MARKET INSIGHTS

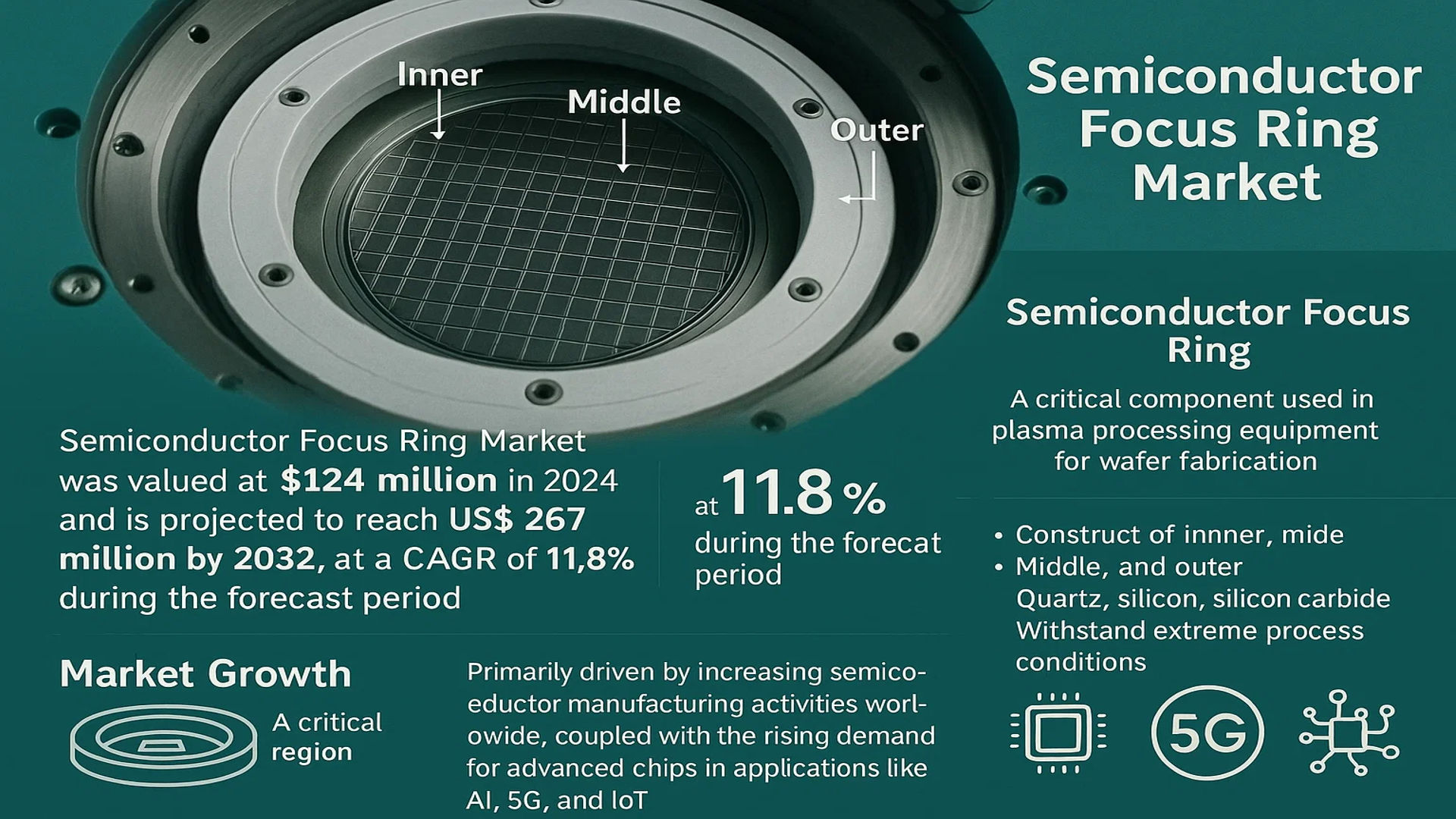

The global Semiconductor Focus Ring Market was valued at 124 million in 2024 and is projected to reach US$ 267 million by 2032, at a CAGR of 11.8% during the forecast period.

A Semiconductor Focus Ring is a critical component used in plasma processing equipment for wafer fabrication. It consists of an inner, middle, and outer region designed to surround the target substrate, ensuring uniform plasma distribution during etching or deposition processes. These rings are typically made from high-purity materials like quartz, silicon, or silicon carbide to withstand extreme process conditions.

The market growth is primarily driven by increasing semiconductor manufacturing activities worldwide, coupled with the rising demand for advanced chips in applications like AI, 5G, and IoT. While the global semiconductor market reached USD 580 billion in 2022 with 4.4% growth, focus ring demand is outpacing overall industry expansion due to their critical role in fabrication processes. The Asia-Pacific region dominates consumption patterns, despite experiencing a 2% decline in overall semiconductor sales in 2022, as it remains the hub for semiconductor manufacturing with leading foundries expanding production capacity.

MARKET DYNAMICS

MARKET DRIVERS

Expansion in Semiconductor Manufacturing Capacities to Accelerate Focus Ring Demand

The global semiconductor industry is witnessing unprecedented capacity expansion, with over 80 new fabrication plants projected to become operational worldwide by 2028. This manufacturing boom directly translates to increased demand for semiconductor processing equipment components, including focus rings. Focus rings play a critical role in plasma etching processes by improving process uniformity and yield rates. As chip manufacturers ramp up production to meet the growing needs of AI, IoT, and 5G applications, the replacement frequency of these consumable components is expected to rise significantly. Recent wafer fab investments in key regions like Taiwan, South Korea, and the United States underscore this growth trajectory.

Technological Advancements in Wafer Processing to Spur Market Growth

Emerging fabrication technologies are driving innovations in focus ring design and materials. The transition to 300mm and larger wafer sizes along with more advanced nodes below 5nm creates stringent requirements for process control, where focus rings become increasingly critical. Leading manufacturers are developing next-generation silicon carbide and quartz-based rings that offer superior plasma resistance and longer operational life. These technological improvements correspond with the industry’s focus on reducing cost-per-transistor while maintaining yield quality.

➤ Recent testing data shows advanced silicon carbide focus rings can extend maintenance cycles by up to 40% compared to conventional materials, significantly impacting fab operational efficiency.

The growing adoption of extreme ultraviolet (EUV) lithography further amplifies the importance of precise plasma control during etching processes. This creates opportunities for focus ring suppliers to develop specialized solutions tailored for cutting-edge fabrication technologies.

MARKET CHALLENGES

High Material Costs and Complex Manufacturing Processes Create Adoption Barriers

The semiconductor focus ring market faces significant cost-related challenges due to the specialized materials and precision engineering required for production. Silicon carbide, one of the most advanced materials, involves expensive manufacturing techniques and limited supplier availability. These factors contribute to premium pricing that can impact adoption rates, particularly among smaller fabrication facilities operating with constrained budgets.

Other Challenges

Precision Tolerance Requirements

Modern semiconductor processes demand focus rings with micrometer-level precision, where even minor dimensional variations can affect plasma distribution and etching uniformity. Maintaining these tight tolerances across production batches requires advanced manufacturing capabilities and rigorous quality control measures.

Supply Chain Vulnerability

The industry’s heavy reliance on specialty material suppliers from limited geographic regions creates potential bottlenecks. Disruptions in raw material availability can directly impact focus ring production lead times and costs, affecting the entire semiconductor manufacturing ecosystem.

MARKET RESTRAINTS

Technical Complexity in Advanced Node Applications Limits Market Penetration

As semiconductor nodes advance below 3nm, focus rings must meet increasingly stringent technical specifications that push the limits of current material science. The creation of ultra-uniform plasma distribution patterns requires rings with exceptional thermal and electrical properties that remain stable across thousands of processing cycles. Many existing materials struggle to meet these requirements without significant redesign or material enhancements.

Additionally, the specialized knowledge required to properly integrate advanced focus rings into new process flows creates another adoption barrier. Without proper implementation, even high-performance rings may fail to deliver their potential benefits. This complexity forces equipment manufacturers and semiconductor fabs to invest in additional training and process development resources.

MARKET OPPORTUNITIES

Strategic Focus on Sustainability and Circular Economy Models Opens New Revenue Streams

The semiconductor industry’s growing emphasis on sustainability and resource efficiency presents manufacturers with opportunities to develop innovative focus ring solutions. Emerging circular economy approaches allow for regenerated and recycled materials in ring construction without compromising performance. Early adopters implementing such sustainable practices gain competitive advantages as fabs increasingly incorporate environmental considerations into procurement decisions.

Furthermore, the development of predictive maintenance technologies coupled with advanced focus ring materials creates opportunities for value-added services. By integrating sensor technologies and wear monitoring systems, suppliers can offer comprehensive solutions that optimize ring replacement cycles while minimizing unplanned equipment downtime.

SEMICONDUCTOR FOCUS RING MARKET TRENDS

Rising Semiconductor Fabrication Demand Accelerates Focus Ring Adoption

The semiconductor focus ring market is experiencing robust growth, driven by escalating demand for advanced semiconductor fabrication processes. With the global market valued at $124 million in 2024, projections indicate it will reach $267 million by 2032, growing at a CAGR of 11.8% during the forecast period. This surge aligns with the semiconductor industry’s expansion, where focus rings play a critical role in plasma etching and deposition processes by ensuring uniform ion distribution across wafers. While the Asia-Pacific region dominates semiconductor manufacturing, recent geopolitical shifts have prompted increased investments in North American and European fabrication facilities, further stimulating demand.

Other Trends

Material Innovation Enhances Performance

The shift from traditional quartz to high-performance materials like silicon carbide (SiC) is gaining momentum. Silicon carbide focus rings exhibit superior durability and plasma resistance, extending operational lifespans by up to 30% compared to quartz alternatives. This transition is particularly evident in 5nm and below process nodes, where etching precision requirements are most stringent. Manufacturers are also exploring hybrid designs combining silicon and ceramic composites to optimize cost-performance ratios.

Automation and Industry 4.0 Integration Reshape Production

Semiconductor equipment manufacturers are increasingly incorporating IoT-enabled monitoring systems into focus ring assemblies. Real-time wear detection algorithms can predict maintenance needs with 95% accuracy, reducing unplanned tool downtime by 22%. This technological leap complements the industry’s broader pivot toward smart factories, where AI-driven process optimization is becoming standard. Meanwhile, collaborative robotics are being deployed for precision handling of focus rings during chamber maintenance – a task previously requiring manual intervention and causing yield loss during recalibration.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Drive Innovation in Semiconductor Focus Ring Technology

The global semiconductor focus ring market operates in a moderately consolidated landscape, with key players competing on technological innovation, material science expertise, and global supply chain capabilities. CoorsTek and FerroTec currently dominate the market, jointly holding approximately 35-40% of the global revenue share in 2024. Their leadership stems from decades of experience in advanced ceramics and semiconductor component manufacturing.

Greene Tweed has emerged as a significant competitor, particularly in the silicon carbide focus ring segment, owing to its proprietary material formulations that extend component lifespan in harsh plasma environments. Its 2023 acquisition of a specialist ceramics manufacturer strengthened its position in the Asia-Pacific market, which accounts for nearly 60% of global semiconductor production capacity.

Mid-sized players like Kallex and Daewon are gaining market traction through specialized offerings. Kallex’s patented quartz-based focus rings demonstrate 30% longer operational life compared to industry standards, while Daewon’s cost-effective solutions have made significant inroads in price-sensitive emerging markets.

The competitive intensity is further heightened by vertical integration strategies. Worldex recently expanded its in-house machining capabilities, reducing lead times by 40%, while Max Luck Technology partnered with three major foundries to co-develop application-specific focus ring designs. Such strategic moves are crucial as semiconductor manufacturers demand tighter integration between processing equipment and consumable components.

List of Key Semiconductor Focus Ring Manufacturers

- CoorsTek (U.S.)

- FerroTec (U.S.)

- Greene Tweed (U.S.)

- Kallex (South Korea)

- Daewon (South Korea)

- Worldex (South Korea)

- Max Luck Technology (Taiwan)

- Coma Technology (Japan)

Segment Analysis:

By Type

Silicon Carbide Segment Leads Due to Superior Durability and Thermal Conductivity

The market is segmented based on type into:

- Quartz

- Subtypes: High-purity, Fused, and others

- Silicon

- Silicon Carbide

- Others

By Application

Wafer Etching Segment Dominates Due to Critical Role in Semiconductor Fabrication

The market is segmented based on application into:

- Wafer Etching

- Plasma Processing

- Semiconductor Manufacturing

- Others

By End User

Foundry Segment Accounts for Significant Share Due to High Production Volumes

The market is segmented based on end user into:

- Foundries

- IDMs (Integrated Device Manufacturers)

- OSAT (Outsourced Semiconductor Assembly and Test)

- Others

Regional Analysis: Semiconductor Focus Ring Market

Asia-Pacific

The Asia-Pacific region dominates the global semiconductor focus ring market, accounting for over 60% of the total demand, driven by massive semiconductor fabrication expansion in countries like Taiwan, South Korea, Japan, and China. Taiwan Semiconductor Manufacturing Company (TSMC) alone accounts for a significant portion of focus ring consumption due to its US$40.9 billion capital expenditure planned for 2023. While China is aggressively growing its domestic semiconductor capabilities through policies like Made in China 2025, Japan remains a key supplier of high-purity silicon and silicon carbide materials used in focus ring production. The region’s leadership stems from both strong demand and established supply chains.

North America

North America’s focus ring market is propelled by advanced chip manufacturing requirements from Intel, Micron, and GlobalFoundries, coupled with government incentives like the US CHIPS Act’s US$52 billion funding package. Silicon carbide focus rings see particularly strong adoption in the region due to their durability in high-power semiconductor applications. However, the market faces challenges from supply chain dependencies on Asian material suppliers and a relatively high cost structure compared to Asian competitors. Research collaborations between national labs and semiconductor equipment manufacturers aim to develop next-generation focus ring materials.

Europe

Europe maintains a specialized position in the focus ring market through technology leadership in advanced materials from companies like CoorsTek and Greene Tweed. The region shows growing demand for silicon carbide rings in power semiconductor applications, particularly from automotive and industrial sectors. The EU’s €43 billion semiconductor industry support plan through the Chips Act is expected to boost local demand. However, limited domestic wafer fab scaling capabilities compared to Asia mean Europe remains more focused on material innovation than volume production of focus rings.

South America

The South American market for semiconductor focus rings remains nascent but shows potential as countries like Brazil develop basic semiconductor packaging and testing capabilities. Most focus ring demand in the region currently comes from maintenance and replacement needs in older semiconductor equipment rather than new installations. Limited local manufacturing capabilities mean the region remains entirely dependent on imports from Asia and North America. While some academic initiatives exist to develop local semiconductor expertise, significant market growth would require major foreign investment or government-led semiconductor programs.

Middle East & Africa

This emerging region is beginning to see semiconductor-related investments, particularly in the UAE and Saudi Arabia, creating new demand for semiconductor equipment components including focus rings. The market currently operates at a small scale, primarily serving maintenance needs for scientific and industrial equipment rather than volume semiconductor manufacturing. While long-term semiconductor development plans exist in several countries, the focus ring market is not expected to see significant expansion until major fabrication facilities are established. However, the region’s strategic location between Asia and Europe offers potential as a future logistics hub for semiconductor components.

Report Scope

This market research report provides a comprehensive analysis of the Global Semiconductor Focus Ring market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the semiconductor equipment industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 124 million in 2024 and is projected to reach USD 267 million by 2032 at a CAGR of 11.8%.

- Segmentation Analysis: Detailed breakdown by material type (Quartz, Silicon, Silicon Carbide, Others) and application (Wafer Etching, Others) to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with particular focus on semiconductor manufacturing hubs like Taiwan, South Korea, and Japan.

- Competitive Landscape: Profiles of leading market participants including Kallex, CoorsTek, Greene Tweed, and FerroTec, covering their product portfolios, manufacturing capabilities, and strategic developments.

- Technology Trends & Innovation: Assessment of advanced materials, plasma processing technologies, and integration with next-generation semiconductor fabrication techniques.

- Market Drivers & Restraints: Evaluation of factors including semiconductor industry growth, wafer size transitions, and the impact of geopolitical factors on supply chains.

- Stakeholder Analysis: Insights for semiconductor equipment manufacturers, foundries, material suppliers, and investors regarding market opportunities and challenges.

The research employs both primary and secondary methodologies, including interviews with industry experts, analysis of company financials, and validation through multiple data sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Semiconductor Focus Ring Market?

-> Semiconductor Focus Ring Market was valued at 124 million in 2024 and is projected to reach US$ 267 million by 2032, at a CAGR of 11.8% during the forecast period.

Which key companies operate in Global Semiconductor Focus Ring Market?

-> Key players include Kallex, Daewon, CoorsTek, Greene Tweed, Worldex, Max Luck Technology, Coma Technology, and FerroTec.

What are the key growth drivers?

-> Key growth drivers include increasing semiconductor manufacturing capacity, transition to larger wafer sizes, and demand for advanced plasma processing equipment.

Which region dominates the market?

-> Asia-Pacific dominates the market, accounting for over 60% of global semiconductor production, with strong demand from Taiwan, South Korea, and China.

What are the emerging trends?

-> Emerging trends include development of longer-lasting focus ring materials, integration with Industry 4.0 technologies, and sustainability initiatives in semiconductor manufacturing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...