MARKET INSIGHTS

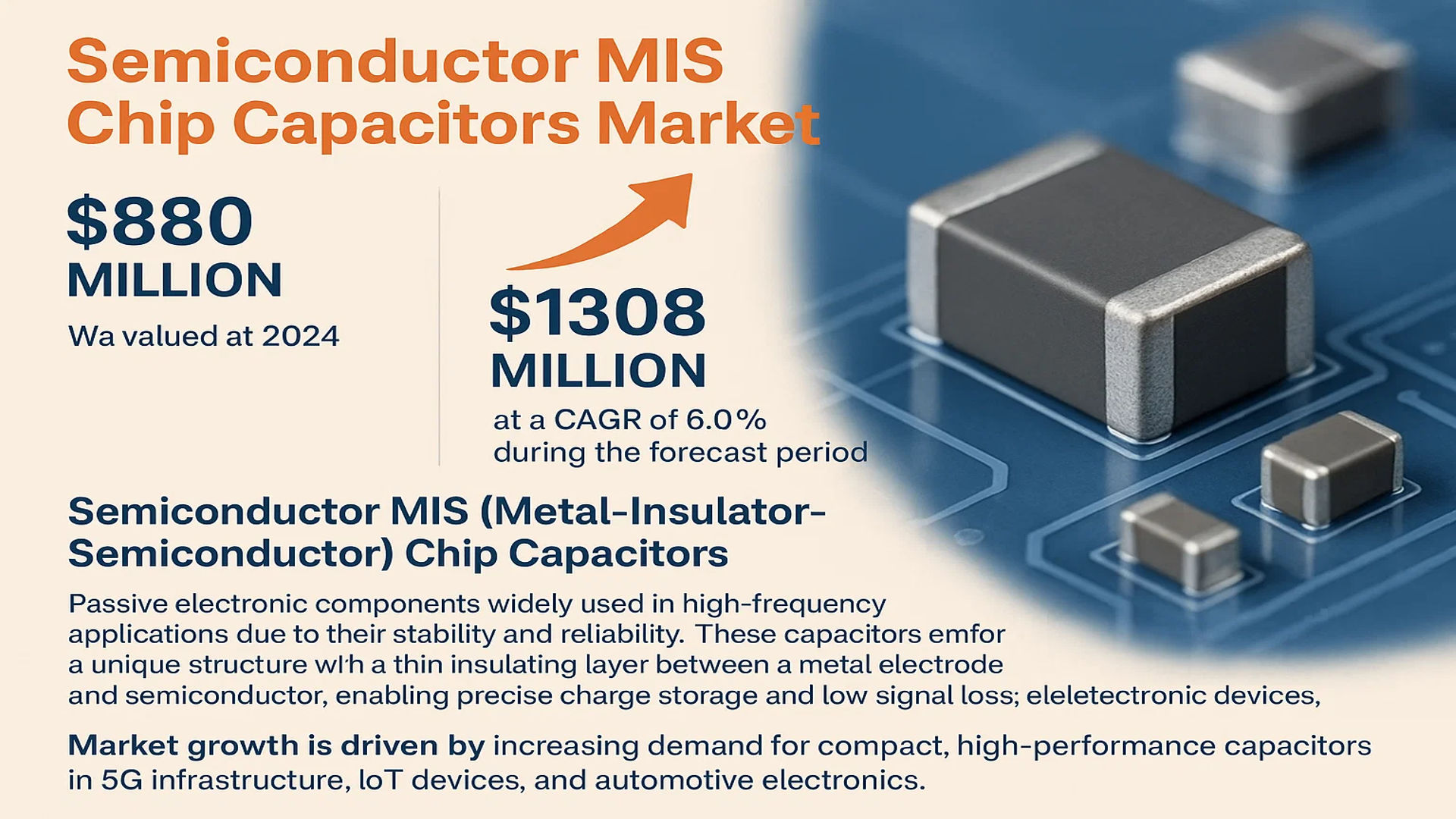

The global Semiconductor MIS Chip Capacitors Market was valued at 880 million in 2024 and is projected to reach US$ 1308 million by 2032, at a CAGR of 6.0% during the forecast period.

Semiconductor MIS (Metal-Insulator-Semiconductor) Chip Capacitors are passive electronic components widely used in high-frequency applications due to their stability and reliability. These capacitors feature a unique structure with a thin insulating layer between a metal electrode and a semiconductor, enabling precise charge storage and low signal loss. They are critical in RF circuits, power management systems, and miniaturized electronic devices.

Market growth is driven by increasing demand for compact, high-performance capacitors in 5G infrastructure, IoT devices, and automotive electronics. The multilayer segment is gaining traction due to its higher capacitance density, while Asia-Pacific dominates production with key players like Murata and TDK expanding capacity. However, supply chain constraints and material cost volatility remain challenges for manufacturers.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Miniaturized Electronic Components to Accelerate Market Growth

The global semiconductor industry is experiencing unprecedented demand for miniaturized electronic components, driven by the rapid advancement of 5G technology, IoT devices, and portable electronics. Semiconductor MIS Chip Capacitors, with their compact Metal-Insulator-Semiconductor structure, are becoming increasingly critical for high-frequency applications where space and performance are paramount. The consumer electronics sector alone is projected to account for over 35% of the total demand for these components by 2026. Furthermore, telecommunications infrastructure upgrades worldwide are creating robust demand for high-performance capacitors in RF applications, with the 5G segment expected to grow at nearly 8% CAGR between 2024-2030.

Automotive Electronics Revolution to Spur Capacitor Adoption

The automotive industry’s shift toward electrification and autonomous driving systems is creating significant opportunities for Semiconductor MIS Chip Capacitors. Modern vehicles now incorporate an average of 3,000-5,000 capacitors across various systems, from advanced driver assistance systems (ADAS) to battery management in electric vehicles. With the global automotive electronics market projected to exceed $400 billion by 2027, the demand for reliable, high-temperature tolerant capacitors is surging. The transition to 48V architectures in vehicles is particularly driving innovation in capacitor technology, requiring components that can handle higher power densities while maintaining stability across wide temperature ranges.

Expansion of Industrial Automation to Fuel Market Expansion

Industrial automation initiatives across manufacturing sectors are generating substantial demand for robust electronic components. Semiconductor MIS Chip Capacitors play vital roles in motor drives, power supplies, and control systems that require long-term reliability under challenging conditions. The push for Industry 4.0 technologies has accelerated capacitor adoption, with the industrial segment expected to grow at nearly 7% annually through 2030. Smart factory implementations and predictive maintenance systems are particularly driving the need for components that can deliver consistent performance in vibration-intensive environments while maintaining precise capacitance characteristics over extended periods.

MARKET RESTRAINTS

Supply Chain Disruptions and Material Shortages to Challenge Market Stability

The semiconductor capacitor market continues to face significant challenges from global supply chain constraints and material shortages. Specialty metals like nickel and titanium used in electrode manufacturing have experienced price fluctuations exceeding 30% in recent years, directly impacting production costs. The industry’s reliance on specific rare earth elements for dielectric materials creates additional vulnerability to geopolitical trade tensions. While capacitor manufacturers are pursuing alternative materials and localized supply chains, transition periods continue to create bottlenecks in production capacity and lead times.

Technical Limitations in High-Frequency Applications to Constrain Adoption

As electronic systems push toward higher frequency operations, Semiconductor MIS Chip Capacitors face inherent limitations in performance characteristics. The parasitic inductance and ESR (Equivalent Series Resistance) properties of traditional capacitor designs create challenges in mmWave (24GHz+) applications. While multilayer designs have improved performance, they still struggle to match the requirements of next-generation RF systems. This technical barrier is particularly evident in aerospace and defense applications where components must maintain stability across extreme environmental conditions while delivering precise high-frequency performance.

Stringent Quality and Reliability Standards to Increase Compliance Costs

The capacitor industry faces mounting pressure from increasingly stringent quality standards across multiple sectors. Automotive applications, for instance, require components to meet AEC-Q200 qualification standards, while medical devices demand compliance with rigorous IEC and ISO specifications. These requirements significantly increase testing costs and time-to-market for new capacitor developments. Additionally, the push for extended product lifecycles exceeding 15 years in industrial applications creates additional design challenges that can limit innovation cycles and increase R&D expenditures.

MARKET CHALLENGES

Intense Price Competition to Squeeze Manufacturer Margins

The Semiconductor MIS Chip Capacitor market has become increasingly commoditized, with price pressures intensifying across all application segments. Asian manufacturers now account for over 65% of global production capacity, creating intense competition that drives prices down by approximately 4-6% annually for standard components. While premium applications in aerospace and medical devices maintain healthier margins, the majority of the market faces constant pressure to reduce costs while maintaining quality standards. This environment makes it particularly challenging for smaller manufacturers to invest in next-generation technologies while remaining price-competitive.

Rapid Technological Evolution to Accelerate Obsolescence Risks

The electronics industry’s breakneck pace of innovation creates significant challenges for capacitor manufacturers. Design cycles for end products continue to shorten, with many consumer electronics now being refreshed every 12-18 months. This rapid turnover increases the risk of component obsolescence, forcing capacitor suppliers to constantly update their product portfolios while maintaining support for legacy systems. The transition to new packaging technologies and substrate materials further complicates production planning, as manufacturers must balance investments in emerging technologies with sustaining traditional manufacturing lines.

Workforce Shortages and Skills Gap to Impact Production Capacity

The semiconductor industry globally faces a critical shortage of skilled technicians and engineers specialized in passive component manufacturing. An estimated 40% of the current workforce in capacitor production will reach retirement age within the next decade, creating significant knowledge transfer challenges. The complex nature of thin-film deposition and precision assembly processes requires extensive training, making it difficult to quickly scale production teams. Furthermore, the industry struggles to attract young engineering talent compared to more “high-profile” semiconductor segments like processors and memory chips.

MARKET OPPORTUNITIES

Emerging Applications in Renewable Energy Systems to Drive New Demand

The rapid expansion of renewable energy infrastructure presents significant opportunities for Semiconductor MIS Chip Capacitors. Solar inverters and wind turbine power converters require robust capacitors capable of handling high voltages and temperatures while maintaining reliability over decades of operation. With global investments in renewable energy projected to exceed $1.7 trillion annually by 2030, capacitor manufacturers are developing specialized product lines to serve this growing market. Energy storage systems, particularly lithium-ion battery management, also create substantial demand for capacitors with enhanced safety features and extended cycle life.

Advanced Packaging Technologies to Enable Performance Breakthroughs

Innovations in semiconductor packaging, including system-in-package (SiP) and 3D heterogeneous integration, are creating new opportunities for embedded capacitor solutions. These advanced packaging approaches require capacitors that can be integrated directly into substrates or interposers while maintaining performance at reduced form factors. The market for embedded passive components is expected to grow at over 9% CAGR through 2030, driven by demands from high-performance computing and mobile devices. Capacitor manufacturers investing in thin-film technologies and novel dielectric materials are well-positioned to capitalize on this trend.

Medical Electronics Expansion to Create Premium Market Segment

The medical device industry’s digital transformation is driving demand for specialized capacitors with enhanced reliability and miniaturization capabilities. Implantable devices, diagnostic equipment, and wearable health monitors all require components that meet stringent biocompatibility standards while delivering consistent performance. With the global medical electronics market projected to reach $8.5 billion by 2027, capacitor manufacturers are developing new product lines featuring improved moisture resistance, sterilization compatibility, and long-term stability. The trend toward point-of-care diagnostics and portable medical equipment further increases the need for compact, high-performance capacitor solutions.

SEMICONDUCTOR MIS CHIP CAPACITORS MARKET TRENDS

Miniaturization and High-Frequency Applications Drive Market Growth

The global semiconductor MIS chip capacitors market is experiencing steady growth, projected to expand from $880 million in 2024 to $1,308 million by 2032, with a compound annual growth rate (CAGR) of 6.0%. One of the primary drivers of this expansion is the increasing demand for miniaturized, high-performance electronic components in telecommunication and consumer electronics. With the rapid adoption of 5G networks, semiconductor MIS chip capacitors are becoming indispensable due to their ability to provide stable capacitance at high frequencies while maintaining compact form factors. The single-layer segment, in particular, is witnessing accelerated demand, expected to grow significantly in the next six years because of its application in RF and microwave circuits.

Other Trends

Automotive Electrification and Industrial Automation

The automotive industry’s shift toward electric vehicles (EVs) and advanced driver-assistance systems (ADAS) is fueling the adoption of semiconductor MIS chip capacitors. These components are critical in power management systems, onboard chargers, and infotainment systems due to their high reliability and thermal stability. Similarly, industrial automation is leveraging these capacitors for motor drives, robotics, and IoT-enabled devices, where precise energy storage and discharge capabilities are essential. The medical sector is another emerging application area, with growing utilization in diagnostic equipment and implantable devices, further broadening the market scope.

Supply Chain Optimization and Regional Market Dynamics

While the market continues to expand, supply chain optimizations are shaping regional dynamics. Asia-Pacific remains the dominant region, particularly China and Japan, due to strong semiconductor manufacturing ecosystems and increasing investments in consumer electronics and 5G infrastructure. Meanwhile, the U.S. market is projected to hold a significant share, driven by innovations in defense and aerospace applications requiring high-performance capacitors. Leading manufacturers such as Murata, TDK, and AVX are strategically focusing on R&D to enhance product efficiency, ensuring they remain competitive in a rapidly evolving market.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Drive Innovation in Semiconductor MIS Chip Capacitors

The global Semiconductor MIS Chip Capacitors Market features a competitive and dynamic environment with multinational corporations, specialized suppliers, and emerging startups all carving out their niches. Leading the charge is Murata Manufacturing Co., Ltd., which holds a dominant position due to its extensive R&D investments and robust product portfolio across consumer electronics and automotive applications. The company’s innovations in multilayer MIS capacitors have solidified its market share, particularly in Asia-Pacific and North America.

TDK Corporation and Vishay Intertechnology, Inc. are also key players, leveraging their decades of expertise in semiconductor components to capture substantial market revenue. These companies focus on high-reliability applications, including medical devices and telecommunications, where precision and durability are critical. TDK recently expanded its production capacity in Southeast Asia to meet rising demand, further strengthening its market position.

Meanwhile, Taiyo Yuden Co., Ltd. and AVX Corporation distinguish themselves through strategic collaborations and niche product offerings. Taiyo Yuden’s ultra-compact MIS capacitors, designed for IoT and wearables, cater to the growing demand for miniaturized electronics. AVX, on the other hand, has prioritized automotive-grade components, aligning with the rapid electrification of vehicles globally.

Growth strategies in this market are heavily centered on innovation. Companies such as KEMET (a Yageo Company) and Johanson Technology, Inc. are focusing on developing high-temperature and high-frequency capacitors, addressing challenges in aerospace and defense applications. Investment in advanced materials and automation is expected to intensify competition, with players vying for differentiation through superior performance and reliability.

List of Key Semiconductor MIS Chip Capacitor Companies Profiled

- Murata Manufacturing Co., Ltd. (Japan)

- TDK Corporation (Japan)

- Vishay Intertechnology, Inc. (U.S.)

- Taiyo Yuden Co., Ltd. (Japan)

- AVX Corporation (U.S.)

- KEMET (Yageo Corporation) (U.S.)

- Johanson Technology, Inc. (U.S.)

- Skyworks Solutions, Inc. (U.S.)

- Kyocera Corporation (Japan)

Segment Analysis:

By Type

Multilayer Segment Dominates Due to Superior Performance in High-Frequency Applications

The market is segmented based on type into:

- Singlelayer

- Subtypes: Silicon-based, GaAs-based, and others

- Multilayer

- Subtypes: LTCC-based, HTCC-based, and others

By Application

Telecommunication Segment Leads Owing to Rapid 5G Network Expansion

The market is segmented based on application into:

- Telecommunication

- Consumer Electronics

- Automotive

- Industrial

- Medical

- Others

By Material

Silicon-Based Capacitors Maintain Market Dominance Through Cost-Effectiveness

The market is segmented based on material into:

- Silicon-based

- Gallium Arsenide (GaAs)-based

- Silicon Carbide (SiC)-based

- Others

By End-User

OEMs Dominate Due to Large-Scale Procurement for Electronic Devices

The market is segmented based on end-user into:

- Original Equipment Manufacturers (OEMs)

- Aftermarket

Regional Analysis: Semiconductor MIS Chip Capacitors Market

Asia-Pacific

The Asia-Pacific region dominates the Semiconductor MIS Chip Capacitors market, accounting for the largest revenue share due to rapid advancements in consumer electronics manufacturing and semiconductor fabrication. China remains the production hub, supported by government initiatives like the “Made in China 2025” strategy, which prioritizes domestic semiconductor self-sufficiency. Japan and South Korea contribute significantly, with companies like Murata and Samsung driving innovation in miniaturized components for smartphones and IoT devices. Meanwhile, India’s growing electronics manufacturing sector presents new opportunities, particularly for mid-range capacitors in industrial and automotive applications. However, supply chain vulnerabilities and trade tensions create challenges for regional market stability.

North America

North America’s market is characterized by high-value applications in defense, aerospace, and 5G infrastructure, where precision and reliability are critical. The U.S. leads adoption with major players like Skyworks and Vishay focusing on R&D for next-generation telecommunications equipment. Recent CHIPS Act funding ($52.7 billion) bolsters domestic semiconductor production, indirectly benefiting capacitor manufacturers. However, strict export controls on advanced technologies and dependence on Asian suppliers for raw materials create operational complexities. The region shows strong demand for multilayer MIS capacitors in medical devices and automotive ADAS systems.

Europe

European demand is driven by automotive electrification and industrial automation, with Germany and France as key markets. Compliance with RoHS and REACH regulations pushes manufacturers toward lead-free and environmentally stable capacitor designs. Companies like TDK and AVX have established strong footholds in automotive-grade components, particularly for electric vehicle power management systems. While the region lags in volume compared to Asia, it maintains leadership in high-reliability applications, with growing investments in research facilities for space and defense technologies. Brexit-related supply chain disruptions continue to impact the UK’s market dynamics.

South America

The South American market remains nascent but shows gradual growth in Brazil and Argentina, primarily serving consumer electronics assembly and renewable energy systems. Economic instability and import dependence constrain market expansion, though local partnerships with global suppliers are increasing. Automotive production recovery post-pandemic has driven demand for basic MIS capacitors in vehicle electronics. Limited local manufacturing capabilities mean most components are imported from Asia and North America, creating price sensitivity challenges.

Middle East & Africa

This emerging market sees demand concentrated in telecommunications infrastructure and oil/gas sector applications. UAE and Saudi Arabia lead adoption through smart city initiatives and 5G rollout programs. While the overall market volume remains low, it exhibits high growth potential with increasing electronics manufacturing in special economic zones. The lack of component production facilities results in complete import reliance, though distributors are expanding regional warehousing to improve supply chain responsiveness. Political uncertainties and fluctuating oil prices intermittently affect investment cycles in key verticals.

Report Scope

This market research report provides a comprehensive analysis of the global Semiconductor MIS Chip Capacitors market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 880 million in 2024 and is projected to reach USD 1,308 million by 2032, growing at a CAGR of 6.0%.

- Segmentation Analysis: Detailed breakdown by product type (Singlelayer, Multilayer), application (Telecommunication, Consumer Electronics, Automotive, Industrial, Medical, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key growth markets.

- Competitive Landscape: Profiles of leading market participants including Skyworks, Vishay, Murata, TDK, and Taiyo Yuden, covering their product portfolios, market share, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging semiconductor technologies, miniaturization trends, and material advancements in capacitor design.

- Market Drivers & Restraints: Evaluation of factors such as increasing demand for electronic devices, 5G deployment, and automotive electronics growth versus supply chain challenges.

- Stakeholder Analysis: Strategic insights for component manufacturers, OEMs, and investors regarding market opportunities and competitive positioning.

The report employs both primary and secondary research methodologies, including expert interviews and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Semiconductor MIS Chip Capacitors Market?

-> Semiconductor MIS Chip Capacitors Market was valued at 880 million in 2024 and is projected to reach US$ 1308 million by 2032, at a CAGR of 6.0% during the forecast period.

Which key companies operate in this market?

-> Major players include Skyworks, Vishay, Murata, TDK, Taiyo Yuden, KEMET, AVX, and Yageo, with the top five companies holding significant market share.

What are the key growth drivers?

-> Growth is driven by increasing demand for consumer electronics, 5G infrastructure deployment, and automotive electronics expansion.

Which region dominates the market?

-> Asia-Pacific leads the market due to strong electronics manufacturing, while North America remains a key innovation hub.

What are the emerging trends?

-> Emerging trends include miniaturization of components, advanced materials for higher capacitance, and integration with IoT devices.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...