MARKET INSIGHTS

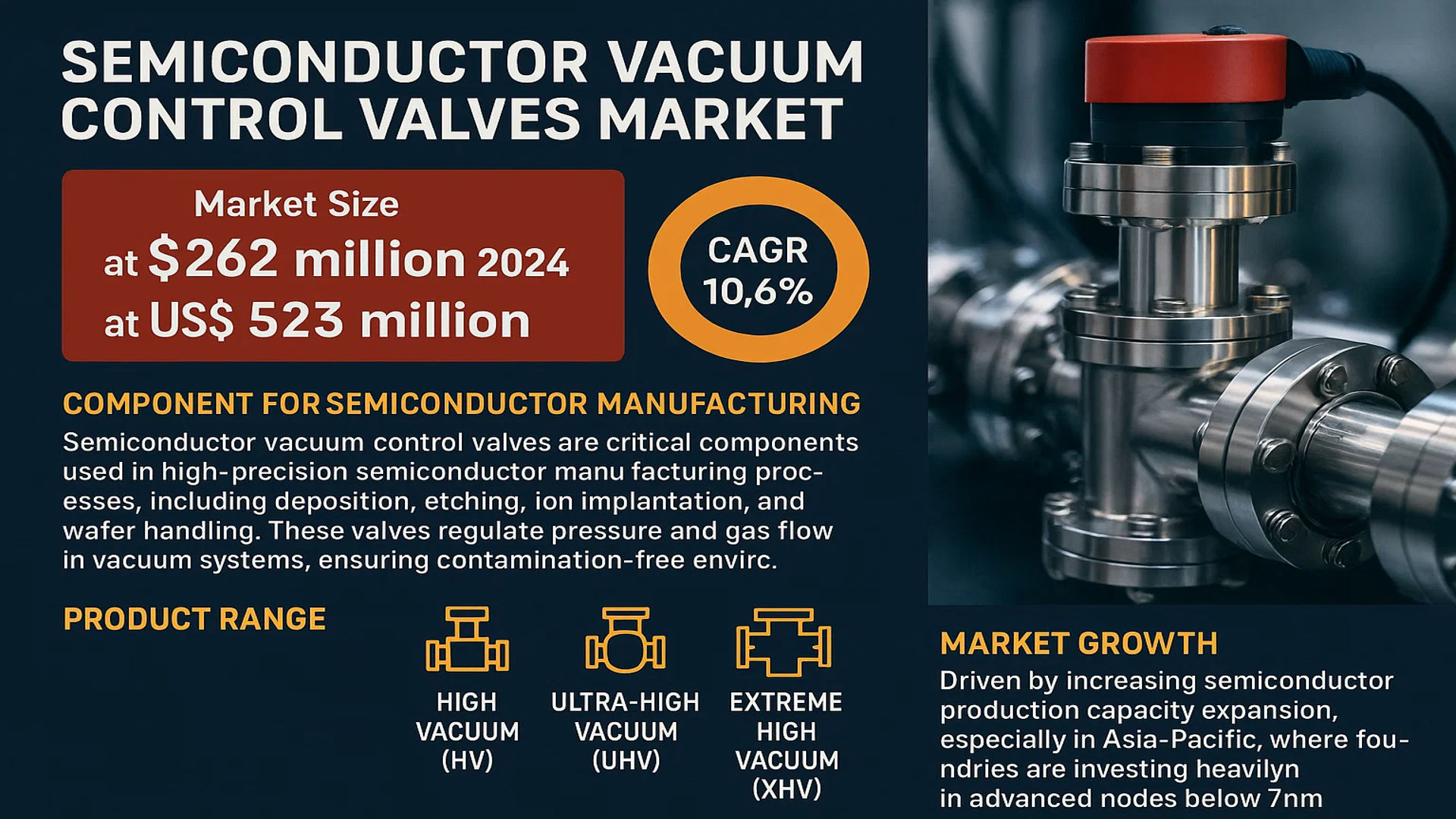

The global Semiconductor Vacuum Control Valves Market was valued at 262 million in 2024 and is projected to reach US$ 523 million by 2032, at a CAGR of 10.6% during the forecast period.

Semiconductor vacuum control valves are critical components used in high-precision semiconductor manufacturing processes, including deposition, etching, ion implantation, and wafer handling. These valves regulate pressure and gas flow in vacuum systems, ensuring contamination-free environments essential for chip fabrication. The product range includes high vacuum (HV), ultra-high vacuum (UHV), and extreme high vacuum (XHV) valves, each designed for specific pressure requirements.

The market growth is driven by increasing semiconductor production capacity expansion, particularly in Asia-Pacific, where foundries are investing heavily in advanced nodes below 7nm. While the analog semiconductor segment grew 20.76% in 2022, the overall semiconductor market is projected to reach USD 790 billion by 2029. Major players like VAT Valves, MKS Instruments, and CKD are developing advanced valve technologies to support emerging semiconductor applications in AI chips and advanced packaging.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Semiconductor Manufacturing Capacities to Drive Demand for Vacuum Control Valves

The global semiconductor industry is experiencing unprecedented growth, with capital expenditures expected to surpass $190 billion by 2025 as manufacturers rapidly expand production capacities to meet demand. This expansion directly fuels demand for precision vacuum control valves used in critical semiconductor fabrication processes such as deposition, etching, and wafer handling. The transition to smaller nanometer nodes (below 7nm) requires increasingly sophisticated vacuum control systems capable of maintaining ultra-high vacuum (UHV) environments with precision down to 0.1 mbar. Advanced logic chips and memory devices demand vacuum valve solutions with contamination-free operation and exceptional reliability to minimize wafer defects.

Technological Advancements in Valve Design Boost Market Adoption

Recent innovations in vacuum valve technology are addressing key industry challenges, including improvements in materials (such as high-purity aluminum alloys), leak-proof sealing mechanisms, and integrated sensing capabilities. Modern vacuum valves now incorporate real-time pressure monitoring and AI-enabled predictive maintenance features, reducing unplanned downtime by up to 40% in semiconductor fab operations. The development of all-metal ultra-clean valves has become particularly crucial for extreme ultraviolet (EUV) lithography applications where particle contamination must be minimized at all costs. These technological advancements are making vacuum control valves not just components, but intelligent subsystems that enhance overall yield management.

Government Initiatives and Semiconductor Independence Strategies Create New Growth Avenues

National semiconductor self-sufficiency programs worldwide are accelerating investments in domestic manufacturing capabilities. The CHIPS and Science Act in the United States has committed $52 billion to bolster semiconductor production, while similar initiatives in the EU, China, and Southeast Asia are collectively investing over $100 billion. These programs mandate the establishment of advanced fabrication facilities that require thousands of specialized vacuum valves per facility. The push for localized supply chains is also prompting valve manufacturers to establish production facilities closer to major semiconductor hubs – a trend expected to persist throughout the decade.

MARKET RESTRAINTS

High Development Costs and Extended Qualification Processes Limit Market Entry

The semiconductor vacuum valve market faces significant barriers due to the rigorous qualification requirements and substantial R&D investments needed to meet industry standards. Developing valves for advanced nodes often requires 18-24 months of testing and validation before achieving production qualification, with certification costs frequently exceeding $20 million per valve design. Small and medium manufacturers struggle with these steep barriers while also contending with the compressed technology transition cycles typical in semiconductor manufacturing.

Supply Chain Complexities Create Operational Challenges

The highly specialized nature of vacuum valve manufacturing makes the supply chain particularly vulnerable to disruptions. Critical components like high-purity seals and corrosion-resistant actuators often have lead times exceeding six months. The industry’s shift toward regionalized production introduces additional complexities, requiring manufacturers to qualify multiple suppliers while maintaining strict quality standards. These factors contribute to inventory management challenges that can potentially delay semiconductor equipment deliveries.

Furthermore, the semiconductor industry’s cyclical nature complicates production planning for valve manufacturers, making it difficult to maintain optimal capacity levels during demand fluctuations. This volatility often results in either inventory shortages during upturns or excess capacity during downturns.

MARKET CHALLENGES

Increasing Technical Complexity Pushes Valve Performance Requirements

As semiconductor manufacturing processes advance to 3nm nodes and below, vacuum control systems must meet increasingly stringent requirements. Valves now need to operate reliably under extreme conditions including ultra-high vacuum levels below 10-9 mbar, temperatures up to 450°C, and corrosive process environments. Meeting these demands requires innovations in materials science and precision engineering, with tolerances now measured in microns rather than millimeters. The industry’s transition to multi-patterning techniques further compounds these challenges by requiring valves to maintain stability through thousands of rapid actuation cycles without performance degradation.

Other Technical Challenges

Particulate Contamination Control

Particle generation remains one of the most persistent challenges, with leading fabs requiring valves to maintain particulate counts below 0.1 particles/cm³ at 0.2μm. Achieving this demands exacting surface finish standards and novel material combinations that minimize wear while ensuring chemical compatibility with aggressive process gases.

Thermal Management

The increasing power densities in semiconductor tools create thermal expansion challenges for vacuum valves. Maintaining seal integrity and actuation precision across wide temperature ranges requires innovative thermal compensation designs and advanced materials with carefully engineered coefficients of thermal expansion.

MARKET OPPORTUNITIES

Emerging Semiconductor Applications Create New Market Segments

The rapid growth of specialized semiconductor applications presents significant opportunities for vacuum valve manufacturers. Emerging areas such as silicon photonics, advanced packaging (including 2.5D/3D ICs), and compound semiconductor manufacturing each require customized vacuum solutions. The power semiconductor market alone, driven by electric vehicle adoption, is expected to require 60% more vacuum valves by 2027 compared to current levels. Similarly, the development of quantum computing chips is creating demand for valves capable of maintaining ultra-high vacuum conditions for extended periods with minimal maintenance.

Digitalization and Smart Manufacturing Enable Value-added Services

The integration of Industry 4.0 technologies into vacuum valves unlocks new service-based business models. Smart valves equipped with IoT sensors and predictive maintenance algorithms allow manufacturers to transition from product sales to comprehensive vacuum management solutions. This shift is particularly valuable for semiconductor manufacturers seeking to optimize tool uptime and reduce operating costs. Remote monitoring capabilities and digital twins of vacuum systems are becoming standard expectations, creating opportunities for valve manufacturers to develop recurring revenue streams through data analytics and performance optimization services.

The increasing focus on sustainability also presents opportunities for valve manufacturers to develop energy-efficient solutions that reduce vacuum system power consumption, a significant operational cost in semiconductor fabrication. Advanced pump-valve synchronization systems and improved flow control algorithms can cut energy use by up to 25% in typical vacuum applications.

SEMICONDUCTOR VACUUM CONTROL VALVES MARKET TRENDS

Growing Semiconductor Manufacturing Investments Drive Vacuum Valve Demand

The global semiconductor vacuum control valves market is experiencing robust growth, fueled by increasing investments in semiconductor manufacturing facilities worldwide. With the semiconductor industry projected to reach $790 billion by 2029, growing at a CAGR of 6%, the demand for precision vacuum components has intensified. Semiconductor vacuum valves, critical for maintaining controlled environments during deposition, etching, and wafer handling processes, are seeing particularly strong adoption in Asia-Pacific where over 60% of global semiconductor production occurs. This growth is further accelerated by the industry’s shift toward smaller process nodes below 7nm, which require ultra-high vacuum environments with tighter contamination control standards.

Other Trends

Advancements in Valve Technology for Extreme Environments

Manufacturers are developing valves capable of withstanding extreme high vacuum (XHV) conditions below 10-12 mbar, driven by cutting-edge semiconductor fabrication requirements. New designs incorporating ceramic sealing surfaces and specialized alloys are emerging to meet the durability demands of processes like atomic layer deposition (ALD) and extreme ultraviolet (EUV) lithography. Furthermore, the integration of smart monitoring systems allows real-time performance tracking, predictive maintenance, and automated adjustments to vacuum levels, significantly improving process control and yield rates in semiconductor fabs.

Expansion of Power Semiconductor Production

The rapid growth of electric vehicles and renewable energy systems is driving substantial investments in power semiconductor manufacturing, creating new demand for vacuum control solutions. While traditional logic and memory segments show fluctuating growth patterns, power semiconductor production is expanding at over 15% annually, requiring specialized vacuum systems for silicon carbide and gallium nitride processes. This trend is particularly pronounced in Europe and North America where automotive and industrial applications are pushing innovation in power electronics manufacturing technologies.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Expansion Define the Semiconductor Vacuum Control Valve Market

The global semiconductor vacuum control valve market is characterized by strong competition among established vendors and emerging players, with the top five companies collectively holding approximately 35-40% market share in 2024. The landscape remains semi-consolidated, where major players leverage their technical expertise and global distribution networks while smaller competitors focus on niche applications and regional markets.

VAT Valves currently leads the market with its comprehensive portfolio of high-vacuum and ultra-high-vacuum solutions, particularly favored for advanced semiconductor manufacturing processes. The company’s recent acquisition of a vacuum valve division in 2023 further strengthened its position in the Asian market. Meanwhile, Pfeiffer Vacuum maintains its stronghold in Europe through continuous R&D investments, capturing significant shares in both deposition and etching applications.

Japanese player ULVAC demonstrates remarkable growth momentum, driven by increasing semiconductor equipment production in Asia-Pacific. Their recent introduction of XHV-grade valves with reduced particle generation addresses critical industry demands for contamination control. Similarly, MKS Instruments continues to expand its vacuum solutions segment, integrating advanced IoT capabilities for real-time valve monitoring and predictive maintenance.

Emerging Chinese manufacturers like Sichuan Jiutian Vacuum Technology and Wenzhou Pioneer Valve are accelerating market competition through cost-effective alternatives, particularly in mid-range vacuum applications. However, these players face challenges in matching the reliability standards and technical certifications required for leading-edge semiconductor fabs.

List of Key Semiconductor Vacuum Control Valve Companies Profiled

- VAT Valves (Switzerland)

- Pfeiffer Vacuum (Germany)

- KITZ SCT (Japan)

- V-TEX (Japan)

- CKD Corporation (Japan)

- MKS Instruments (U.S.)

- Kurt J. Lesker Company (U.S.)

- Irie Koken (Japan)

- VACOM GmbH (Germany)

- ULVAC (Japan)

Segment Analysis:

By Type

Ultra-high Vacuum (UHV) Valves Segment Dominates Due to High Demand in Precision Semiconductor Manufacturing

The market is segmented based on type into:

- High Vacuum (HV)

- Ultra-high Vacuum (UHV)

- Extreme High Vacuum (XHV)

- Others

By Application

Deposition Segment Leads as Vacuum Control Valves are Critical for Thin Film Processes

The market is segmented based on application into:

- Deposition

- Etching and Cleaning

- Implantation of Ion

- Handling of Wafers

- Lithography

- Wafer Inspection and Metrology

By Valve Mechanism

Pneumatic Valves Segment Holds Significant Share Due to Reliability in Semiconductor Fab Environments

The market is segmented based on valve mechanism into:

- Manual Valves

- Pneumatic Valves

- Electric Valves

- Others

By Material

Stainless Steel Segment Dominates for Its Corrosion Resistance in Cleanroom Environments

The market is segmented based on material into:

- Stainless Steel

- Aluminum

- Ceramic

- Others

Regional Analysis: Semiconductor Vacuum Control Valves Market

Asia-Pacific

The Asia-Pacific region dominates the global semiconductor vacuum control valves market, accounting for over 45% of the total revenue share in 2024. This leadership stems from the region’s robust semiconductor manufacturing ecosystem, particularly in China, South Korea, Taiwan, and Japan. China, the world’s largest semiconductor equipment consumer, continues to invest heavily in domestic chip production, driving demand for high-performance vacuum valves. Projects like China’s $150 billion semiconductor self-sufficiency initiative accelerate adoption. However, geopolitical tensions and export restrictions on advanced chip technology present challenges. Meanwhile, South Korea’s focus on memory production and Japan’s strength in materials science sustain steady demand. The shift toward 3D NAND and advanced logic nodes further intensifies requirements for ultra-high vacuum (UHV) valves with contamination-free operation.

North America

North America holds 25% market share, led by the U.S. semiconductor equipment sector and R&D initiatives. The CHIPS and Science Act’s $52 billion funding bolsters domestic wafer fab expansion, directly benefiting vacuum valve suppliers. Major OEMs like Applied Materials and Lam Research drive innovation in atomic layer deposition (ALD) and extreme ultraviolet (EUV) lithography, requiring precise vacuum control. Strict ITAR regulations and emphasis on supply chain resilience favor localized production. Canada and Mexico are emerging as secondary markets, though technological maturity lags behind the U.S. A critical challenge is the talent shortage in semiconductor equipment engineering, potentially slowing deployment.

Europe

Europe contributes 18% of global demand, with Germany, France, and the Netherlands as key markets. The EU Chips Act’s €43 billion investment aims to double Europe’s semiconductor market share by 2030, creating opportunities for valve manufacturers serving automotive and industrial IoT applications. Strict REACH regulations push suppliers to develop PFAS-free sealing solutions. Collaborative R&D projects between academic institutions (e.g., IMEC) and industry players accelerate innovations in quantum computing and photonics-compatible vacuum systems. However, high energy costs and fragmented supply chains hinder cost competitiveness against Asian peers.

Middle East & Africa

The MEA region is a nascent but fast-growing market, projected to expand at 12% CAGR through 2032. Saudi Arabia’s $6 billion semiconductor hub under NEOM and Israel’s thriving fabless chip design sector stimulate demand. While vacuum valve adoption remains limited to research labs and small-scale production, investments in compound semiconductors (GaN, SiC) for energy applications show promise. Infrastructure gaps and reliance on imports temper short-term growth, though partnerships with Asian and European suppliers are bridging this divide.

South America

South America accounts for under 5% of global demand, with Brazil leading in microelectronics research. Recent tax incentives for semiconductor equipment imports aim to kickstart local packaging and testing facilities. However, currency instability and lack of wafer fab investments restrict market potential. Most demand stems from maintenance/replacement cycles in legacy industrial systems rather than cutting-edge semiconductor fabs.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Semiconductor Vacuum Control Valves markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (High Vacuum, Ultra-high Vacuum, Extreme High Vacuum), application (Deposition, Etching, Wafer Handling, etc.), and end-user industries.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis.

- Competitive Landscape: Profiles of 15+ leading market participants including VAT Valves, Pfeiffer Vacuum, MKS Instruments, and ULVAC, detailing their market share and strategies.

- Technology Trends: Assessment of emerging vacuum valve technologies, materials innovation, and integration with semiconductor fabrication processes.

- Market Drivers & Restraints: Evaluation of semiconductor industry growth, fab expansions, and supply chain challenges impacting vacuum valve demand.

- Stakeholder Analysis: Strategic insights for valve manufacturers, semiconductor equipment suppliers, and investors in the vacuum technology ecosystem.

The research methodology combines primary interviews with industry experts and analysis of verified market data from semiconductor equipment manufacturers and valve suppliers.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Semiconductor Vacuum Control Valves Market?

-> Semiconductor Vacuum Control Valves Market was valued at 262 million in 2024 and is projected to reach US$ 523 million by 2032, at a CAGR of 10.6% during the forecast period.

Which key companies operate in Global Semiconductor Vacuum Control Valves Market?

-> Leading players include VAT Valves, Pfeiffer Vacuum, KITZ SCT, MKS Instruments, ULVAC, CKD, and Kurt J. Lesker, collectively holding over 60% market share.

What are the key growth drivers?

-> Primary drivers include increasing semiconductor fab investments (global semiconductor market projected to reach USD 790 billion by 2029), advanced node manufacturing requirements, and growth in IoT/5G applications.

Which region dominates the market?

-> Asia-Pacific accounts for 65% of global demand, driven by semiconductor manufacturing hubs in Taiwan, South Korea, China, and Japan.

What are the emerging trends?

-> Emerging trends include smart vacuum valves with IoT connectivity, corrosion-resistant materials for extreme processes, and miniaturized valves for compact semiconductor tools.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...