory Modules

- Subtypes: DDR4, DDR5, and others

By Application

Internet Data Center (IDC) Segment Dominates Due to Rising Cloud Computing and Big Data Analytics Demand

The market is segmented based on application into:

- IDC (Internet Data Center)

- EDC (Enterprise Data Center)

- Others

Regional Analysis: Server Memory for Data Centers Market

Asia-Pacific

The Asia-Pacific region dominates the global server memory market, driven by rapid digital transformation and massive investments in hyperscale data centers. China, Japan, South Korea, and India collectively account for over 45% of global demand, with China leading due to its booming cloud computing sector and expanding 5G infrastructure. Key players like Samsung, SK Hynix, and Changxin Memory Technologies (CXMT) operate heavily in this region, supplying high-performance SSDs and DRAM modules for data-intensive applications. While cost-competitive solutions remain popular, advancements in DDR5 and NAND flash technologies are pushing the shift toward energy-efficient deployments. However, geopolitical tensions and export restrictions pose supply chain risks.

North America

North America, particularly the U.S., leads in high-capacity memory adoption, fueled by hyperscalers like AWS, Google, and Microsoft expanding their data center footprint. The market prioritizes low-latency, high-bandwidth solutions, with Micron Technology and Western Digital driving innovations in enterprise-grade SSDs and persistent memory. Government initiatives like the CHIPS and Science Act, allocating $52 billion for semiconductor R&D, are accelerating domestic production. However, stringent data sovereignty laws and trade disputes with China impact sourcing strategies for memory components.

Europe

Europe’s market is characterized by stringent data privacy regulations (GDPR) and a push for sustainability in data center operations. Countries like Germany, the UK, and France are investing in edge computing and hybrid cloud models, increasing demand for low-power DDR4 and NVMe SSDs. Local manufacturers like Infineon and STMicroelectronics collaborate with global players to meet regional requirements. The EU’s focus on semiconductor self-sufficiency under the European Chips Act further supports the development of advanced memory solutions, though reliance on imports persists. Energy efficiency remains a critical benchmark due to rising operational costs.

South America

South America’s market is nascent but growing, with Brazil and Argentina emerging as key hubs for enterprise data centers. The adoption of server memory is driven by increasing cloud service penetration, though budget constraints limit large-scale deployments. Most memory modules are imported, with Kingston and ADATA being preferred suppliers due to competitive pricing. Infrastructure bottlenecks and economic instability remain hurdles, but investments in AI and IoT applications are expected to boost demand for scalable memory solutions in the long term.

Middle East & Africa

The MEA region is witnessing gradual expansion, led by Saudi Arabia, UAE, and South Africa, where smart city projects and digital government initiatives are fueling data center growth. Demand centers on reliable, high-availability memory for financial and telecom sectors, with Samsung and SK Hynix dominating imports. While renewable energy-powered data centers are gaining traction, the high cost of advanced memory technologies slows adoption. Partnerships with global hyperscalers and local investments in AI infrastructure could unlock future opportunities.

Report Scope

This market research report provides a comprehensive analysis of the Global Server Memory for Data Centers market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 14,560 million in 2024 and is projected to reach USD 27,350 million by 2032, growing at a CAGR of 8.1%.

- Segmentation Analysis: Detailed breakdown by product type (SSD and Memory Modules), application (IDC, EDC, and others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. The U.S. and China are key growth markets.

- Competitive Landscape: Profiles of leading market participants, including Samsung, SK Hynix, Micron Technology, Kioxia, and Western Digital, among others, with their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies such as DDR advancements, persistent memory, and AI-driven storage optimization in server memory solutions.

- Market Drivers & Restraints: Evaluation of factors driving market growth, including data center expansion, cloud computing demand, and 5G deployment, alongside challenges like supply chain disruptions and high costs.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of the Global Server Memory for Data Centers Market?

-> Server Memory for Data Centers market was valued at 14560 million in 2024 and is projected to reach US$ 27350 million by 2032, at a CAGR of 8.1% during the forecast period.

Which key companies operate in the Global Server Memory for Data Centers Market?

-> Key players include Samsung, SK Hynix, Micron Technology, Kioxia, Western Digital, and Kingston Technology, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for cloud computing, expansion of hyperscale data centers, and advancements in AI and machine learning workloads.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by China and South Korea, while North America remains a dominant market due to high data center investments.

What are the emerging trends?

-> Emerging trends include high-capacity DDR5 adoption, persistent memory solutions, and energy-efficient server memory designs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...