Semiconductor Rare Earth Materials Market Insights

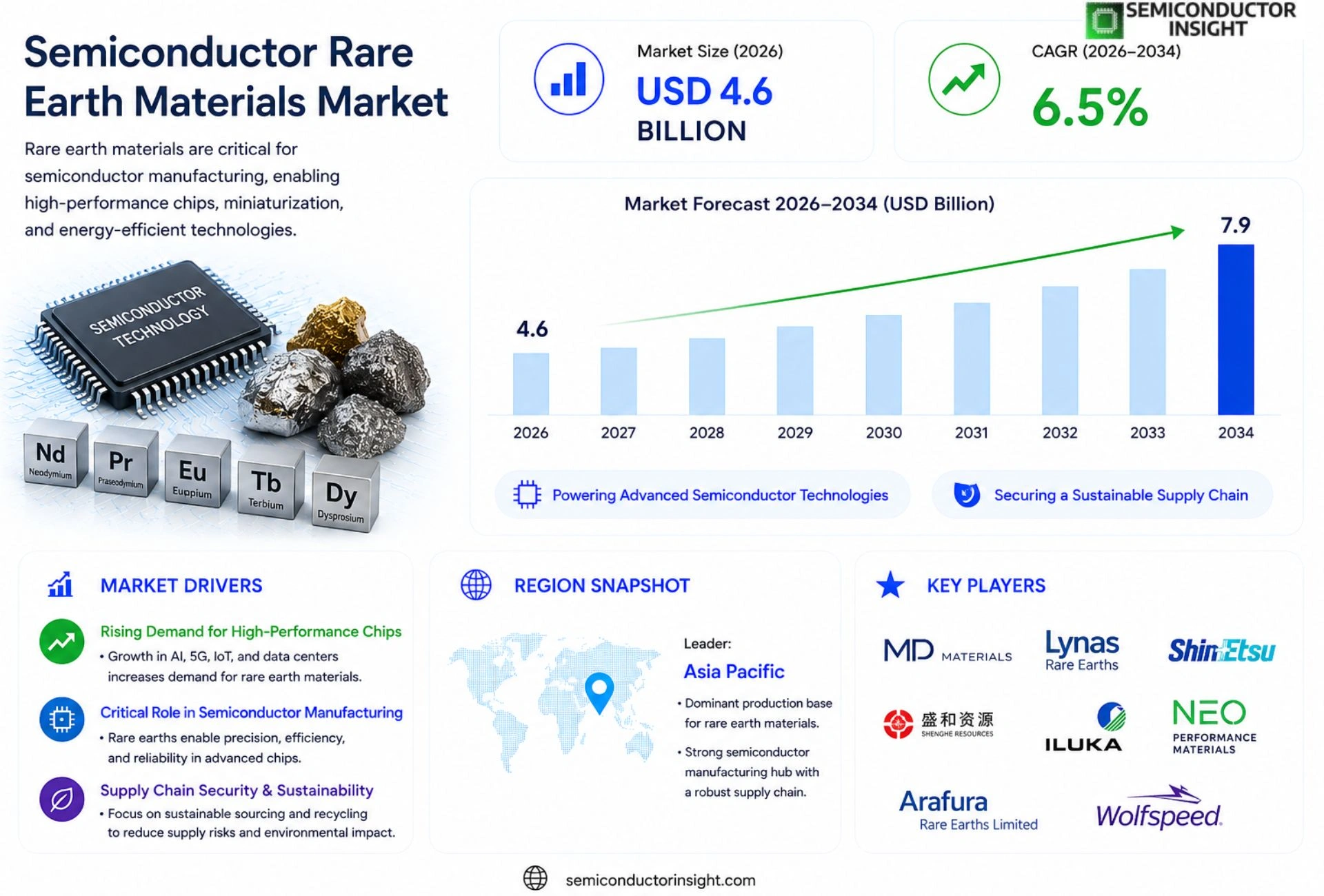

Global Semiconductor Rare Earth Materials Market size was valued at USD 4.3 billion in 2025. The market is projected to grow from USD 4.6 billion in 2026 to USD 7.9 billion by 2034, exhibiting a CAGR of 6.5% during the forecast period.

Semiconductor rare earth materials comprise high‑purity neodymium, dysprosium, terbium, and yttrium compounds used in magnetic thin films, substrate doping, and optical coatings that enable advanced logic chips, power‑electronics, and photonic devices. Their unique magnetic and optical properties allow miniaturization and efficiency gains in next‑generation semiconductors.

The market is accelerating because demand for AI‑driven data centers and electric‑vehicle power modules is surging, while supply constraints are easing as new mining projects in China and Australia come online. Furthermore, government incentives for domestic rare‑earth processing and collaborations between chipmakers such as Intel and material suppliers are driving adoption.

MARKET DRIVERS

Increasing Demand for High‑Performance Electronics

Semiconductor Rare Earth Materials Market is being propelled by a surge in demand for faster, smaller, and more energy‑efficient devices. Rare‑earth dopants such as europium and terbium enable higher electron mobility, which is essential for next‑generation smartphones, data‑center processors, and automotive infotainment systems. Industry analysts forecast a compound annual growth rate of roughly 6% through 2030, reflecting the expanding role of these materials in advanced semiconductor architectures.

Shift Toward Sustainable Manufacturing

Manufacturers are increasingly adopting circular‑economy practices, recycling rare‑earth elements from end‑of‑life electronics to reduce environmental impact. This sustainability push not only lowers raw‑material waste but also strengthens the supply base, giving companies a competitive edge Semiconductor Rare Earth Materials Market. Green‑process initiatives are expected to add approximately 2‑3 percentage points to annual market growth.

➤ Integrating rare‑earth dopants can boost transistor switching speed by up to 15%, delivering tangible performance gains for high‑frequency applications.

Overall, the convergence of performance‑driven demand, regulatory incentives for greener production, and ongoing R&D investments creates a robust foundation for Semiconductor Rare Earth Materials Market to expand across multiple high‑tech sectors.

MARKET CHALLENGES

Supply Chain Volatility

Geopolitical tensions and export restrictions on rare‑earth ores have introduced significant uncertainty into Semiconductor Rare Earth Materials Market. Limited mining capacity outside of a few dominant regions leads to price spikes, which can erode profit margins for semiconductor manufacturers relying on steady material flows.

Other Challenges

Geopolitical Constraints

Countries that control rare‑earth mining are tightening export controls, prompting manufacturers to diversify sourcing strategies. This diversification process involves higher logistics costs and longer lead times, further complicating supply chain resilience.

MARKET RESTRAINTS

High Material Costs

Rare‑earth elements command premium prices due to the intensive extraction and refining processes required. The elevated cost structure acts as a restraint on Semiconductor Rare Earth Materials Market, especially for cost‑sensitive segments such as consumer electronics, where price competitiveness remains a critical factor.

MARKET OPPORTUNITIES

Emerging Applications in Quantum Computing

Quantum processors rely on precise control of electron spin states, a capability enhanced by rare‑earth materials with unique magnetic properties. This creates a high‑growth niche withSemiconductor Rare Earth Materials Market, as research institutions and technology firms invest heavily in quantum‑ready semiconductor platforms.

Semiconductor Rare Earth Materials Market Trends

AI‑Driven Data Center Expansion Drives Rare‑Earth Demand

Semiconductor Rare Earth Materials Market is experiencing a sharp uptick as AI‑driven data centers require higher‑performance logic chips. Increased power density and thermal‑management constraints push designers toward magnetic thin‑film layers that rely on high‑purity neodymium and dysprosium. Simultaneously, electric‑vehicle power modules benefit from rare‑earth‑based substrate doping that improves efficiency. The unique optical properties of terbium and yttrium compounds also enable photonic interconnects that reduce latency in AI accelerator modules. While demand has accelerated, supply constraints are beginning to ease because new mining projects in China and Australia have reached commercial production. This balance of rising consumption and expanding supply creates a favorable environment for market participants and supports the projected growth through 2034.

Other Trends

Geopolitical Supply Dynamics

Recent policy shifts in China and Australia have increased the availability of high‑purity rare‑earth ores, directly influencing Semiconductor Rare Earth Materials Market. Government incentives for domestic processing aim to reduce reliance on export‑controlled sources, encouraging the establishment of recycling facilities in Europe and North America. These initiatives improve material security for chipmakers and lower logistics costs for end‑users. At the same time, trade discussions between major economies are facilitating joint research programs that focus on alternative extraction techniques, further diversifying the supply base and mitigating geopolitical risk.

Emerging Chip‑Material Partnerships

Strategic collaborations between leading semiconductor manufacturers and rare‑earth suppliers are accelerating technology adoption. Companies such as Intel have entered multi‑year agreements with material producers to co‑develop magnetic thin‑film processes optimized for next‑generation logic nodes. These partnerships streamline qualification cycles, reduce time‑to‑market, and create a feedback loop that drives both material performance improvements and circuit design innovations. As the ecosystem matures, Semiconductor Rare Earth Materials Market is poised to sustain its momentum, delivering higher efficiency and miniaturization for future electronic systems.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Positioning and Market Dynamics in the Global Semiconductor Rare Earth Materials Industry

The global Semiconductor Rare Earth Materials Market is characterized by a moderately consolidated competitive structure, with a handful of large-scale integrated producers commanding significant market share alongside a growing number of specialized material suppliers. China Northern Rare Earth Group stands as the dominant force in the industry, leveraging its vertically integrated operations spanning mining, separation, and high-purity compound refining to supply neodymium, dysprosium, terbium, and yttrium compounds critical to advanced logic chips and power-electronics applications. The company’s scale and proximity to primary ore deposits in Inner Mongolia afford it a substantial cost advantage that remains difficult for non-Chinese producers to replicate in the near term. MP Materials, the largest rare earth producer in the United States, has emerged as a strategic counterweight, supported by federal incentives and long-term supply agreements with domestic chipmakers and defense contractors. Lynas Rare Earths of Australia further reinforces the ex-China supply chain through its Mount Weld mining operations and Malaysian separation facility, positioning itself as a preferred partner for semiconductor manufacturers seeking geopolitically diversified sourcing. Collectively, these three companies define the upper tier of the competitive landscape and are central to government-backed initiatives aimed at reducing dependence on single-source supply chains.

Beyond the leading players, a number of niche but strategically significant companies contribute specialized capabilities across processing, purification, and application-specific material development. Shin-Etsu Chemical and TDK Corporation of Japan supply ultra-high-purity rare earth compounds and rare earth permanent magnet materials tailored for thin-film deposition and photonic device manufacturing. Neo Performance Materials, headquartered in Canada, operates rare earth separation and alloying facilities across Europe and Asia, serving semiconductor substrate doping and optical coating segments. Solvay of Belgium brings advanced chemical processing expertise to rare earth purification for next-generation semiconductor applications. Energy Fuels Inc. is expanding its rare earth separation capabilities in the United States, targeting domestic supply for the growing electric-vehicle power module and AI data center segments. Vital Metals of Australia and Pensana Rare Earths are advancing upstream mining and early-stage processing projects that are expected to contribute incremental supply to the market through the forecast period. Meanwhile, Ucore Rare Metals is developing proprietary separation technology aimed at delivering high-purity rare earth oxides for semiconductor-grade end uses, and Arafura Rare Earths is progressing its Nolans Project in Australia as a future source of separated rare earth products for the global technology supply chain.

List of Key Semiconductor Rare Earth Materials Companies Profiled

- China Northern Rare Earth Group

- MP Materials Corp.

- Lynas Rare Earths Ltd.

- Shin-Etsu Chemical Co., Ltd.

- TDK Corporation

- Neo Performance Materials Inc.

- Solvay S.A.

- Energy Fuels Inc.

- Vital Metals Ltd.

- Pensana Rare Earths plc

- Ucore Rare Metals Inc.

- Arafura Rare Earths Ltd.

- China Minmetals Rare Earth Co., Ltd.

- Grirem Advanced Materials Co., Ltd.

- Stanford Advanced Materials

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Neodymium‑based Materials

|

| By Application |

|

Magnetic Thin Films

|

| By End User |

|

Semiconductor Manufacturers

|

| By Material |

|

High‑Purity Alloys

|

| By Functional Role |

|

Miniaturization Enabler

|

Regional Analysis: North America

The US Semiconductor Rare Earth Materials Market is characterized by a complex supply chain involving mining, processing, and integration into semiconductor manufacturing. Geopolitical factors and logistical challenges can significantly impact the availability and cost of these crucial materials.

Ongoing research and development efforts are focused on finding alternative materials and improving the efficiency of rare earth element utilization in semiconductor applications. This includes exploring new extraction methods and developing more sustainable chemical processes.

Significant investments are being directed towards strengthening domestic rare earth material production and processing capabilities within the United States. These investments are aimed at ensuring a stable and secure supply for the rapidly growing semiconductor industry.

Government regulations concerning the mining, processing, and import of rare earth materials play a crucial role in shaping the market dynamics. Compliance with environmental and safety standards is a key consideration for businesses operating in this sector.

Europe

Europe presents a dynamic and strategically important region withSemiconductor Rare Earth Materials Market. With a strong emphasis on technological innovation and sustainable development, European nations are actively working to secure their access to critical materials. The region’s advanced manufacturing base, particularly in countries like Germany, France, and the Netherlands, drives significant demand for high-purity rare earth elements used in semiconductor production. Initiatives such as the European Chips Act are aimed at bolstering domestic semiconductor manufacturing and establishing resilient supply chains. Collaboration between European countries and international partners is crucial for ensuring a stable supply of these materials. The focus on circular economy principles and responsible sourcing is also gaining traction, influencing business practices and investment decisions.

Asia-Pacific

Asia-Pacific is the dominant force in the global Semiconductor Rare Earth Materials Market, driven by the presence of major semiconductor manufacturers and a rapidly expanding electronics industry. Countries like China, Japan, South Korea, and Taiwan are key players in the production and consumption of these materials. China currently holds a significant share in the rare earth mining and processing industry, but other nations are investing in domestic capabilities to reduce dependence. The region’s strong manufacturing ecosystem and robust R&D infrastructure support continuous innovation and technological advancements in semiconductor materials. However, geopolitical tensions and trade dynamics pose challenges to the region’s supply chains.

South America

South America represents a smaller but growing market for Semiconductor Rare Earth Materials. Countries with emerging electronics industries and increasing investments in technology are driving demand. While the region has some rare earth reserves, the development of mining and processing infrastructure is still in its early stages. Opportunities exist for international suppliers to establish partnerships and supply chains in this region.

Middle East & Africa

The Middle East and Africa represent relatively nascent markets for Semiconductor Rare Earth Materials, but with significant growth potential in the coming years. Increasing investments in technology and infrastructure development, particularly in countries like Saudi Arabia and South Africa, are driving demand for these materials. The region’s rare earth resources are largely untapped, presenting opportunities for exploration and development.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor Rare Earth Materials Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor Rare Earth Materials Market?

-> Semiconductor Rare Earth Materials Market size was valued at USD 4.3 billion in 2025. The market is projected to grow from USD 4.6 billion in 2026 to USD 7.9 billion by 2034, exhibiting a CAGR of 6.5%.

Which key companies operate Semiconductor Rare Earth Materials Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...