MARKET INSIGHTS

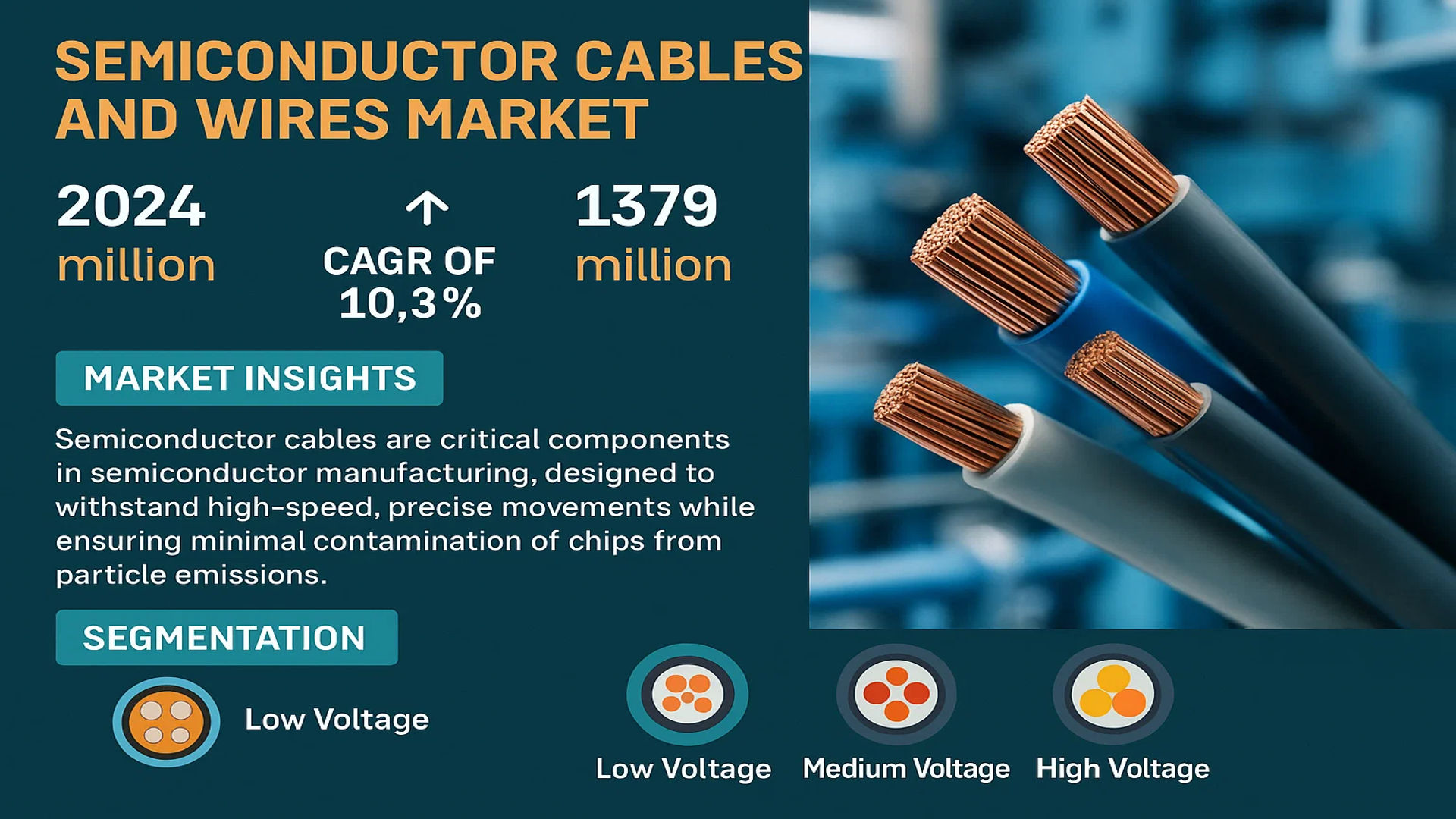

The global Semiconductor Cables and Wires Market was valued at 706 million in 2024 and is projected to reach US$ 1379 million by 2032, at a CAGR of 10.3% during the forecast period.

Semiconductor cables and wires are critical components in semiconductor manufacturing, designed to withstand high-speed, precise movements while ensuring minimal contamination of chips from particle emissions. These specialized cables facilitate efficient power transmission, signal integrity, and reliable connectivity in semiconductor fabrication equipment. They are categorized into low voltage, medium voltage, and high voltage segments, catering to diverse applications in mechanical equipment, instrumentation systems, information transmission, and power systems.

The market growth is driven by the rapid expansion of the semiconductor industry, which was valued at USD 579 billion in 2022 and is projected to reach USD 790 billion by 2029, growing at a CAGR of 6%. While segments like analog ICs and sensors showed strong growth (20.76% and 16.31% year-over-year in 2022, respectively), memory segments faced a decline. Increasing demand for IoT-based electronics and hybrid microprocessors further propels the need for advanced semiconductor cables and wires. Key players such as Helukabel, Gore, and LEONI are innovating to meet these evolving requirements.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Performance Computing and AI Applications Fuels Semiconductor Cable Adoption

The global semiconductor industry is undergoing a radical transformation driven by the exponential growth of artificial intelligence, 5G networks, and cloud computing. The average data center now requires up to 20% more high-performance cabling compared to traditional setups, with AI-specific workloads demanding ultra-low-latency connections. This technological shift is driving semiconductor manufacturers to adopt specialized cables and wires capable of handling higher frequencies while minimizing signal loss. As the AI chip market is projected to grow at 38% annually through 2030, semiconductor cables must evolve to support data transfer rates exceeding 112Gbps per lane for next-generation applications.

Automotive Semiconductor Boom Creates New Wiring Requirements

The automotive industry’s rapid electrification represents a significant growth driver, with electric vehicles requiring nearly 2.5 times more semiconductor content than conventional vehicles. Modern EV powertrains demand specialized high-voltage cables capable of operating in extreme temperature ranges (-40°C to 150°C) while maintaining flexibility and EMI shielding. The average premium electric vehicle now contains over 5 kilometers of specialized wiring, creating substantial demand for semiconductor-grade components. Additionally, advanced driver assistance systems (ADAS) require ultra-reliable connections for sensor arrays, with failure rates needing to remain below 0.1 parts per million to meet automotive safety standards.

Miniaturization Trend in Electronics Drives Innovation in Micro-Coaxial Solutions

Consumer electronics manufacturers continue pushing the boundaries of device miniaturization, with semiconductor cables now requiring diameters below 0.3mm while maintaining GHz-range transmission capabilities. The smartphone industry alone consumes approximately 18% of global semiconductor cables, with each flagship device containing multiple high-speed interconnects for cameras, displays, and sensors. This trend is accelerating the adoption of advanced materials such as liquid crystal polymer (LCP) insulation, which enables signal integrity at thicknesses impossible with traditional PTFE solutions. Recent innovations include flexible hybrid electronics that combine printed circuits with ultra-thin cabling for wearable medical devices and foldable displays.

MARKET RESTRAINTS

Material Shortages and Supply Chain Disruptions Constrain Market Growth

The semiconductor cable industry faces significant challenges from ongoing material shortages, particularly for specialty metals and high-performance polymers. Palladium-loaded dielectrics, crucial for high-frequency applications, have seen lead times extend beyond 26 weeks in recent quarters, while the price of ultra-pure copper conductors has fluctuated by as much as 40% annually. These supply chain issues are compounded by geopolitical factors affecting raw material availability, with certain rare earth elements becoming increasingly difficult to source at commercial scales. Manufacturers are struggling to maintain production volumes while meeting stringent semiconductor-grade purity requirements that often exceed 99.9999% for critical components.

Technical Challenges in High-Speed Signal Integrity Pose Development Hurdles

As data rates push beyond 112Gbps, semiconductor cables face fundamental physics challenges in maintaining signal integrity. Insertion loss becomes critical at these frequencies, with even 0.1dB/inch variations potentially causing system-level failures. The industry is witnessing growing instances of electromagnetic interference (EMI) in dense packaging environments, requiring complex shielding solutions that add weight and cost. Additionally, thermal management becomes increasingly difficult as power densities rise, with some high-performance computing applications generating over 500W per linear foot of cabling. These technical barriers significantly extend development cycles and qualification timelines for next-generation products.

MARKET CHALLENGES

Increasing Complexity of Qualification Standards Across Regions

Semiconductor cable manufacturers face mounting challenges from diverging international standards and certification requirements. The certification process for a single cable design can now exceed 18 months when accounting for all regional variations in safety, emissions, and material regulations. Automotive applications present particularly complex hurdles, with OEMs maintaining over 200 distinct specifications for wire and cable components. This regulatory environment creates substantial barriers to entry for smaller suppliers while forcing established players to maintain extensive testing facilities and certification teams. The situation is further complicated by emerging sustainability regulations that restrict certain traditional materials without commercially viable alternatives.

Workforce Shortages Impact Technical Manufacturing Capabilities

The semiconductor cable industry is experiencing critical shortages of skilled technicians capable of operating precision wire drawing and insulation equipment. Specialized positions such as high-frequency test engineers now command salary premiums exceeding 35% above industry averages, reflecting intense competition for limited talent pools. This skills gap is particularly acute in regions with aging workforces, where retirement rates outpace new technical education pipelines. Many manufacturers report that workforce limitations now constrain production capacity more than physical plant limitations, with some facilities operating at only 75% of potential output due to staffing challenges.

MARKET OPPORTUNITIES

Emerging Photonic Integration Creates New Hybrid Cable Demands

The convergence of electrical and optical signaling in semiconductor systems presents significant growth opportunities for hybrid cable solutions. Leading-edge data centers are deploying copper-photonic hybrid cables that combine 112Gbps electrical lanes with parallel optical channels in single assemblies. This emerging technology segment is projected to grow at 42% CAGR through 2030 as hyperscalers upgrade infrastructure. Additionally, the automotive lidar market is driving demand for specialized fiber-copper hybrid cables capable of handling both high-voltage power and multi-gigabit sensor data in harsh environments. These applications require entirely new cable architectures that combine the benefits of both transmission mediums.

Sustainability Initiatives Drive Demand for Recyclable and Bio-Based Materials

Growing environmental regulations and corporate sustainability commitments are creating strong market pull for eco-conscious semiconductor cable solutions. Several major OEMs have committed to using 50% recycled content in cabling by 2025, driving innovation in material science. Recent breakthroughs include insulation materials derived from plant-based polymers that maintain performance at temperatures up to 150°C while being fully compostable. The market for sustainable semiconductor cables is expected to triple within five years, with premium pricing of 15-20% above conventional products reflecting strong buyer willingness to pay for green solutions. This trend is particularly pronounced in European and North American markets where regulatory pressures are most intense.

SEMICONDUCTOR CABLES AND WIRES MARKET TRENDS

Rising Demand for High-Precision Manufacturing Drives Market Expansion

The semiconductor industry is experiencing a surge in demand for high-performance cables and wires due to the increasing complexity of semiconductor manufacturing processes. With the global semiconductor cables and wires market valued at US$ 706 million in 2024 and projected to reach US$ 1,379 million by 2032, growth is being driven by the need for components that can endure ultra-cleanroom environments while maintaining signal integrity. The industry’s shift toward 5nm and 3nm chip fabrication requires cables and wires with minimal particulate emissions and electromagnetic interference, making high-grade materials like fluoropolymers and specialized shielding essential.

Other Trends

Integration of IoT and AI Accelerates Innovation

The rapid adoption of IoT and AI-driven automation in semiconductor production is pushing the boundaries of cable and wire technology. Manufacturers are increasingly requiring flexible, heat-resistant cabling solutions that can withstand the rigorous motion of robotic arms and precision equipment. With the semiconductor industry projected to grow at a CAGR of 6% through 2029, particularly in segments like analog ICs (which saw 20.76% year-over-year growth in 2022), industry players are focusing on developing cables with enhanced durability and signal consistency to support next-generation automation.

Electrification of Automotive and Industrial Sectors Expands Applications

As the automotive and industrial sectors transition toward electrification, the demand for semiconductor-grade wiring is expanding beyond traditional foundry applications. The rise of electric vehicles (EVs) and smart manufacturing systems has created new requirements for high-voltage cabling that can operate reliably in extreme conditions. Semiconductor cables are now being engineered to handle higher current densities while maintaining thermal stability, particularly in power management applications. Additionally, the growing emphasis on miniaturization in electronic components is fueling development in ultra-thin, flexible cabling solutions with superior conductive properties for compact chip designs.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Suppliers Reinforce Market Position Through Innovation and Strategic Partnerships

The global semiconductor cables and wires market features a diverse mix of established and emerging players, with competition intensifying due to rising demand from semiconductor fabrication plants (fabs) and IoT-driven electronics. Helukabel and Staubli currently dominate the market, accounting for a combined revenue share of approximately 18-22% in 2024. Their leadership stems from proprietary cable technologies that minimize particle generation—a critical requirement in cleanroom semiconductor production environments.

BizLink and LEONI have significantly expanded their footprint through strategic acquisitions, with BizLink’s 2023 purchase of a German specialty cable manufacturer strengthening its EU market position. Meanwhile, Asian players like Totoku and Shanghai Electric are gaining traction through cost-competitive solutions tailored for high-volume memory chip production facilities.

The market is witnessing two distinct strategic approaches: Global players are investing heavily in R&D for ultra-low particulate cables compatible with extreme ultraviolet (EUV) lithography systems, while regional suppliers focus on optimizing supply chains to reduce lead times for replacement parts. This dual dynamic creates opportunities for collaboration, with several Tier 2 manufacturers now serving as authorized subcontractors for major brands.

Recent developments highlight the industry’s rapid evolution. Pfeiffer Vacuum launched a new line of vacuum-compatible cabling in Q1 2024, while MKS Instruments acquired a key polymer supplier to vertically integrate its high-purity wire production. Such moves indicate the growing emphasis on controlling material quality throughout the supply chain.

List of Key Semiconductor Cable and Wire Manufacturers

- Helukabel (Germany)

- W. L. Gore & Associates (U.S.)

- Staubli International AG (Switzerland)

- Comet Group (Switzerland)

- Totoku Electric Co., Ltd. (Japan)

- JEM Electronics, Inc. (U.S.)

- Schmalz GmbH (Germany)

- BizLink Holding Inc. (Taiwan)

- CeramTec GmbH (Germany)

- Allectra GmbH (Germany)

- Tatsuta Electric Wire & Cable Co., Ltd. (Japan)

- Pfeiffer Vacuum Technology AG (Germany)

- LEONI AG (Germany)

- Agilent Technologies, Inc. (U.S.)

- MKS Instruments, Inc. (U.S.)

Segment Analysis:

By Type

Low Voltage Cables Dominate Due to Widespread Use in Semiconductor Equipment

The market is segmented based on type into:

- Low Voltage

- Subtypes: Signal cables, Control cables, Data transmission cables

- Medium Voltage

- High Voltage

- Specialty Cables

- Subtypes: Ultra-high purity cables, Vacuum-grade cables, Radiation-resistant cables

By Application

Mechanical Equipment and Instrumentation Segment Leads Market Due to High Precision Requirements

The market is segmented based on application into:

- Mechanical Equipment and Instrumentation System

- Information Transmission System

- Power System

- Semiconductor Processing Equipment

By Material

Copper-based Cables Maintain Dominance for Superior Conductivity

The market is segmented based on material into:

- Copper

- Aluminum

- Gold-plated

- Special Alloys

By End User

Foundries Account for Largest Share Due to Massive Production Volumes

The market is segmented based on end user into:

- Semiconductor Foundries

- IDM (Integrated Device Manufacturers)

- OSAT (Outsourced Semiconductor Assembly and Test)

- Research Institutes

Regional Analysis: Semiconductor Cables and Wires Market

Asia-Pacific

The Asia-Pacific region dominates the global semiconductor cables and wires market, accounting for over 45% of total demand in 2024. This leadership position stems from China’s massive semiconductor fab expansion, with 31 new facilities planned or under construction through 2026. Taiwan, South Korea, and Japan contribute significantly through established semiconductor ecosystems requiring high-performance connectivity solutions. While cost-competitive manufacturers drive volume, the region is shifting toward higher-grade cables with EMI shielding to support advanced nodes below 10nm. Government initiatives like India’s $10 billion semiconductor incentive package further stimulate local demand, though supply chain maturity remains a challenge for emerging markets.

North America

With semiconductor production projected to grow 12% annually through 2030, North America presents stringent quality requirements for cables and wires in cleanroom environments. The CHIPS Act’s $52 billion funding accelerates domestic semiconductor manufacturing, creating demand for ultra-high purity cables that prevent particulate contamination. U.S. manufacturers emphasize robotic automation-compatible wiring with enhanced flex life ratings above 10 million cycles. However, reliance on Asian suppliers for certain specialty materials creates supply chain vulnerabilities that local players are addressing through vertical integration strategies.

Europe

Europe’s semiconductor cable market focuses on technical textiles integration and sustainability, with EU directives pushing for halogen-free flame-retardant materials in wafer handling applications. Germany’s strong industrial base drives demand for high-voltage power distribution cables in semiconductor equipment, while Nordic countries prioritize cryogenic-rated wiring for quantum computing research facilities. The region’s 15% import dependency on critical cable components has spurred R&D investments in alternative materials to mitigate supply risks, particularly for vacuum-compatible wiring systems.

South America

Brazil’s emerging semiconductor packaging industry creates niche opportunities for specialty cables, particularly in thermal management applications. However, the region represents less than 5% of global demand, constrained by limited local semiconductor manufacturing. Most cable requirements are met through imports from North America and Asia. Argentinian research institutions show growing interest in radiation-hardened cables for space applications, but commercial adoption remains limited without stronger government support for technology transfer programs.

Middle East & Africa

The Middle East’s semiconductor cable market centers on oil & gas sensor applications rather than chip manufacturing, with UAE and Saudi Arabia investing in fabless design houses that outsource production. South Africa’s mining sector drives demand for ruggedized instrumentation cables in semiconductor-based sensing equipment. While direct semiconductor application remains limited, the region shows potential for cable recycling technologies as global sustainability pressures increase, with several pilot projects underway for precious metal recovery from discarded wiring.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Semiconductor Cables and Wires markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Semiconductor Cables and Wires Market?

-> Semiconductor Cables and Wires Market was valued at 706 million in 2024 and is projected to reach US$ 1379 million by 2032, at a CAGR of 10.3% during the forecast period.

Which key companies operate in Global Semiconductor Cables and Wires Market?

-> Key players include Helukabel, Gore, Staubli, Comet, Totoku, JEM Electronics, Schmalz, BizLink, and CeramTec, among others.

What are the key growth drivers?

-> Key growth drivers include rising semiconductor manufacturing, demand for high-performance cables in IoT and automation, and increasing investments in semiconductor fabrication plants.

Which region dominates the market?

-> Asia-Pacific dominates the market, driven by semiconductor manufacturing hubs in China, Taiwan, South Korea, and Japan.

What are the emerging trends?

-> Emerging trends include miniaturization of semiconductor components, adoption of ultra-high purity materials, and integration of AI-driven quality control in cable manufacturing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...