Semiconductor Sealing O-ring Market Insights

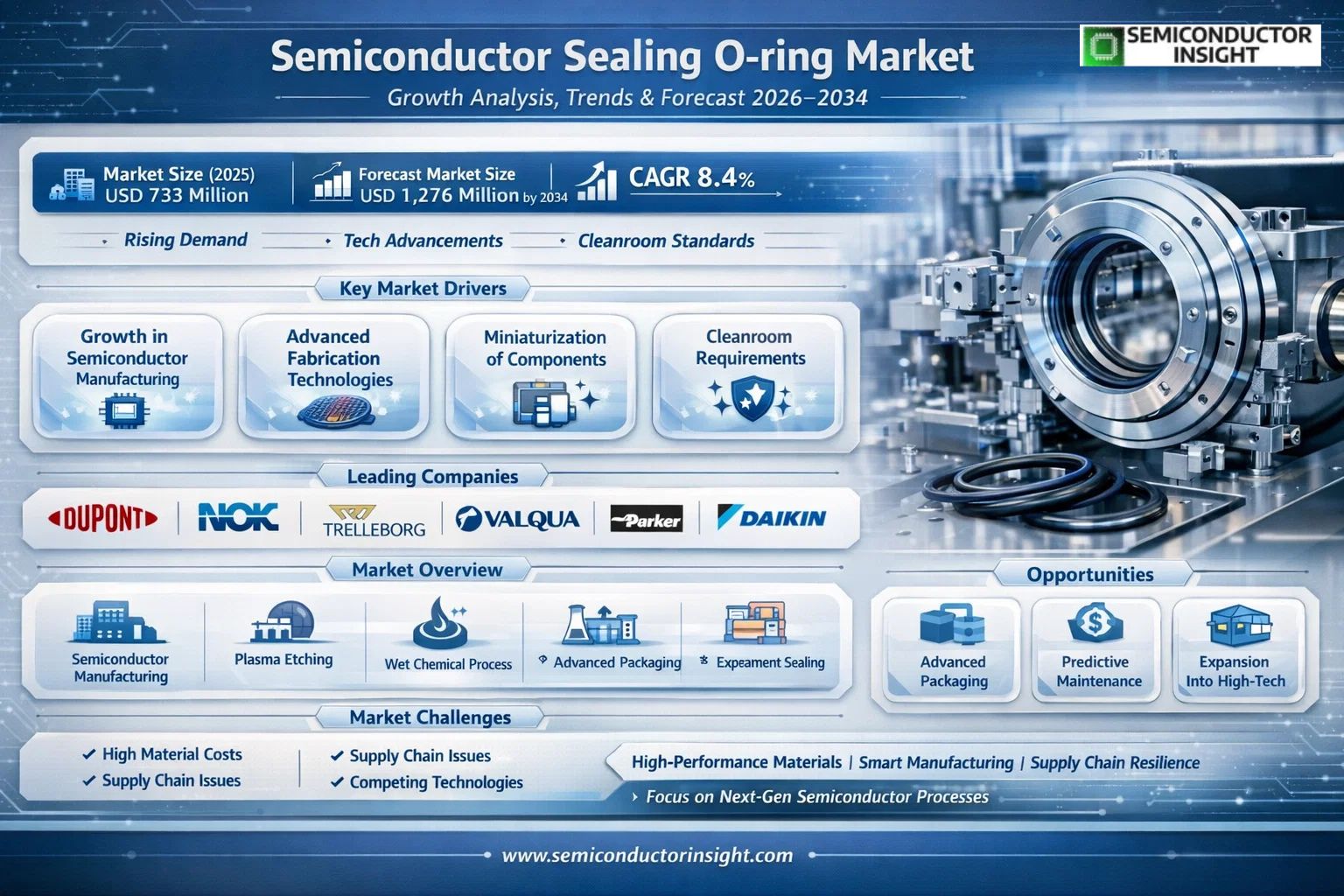

Global Semiconductor Sealing O-ring market size was valued at USD 733 million in 2025. The market is projected to grow from USD 793 million in 2026 to USD 1,276 million by 2034, exhibiting a CAGR of 8.4% during the forecast period.

Semiconductor Sealing O-rings are precision-engineered elastomeric seals critical for maintaining the integrity of semiconductor fabrication equipment. These components are designed to prevent the escape of process gases and fluids, ensure ultra-high vacuum conditions, and protect sensitive processes from particulate and molecular contamination. Key material types include FFKM (Perfluoroelastomer), FKM (Fluoroelastomer), FVMQ (Fluorosilicone), and VMQ (Silicone), each selected for specific chemical resistance and thermal stability properties required in processes like plasma etching, chemical vapor deposition (CVD), and wet cleaning.

The market’s robust growth is primarily driven by the relentless expansion of global semiconductor manufacturing capacity, fueled by demand for advanced electronics, electric vehicles, and AI hardware. This capital expenditure boom necessitates reliable, high-performance sealing solutions. Furthermore, the transition to more advanced process nodes below 7nm and the proliferation of 3D NAND and extreme ultraviolet (EUV) lithography create a need for O-rings that can withstand increasingly aggressive chemistries and higher temperatures. However, growth faces headwinds from the high cost of advanced materials like FFKM and competition from alternative sealing technologies. Recent industry developments include key players expanding their high-purity polymer production capabilities to meet stringent cleanroom standards and mitigate supply chain risks.

MARKET DRIVERS

Robust Demand from Advanced Fabrication Facilities

The relentless construction and operation of new advanced fab facilities, particularly for sub-7nm process nodes, is a primary engine for semiconductor sealing o-ring market. These fabs require thousands of high-purity o-rings for critical gas, chemical, and vacuum systems where any contamination risks billion-dollar production lines. The shift towards extreme ultraviolet (EUV) lithography, which operates under ultra-high vacuum conditions, further intensifies the demand for specialized sealing solutions that can maintain integrity under demanding operational parameters. This technological arms race directly translates into growing consumption rates for high-performance seals.

Stringent Material and Purity Standards

Regulatory and industry standards for contamination control, such as those from SEMI, continuously evolve, mandating the use of higher-grade materials in semiconductor manufacturing. This drives innovation and adoption of advanced perfluoroelastomer (FFKM) and modified fluoroelastomer (FKM) o-rings that offer superior chemical resistance, low outgassing, and ultra-low extractable ion levels. The need to prevent yield loss from metallic or particle contamination compels equipment manufacturers and fabs to specify and procure these premium sealing components, supporting market value growth.

➤ Global push for semiconductor self-sufficiency and the resulting government-backed investments in domestic chip production are creating sustained, long-term demand for the entire semiconductor supply chain, including critical sealing components like o-rings.

Furthermore, the expansion of semiconductor sealing o-ring market is closely tied to the growth in semiconductor packaging and testing, where thermal management and protection from environmental factors during burn-in and testing also rely on reliable elastomeric seals.

MARKET CHALLENGES

Intense Performance Requirements and Material Costs

Developing and manufacturing o-rings that meet the extreme demands of next-generation semiconductor tools presents a significant technical and economic challenge. Formulations must withstand aggressive plasma environments, high temperatures from chamber processes, and corrosive wet chemicals without degrading. The raw materials for high-performance perfluoroelastomers are expensive and complex to process, leading to high unit costs. This creates a persistent challenge for manufacturers to balance performance with cost-effectiveness for high-volume fab adoption.

Other Challenges

Supply Chain and Quality Consistency

Maintaining a resilient and traceable supply chain for specialty polymers is difficult, with geopolitical factors and raw material availability causing volatility. Any batch-to-batch inconsistency in material properties can lead to seal failure, resulting in costly tool downtime and potential wafer scrap, making quality control paramount and challenging.

Competition from Alternative Sealing Technologies

In certain ultra-high vacuum or high-temperature applications within semiconductor equipment, metal seals or bonded seal solutions are sometimes favored over elastomeric o-rings. This competition necessitates continuous innovation in o-ring design and material science to maintain market share in these niche, high-value segments.

MARKET RESTRAINTS

Cyclical Nature of Semiconductor Capital Expenditure

Semiconductor sealing o-ring market is inherently tied to the capital expenditure cycles of chip manufacturers. During periods of oversupply or economic downturn, fab expansion and tool purchases slow dramatically, leading to a direct and pronounced reduction in demand for new sealing components. This cyclicality makes long-term production planning and inventory management challenging for o-ring suppliers, as demand can fluctuate sharply independent of the product’s technical merits. The market’s growth is therefore restrained by these macroeconomic and industry-specific investment cycles.

Prolonged Qualification Processes

The adoption of any new o-ring material or design in a semiconductor fabrication tool is subject to an extensive and costly qualification process that can last over 24 months. Equipment manufacturers (OEMs) and end-user fabs require exhaustive testing for outgassing, chemical compatibility, and long-term reliability under stress. This lengthy timeline acts as a significant barrier to entry for new suppliers and slows the commercialization pace of next-generation sealing solutions, restraining faster market innovation cycles.

MARKET OPPORTUNITIES

Growth in Heterogeneous Integration and Advanced Packaging

The industry trend towards heterogeneous integration and advanced packaging (e.g., 2.5D, 3D ICs) opens new frontiers for semiconductor sealing o-ring market. These processes often involve novel materials, thermal compression bonding, and specialized molding compounds that require seals resistant to different thermal and chemical environments than front-end processes. This creates a demand for application-specific o-ring solutions tailored to packaging and assembly tools, representing a diversified growth avenue beyond traditional wafer fabrication equipment.

Development of Smart and Predictive Maintenance Solutions

Integrating sensor technology or developing o-rings with proprietary tracer elements that enable predictive maintenance is a significant opportunity. Seals that can indicate impending failure through measurable changes in condition (e.g., conductivity, embedded sensors for compression loss) would provide immense value by preventing unplanned tool downtime. This innovation could shift the market from a commodity component model to a value-added, service-oriented solution, enhancing customer loyalty and creating new revenue streams for manufacturers in semiconductor sealing o-ring market.

Expansion into Adjacent High-Tech Manufacturing

The material science and manufacturing expertise developed for semiconductor sealing o-ring market is directly transferable to other high-precision industries. The growing markets for flat panel displays (FPD), micro-electromechanical systems (MEMS), and photovoltaic (PV) cell manufacturing all utilize similar vacuum, chemical delivery, and plasma process tools. This presents a strategic opportunity for market leaders to leverage their technological portfolio and expand their customer base, mitigating the risks associated with semiconductor industry cycles.

Key Semiconductor Sealing O-ring Market Trends

Material Innovation for Extreme Processes

The rapid evolution of semiconductor fabrication technologies is a primary trend shaping semiconductor sealing o-ring market. Advanced manufacturing nodes and complex processes like plasma etching and chemical vapor deposition demand seals with superior chemical resistance and thermal stability. This has accelerated the adoption and development of high-performance elastomers such as FFKM (Perfluoroelastomer) and FKM (Fluoroelastomer). These advanced compounds are engineered to withstand aggressive chemistries, high temperatures, and ultra-high vacuum environments critical for wafer fabrication. The ongoing trend of device miniaturization further intensifies the requirement for precise materials that can maintain integrity under more extreme conditions, while also preventing particle generation that could contaminate the cleanroom environment. This focus on material specificity is a response to the need for longer service life and reduced equipment downtime in semiconductor plants.

Other Trends

Integration with Smart Manufacturing and Sustainability

O-ring suppliers are increasingly integrating their products into predictive maintenance and Industry 4.0 frameworks. This involves developing seals with embedded sensor capabilities or creating digital twins to monitor performance and predict failure. This trend enhances overall equipment efficiency by preventing unplanned downtime and optimizing seal replacement schedules. Concurrently, sustainability initiatives are gaining traction, driven by both regulatory frameworks and corporate responsibility goals. Manufacturers are focusing on improving material efficiency, extending product lifetime to reduce waste, and developing formulations that align with environmental, health, and safety (EHS) standards without compromising on sealing performance in semiconductor sealing o-ring market.

Supply Chain Resilience and Regionalization

Geopolitical dynamics and the push for supply chain security are causing significant shifts in semiconductor sealing o-ring market. Major semiconductor-producing regions, including North America, Europe, and Asia-Pacific, are emphasizing local manufacturing capabilities. This regionalization trend is prompting O-ring suppliers to establish local production and inventory hubs to ensure just-in-time delivery and closer collaboration with semiconductor equipment manufacturers. This move enhances resilience against logistical disruptions and aligns with the broader industry’s strategy for securing critical component supply chains, directly influencing procurement and partnership strategies within the sealing components sector.

COMPETITIVE LANDSCAPE

Key Industry Players

A Market Defined by Specialization and Material Innovation for Ultra-High Purity

Global semiconductor sealing O-ring market is characterized by a competitive mix of large, diversified industrial sealing giants and specialized, technology-focused manufacturers. Leadership is strongly correlated with expertise in high-performance elastomers, particularly perfluoroelastomers (FFKM) and fluoroelastomers (FKM), which are critical for withstanding aggressive chemistries, extreme temperatures, and maintaining vacuum integrity in semiconductor fabrication tools. DuPont, through its Kalrez® brand, and Daikin (with its Dai-El® products) are often viewed as technology and market share leaders in the premium FFKM segment, setting benchmarks for purity and performance. These leaders are complemented by major global sealing suppliers like Trelleborg Sealing Solutions, NOK Corporation, and Parker Hannifin, which leverage broad material portfolios and global distribution to serve a wide range of semiconductor OEMs and end-users. The market structure is moderately consolidated at the high-end but fragmented at the mid-range, with competition intensifying around material science advancements, supply chain reliability, and value-added technical support.

Beyond the top-tier players, a significant number of specialized companies compete effectively in niche applications or regional markets. Firms like Greene Tweed, MFC Sealing Technology, and Precision Polymer Engineering (an IDEX company) are renowned for their engineering capabilities and custom sealing solutions tailored for specific process chambers or wet chemical applications. In Asia, a critical region for semiconductor manufacturing, players such as Shanghai Xinmi Technology (IC Seal), Yoson Seals, and Shenzhen HAO-O have grown substantially by offering cost-competitive, high-quality alternatives and localized support. Other notable participants like VALQUA, Freudenberg Sealing Technologies, and Applied Seals focus on integrating sealing solutions with other critical components, offering system-level value. This diverse ecosystem ensures that semiconductor equipment manufacturers have access to a range of sealing options, from ultra-high-purity, mission-critical seals to reliable, cost-effective solutions for less demanding environments, driving continuous innovation across the supply chain.

List of Key Semiconductor Sealing O-ring Companies Profiled

- DuPont (Kalrez®)

- NOK Corporation

- Trelleborg Sealing Solutions

- VALQUA, Ltd.

- Parker Hannifin Corporation

- Daikin Industries, Ltd. (Dai-El®)

- Freudenberg Sealing Technologies

- Greene Tweed

- Precision Polymer Engineering (PPE) / IDEX

- MFC Sealing Technology (Mikron)

- Shanghai Xinmi Technology (IC Seal)

- Applied Seals

- Maxmold Polymer

- Air Water Mach

- Northern Engineering Sheffield (NES) / Integrated Polymer Solutions

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Perfluoroelastomer (FFKM) represents a critical, high-performance segment driven by its unparalleled chemical resistance and thermal stability in extreme semiconductor fabrication environments. Material superiority ensures long-term reliability in aggressive plasma and high-temperature processes, directly supporting the trend of advanced node manufacturing. Despite higher costs, its adoption is considered essential for preventing contamination and ensuring vacuum integrity in leading-edge foundries, creating a strong value proposition for manufacturers prioritizing yield and equipment uptime. |

| By Application |

|

Plasma Process applications are a dominant and technically demanding segment due to the hostile operating conditions within etching and deposition chambers. This segment demands O-rings with exceptional resistance to reactive gases, high temperatures, and energetic ions. The continuous drive for smaller geometries and more complex chip architectures intensifies the need for seals that maintain ultra-high vacuum integrity without degrading, making material innovation and precision engineering key competitive factors for suppliers targeting this high-value application. |

| By End User |

|

Semiconductor Fabrication Plants (Fabs) constitute the largest consumption base, driven by relentless production scale-up and the critical nature of sealing components as consumables. Fabs prioritize O-ring suppliers that guarantee contamination control, consistent performance, and seamless integration into sensitive cleanroom workflows. This segment exhibits a strong focus on total cost of ownership rather than just initial price, favoring partnerships with suppliers that offer technical support and reliability data to minimize unplanned tool downtime and safeguard production yields. |

| By Material Performance |

|

Ultra-High Purity & Low Outgassing materials are the defining segment for advanced semiconductor manufacturing, where even minute particulate or molecular contamination can ruin entire wafer batches. This performance tier is non-negotiable for leading-edge logic and memory production, pushing suppliers to master specialized compounding and cleaning processes. The segment’s growth is tightly coupled with industry roadmaps requiring stricter contamination controls, creating a high barrier to entry and favoring established, certified suppliers with proven cleanroom manufacturing credentials. |

| By Specification Level |

|

Custom-Engineered solutions are increasingly critical as semiconductor tool designs become more specialized and process windows narrower. This segment involves close collaboration between seal manufacturers and equipment OEMs to develop O-rings with precise dimensions, unique material formulations, or specific certification packages. The value lies in solving unique sealing challenges related to space constraints, new chemistries, or higher pressure regimes, making it a key area for differentiation and building long-term, sticky customer relationships based on deep technical expertise. |

Regional Analysis: Semiconductor Sealing O-ring Market

Asia-Pacific

The region hosts the world’s most concentrated semiconductor manufacturing base. This creates an integrated ecosystem for semiconductor sealing o-ring market, with component production and material formulation facilities strategically located near major fabs. This proximity enables just-in-time delivery and close collaboration on custom sealing specifications for new tool installations and process technologies.

Local manufacturers in semiconductor sealing o-ring market are highly responsive to technological shifts. The drive towards smaller nodes and new materials like high-k dielectrics necessitates O-rings with extreme purity and compatibility. Regional seal developers excel in rapid prototyping and qualification cycles with tool OEMs and chipmakers, fostering a culture of fast-paced innovation.

Demand is multifaceted. Beyond leading-edge logic, semiconductor sealing o-ring market in Asia-Pacific is bolstered by massive investments in memory production, power semiconductors, and outsourced assembly and test (OSAT) facilities. Each segment presents unique sealing challenges, from aggressive chemistries in wafer cleaning to high plasma exposure in etching chambers.

The competitive landscape compels suppliers to exceed baseline quality standards. Success in semiconductor sealing o-ring market here depends on achieving certifications compliant with the strict contamination control protocols of global chipmakers. Suppliers invest heavily in cleanroom manufacturing, material traceability, and lot-to-lot consistency to secure long-term contracts.

North America

The North American Semiconductor Sealing O-ring Market is characterized by high-value, specialized demand driven by R&D-intensive activities and the presence of major fabless semiconductor companies, integrated device manufacturers (IDMs), and leading equipment OEMs. Demand centers on sealing solutions for next-generation process development, pilot production lines, and high-mix, low-volume specialty fabrication. The market dynamics are shaped by a strong focus on intellectual property and partnerships between seal manufacturers and research consortia to develop materials for extreme environments, such as those found in EUV lithography tools. Material innovation for semiconductor sealing o-ring market is a key differentiator, with suppliers often co-engineering elastomer formulations with chipmakers to address new chemical introductions and temperature extremes.

Europe

Europe holds a significant position in semiconductor sealing o-ring market as a center for advanced materials science and precision engineering. Demand is robust from leading capital equipment suppliers for etching, deposition, and lithography systems, which require highly reliable sealing components. The regional market is influenced by stringent environmental and safety regulations, prompting innovation in environmentally benign, long-lasting, and high-performance sealing materials. The presence of key automotive and industrial semiconductor producers also drives steady demand for O-rings used in power module manufacturing and MEMS fabrication. Collaboration between chemical companies specializing in high-purity fluoropolymers and sealing manufacturers strengthens the regional supply chain for semiconductor sealing o-ring market.

South America

semiconductor sealing o-ring market in South America is a developing but growing segment, primarily driven by maintenance, repair, and operations (MRO) demand for existing industrial and legacy semiconductor equipment. The market is more focused on replacement seals and standard products rather than advanced co-development. Growth is linked to the gradual expansion of regional electronics manufacturing and the need for reliable components in related high-tech industries. Suppliers operating here typically distribute products from global manufacturers, with market dynamics emphasizing logistics, pricing, and availability for a diverse range of industrial sealing applications that overlap with semiconductor tool requirements.

Middle East & Africa

This region represents an emerging frontier in Global Semiconductor Sealing O-ring Market, with nascent demand linked to strategic national investments in technology and diversification efforts. Initial demand stems from the establishment of research facilities, pilot plants, and partnerships with international technology firms. The market is currently import-dependent, with dynamics centered on establishing reliable distribution channels and providing technical support for sealing solutions in harsh environmental conditions. Long-term growth potential is tied to the development of local high-tech manufacturing ecosystems and the accompanying need for precision components like Semiconductor Sealing O-rings in supporting infrastructure.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor Sealing O-ring Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- ✅ Market Overview: The report begins with an overview outlining the current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of sealing solutions in powering advancements across the semiconductor manufacturing ecosystem.

- ✅ Market Size & Forecast: Historical data and future projections for revenue (USD Millions) and unit shipments (K Pcs) across major regions and segments, including CAGR analysis.

- ✅ Segmentation Analysis: Detailed breakdown by product Type (e.g., FFKM, FKM, FVMQ, VMQ, Others) and Application (e.g., Thermal Process, Plasma Process, Wet Chemical Process, Others) to identify high-growth segments.

- ✅ Regional Insights: Insights into market performance across North America, Europe, Asia, South America, and the Middle East & Africa, including detailed country-level analysis.

- ✅ Competitive Landscape: Profiles of leading market participants, including their product offerings, market share, and recent developments such as mergers, acquisitions, and partnerships.

- ✅ Technology Trends & Innovation: Assessment of advancements in sealing material technology, fabrication techniques, and evolving industry standards for contamination control.

- ✅ Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges such as material costs, competition, and supply chain dynamics.

- ✅ Stakeholder Insights: Actionable insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving market ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, manufacturers, and suppliers, combined with data from verified sources to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor Sealing O-ring Market?

-> Global Semiconductor Sealing O-ring Market was valued at USD 733 million in 2025 and is projected to reach USD 1276 million by 2034, growing at a CAGR of 8.4% during the forecast period.

Which key companies operate in Semiconductor Sealing O-ring Market?

-> Key players include DuPont, NOK Corporation, Trelleborg, VALQUA, Parker Hannifin, Daikin, Freudenberg, Precision Polymer Engineering (PPE) (IDEX), and Greene Tweed, among others.

What are the key growth drivers?

-> Key growth drivers include growth in semiconductor manufacturing, technological advancements in fabrication, miniaturization of electronic components, increasing demand for cleanroom environments, and environmental regulations promoting sustainable processes.

Which region dominates the market?

-> Asia is a key regional market, driven by major semiconductor manufacturing hubs in countries like China, Japan, South Korea, and Southeast Asia.

What are the emerging trends?

-> Emerging trends focus on the adoption of high-performance materials like FFKM, precision sealing for miniaturized components, and enhanced sealing solutions to meet stringent contamination control standards in advanced semiconductor processes.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...