MARKET INSIGHTS

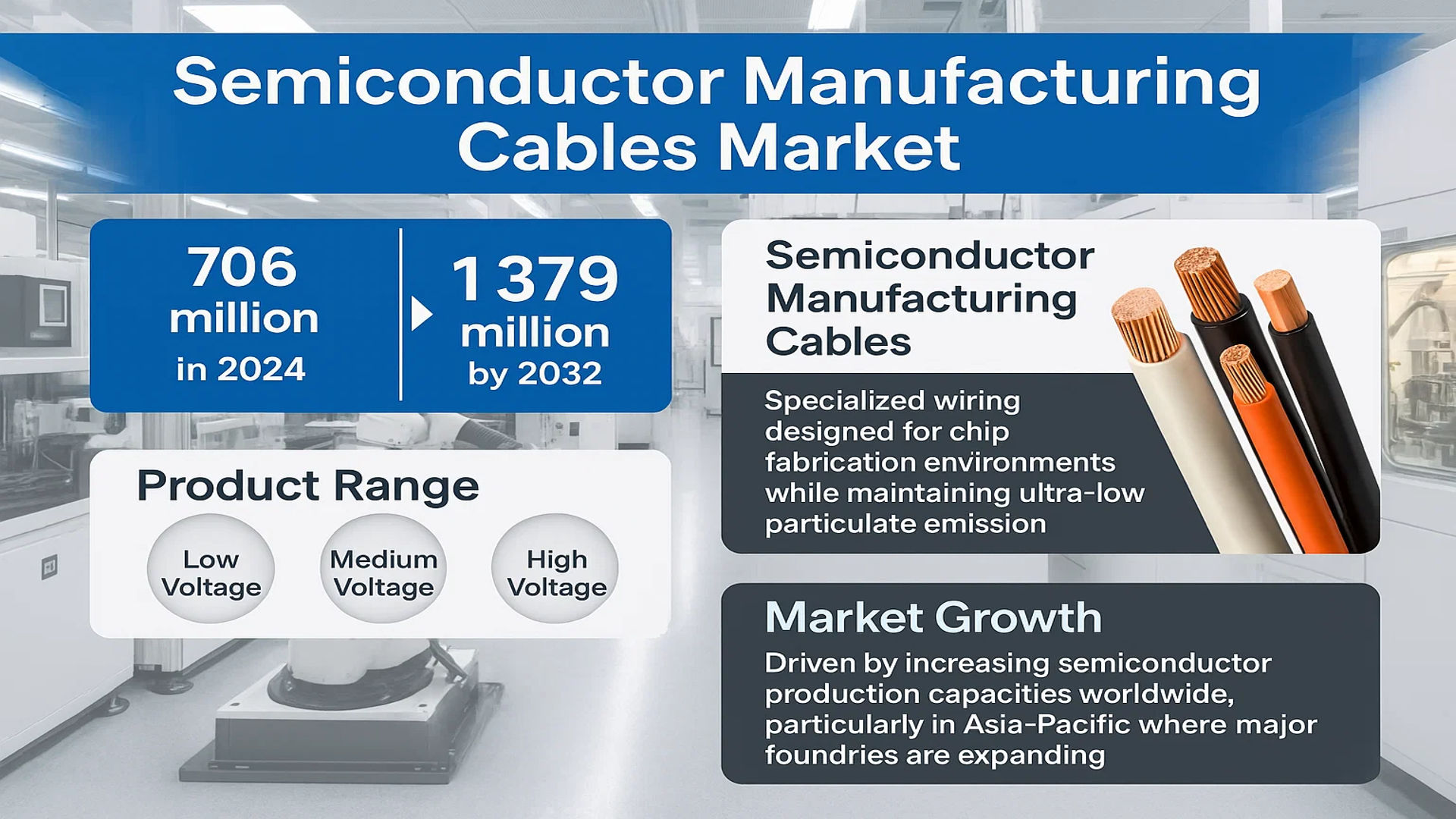

The global Semiconductor Manufacturing Cables Market was valued at 706 million in 2024 and is projected to reach US$ 1379 million by 2032, at a CAGR of 10.3% during the forecast period.

Semiconductor manufacturing cables are specialized wiring solutions designed to meet the stringent requirements of chip fabrication environments. These cables must withstand fast-paced, precise movements while maintaining ultra-low particulate emission to prevent contamination of sensitive semiconductor components. The product range includes low voltage, medium voltage, and high voltage variants, each serving distinct functions in mechanical equipment, information transmission, and power systems within semiconductor facilities.

The market growth is driven by increasing semiconductor production capacities worldwide, particularly in Asia-Pacific where major foundries are expanding. While the global semiconductor market reached USD 580 billion in 2022 with 4.4% growth, certain segments like Analog (20.8% growth) and Sensors (16.3% growth) demonstrated particularly strong demand for specialized cabling solutions. Key players including Helukabel, Gore, and Staubli are investing in advanced materials to meet evolving industry standards for cleanroom compatibility and signal integrity.

MARKET DYNAMICS

MARKET DRIVERS

Rising Semiconductor Production to Fuel Demand for High-Performance Cables

The global semiconductor manufacturing industry continues to grow at an unprecedented pace, driving demand for specialized manufacturing cables. Semiconductor production capacity is expected to increase by over 40% within the next five years, creating significant opportunities for cable manufacturers. High-performance cables are critical components in semiconductor fabrication equipment, where they must maintain signal integrity while withstanding extreme environments. The shift towards smaller node sizes (below 7nm) requires cables with enhanced precision and reduced particle emission.

Increasing Automation in Fabs to Boost Market Growth

Semiconductor fabrication facilities are rapidly adopting automated systems to improve yield and reduce contamination risks. Automated material handling systems and robotics require durable, flexible cables that can maintain reliability through millions of cycles. The wafer handling robot market alone is projected to grow at a CAGR of 11.2% through 2030, directly increasing demand for specialized motion cables. These cables must withstand continuous flexing while maintaining signal integrity in cleanroom environments.

The transition to Industry 4.0 in semiconductor manufacturing is accelerating investments in smart factory technologies. This includes real-time monitoring systems that rely on high-speed data transmission cables capable of operating in vacuum environments and extreme temperatures up to 300°C.

➤ For instance, leading semiconductor equipment manufacturers now require cables with less than 10 particles/ft³ emission rates for cleanroom applications.

Furthermore, the increasing complexity of semiconductor manufacturing processes, including multi-patterning lithography and 3D NAND stacking, requires specialized cable solutions that can maintain performance despite higher thermal and mechanical stresses.

MARKET RESTRAINTS

Stringent Cleanroom Requirements to Limit Market Expansion

While the semiconductor cable market shows strong growth potential, stringent cleanroom standards present significant challenges. Semiconductor fabs require cables that meet ISO Class 1 standards, meaning they must emit fewer than 10 particles (≥0.1 μm) per cubic foot of air during operation. Developing cables that maintain these standards throughout their lifecycle requires expensive materials and specialized manufacturing processes, increasing costs by as much as 300% compared to industrial-grade cables.

Other Restraints

Technological Complexity

Modern semiconductor manufacturing involves multiple process steps with varying environmental conditions. Cables must maintain performance across temperature ranges from -200°C to 300°C while resisting chemical exposure from acids, solvents and plasmas. Developing materials that meet these diverse requirements without compromising flexibility or durability presents substantial engineering challenges.

Certification Bottlenecks

The certification process for semiconductor-grade cables typically takes 12-18 months, slowing time-to-market for new products. Each major semiconductor equipment manufacturer has unique testing protocols, requiring cable suppliers to navigate a complex web of qualification requirements.

MARKET OPPORTUNITIES

Emerging Packaging Technologies to Create New Cable Requirements

Advanced packaging technologies like 3D IC stacking and heterogeneous integration are creating new opportunities for semiconductor cable manufacturers. These advanced packaging approaches require specialized interconnect solutions capable of handling higher current densities and faster data rates while maintaining mechanical stability. The advanced packaging equipment market is projected to grow at 8.7% CAGR, driven by the shift towards chiplets and system-in-package designs.

The development of fan-out wafer-level packaging (FOWLP) and through-silicon via (TSV) technologies requires cables that can maintain signal integrity at data rates exceeding 56 Gbps. This is driving innovation in cable materials and shielding technologies to minimize crosstalk and impedance variations. Cable manufacturers that can deliver solutions optimized for these emerging packaging techniques will capture significant market share.

MARKET CHALLENGES

Supply Chain Constraints to Challenge Market Growth

The semiconductor cable market faces significant supply chain challenges, particularly for specialty materials. Fluoropolymers and high-performance shielding materials have seen lead times extend to 12 months or more due to increased demand across multiple industries. This creates bottlenecks in cable production, with some manufacturers reporting 20-30% longer delivery times compared to pre-pandemic levels.

Other Challenges

Skilled Labor Shortage

The specialized nature of semiconductor cable manufacturing requires highly trained technicians and engineers. However, the industry faces a shortage of qualified personnel, with an estimated 50,000 unfilled positions in precision manufacturing across key semiconductor markets. This labor gap is particularly acute for positions requiring expertise in high-frequency signal integrity and cleanroom-compatible material science.

Rapid Technology Changes

The semiconductor industry’s relentless pace of innovation creates challenges for cable manufacturers. Equipment lifespan typically exceeds 10 years, while semiconductor node transitions occur every 18-24 months. This mismatch requires cable solutions that can accommodate future equipment upgrades without complete replacement, adding complexity to product development.

SEMICONDUCTOR MANUFACTURING CABLES MARKET TRENDS

Rising Demand for High-Purity and High-Performance Cables in Semiconductor Production

The semiconductor manufacturing industry is witnessing a surge in demand for specialized cables capable of maintaining ultra-high purity and performance standards. With global semiconductor market revenues exceeding $580 billion in 2022, manufacturers are investing heavily in cabling solutions that minimize particle emission and contamination risks during fabrication. High-voltage and medium-voltage cables, in particular, are seeing increased adoption due to their ability to withstand the extreme conditions of cleanroom environments. The growing complexity of semiconductor devices, including 5G chips and AI processors, necessitates cables with superior electrical insulation and resistance to electromagnetic interference.

Other Trends

Automation and Industry 4.0 Integration

The shift toward fully automated semiconductor fabs is accelerating the need for durable, flexible cables that can support high-speed robotic movements without degradation. Cable management systems that reduce particulate contamination while maintaining signal integrity are becoming crucial, especially as wafer sizes increase to 300mm and beyond. Industry 4.0 advancements demand real-time data transmission, pushing manufacturers to adopt fiber-optic and shielded twisted-pair cables that meet stringent bandwidth requirements.

Geopolitical Shifts Reshaping Supply Chain Strategies

Recent supply chain disruptions have forced semiconductor manufacturers to reconsider their cable procurement strategies. While the Asia-Pacific region remains dominant with over 58% market share in semiconductor production, companies are increasingly diversifying suppliers across North America and Europe to mitigate risks. This geographic diversification is creating opportunities for cable manufacturers with localized production capabilities. The CHIPS Act in the U.S. and similar initiatives in the EU are expected to drive $200+ billion in new semiconductor fab investments by 2030, significantly expanding the addressable market for specialized manufacturing cables.

Advances in Material Science Enhancing Cable Performance

Innovations in fluoropolymer insulation and ceramic-based shielding materials are enabling cables to operate reliably in semiconductor tools with extreme temperature fluctuations. New composite materials reduce outgassing – a critical requirement in vacuum deposition processes – while maintaining flexibility for robotic arm installations. Leading manufacturers are reporting 30-50% longer service life with these advanced materials compared to conventional PTFE-insulated cables, significantly reducing maintenance costs in multi-billion-dollar fabrication plants.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Cable Manufacturers Focus on Precision and Contamination Control to Gain Competitive Edge

The global semiconductor manufacturing cables market features a diverse competitive landscape, with established multinational corporations and specialized manufacturers vying for market share. Helukabel and LEONI currently dominate the market, holding approximately 18% and 15% revenue shares respectively in 2024. Their leadership stems from extensive R&D investments in ultra-clean cable solutions and strong relationships with semiconductor equipment OEMs.

Staubli has emerged as a key challenger, particularly in the high-voltage cable segment, with its innovative connector systems that minimize particle generation. The company’s recent expansion in Asia has significantly boosted its market presence. Similarly, Pfeiffer Vacuum and MKS Instruments have strengthened their positions through specialized vacuum-compatible cable solutions essential for semiconductor fabrication processes.

Manufacturers are increasingly focusing on developing cables that meet the stringent cleanliness requirements of advanced semiconductor nodes. This has led to strategic partnerships, such as Gore’s collaboration with major chip manufacturers to develop proprietary insulation materials that reduce outgassing, a critical factor in semiconductor yield management.

The market also sees active participation from Asian players like Totoku and Shanghai Electric, who are gaining traction through cost-competitive offerings while progressively improving their technical capabilities. These regional specialists are expected to capture greater market share as semiconductor production continues to expand across Asia.

List of Key Semiconductor Manufacturing Cable Companies

- Helukabel (Germany)

- Gore (U.S.)

- Staubli (Switzerland)

- Comet Group (Switzerland)

- Totoku Electric Co., Ltd. (Japan)

- JEM Electronics (Japan)

- Schmalz (Germany)

- BizLink (Taiwan)

- LEONI (Germany)

- Pfeiffer Vacuum (Germany)

- MKS Instruments (U.S.)

- Shanghai Electric (China)

Segment Analysis:

By Type

Low Voltage Cables Dominate the Market Due to Wide Usage in Precision Semiconductor Manufacturing Equipment

The market is segmented based on type into:

- Low Voltage

- Subtypes: Shielded cables, Flexible cables, and others

- Medium Voltage

- High Voltage

By Application

Mechanical Equipment and Instrumentation System Segment Leads Due to Critical Role in Semiconductor Fabrication

The market is segmented based on application into:

- Mechanical Equipment and Instrumentation System

- Information Transmission System

- Power System

Regional Analysis: Semiconductor Manufacturing Cables Market

Asia-Pacific

The Asia-Pacific region dominates the semiconductor manufacturing cables market, driven by China, South Korea, Japan, and Taiwan, which collectively account for over 60% of global semiconductor production. China’s ambitious semiconductor self-sufficiency push through initiatives like the “Made in China 2025” strategy and the National Integrated Circuit Industry Investment Fund has significantly increased demand for precision cables in fabrication facilities. Taiwan Semiconductor Manufacturing Company (TSMC) alone invests $28 billion annually in advanced node production, requiring ultra-clean, high-reliability cabling solutions. While cost competition remains fierce, regional players like Shanghai Electric and Tatsuta are gaining market share through localized supply chains. Japan’s legacy in materials science continues to drive innovation in contamination-resistant cables, particularly for extreme ultraviolet (EUV) lithography applications.

North America

North America maintains strong demand for high-performance semiconductor cables, particularly from leading fabs like Intel’s $20 billion Ohio project and GlobalFoundries’ expansion in New York. The CHIPS and Science Act’s $52 billion in semiconductor manufacturing incentives is accelerating domestic capacity growth, with cable specifications demanding stricter UL and SEMI compliance standards. U.S.-based suppliers such as Gore and MKS Instruments lead in developing fluoropolymer-insulated cables capable of withstanding high-vacuum environments below 10-9 Torr. However, the market faces challenges from longer equipment approval cycles and workforce shortages in specialized cable assembly.

Europe

Europe’s semiconductor cable market thrives on niche applications in power electronics and MEMS manufacturing, with Germany’s Infineon and Netherlands’ ASML driving demand for customized solutions. EU’s €43 billion Chips Act targets 20% global production share by 2030, requiring advanced cabling for new 300mm fabs. Suppliers like LEONI and Schmalz excel in robotic cable management systems for automated material handling, while strict REACH regulations push adoption of halogen-free cable compounds. The region struggles with higher production costs compared to Asian counterparts, though superior ESD protection (below 108 ohms) commands premium pricing.

South America

South America represents an emerging market, with Brazil’s CEITEC and Argentina’s TIN driving basic semiconductor packaging cable needs. Limited local cable manufacturing forces reliance on imports from U.S. and Asian suppliers, particularly for high-voltage applications in test equipment. While economic instability hinders large-scale investments, regional growth opportunities exist in refurbished semiconductor tool cabling and aftermarket replacements. The absence of stringent cleanroom certification requirements lowers barriers for entry-level suppliers.

Middle East & Africa

The Middle East shows nascent semiconductor cable demand through Saudi Arabia’s Vision 2030 high-tech investments and Israel’s strengthening fabless ecosystem. Türkiye’s Aselsan has emerged as a regional consumer of radiation-hardened cables for defense semiconductors. Africa’s market remains constrained by infrastructure gaps, though South Africa’s semiconductor test & packaging facilities generate steady demand for basic instrumentation cables. The region exhibits the fastest growth rate (projected 12% CAGR) from a small base, with future potential tied to data center construction and IoT device assembly plants.

Report Scope

This market research report provides a comprehensive analysis of the global Semiconductor Manufacturing Cables market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 706 million in 2024 and is projected to reach USD 1,379 million by 2032, growing at a CAGR of 10.3%.

- Segmentation Analysis: Detailed breakdown by product type (Low Voltage, Medium Voltage, High Voltage), application (Mechanical Equipment, Information Transmission, Power Systems), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with Asia-Pacific leading due to semiconductor manufacturing hubs in China, Japan, and South Korea.

- Competitive Landscape: Profiles of leading market participants including Helukabel, Gore, Staubli, BizLink, and LEONI, covering their product portfolios, manufacturing capabilities, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging cable technologies for semiconductor fabrication, including ultra-clean materials, EMI shielding solutions, and high-temperature resistant designs.

- Market Drivers & Restraints: Analysis of factors driving growth (increased semiconductor production, fab expansions) and challenges (supply chain disruptions, material costs).

- Stakeholder Analysis: Strategic insights for semiconductor equipment manufacturers, cable suppliers, and investors navigating the evolving market landscape.

The research methodology combines primary interviews with industry experts and secondary data from verified sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Semiconductor Manufacturing Cables Market?

-> Semiconductor Manufacturing Cables Market was valued at 706 million in 2024 and is projected to reach US$ 1379 million by 2032, at a CAGR of 10.3% during the forecast period.

Which key companies operate in this market?

-> Major players include Helukabel, Gore, Staubli, BizLink, LEONI, MKS Instruments, and Pfeiffer Vacuum.

What are the key growth drivers?

-> Growth is driven by rising semiconductor production, new fab constructions, and demand for advanced cable solutions in chip manufacturing.

Which region dominates the market?

-> Asia-Pacific dominates with over 60% market share, led by semiconductor manufacturing hubs in China, Taiwan, South Korea, and Japan.

What are the emerging trends?

-> Key trends include development of contamination-free cables, integration of smart monitoring systems, and adoption of high-purity materials.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...