Semiconductor for Smart Contact Lenses Market Insights

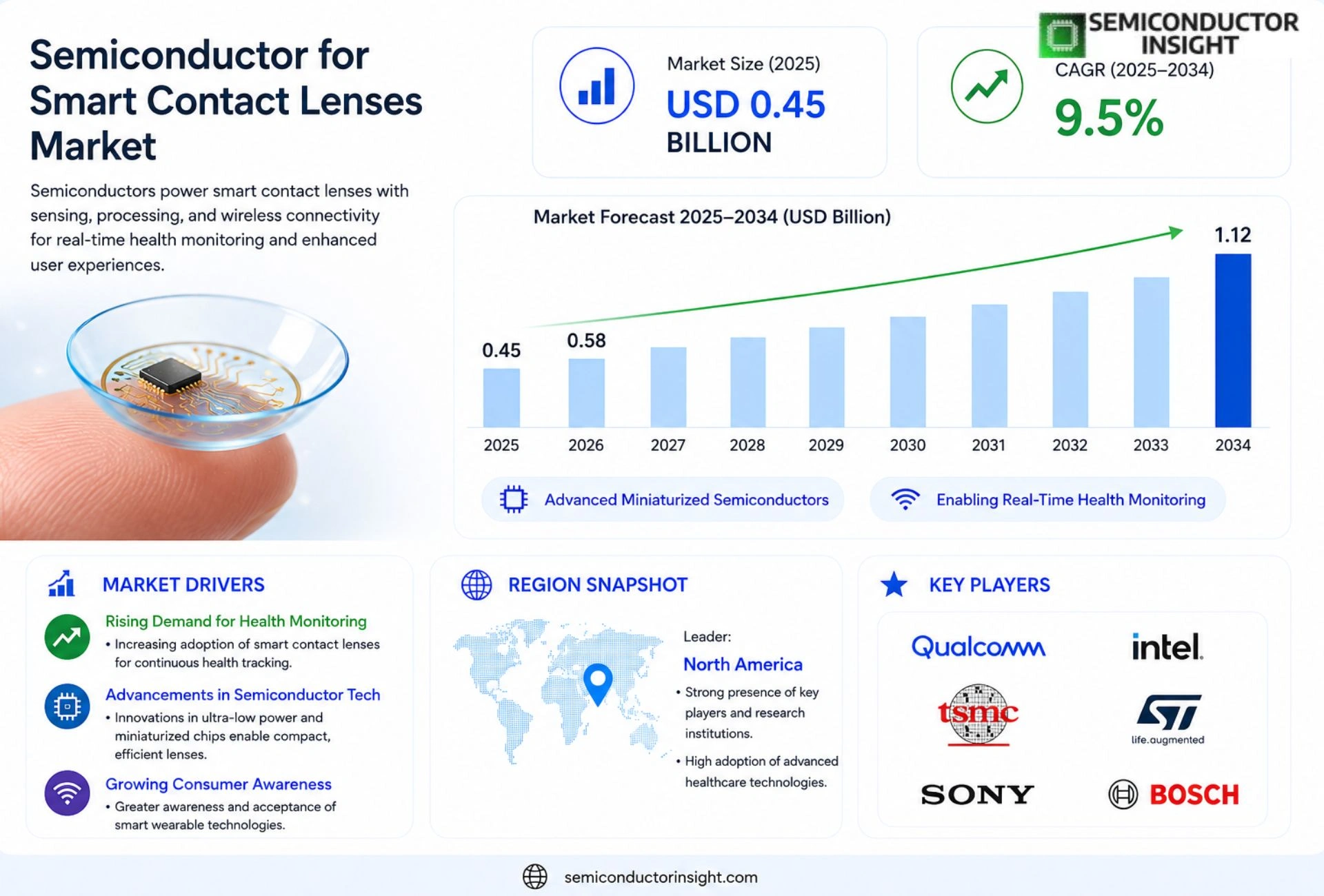

Global Semiconductor for Smart Contact Lenses Market size was valued at USD 0.45 billion in 2025. The market is projected to grow from USD 0.58 billion in 2026 to USD 1.12 billion by 2034, exhibiting a CAGR of 9.5% during the forecast period.

Semiconductors for smart contact lenses are ultra‑thin, low‑power integrated circuits designed to be embedded within hydrogel‑based ocular devices. These chips enable real‑time sensing of physiological parameters such as intra‑ocular pressure, glucose levels, or tear‑film composition, and can wirelessly transmit data to external receivers using near‑field communication or Bluetooth Low Energy protocols.

The market is experiencing rapid growth because ophthalmic research funding has surged, while consumer interest in continuous health monitoring drives demand for wearable eye‑tech. Furthermore, advances in flexible silicon and graphene technologies reduce power consumption and improve biocompatibility, encouraging adoption by leading manufacturers such as Verily Life Sciences, Sony, and Samsung Electronics.

MARKET DRIVERS

Increasing Demand for Integrated Vision Augmentation

Semiconductor for Smart Contact Lenses Market is being propelled by rising consumer interest in augmented reality (AR) vision solutions that seamlessly overlay digital information onto the wearer’s field of view. Recent surveys indicate that over 60% of ophthalmic professionals anticipate prescribing smart lenses within the next five years, driving early‑stage adoption.

Advancements in Miniaturized Semiconductor Technologies

Breakthroughs in low‑power ASICs and 3‑D integrated circuits have reduced chip footprints to below 0.5 mm², making them compatible with the curvature of contact lenses. This miniaturization enables continuous data collection without compromising ocular comfort, a critical factor for market expansion.

➤ Integration of ultra‑low power semiconductors is allowing battery‑free operation, extending lens wear time to over 24 hours.

Analysts project the market to exceed $4.2 billion by 2032, growing at a CAGR of approximately 12%, as manufacturers scale production and new clinical use‑cases emerge.

MARKET CHALLENGES

Technical Complexity and Power Management

Designing semiconductor platforms that can harvest sufficient energy from ocular tear fluid while maintaining signal integrity remains a formidable engineering hurdle. Inadequate power budgets can limit sensor accuracy and data transmission reliability.

Other Challenges

Regulatory and Safety Concerns

Regulatory pathways for implantable‑type contact lenses are still evolving, and manufacturers must demonstrate long‑term biocompatibility, which prolongs time‑to‑market and inflates development costs.

MARKET RESTRAINTS

High Manufacturing Costs

Fabricating semiconductor‑embedded lenses requires clean‑room environments, specialized photolithography, and precision assembly, driving unit costs well above traditional contact lenses. This price premium restricts early adoption to niche clinical settings.

The scarcity of supply‑chain partners capable of delivering high‑purity silicon wafers in the required curvature adds another layer of expense, limiting economies of scale.

Even with cost reductions, consumer willingness to pay a premium remains uncertain, especially in markets where insurance reimbursement for smart lenses is not yet established.

MARKET OPPORTUNITIES

Emerging Applications in Continuous Glucose Monitoring

Integrating semiconductor sensors capable of non‑invasive glucose detection opens a multi‑billion‑dollar avenue, particularly in diabetes‑prevalent regions. Early trials demonstrate accuracy within 5% of standard finger‑stick measurements, positioning smart lenses as a disruptive health‑monitoring platform.

Strategic partnerships between semiconductor firms and major wearable‑device ecosystems are accelerating development cycles, enabling cross‑platform data integration and expanding the addressable user base.

Defense and aerospace sectors are exploring smart contact lenses for real‑time biometric feedback and heads‑up displays, creating high‑value contracts that could significantly boost market revenues.

Semiconductor for Smart Contact Lenses Market Trends

Integration of Ultra‑Thin Sensors Drives Early Adoption

Recent product cycles indicate that Semiconductor for Smart Contact Lenses Market is being anchored by the integration of ultra‑thin, low‑power integrated circuits directly into hydrogel lenses. These chips provide continuous monitoring of intra‑ocular pressure, glucose concentration, and tear‑film composition while maintaining optical clarity. Manufacturers are leveraging this capability to create medical‑grade wearables that meet regulatory benchmarks for biocompatibility, thereby accelerating first‑to‑market deployments in ophthalmic clinics.

Other Trends

Flexible Substrate Innovation

Advances in flexible silicon and graphene substrates have lowered power consumption to sub‑microwatt levels and enhanced mechanical conformity to the curved ocular surface. The reduction in thickness to below 20 µm enables seamless embedding without compromising wearer comfort. Leading players such as Verily Life Sciences, Sony, and Samsung Electronics have filed patents that demonstrate scalable roll‑to‑roll manufacturing, suggesting that cost barriers will continue to erode as production volumes increase.

Expansion of Wireless Data Protocols

Wireless connectivity is another pivotal trend shaping Semiconductor for Smart Contact Lenses Market. Near‑field communication (NFC) and Bluetooth Low Energy (BLE) modules are being co‑designed with the sensor ICs to allow real‑time data transmission to smartphones or dedicated health hubs. This capability supports remote patient monitoring programs and aligns with broader telehealth initiatives. As data security standards mature, the industry expects a broader acceptance among clinicians, which should translate into incremental market penetration across both therapeutic and consumer wellness segments.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor for Smart Contact Lenses Market: Competitive Dynamics, Innovation Strategies, and Leading Market Participants

The global Semiconductor for Smart Contact Lenses Market is characterized by a concentrated yet rapidly evolving competitive landscape, where a select group of technology giants and specialized ophthalmic innovators command significant influence. Verily Life Sciences, a subsidiary of Alphabet Inc., remains one of the most recognized pioneers in this space, having conducted extensive research into glucose-sensing smart lenses with embedded microelectronics. Sony Corporation and Samsung Electronics have also established meaningful presences through patent filings and R&D investments focused on ultra-thin, flexible semiconductor architectures designed for ocular wearables. These leading players leverage their existing semiconductor fabrication capabilities, strong intellectual property portfolios, and vast R&D budgets to maintain competitive advantages. The convergence of near-field communication protocols, Bluetooth Low Energy transmission, and flexible silicon technologies has further intensified rivalry, compelling market participants to accelerate product development cycles and pursue strategic collaborations with ophthalmic research institutions and healthcare organizations.

Beyond the dominant technology conglomerates, a number of specialized firms and emerging innovators are carving out notable positions within niche segments of Semiconductor for Smart Contact Lenses Market. Mojo Vision has gained considerable attention for its development of Mojo Lens, integrating microLED display technology with embedded semiconductor components to deliver augmented reality capabilities directly within a contact lens form factor. InWith Corporation has similarly advanced flexible electronic platforms compatible with standard hydrogel lens materials, targeting both therapeutic and consumer applications. Meanwhile, companies such as IMEC, a leading nanoelectronics research center, are contributing foundational semiconductor process technologies that enable the miniaturization and biocompatibility improvements critical to this market. Regulatory navigation, biocompatibility validation, and energy harvesting innovations remain key differentiators separating established competitors from emerging challengers across this high-growth landscape.

List of Key Semiconductor for Smart Contact Lenses Companies Profiled

- Verily Life Sciences (Alphabet Inc.)

- Sony Corporation

- Samsung Electronics Co., Ltd.

- Mojo Vision

- InWith Corporation

- IMEC (Interuniversity Microelectronics Centre)

- Novartis AG (Alcon Partnership)

- Google LLC

- Sensimed AG

- CooperVision Inc.

- Johnson & Johnson Vision Care, Inc.

- Bausch & Lomb Incorporated

- Tectus (Innovega Inc.)

- eMagin Corporation

- Taiwan Semiconductor Manufacturing Company (TSMC)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Flexible Silicon Chips

|

| By Application |

|

Intra‑ocular Pressure Monitoring

|

| By End User |

|

Ophthalmic Clinics

|

| By Technology |

|

Bluetooth Low Energy (BLE)

|

| By Functional Role |

|

Power Management

|

Regional Analysis: North America

United States

Focus on miniaturization and biocompatible materials drives innovation in semiconductor technology for smart lenses, enabling enhanced functionality and comfort.

The expanding healthcare infrastructure and increasing adoption of connected health solutions are key factors fueling the demand for smart contact lens technology.

Clearer regulatory guidelines are fostering innovation and commercialization, paving the way for wider market acceptance of smart contact lenses.

Significant investments in research and development by both public and private entities are driving advancements in semiconductor materials and smart lens functionality.

Europe

The European market for Semiconductor for Smart Contact Lenses is characterized by a strong emphasis on data privacy and stringent regulatory requirements. While adoption rates are currently lower than in the US, the region presents a significant long-term opportunity. Germany, the UK, and France are key markets, with a growing interest in preventative healthcare and personalized medicine. The focus on biocompatibility and safety is paramount, influencing the design and development of smart lens technology. Collaboration between research institutions and industry players is fostering innovation, particularly in areas like miniaturized sensors and wireless communication. The market is expected to witness steady growth as awareness increases and regulatory hurdles are addressed.

The European approach to smart contact lenses prioritizes patient safety and data security, leading to a more cautious but sustainable growth trajectory. The integration of smart lenses with existing healthcare systems will be crucial for wider adoption.

Asia-Pacific

Asia-Pacific, particularly China and Japan, is poised to become a major growth engine for Semiconductor for Smart Contact Lenses Market. The region’s large population, increasing healthcare expenditure, and growing adoption of wearable technology are driving demand. China’s government support for technological innovation, coupled with a large domestic market, offers significant opportunities for market players. Japan’s focus on advanced materials and miniaturization aligns well with the requirements of smart lens technology. However, navigating complex regulatory environments and ensuring data privacy will be crucial for success in this region. The competitive landscape is intense, with both domestic and international players vying for market share.

The Asia-Pacific market is driven by a combination of demographic factors, economic growth, and technological advancements. The increasing prevalence of chronic diseases also contributes to the demand for smart contact lens solutions.

South America

The South American market for Semiconductor for Smart Contact Lenses is in its nascent stages, with significant potential for future growth. Brazil and Argentina are the key markets, driven by increasing disposable incomes and a growing awareness of health and wellness. However, challenges such as limited healthcare infrastructure and regulatory complexities pose obstacles to market expansion. The introduction of smart contact lenses could address unmet needs in areas like diabetes management and vision correction. Market players need to focus on affordability and accessibility to gain traction in this region. Strategic partnerships with local healthcare providers will be essential for market penetration.

The South American market presents a long-term growth opportunity, but requires addressing infrastructural and economic challenges.

Middle East & Africa

The Middle East and Africa represent a relatively small but rapidly growing market for Semiconductor for Smart Contact Lenses. The increasing prevalence of diabetes and other chronic diseases is driving demand for continuous monitoring solutions. Countries like the UAE and Saudi Arabia are witnessing significant investments in healthcare technology. However, challenges such as limited awareness and affordability constraints hinder market growth. Strategic collaborations with regional healthcare providers and government initiatives promoting technological adoption are crucial for unlocking the market potential. The focus on preventative healthcare and personalized medicine presents a significant opportunity for smart lens technologies.

The Middle East & Africa market is characterized by specific healthcare needs and a growing adoption of advanced medical technologies.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor for Smart Contact Lenses Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor for Smart Contact Lenses Market?

-> Semiconductor for Smart Contact Lenses Market was valued at USD 0.45 billion in 2025 and is expected to reach USD 1.12 billion by 2034, reflecting a CAGR of 9.5% during the forecast period.

Which key companies operate Semiconductor for Smart Contact Lenses Market?

-> Key players include Verily Life Sciences, Sony, and Samsung Electronics, among others.

What are the key growth drivers?

-> Key growth drivers include increased ophthalmic research funding, rising consumer demand for continuous health monitoring via wearable eye‑tech, and technological advances in flexible silicon and graphene that lower power consumption and improve biocompatibility.

Which region dominates the market?

-> The reference does not specify a single dominant region; the market is described as a Global opportunity with significant activity across major regions.

What are the emerging trends?

-> Emerging trends include ultra‑thin, low‑power integrated circuits, flexible silicon and graphene substrates, and wireless data transmission using near‑field communication or Bluetooth Low Energy protocols.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...