Semiconductor Recycling Market Insights

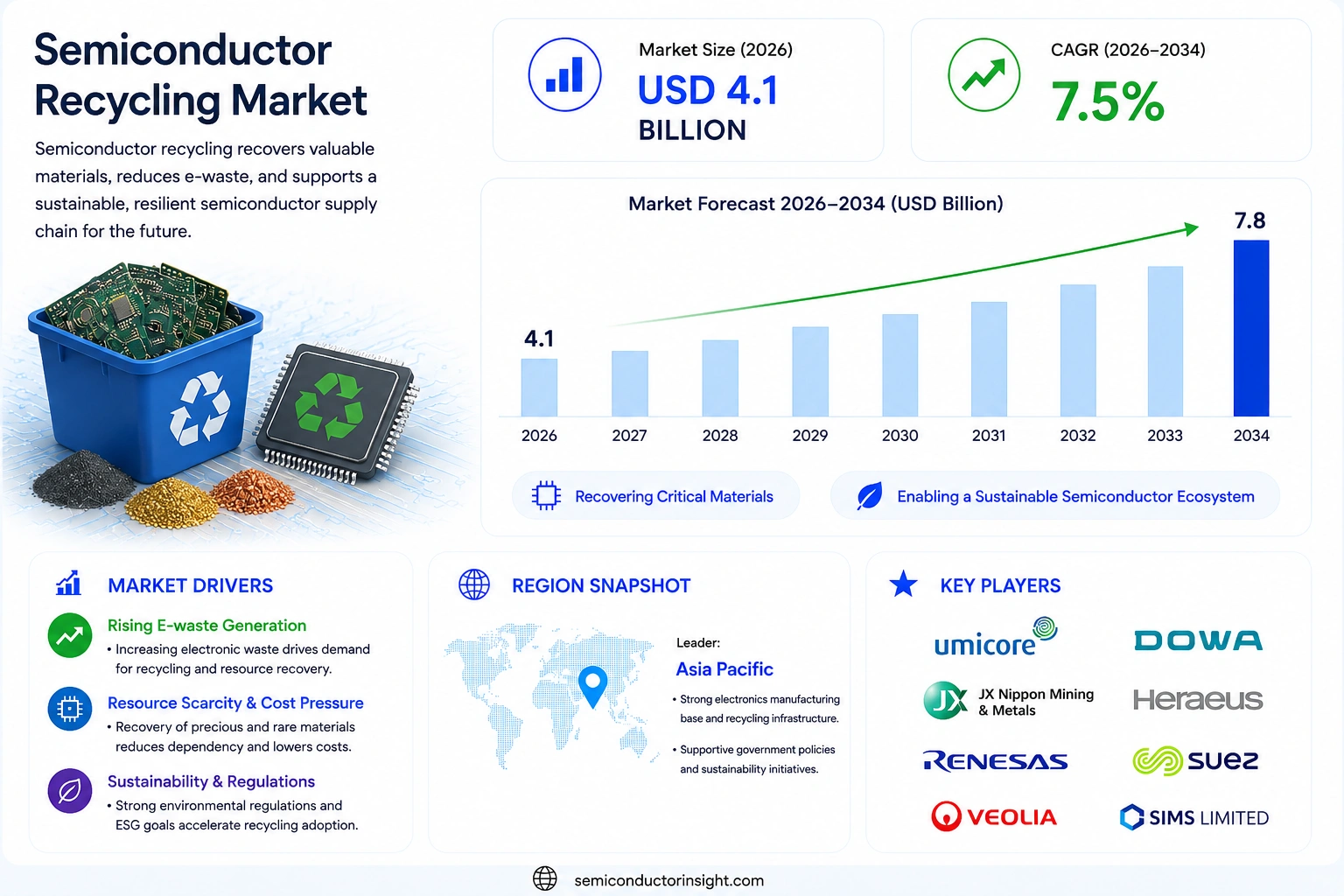

Semiconductor Recycling Market size was valued at USD 3.9 billion in 2025. The market is projected to grow from USD 4.1 billion in 2026 to USD 7.8 billion by 2034, exhibiting a CAGR of 7.5% during the forecast period.

Semiconductor recycling involves the collection, dismantling, and recovery of valuable materials such as silicon wafers, copper, gold, palladium, and rare‑earth elements from end‑of‑life chips and manufacturing scrap. The process restores critical resources for reuse in new device fabrication while reducing hazardous waste.

The market is experiencing rapid growth because stricter e‑waste regulations worldwide are driving manufacturers toward circular‑economy models. Furthermore, the soaring demand for high‑purity metals,especially gold and palladium used in advanced nodes,makes recovery economically attractive. Companies such as Umicore, TES Group, and Dowa Holdings have expanded capacity through recent investments; for example, Umicore announced a joint venture with Intel in March 2024 to upscale reclaimed silicon feedstock production. These initiatives, combined with rising sustainability commitments across the semiconductor supply chain, are fueling market expansion.

MARKET DRIVERS

Rising E‑waste Generation

The global volume of electronic waste surpassed 57 million metric tons in 2022, and semiconductors account for roughly 10 % of this material stream. As device mini‑aturization accelerates, the absolute quantity of recoverable semiconductor components is expanding, creating a clear supply pull for Semiconductor Recycling Market.

Regulatory Incentives

Major economies, including the EU, China, and the United States, have introduced stricter e‑waste directives and extended‑producer‑responsibility (EPR) schemes that mandate the recovery of high‑value materials. These policies are driving manufacturers to invest in dedicated recycling streams to ensure compliance and reduce landfill penalties.

➤ “Circular sourcing of semiconductor-grade silicon reduces the carbon footprint of chip production by up to 30 %, notes a recent industry sustainability forum.

Investment in advanced reverse‑engineering and hydrometallurgical processes is also gaining traction, enabling the extraction of rare‑earth elements with higher purity, thereby reinforcing the economic case for recycling initiatives.

MARKET CHALLENGES

High Collection Costs

Collecting dispersed semiconductor waste from consumer electronics, automotive modules, and industrial equipment incurs significant logistics expenses. The fragmented nature of end‑of‑life (EOL) devices often leads to low fill‑rates in collection bins, inflating per‑ton processing costs for recyclers.

Other Challenges

Technical Complexity

Semiconductor wafers are typically encapsulated within multi‑layered PCBs and polymeric packages. Separating intact dies without damaging functional microstructures requires precision equipment, which heightens capital expenditures and limits scalability.

MARKET RESTRAINTS

Limited Recycling Infrastructure

Only a handful of specialized facilities worldwide are equipped to handle the delicate nature of semiconductor recovery. The scarcity of such plants results in longer lead times and forces many manufacturers to resort to virgin material sourcing, constraining market expansion.

MARKET OPPORTUNITIES

Emerging Urban Mining Initiatives

Cities are launching “urban mining programs that target high‑density electronic waste streams, offering dedicated drop‑off points for semiconductor‑rich devices. These initiatives create a reliable feedstock pipeline, enabling economies of scale and fostering partnerships between municipalities and recycling enterprises.

Furthermore, advances in laser‑based depackaging and low‑temperature chemical leaching promise to lower processing energy requirements, making recycled semiconductor materials increasingly competitive against primary sources.

Semiconductor Recycling Market Trends

Regulatory Pressure Accelerates Circular‑Economy Adoption

Semiconductor Recycling Market is being reshaped by increasingly stringent e‑waste legislation across Europe, North America and parts of Asia. Governments are mandating higher recovery rates for end‑of‑life chips and manufacturing scrap, which forces semiconductor manufacturers to integrate circular‑economy practices into their supply chains. This regulatory environment not only reduces hazardous waste but also creates a predictable demand for recovered high‑purity metals. As a result, companies are investing in dedicated recycling facilities and establishing long‑term contracts with downstream users, ensuring a steady flow of reclaimed silicon, copper, gold, palladium and rare‑earth elements. The trend is further reinforced by corporate sustainability pledges that tie executive compensation to measurable reductions in virgin material consumption.

Other Trends

Material Recovery Innovation

Advances in separation technology are boosting the efficiency of material recovery withSemiconductor Recycling Market. Hydro‑metallurgical processes now achieve gold and palladium purity levels suitable for direct reuse in advanced node fabrication, while mechanical stripping techniques reduce silicon wafer breakage, preserving feedstock quality. In parallel, research into solvent‑based extraction of rare‑earth elements is delivering higher yields with lower energy inputs. These technical improvements lower operating costs and make recycling economically attractive even when commodity prices fluctuate, encouraging more players to enter the value chain.

Strategic Capacity Expansion by Industry Leaders

Major recyclers such as Umicore, TES Group and Dowa Holdings are scaling capacity to meet the heightened demand generated by regulatory and market forces. Umicore’s joint venture with Intel announced in early 2024 expands reclaimed silicon feedstock production, positioning the partnership to supply a significant share of future wafer requirements. TES Group has opened a new plant in Southeast Asia focused on high‑throughput gold recovery, while Dowa Holdings is upgrading its rare‑earth extraction lines to support next‑generation semiconductor designs. These investments, combined with broader sustainability commitments across the semiconductor supply chain, are solidifying the market’s transition from niche service to a core component of device manufacturing.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Recycling Market is characterized by a concentrated group of established material recovery specialists, e-waste processors, and vertically integrated smelters competing across silicon wafer reclamation, precious metal recovery, and hazardous waste management segments.

Semiconductor Recycling Market is dominated by a handful of large-scale integrated recyclers and precious metal refiners that have built significant competitive moats through proprietary hydrometallurgical and pyrometallurgical processing capabilities. Umicore S.A. stands as one of the most prominent players in this space, leveraging its advanced integrated smelting and refining operations to recover high-purity gold, palladium, copper, and other critical materials from end-of-life semiconductors and manufacturing scrap. The company further strengthened its market position through a joint venture with Intel announced in March 2024, aimed at upscaling reclaimed silicon feedstock production. Dowa Holdings, a Japan-based metals recycler, similarly commands a strong regional presence in Asia, supported by decades of expertise in non-ferrous metal recovery from electronic waste streams. TES Group has also expanded its global semiconductor recycling capacity through strategic facility investments, positioning itself as a leading end-to-end e-waste and semiconductor materials recovery operator across Europe and Asia-Pacific. These tier-one players benefit from economies of scale, regulatory compliance infrastructure, and long-term supply agreements with leading semiconductor original equipment manufacturers (OEMs), making market entry increasingly challenging for smaller competitors.

Beyond the dominant tier-one operators, the semiconductor recycling competitive landscape includes a diverse set of niche players and regional specialists that focus on specific material streams or geographies. Companies such as Sims Limited and Boliden AB have carved out meaningful positions by integrating semiconductor scrap recycling into broader electronic waste and base metals recovery platforms. Meanwhile, specialized silicon wafer reclaim service providers such as NOVA Electronic Materials and Pure Wafer (now part of Entegris) serve semiconductor fabrication facilities directly by refurbishing used wafers for reuse in device manufacturing, reducing raw material consumption across the supply chain. Korean operators including Youngpoong Corporation and LS-Nikko Copper have expanded precious metal recovery operations targeting semiconductor manufacturing residues generated by the country’s large-scale chip fabrication industry. As sustainability mandates and circular-economy commitments intensify across the global semiconductor supply chain, these niche and mid-tier recyclers are increasingly forming partnerships with fabless chip designers, foundries, and contract manufacturers to secure consistent feedstock volumes, creating a more competitive and dynamic market structure.

List of Key Semiconductor Recycling Companies Profiled

- Umicore S.A.

- Dowa Holdings Co., Ltd.

- TES Group

- Sims Limited

- Boliden AB

- NOVA Electronic Materials, LLC

- Pure Wafer (Entegris, Inc.)

- Youngpoong Corporation

- LS-Nikko Copper Inc.

- Heraeus Holding GmbH

- Aurubis AG

- Electronic Recyclers International (ERI)

- Stena Metall Group

- Global Electric Electronic Processing (GEEP)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Integrated Circuits are the primary focus of recycling efforts because they contain dense concentrations of high‑value metals and silicon.

|

| By Application |

|

Consumer Electronics drive recycling demand due to frequent product refresh cycles and high volumes of end‑of‑life devices.

|

| By End User |

|

Semiconductor Manufacturers are positioned as the leading end‑user segment, integrating reclaimed feedstock into new wafer production.

|

| By Material |

|

Precious Metals dominate material‑focused recycling because of their critical role in high‑performance circuitry.

|

| By Process |

|

Hydrometallurgical Recovery is recognized as the leading process due to its ability to selectively extract high‑purity metals while minimizing environmental impact.

|

Regional Analysis: North America

The North American Semiconductor Recycling Market is heavily influenced by environmental regulations at both federal and state levels. These regulations mandate responsible e-waste management and promote the recovery of valuable materials. Compliance with these rules is a critical aspect of business operations for all players in the market.

Innovation in semiconductor recycling technologies is a key driver of market growth in North America. Advancements in automated dismantling processes, hydrometallurgy, and pyrometallurgy are improving the efficiency and effectiveness of material recovery. Investment in these technologies is crucial for meeting the growing demand and maximizing resource utilization.

The semiconductor recycling supply chain in North America involves collection, transportation, processing, and refining of materials. Establishing a robust and efficient supply chain is essential for ensuring the smooth functioning of the market. Collaboration among stakeholders across the value chain is crucial for optimizing resource flows and minimizing environmental impact.

Key drivers for the North American Semiconductor Recycling Market include the increasing volume of electronic waste, the scarcity of critical materials, and the growing emphasis on sustainability and circular economy practices within the semiconductor industry.

Europe

The European Semiconductor Recycling Market is characterized by a strong commitment to environmental sustainability and a well-established regulatory framework. The European Union’s WEEE (Waste Electrical and Electronic Equipment) Directive and RoHS (Restriction of Hazardous Substances) Directive drive the collection and responsible management of electronic waste, including semiconductor devices. The region is witnessing a growing focus on closed-loop recycling systems and the recovery of valuable materials to reduce reliance on primary resources. Business strategies in Europe emphasize innovation in recycling technologies, collaboration among stakeholders, and adherence to stringent environmental standards.

Asia-Pacific

Asia-Pacific is the largest semiconductor manufacturing hub globally, and consequently, a significant generator of semiconductor waste. The market in this region is characterized by rapid growth and increasing demand for advanced recycling solutions. Countries like China, Japan, and South Korea are driving the market through investments in R&D and the implementation of stricter environmental regulations. The focus is on developing cost-effective and efficient recycling processes to manage the growing volume of semiconductor waste. Business strategies in Asia-Pacific emphasize capacity building, technological upgrades, and establishing robust regulatory frameworks.

South America

Semiconductor Recycling Market in South America is still in its nascent stages but is expected to witness significant growth in the coming years. The increasing adoption of electronics and the growing awareness of e-waste management issues are driving market demand. Challenges include limited infrastructure and regulatory frameworks, but opportunities exist for companies to establish recycling facilities and develop sustainable solutions. Focus is shifting towards establishing collection networks and developing partnerships with semiconductor manufacturers.

Middle East & Africa

Semiconductor Recycling Market in the Middle East & Africa is relatively small but has significant potential for growth. The increasing investments in technology and infrastructure in the region are leading to a rise in electronic waste generation. While regulatory frameworks are still developing, there is a growing awareness of the need for responsible e-waste management. Opportunities exist for recycling companies to establish operations and cater to the growing demand for environmentally sound solutions.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor Recycling Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor Recycling Market?

-> Semiconductor Recycling Market was valued at USD 3.9 billion in 2025 and is expected to reach USD 7.8 billion by 2034. The forecast CAGR is 7.5% during the period.

Which key companies operate Semiconductor Recycling Market?

-> Key players include Umicore, TES Group, Dowa Holdings, Intel, among others.

What are the key growth drivers?

-> Key growth drivers include stricter e‑waste regulations, rising demand for high‑purity metals such as gold and palladium, and increased sustainability commitments across the semiconductor supply chain.

Which region dominates the market?

-> The reference does not specify a dominant region; market expansion is driven globally by regulatory pressure and material demand.

What are the emerging trends?

-> Emerging trends include circular‑economy recycling models, joint‑venture initiatives such as the Umicore‑Intel partnership, and heightened recovery of high‑purity metals for advanced node manufacturing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...