MARKET INSIGHTS

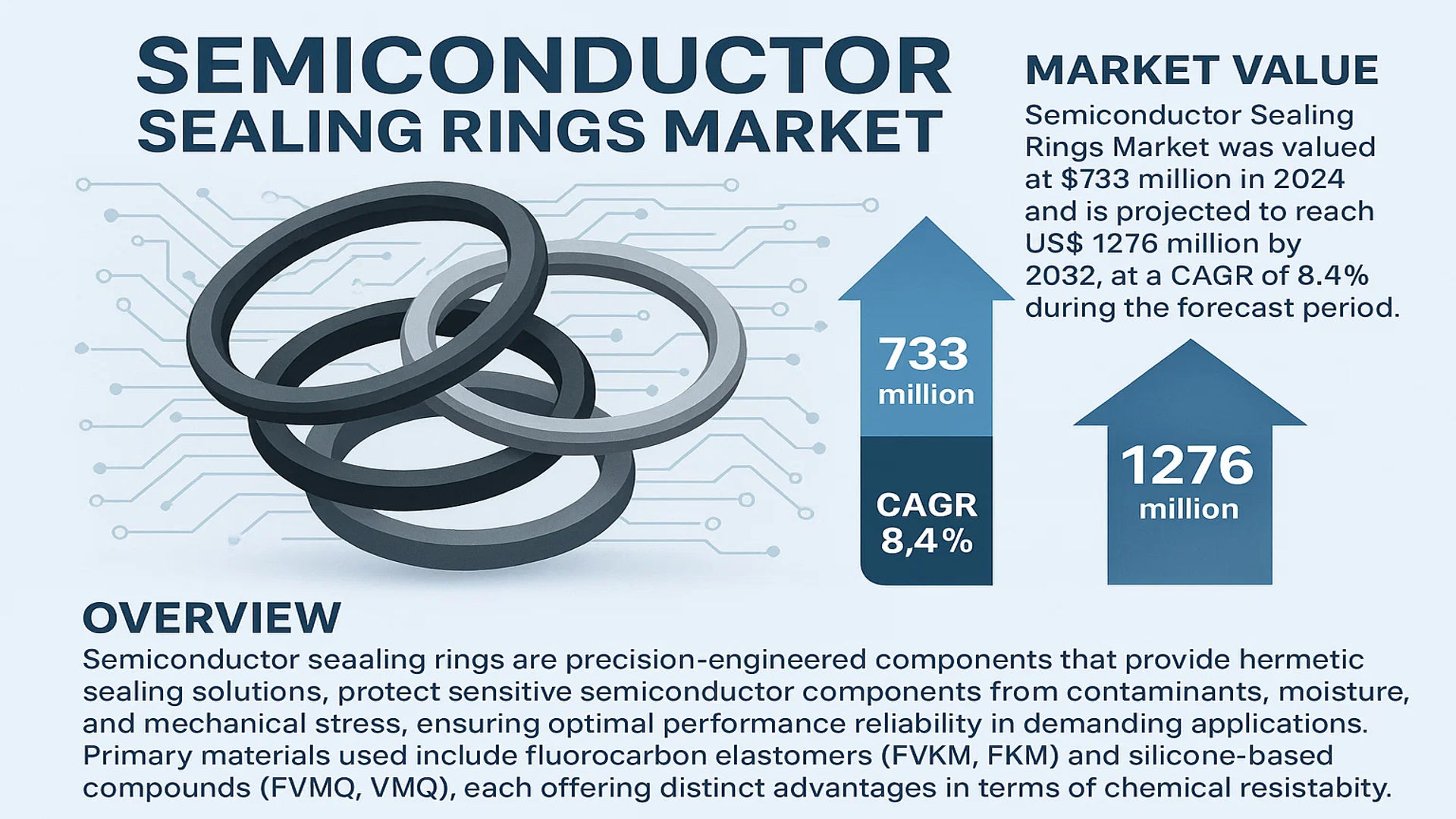

The global Semiconductor Sealing Rings Market was valued at 733 million in 2024 and is projected to reach US$ 1276 million by 2032, at a CAGR of 8.4% during the forecast period.

Semiconductor sealing rings are precision-engineered components that provide hermetic sealing solutions for semiconductor manufacturing equipment and devices. These rings play a critical role in protecting sensitive semiconductor components from environmental contaminants, moisture, and mechanical stress, ensuring optimal performance and reliability in demanding applications. The primary materials used include fluorocarbon elastomers (FFKM, FKM) and silicone-based compounds (FVMQ, VMQ), each offering distinct advantages in terms of chemical resistance, temperature stability, and longevity.

Market growth is being driven by the expanding semiconductor industry, particularly in Asia-Pacific regions, where countries like China, Taiwan, and South Korea are increasing their chip manufacturing capabilities. The shift toward advanced packaging technologies and the miniaturization of semiconductor components are creating higher demand for specialized sealing solutions. Additionally, investments in electric vehicles, 5G infrastructure, and IoT devices are contributing to the market expansion. Key players such as DuPont, Trelleborg, and Parker Hannifin are focusing on developing innovative materials to meet the evolving requirements of semiconductor fabrication processes.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Semiconductor Industry Fuels Demand for High-Performance Sealing Solutions

The global semiconductor industry is experiencing unprecedented growth, with production volumes expected to exceed 1 trillion semiconductor units annually by 2030. This rapid expansion across memory chips, logic devices, and advanced packaging directly correlates with increased demand for reliable sealing components. Sealing rings play a critical role in protecting sensitive semiconductor equipment during fabrication processes such as thermal treatment, plasma etching, and chemical vapor deposition. Leading foundries are expanding production capacity worldwide, with investments exceeding $200 billion in new fabrication facilities expected between 2024-2030.

Material Advancements Enable Broader Application Scope

Recent developments in fluoropolymer and silicone-based materials have revolutionized sealing performance in extreme semiconductor environments. Advanced formulations now withstand temperatures exceeding 300°C while maintaining chemical resistance to aggressive etchants and cleaning solutions. These material innovations allow sealing rings to perform reliably through thousands of process cycles in critical applications. Manufacturers are particularly focused on developing FFKM (Perfluoroelastomer) compounds that combine exceptional purity with extended service life, addressing the semiconductor industry’s need for reduced particle generation and maintenance downtime.

Increasing Process Complexity Demands Enhanced Sealing Solutions

As semiconductor manufacturers transition to advanced nodes below 5nm, process requirements have become significantly more demanding. The introduction of extreme ultraviolet (EUV) lithography and new deposition techniques creates challenging operating conditions where conventional seals fail prematurely. This technological evolution drives adoption of specialized sealing rings designed for ultra-high vacuum environments and plasma-rich processes. Leading equipment manufacturers now specify customized sealing solutions that can maintain integrity under cycling pressures from atmospheric to 10-9 torr while resisting degradation from radical species.

MARKET RESTRAINTS

Premium Material Costs Limit Adoption in Price-Sensitive Segments

While high-performance sealing materials deliver exceptional characteristics, their premium pricing creates adoption barriers, particularly for semiconductor packaging applications where cost pressures are intense. Specialty elastomers like FFKM can cost 5-10 times more than standard FKM materials, leading some manufacturers to compromise on performance for cost savings. This pricing disparity becomes more pronounced in regions where semiconductor component producers operate on thinner margins, forcing sealing ring suppliers to balance material performance with economic viability.

Stringent Certification Requirements Extend Development Timelines

The semiconductor industry maintains rigorous standards for component cleanliness and outgassing characteristics, requiring sealing ring manufacturers to undergo extensive qualification processes. New material formulations often require 12-18 months of testing before gaining approval for use in production environments. These delays can postpone the commercialization of innovative sealing solutions, particularly when dealing with next-generation fab requirements. Additionally, the need for full material traceability and lot-to-lot consistency adds significant compliance costs throughout the supply chain.

Supply Chain Vulnerabilities Impact Material Availability

Specialty polymers used in semiconductor sealing rings face supply constraints due to limited global production capacity and complex manufacturing processes. Recent disruptions in fluoropolymer supply chains have caused lead time extensions exceeding six months for certain high-performance compounds. These challenges are exacerbated by the concentrated nature of raw material suppliers, with three companies controlling over 80% of global FFKM production capacity. Semiconductor equipment makers are increasingly requiring dual sourcing strategies, adding complexity to sealing ring procurement and inventory management.

MARKET CHALLENGES

Miniaturization Trends Test Sealing Performance Limits

As semiconductor feature sizes continue shrinking below 3nm, sealing solutions face unprecedented technical challenges. The industry’s transition to gate-all-around transistor architectures and 3D NAND structures with hundreds of layers requires seals that can prevent contamination at the atomic level. Particulate generation from seal degradation must now be controlled below 0.1 microns, pushing material science to its limits. Furthermore, sealing designs must accommodate increasingly complex chamber geometries without compromising performance, driving innovation in both materials and manufacturing techniques.

Other Challenges

Thermal Cycling Durability

Repeated thermal cycling between extreme temperatures causes progressive seal hardening and eventual failure modes. Advanced nodes require seals to maintain elasticity through 10,000+ cycles between ambient and 300°C operating conditions, with no measurable change in mechanical properties.

Plasma Resistance

High-density plasma environments accelerate seal degradation through both chemical attack and physical sputtering. Developing materials that resist erosion while maintaining low outgassing characteristics presents ongoing formulation challenges for material scientists.

MARKET OPPORTUNITIES

Emerging Packaging Technologies Create New Application Areas

The rapid growth of advanced packaging techniques including chiplet architectures and 3D integration presents significant growth opportunities. These packaging approaches require innovative sealing solutions for hybrid bonding equipment, thermal compression systems, and underfill processes. Specialized seals capable of withstanding the unique combination of mechanical pressure, thermal stress, and chemical exposure in these applications represent a high-growth segment. Equipment manufacturers are increasingly collaborating with seal suppliers to co-develop customized solutions for next-generation packaging lines.

Regional Semiconductor Expansion Drives Localization Strategies

Government initiatives worldwide are driving over $500 billion in semiconductor manufacturing investments, creating opportunities for localized sealing ring production. Markets across North America, Europe, and Asia are establishing domestic supply chains for critical semiconductor components, including specialized sealing solutions. This trend enables sealing ring manufacturers to establish regional technical centers and production facilities closer to emerging fab clusters. Several leading suppliers have announced capacity expansion projects aligned with major semiconductor investment announcements, positioning themselves to serve growing regional demands.

Smart Manufacturing Integration Enhances Value Proposition

The integration of Industry 4.0 technologies into sealing solutions presents new opportunities for value-added services. Advanced sealing rings incorporating embedded sensors can provide real-time data on wear characteristics, temperature profiles, and performance degradation. This predictive maintenance capability helps semiconductor manufacturers optimize process tool uptime and reduce unscheduled maintenance events. Leading suppliers are developing intelligent sealing systems that integrate with equipment health monitoring platforms, creating new service-based revenue models beyond traditional product sales.

SEMICONDUCTOR SEALING RINGS MARKET TRENDS

Growing Demand for High-Performance Sealing Materials Driving Market Expansion

The global Semiconductor Sealing Rings market is witnessing a strong demand surge due to advancements in sealing material technologies. High-performance materials such as FFKM (Perfluoroelastomer) and FKM (Fluoroelastomer) are gaining traction due to their superior resistance to extreme temperatures, aggressive chemicals, and plasma exposure. The market is projected to grow at a CAGR of 8.4% from 2024 to 2032, driven by their increasing adoption in semiconductor manufacturing processes, including thermal and plasma applications. The shift towards miniaturization in semiconductor devices has further amplified the need for reliable, contamination-resistant sealing solutions.

Other Trends

Rise in Semiconductor Manufacturing Investments

Global semiconductor fabrication capacity is expanding rapidly, with new facilities being established across Asia-Pacific, North America, and Europe. This expansion is significantly boosting the demand for sealing rings, particularly in wafer processing and etching applications. Countries like Taiwan, South Korea, and China are at the forefront of semiconductor production, contributing to nearly 65% of global sealing ring consumption in 2024. Meanwhile, government incentives in the U.S. and Europe to strengthen local semiconductor supply chains are expected to further accelerate market growth.

Increasing Focus on Hermetic Sealing in Advanced Packaging

The rise of advanced semiconductor packaging techniques, such as 3D ICs and heterogeneous integration, has intensified the need for hermetic sealing solutions that protect sensitive components from moisture and contaminants. Sealing rings made from materials like FVMQ (Fluorosilicone) and VMQ (Silicone) are particularly sought after in this segment due to their flexibility and durability in high-vacuum environments. With the semiconductor industry shifting towards smaller, more complex node technologies, the demand for precision-engineered sealing solutions continues to climb.

Shift Towards Sustainable Manufacturing Processes

Environmental concerns and regulatory pressures are pushing semiconductor manufacturers to adopt eco-friendly sealing materials with lower environmental impact. Leading suppliers like Trelleborg and DuPont are investing in the development of sealing rings with reduced chemical emissions and improved recyclability. As sustainability becomes a key competitive differentiator, this trend is expected to reshape material preferences and innovation strategies across the semiconductor sealing rings market in the coming years.

COMPETITIVE LANDSCAPE

Key Industry Players

Advanced Material Innovations and Global Presence Drive Market Competition

The global semiconductor sealing rings market is characterized by a fragmented yet competitive landscape, with key players focusing on material innovations, strategic collaborations, and expansion in emerging semiconductor hubs. While established corporations dominate revenue shares, regional specialists maintain strong footholds through application-specific solutions.

DuPont leads the market with its proprietary Kalbion® and Vespel® lines of high-performance sealing materials, particularly in the FFKM segment which constitutes over 35% of industrial applications. Their 2023 acquisition of Rogers Corporation’s elastomer division further strengthened their semiconductor materials portfolio.

Asian manufacturers like NOK Corporation and VALQUA are gaining traction through cost-competitive FKM and FVMQ solutions, capturing nearly 28% of the regional market. Meanwhile, Trelleborg Sealing Solutions maintains technological leadership in plasma-resistant seals, critical for advanced fab processes.

Recent developments highlight increasing vertical integration, with Parker Hannifin launching an end-to-end sealing system for EUV lithography tools, while Daikin Industries expanded its fluoropolymer production capacity by 40% in 2024 specifically for semiconductor applications.

List of Key Semiconductor Sealing Ring Manufacturers

- DuPont de Nemours, Inc. (U.S.)

- NOK Corporation (Japan)

- Trelleborg AB (Sweden)

- VALQUA, Ltd. (Japan)

- Parker Hannifin Corp (U.S.)

- Daikin Industries (Japan)

- Freudenberg Sealing Technologies (Germany)

- Greene Tweed (U.S.)

- Precision Polymer Engineering (IDEX) (UK)

- Shanghai Xinmi Technology (China)

Market competition intensifies as companies develop seals capable of withstanding extreme conditions in next-gen chip manufacturing, where thermal stability above 300°C and chemical resistance become critical differentiators.

Segment Analysis:

By Type

FFKM Segment Leads Due to Superior Chemical and Thermal Resistance in Harsh Semiconductor Environments

The market is segmented based on material type into:

- FFKM (Perfluoroelastomer)

- Key properties: Extreme chemical resistance, high-temperature stability

- FKM (Fluoroelastomer)

- FVMQ (Fluorosilicone)

- VMQ (Silicone)

- Others

By Application

Thermal Process Segment Dominates Due to Expansion of Semiconductor Manufacturing Capabilities

The market is segmented based on application into:

- Thermal Process

- Plasma Process

- Wet Chemical Process

- Others

By End-User

Semiconductor Equipment Manufacturers Represent the Primary Customer Base

The market is segmented based on end-users into:

- Semiconductor Equipment Manufacturers

- Semiconductor Foundries

- IDM (Integrated Device Manufacturers)

- Support Services

By Seal Type

O-Rings Remain the Most Widely Used Configuration in Semiconductor Applications

The market is segmented based on seal configuration into:

- O-Rings

- Custom Molded Seals

- Gaskets

- Other Specialized Configurations

Regional Analysis: Semiconductor Sealing Rings Market

Asia-Pacific

The Asia-Pacific region dominates the semiconductor sealing rings market, accounting for over 45% of global demand due to robust semiconductor manufacturing activities in China, Japan, South Korea, and Taiwan. China’s aggressive semiconductor self-sufficiency policy, including the $143 billion CHIPS Act equivalent, is accelerating local production of critical components like sealing rings. Japan remains a technology leader in high-performance fluoropolymer materials (FFKM/FKM), while Taiwan and South Korea benefit from their established semiconductor fabrication ecosystems. The region’s competitive advantage stems from vertically integrated supply chains and government subsidies supporting material innovation for advanced nodes below 7nm.

North America

North America maintains strong technological leadership in specialized sealing solutions, with the U.S. accounting for 28% of high-end FFKM sealing ring production. Silicon Valley’s R&D ecosystem and Arizona’s expanding semiconductor fabs (e.g., TSMC’s $40 billion investment) drive demand for contamination-resistant seals. Material science innovations from companies like DuPont and Greene Tweed focus on extreme environment applications, including AI/ML chip packaging and quantum computing. However, dependence on Asian manufacturing for standard VMQ/FVMQ rings creates supply chain vulnerabilities addressed through the U.S. CHIPS Act provisions for onshore materials production.

Europe

Europe’s market is characterized by precision engineering, with Germany and Switzerland leading in ultra-clean sealing solutions for semiconductor equipment manufacturers like ASML. Strict EU REACH regulations push adoption of PFAS-free alternatives, particularly in the Benelux and Nordic countries where environmental standards are most stringent. The region specializes in custom-engineered seals for EUV lithography systems, commanding premium pricing. Collaborative R&D initiatives like the European Chips Act allocate €43 billion to strengthen semiconductor sovereignty, including material innovations for next-generation packaging.

South America

The region represents an emerging market with Brazil developing local capabilities in basic VMQ sealing rings for consumer electronics manufacturing. Limited semiconductor infrastructure restricts demand to replacement parts for industrial equipment, though Mexico shows potential as a nearshoring hub for U.S. chipmakers. Challenges include reliance on imported high-performance materials and underdeveloped testing facilities for semiconductor-grade components. Recent trade agreements may facilitate technology transfers, particularly in industrial automation applications.

Middle East & Africa

Market growth is nascent but strategic, with Israel emerging as a niche player in military/aerospace-grade sealing solutions. Saudi Arabia’s $6 billion semiconductor initiative signals long-term potential, though current demand focuses on oil & gas sensor applications. The lack of local material science expertise and semiconductor fabs limits immediate opportunities, but partnerships with Asian and European manufacturers could develop regional capabilities, especially for automotive and renewable energy applications in the GCC countries.

Report Scope

This market research report provides a comprehensive analysis of the global Semiconductor Sealing Rings market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 733 million in 2024 and is projected to reach USD 1,276 million by 2032 at a CAGR of 8.4%.

- Segmentation Analysis: Detailed breakdown by material type (FFKM, FKM, FVMQ, VMQ, Others) and application (Thermal Process, Plasma Process, Wet Chemical Process, Others) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with Asia-Pacific accounting for over 45% market share in 2024.

- Competitive Landscape: Profiles of 20+ leading manufacturers including DuPont, Trelleborg, Parker Hannifin, and Freudenberg, covering their market share, product portfolios, and strategic developments.

- Technology Trends: Analysis of advanced sealing materials like high-performance silicones and fluoropolymers that enhance thermal stability (up to 300°C) and chemical resistance.

- Market Drivers: Evaluation of semiconductor industry growth, increasing fab investments (over USD 500 billion projected by 2030), and demand for reliable component protection.

- Stakeholder Analysis: Strategic insights for material suppliers, OEMs, foundries, and investors regarding supply chain dynamics and emerging opportunities.

The report employs primary interviews with industry leaders and analysis of verified market data from semiconductor equipment manufacturers and material suppliers.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Semiconductor Sealing Rings Market?

-> Semiconductor Sealing Rings Market was valued at 733 million in 2024 and is projected to reach US$ 1276 million by 2032, at a CAGR of 8.4% during the forecast period.

Which key companies operate in this market?

-> Leading players include DuPont, NOK Corporation, Trelleborg, VALQUA, Parker Hannifin, Daikin, and Freudenberg, with the top 5 companies holding 35-40% market share.

What are the key growth drivers?

-> Growth is driven by semiconductor industry expansion, increasing chip fabrication plants, and demand for advanced materials that withstand extreme process conditions.

Which region dominates the market?

-> Asia-Pacific dominates with over 45% share (2024), led by semiconductor manufacturing hubs in China, Taiwan, South Korea and Japan.

What are the emerging material trends?

-> Emerging trends include FFKM materials for extreme conditions, hybrid polymer formulations, and eco-friendly sealing solutions with lower outgassing properties.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...