Semiconductor for Robotic Surgery Systems Market Insights

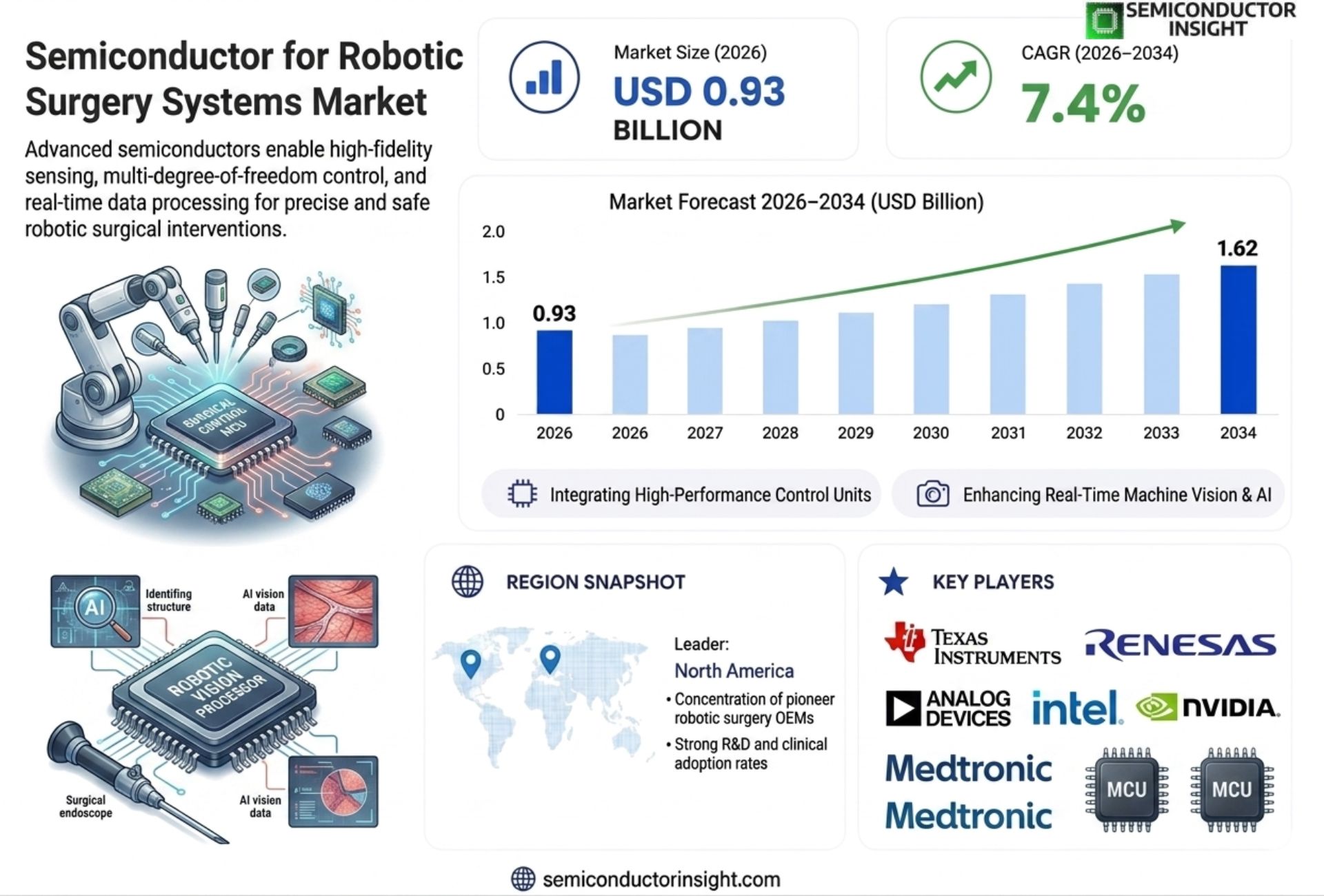

Global Semiconductor for Robotic Surgery Systems Market size was valued at USD 0.87 billion in 2025. The market is projected to grow from USD 0.93 billion in 2026 to USD 1.62 billion by 2034, exhibiting a CAGR of 7.4% during the forecast period.

Semiconductors for robotic surgery systems encompass application‑specific integrated circuits (ASICs), system‑on‑chips (SoCs), power‑management ICs and high‑precision sensor chips that enable real‑time motion control, haptic feedback and image processing within minimally invasive surgical robots.

The market is accelerating because hospitals are expanding robotic surgery programs, while advances in AI‑driven navigation demand higher‑performance chips. However, supply chain constraints for advanced silicon pose challenges; furthermore, regulatory approvals for new devices drive investment from major players such as Intuitive Surgical, Medtronic and Siemens Healthineers.

MARKET DRIVERS

Advances in Precision Imaging

Recent breakthroughs in high‑resolution imaging sensors have enabled robotic surgery platforms to deliver sub‑millimeter precision. These imaging modules rely on specialized semiconductors that process massive data streams in real time, reducing latency and improving surgeon control. Manufacturers are investing heavily in integrating AI‑enabled chips, which further enhances tissue differentiation and reduces operative risk.

Growth of Minimally Invasive Procedures

The global shift toward minimally invasive surgery is driving demand for more reliable, compact semiconductor components. Hospitals are adopting robotic systems to shorten patient recovery times and lower overall healthcare costs. As procedure volumes rise, the need for durable, low‑power chips that can withstand sterilization cycles becomes critical.

➤ “The integration of next‑generation power‑efficient semiconductors is projected to accelerate the adoption of robotic surgery platforms by up to 15 % over the next three years.”

Regulatory agencies have also streamlined approval pathways for devices that demonstrate enhanced safety through advanced semiconductor control units, creating a favorable environment for market expansion.

MARKET CHALLENGES

High Development Costs

Designing radiation‑hard, biocompatible semiconductor modules demands substantial R&D investment. Small‑ and medium‑size suppliers often lack the capital to meet these stringent standards, limiting competition and driving up component prices.

Other Challenges

Supply Chain Vulnerabilities

Global shortages of silicon wafers and specialized packaging materials have intermittently constrained production capacity, forcing manufacturers to maintain larger safety stocks and increasing lead times.

MARKET RESTRAINTS

Stringent Regulatory Oversight

Regulatory bodies require extensive validation of every semiconductor component used in robotic surgery systems. The compliance testing timeline can extend project schedules by 12‑18 months, discouraging rapid product iteration and raising entry barriers for new market participants.

MARKET OPPORTUNITIES

Emerging AI‑Driven Surgical Assistants

Artificial‑intelligence algorithms are being embedded directly into on‑board chips, enabling real‑time decision support and autonomous safety checks. Companies that can deliver low‑latency, AI‑optimized semiconductors stand to capture a growing share of the market as hospitals seek smarter, more efficient robotic systems. Additionally, the rise of tele‑operated surgery in remote regions presents a compelling use‑case for robust, energy‑efficient semiconductor solutions.

Semiconductor for Robotic Surgery Systems Market Trends

AI‑Driven Precision Control Expands Market Reach

Semiconductor for Robotic Surgery Systems Market is being reshaped by rapid integration of artificial‑intelligence algorithms that require higher‑performance ASICs, system‑on‑chips and sensor arrays. AI‑enabled navigation and real‑time image processing push demand for chips that deliver sub‑millisecond latency and ultra‑low power consumption, allowing surgical robots to execute complex maneuvers with unprecedented accuracy. Hospitals expanding robotic programmes are adopting platforms that incorporate these advanced chips, which in turn drives component suppliers to prioritize AI‑centric designs and tighter integration across the hardware stack.

Other Trends

Supply‑Chain Constraints for Advanced Silicon

Global semiconductor fabs are operating near capacity, creating bottlenecks for the high‑precision silicon needed in robotic surgery devices. The scarcity of specialized wafers and the limited number of foundries capable of producing medical‑grade ASICs increase lead times and pressure on pricing. Manufacturers are responding by securing long‑term contracts with tier‑one foundries and by investing in in‑house design capabilities to mitigate exposure to external disruptions. These actions help maintain a steady flow of components while preserving the stringent reliability standards required for surgical applications.

Regulatory Momentum and Capital Investment

Regulatory pathways for new robotic surgery systems are becoming clearer, encouraging major players such as Intuitive Surgical, Medtronic and Siemens Healthineers to allocate additional capital toward next‑generation semiconductor solutions. Faster approval cycles for devices that demonstrate improved safety through precise motion control and enhanced haptic feedback enable companies to bring AI‑enhanced platforms to market more quickly. This regulatory confidence is also attracting venture funding for niche chip designers that specialize in low‑noise sensors and power‑management ICs tailored to the strict compliance requirements of the medical sector.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Technologies Powering Robotic Surgery Systems

Semiconductor segment for robotic surgery systems is currently led by integrated‑circuit powerhouses that provide high‑performance application‑specific integrated circuits (ASICs), system‑on‑chips (SoCs) and AI‑accelerated GPUs essential for real‑time motion control, haptic feedback and advanced image processing. Intel’s Xeon and Movidius families, NVIDIA’s Jetson platforms, and Texas Instruments’ precision‑control SoCs dominate the upper‑tier market, offering the computational density and low‑latency interfaces demanded by next‑generation surgical robots. Their extensive automotive and industrial experience translates into robust supply chains, enabling manufacturers such as Intuitive Surgical and Medtronic to scale robot deployments while meeting rigorous regulatory requirements.

Beyond the core leaders, a broad cohort of niche semiconductor firms supplies specialized components that enhance sensor accuracy, power‑management efficiency and miniaturization. Analog Devices and Maxim Integrated deliver high‑precision analog front ends and sensor signal‑conditioning chips, while STMicroelectronics, Infineon Technologies and NXP Semiconductors focus on ultra‑low‑power microcontrollers and safety‑critical power‑management ICs. Emerging players such as ON Semiconductor, Microchip Technology and Renesas Electronics contribute cost‑effective mixed‑signal solutions that enable smaller robotic arms and more affordable systems, expanding market adoption in regional hospitals.

List of Key Semiconductor Companies Profiled

- Intel Corporation

- NVIDIA Corporation

- Texas Instruments

- Analog Devices

- STMicroelectronics

- Infineon Technologies

- NXP Semiconductors

- Qualcomm

- Broadcom Inc.

- Renesas Electronics

- ON Semiconductor

- Microchip Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

ASICs & SoCs drive the architecture of robotic surgery platforms because they integrate compute, control and communication in a single silicon footprint. – Enable real‑time AI‑enhanced image analysis while maintaining low latency. – Reduce board‑level complexity, supporting compact robot arms and easier sterilization. – Offer design flexibility that accommodates evolving surgical algorithms and sensor arrays. |

| By Application |

|

Image Processing is the leading application segment as surgeons rely on ultra‑high‑definition visualisation and AI‑driven tissue recognition. – Semiconductor engines deliver rapid pixel‑level analysis for augmented reality overlays. – Tight integration with sensor chips provides depth perception essential for precise instrument positioning. – Continuous firmware upgrades enable newer algorithms without hardware redesign. |

| By End User |

|

Hospitals emerge as the dominant end‑user due to their investment in comprehensive robotic suites and focus on minimally invasive procedures. – Require highly reliable, fault‑tolerant chips that meet stringent regulatory standards. – Prioritize scalable architectures to support multiple surgical specialties. – Favor long‑term vendor partnerships that ensure supply chain resilience and post‑sale support. |

| By Integration Level |

|

Integrated Modules are gaining traction as they encapsulate power, processing and sensor interfaces within a single footprint. – Simplify mechanical design of robotic arms, reducing cable clutter and potential failure points. – Accelerate time‑to‑market for new surgical robots by leveraging pre‑qualified module libraries. – Offer thermal management solutions that align with the stringent operating environments of operating rooms. |

| By Functional Role |

|

Control Electronics remain the cornerstone of robotic surgery systems because they orchestrate precise movements and safety interlocks. – Provide deterministic latency essential for real‑time instrument articulation. – Integrate redundancy features that satisfy surgical safety certifications. – Enable seamless firmware updates that incorporate the latest AI‑driven assistance algorithms. |

Regional Analysis: North America

The continuous evolution of semiconductor technology, including the development of more powerful and energy-efficient chips, is a key driver of the market in the US. Miniaturization and increased processing capabilities are essential for enhancing the precision and functionality of robotic surgical systems.

Rising healthcare spending in the United States directly translates to greater investment in advanced medical technologies like robotic surgery. This creates a sustained demand for sophisticated semiconductor components.

The US regulatory environment, overseen by bodies like the FDA, plays a crucial role in shaping the market. Clear and efficient approval processes for robotic surgical systems with advanced semiconductors are essential for market growth.

Collaborations between semiconductor companies and medical device manufacturers are fostering innovation and facilitating the development of cutting-edge robotic surgery systems in the USA.

Europe

Europe represents a significant and steadily growing market for Semiconductor for Robotic Surgery Systems. Driven by advancements in healthcare and a commitment to technological innovation, the region is witnessing increasing adoption of robotic surgery. The focus on precision and minimally invasive procedures is creating demand for advanced semiconductor solutions. Key markets within Europe, such as Germany, the UK, and France, are leading the way in embracing this technology. The relatively high cost of healthcare in some European countries presents both a challenge and an opportunity, as it encourages investment in advanced, cost-effective surgical solutions. The European Union’s emphasis on medical device regulation and standardization also influences market dynamics.

Asia-Pacific

Asia-Pacific is emerging as a rapidly expanding market for Semiconductor for Robotic Surgery Systems. Fueled by a growing middle class, increasing healthcare awareness, and government initiatives to modernize healthcare infrastructure, the region presents substantial growth potential. Countries like Japan, China, and South Korea are at the forefront of this growth, with significant investments in robotics and medical technology. The expanding healthcare expenditure in these nations is a key driver. The presence of a large and skilled workforce also supports the development and manufacturing of these systems. Competition from local manufacturers is intensifying, creating a dynamic market environment.

South America

South America represents a smaller but gradually developing market for Semiconductor for Robotic Surgery Systems. Healthcare infrastructure and adoption rates vary across the region, but there is a growing interest in advanced surgical technologies. Brazil and Argentina are key markets with increasing investments in healthcare. The increasing affordability of medical devices and the growing awareness of the benefits of robotic surgery are contributing to market expansion. Government initiatives to improve healthcare access are also playing a role.

Middle East & Africa

The Middle East & Africa market for Semiconductor for Robotic Surgery Systems is in its nascent stages but holds significant long-term potential. Rising healthcare expenditure, particularly in countries like Saudi Arabia and the UAE, coupled with government investments in healthcare infrastructure, are driving demand. The region’s focus on attracting advanced medical technologies and fostering innovation is creating opportunities for growth. The market is expected to witness substantial expansion in the coming years as healthcare infrastructure continues to develop.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor for Robotic Surgery Systems Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor for Robotic Surgery Systems Market?

-> Semiconductor for Robotic Surgery Systems Market was valued at USD 0.87 billion in 2025 and is expected to reach USD 1.62 billion by 2034.

Which key companies operate Semiconductor for Robotic Surgery Systems Market?

-> Key players include Intuitive Surgical, Medtronic, and Siemens Healthineers, among others.

What are the key growth drivers?

-> Key growth drivers include expansion of robotic surgery programs in hospitals, increasing demand for AI‑driven navigation, development of high‑performance ASICs, SoCs and sensor chips, and regulatory approvals stimulating investment.

Which region dominates the market?

-> Regional dominance information is not explicitly disclosed in the available data.

What are the emerging trends?

-> Emerging trends include integration of AI‑based navigation, advancement of high‑precision sensor chips, and development of power‑management ICs tailored for robotic surgery applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...