Semiconductor Aluminum Alloy Vacuum Chamber Market Insights

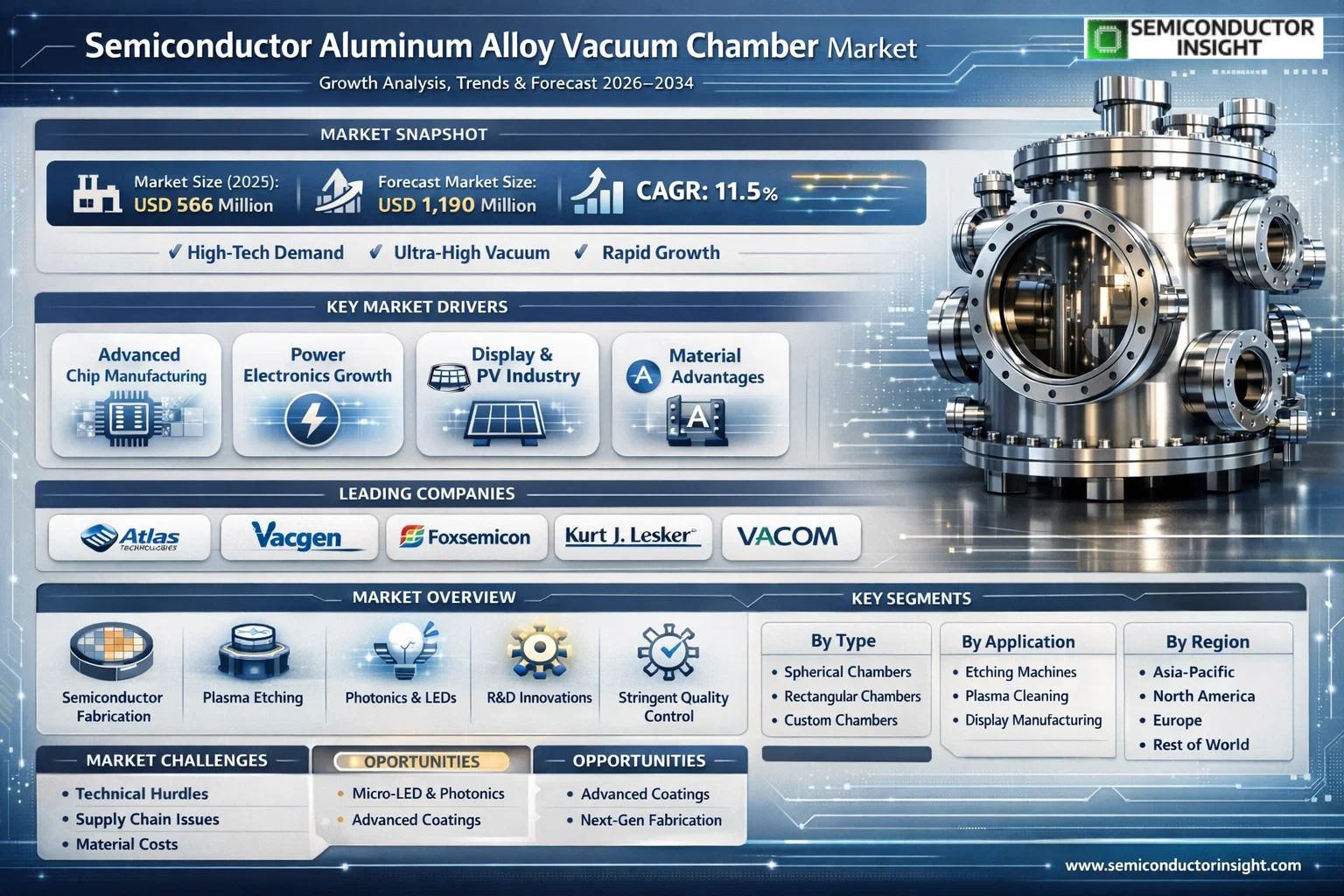

Global Semiconductor Aluminum Alloy Vacuum Chamber market size was valued at USD 566 million in 2025. The market is projected to grow from USD 631 million in 2026 to USD 1,190 million by 2034, exhibiting a CAGR of 11.5% during the forecast period.

Semiconductor Aluminum Alloy Vacuum Chambers are critical components used to create and maintain a controlled, low-pressure environment essential for advanced semiconductor manufacturing processes. These chambers facilitate key fabrication steps such as thin-film deposition, plasma etching, and ion implantation by providing an ultra-clean vacuum that minimizes contamination. Their construction from specialized aluminum alloys offers significant advantages over traditional materials like stainless steel, including lower magnetism, reduced outgassing of carbon-based impurities, and faster radioactive decay rates after particle bombardment,all crucial for producing high-yield, defect-free chips.

The market is experiencing robust growth driven by the relentless expansion of Global semiconductor industry and the increasing complexity of chip manufacturing nodes. The surge in demand for advanced logic and memory chips, power semiconductors for electric vehicles, and displays for consumer electronics directly fuels the need for high-performance vacuum processing equipment. However, technical challenges persist; achieving ultra-high vacuum seals with softer aluminum flanges remains an engineering hurdle that limits some applications. Key industry players like Atlas Technologies, Kurt J. Lesker Company, and Ferrotec are actively engaged in developing solutions to overcome these barriers and capitalize on the growing demand across applications such as plasma cleaning machines and etching systems.

MARKET DRIVERS

Demand Surge from Advanced Semiconductor Fabrication

The primary growth driver for Semiconductor Aluminum Alloy Vacuum Chamber Market is Global expansion of advanced node semiconductor manufacturing, particularly for sub-7nm processes. These processes require ultra-high vacuum environments for critical steps like atomic layer deposition and extreme ultraviolet lithography. Aluminum alloys, especially the 6061 and 7075 series, are preferred for their excellent strength-to-weight ratio, machinability, and outgassing properties, making them ideal for constructing the large, complex chambers needed in modern fabs.

Investment in Compound Semiconductor and R&D

Growth in power electronics and photonics, utilizing materials like silicon carbide and gallium nitride, is creating a secondary demand stream. The fabrication of these compound semiconductors also relies on precise vacuum environments. Concurrently, significant R&D investment in quantum computing and advanced packaging (e.g., 3D ICs) is pushing the specifications for vacuum chambers, requiring custom-engineered aluminum alloy components capable of maintaining pristine conditions for sensitive quantum and heterogeneous integration processes.

➤ The market is projected to grow at a CAGR of approximately 8.5% over the next five years, directly correlated with the number of new wafer fab projects announced worldwide.

Furthermore, the industry’s shift towards larger wafer sizes and cluster tool configurations necessitates larger, more integrated vacuum chambers, directly benefiting suppliers who can provide monolithic or welded aluminum alloy structures that minimize potential leak points compared to assemblies.

MARKET CHALLENGES

High Technical and Manufacturing Barriers

A central challenge in Semiconductor Aluminum Alloy Vacuum Chamber Market is the extreme technical precision required. Chambers must achieve and maintain ultra-high vacuum levels, often below 1×10⁻⁹ Torr, which demands flawless welding techniques, superior surface finishes, and meticulous cleaning to prevent contamination. Any porosity or impurity in the aluminum alloy can lead to virtual leaks and process yield loss, making quality control paramount and expensive.

Other Challenges

Material Supply Chain and Cost Volatility

The aerospace-grade aluminum alloys required are subject to global supply chain fluctuations and commodity pricing. Disruptions can delay chamber production and increase costs for equipment OEMs.

Competition from Alternative Materials

While aluminum dominates, specific high-temperature processes create niches for stainless steel or specialized coatings, pressuring aluminum alloy chamber makers to continuously innovate in thermal management and surface treatment.

MARKET RESTRAINTS

Cyclical Nature of Semiconductor Capital Expenditure

Semiconductor Aluminum Alloy Vacuum Chamber Market is inherently tied to the capital expenditure cycles of chip manufacturers. During downturns, fab expansions and tool purchases are delayed or canceled, leading to a direct and immediate reduction in demand for new vacuum chambers. This cyclicality makes long-term production planning and inventory management difficult for chamber manufacturers, who must maintain high technical expertise even during slow market periods.

Long Replacement Cycles and High Durability

Restraining new sales is the exceptional durability and long service life of well-manufactured aluminum alloy vacuum chambers. With proper maintenance, these chambers can remain in operation for decades. Unless a fab is upgrading to a new process technology that requires a completely different chamber geometry or material specification, the need for a direct replacement is infrequent, limiting the aftermarket to components like seals and viewports rather than entire chamber structures.

MARKET OPPORTUNITIES

Expansion into Emerging Fabrication Frontiers

Significant opportunities exist beyond traditional logic and memory fabs. The rapid commercial scaling of micro-LED displays and silicon photonics requires dedicated, high-throughput vacuum process tools. Semiconductor Aluminum Alloy Vacuum Chamber Market is poised to supply specialized chambers for these applications, where size, vacuum integrity, and compatibility with novel precursor chemistries are critical.

Adoption of Advanced Manufacturing and Coatings

The integration of technologies like additive manufacturing for complex internal geometries and the development of novel anodizing or ceramic-based coatings present a key opportunity. These innovations can enhance chamber performance by improving pumping speed, reducing particle generation, and extending maintenance intervals, creating value-added, higher-margin products within the market.

Semiconductor Aluminum Alloy Vacuum Chamber Market Trends

Material Science Innovation Overcoming Technical Constraints

A key trend in Semiconductor Aluminum Alloy Vacuum Chamber Market is focused on overcoming the material’s intrinsic challenges to meet advanced manufacturing demands. While advantageous for low magnetism, high thermal conductivity, and fast radioactive decay, aluminum’s softer texture has historically limited its use in ultra-high vacuum (UHV) applications requiring metal seals. Ongoing research and development is targeting advanced aluminum treatments, alloy compositions, and engineered flange designs that enhance hardness and compatibility with UHV sealing technologies. This continuous improvement in material performance is broadening the application scope for these vacuum chambers in critical fabrication tools, including etching systems and deposition equipment.

Other Trends

Specialization for Advanced Applications

There is a rising demand for chambers customized for specific semiconductor processes. Chambers are being designed with materials like Al-Mg-Sc alloys or with inner surface treatments to minimize particulate generation and reduce contamination from carbon-based gases. This is particularly crucial for next-generation nodes and power semiconductor manufacturing, where chamber cleanliness and vacuum integrity directly impact device yield and performance.

Strategic Focus on Process Integration and Supply Chain

Manufacturers are increasingly collaborating with equipment makers and semiconductor fabricators to offer integrated vacuum solutions. This trend moves beyond selling standardized chambers to providing fully tested assemblies that incorporate components like pumps, gauges, and valves. Such integration ensures system compatibility and reliability. Concurrently, the market’s supply chain is evolving to manage the specialized machining, welding, and finishing required for high-performance aluminum alloy vacuum chambers, with players strengthening their technical service and support capabilities globally.

COMPETITIVE LANDSCAPE

Key Industry Players

A concentrated market with global leaders and specialized regional suppliers

Global Semiconductor Aluminum Alloy Vacuum Chamber market is characterized by a consolidated competitive environment where a handful of established global players command significant market share. The market leaders, such as Atlas Technologies, Kurt J. Lesker, and Ferrotec, possess extensive expertise in vacuum technology and have established strong relationships with major semiconductor equipment manufacturers. These companies lead through their advanced engineering capabilities, comprehensive product portfolios for critical applications like plasma cleaning and etching machines, and robust global sales and support networks. Market concentration is driven by high technical barriers, including the need for ultra-high vacuum integrity, precise machining of aluminum alloys, and stringent certification processes required by the semiconductor fabrication industry. Significant investment in R&D to overcome challenges related to aluminum’s softness and sealing compatibility is a key differentiator for these top firms.

Beyond the dominant leaders, the competitive landscape includes several significant players that cater to specific niches or regional markets. Companies like VACOM and Keller Technology are recognized for high-precision components, while Asian manufacturers such as Foxsemicon and Chung-Hsin Electric and Machinery Manufacturing Corp. (CHEM) hold strong positions in the vital Asia-Pacific market, offering competitive solutions for display panel and photovoltaic manufacturing segments. Other notable participants, including Diener Electronic and Htc Vacuum, focus on specialized subsystems or cost-competitive offerings. The market is further populated by technology-focused firms driving innovation in aluminum alloy treatments and magnetic permeability reduction, crucial for next-generation semiconductor processes. Strategic activities such as mergers, acquisitions, and partnerships aimed at expanding technological capabilities and geographic reach are common among key competitors.

List of Key Semiconductor Aluminum Alloy Vacuum Chamber Companies Profiled

- Atlas Technologies

- Kurt J. Lesker Company

- Vacgen Ltd.

- Foxsemicon Integrated Technology Inc.

- VACOM GmbH

- Keller Technology Corporation

- Diener Electronic GmbH & Co. KG

- GNB Corporation

- Chung-Hsin Electric and Machinery Manufacturing Corp. (CHEM)

- Ferrotec (USA) Corporation

- Htc Vacuum

- Changqiao Vacuum Technology

- MKS Instruments

- Pfeiffer Vacuum

- IHI Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Spherical Vacuum Chamber is a prominent segment due to inherent structural and performance advantages in semiconductor manufacturing environments.

|

| By Application |

|

The Etching Machine application is fundamentally the leading and most demanding segment for aluminum alloy vacuum chambers.

|

| By End User |

|

Semiconductor Integrated Circuit Fabs constitute the most sophisticated and quality-intensive end-user segment.

|

| By Manufacturing Complexity |

|

The demand is strongest for Custom-Engineered & Multi-Port Chambers, which represent the high-value segment.

|

| By Primary Material Advantage |

|

The Ultra-High Vacuum & Purity advantage is the foundational driver for aluminum alloy adoption over traditional materials.

|

Regional Analysis: Semiconductor Aluminum Alloy Vacuum Chamber Market

Asia-Pacific

The Asia-Pacific region’s market leadership is built on its unparalleled concentration of integrated device manufacturers and pure-play foundries. This high density of major customers creates a localized, high-volume demand center for Semiconductor Aluminum Alloy Vacuum Chamber Market, attracting global equipment suppliers and fostering a competitive, innovation-driven local vendor ecosystem.

National industrial policies, such as China’s “Made in China 2025” and similar initiatives in Japan, South Korea, and India, provide critical financial and regulatory support for semiconductor manufacturing expansion. These policies drive the construction of new fabs and the modernization of existing ones, directly increasing procurement for advanced aluminum alloy vacuum chamber systems.

As the primary location for cutting-edge process node development and high-volume manufacturing, Asia-Pacific fabs are early and aggressive adopters of the latest deposition and etching technologies. This necessitates the use of next-generation Semiconductor Aluminum Alloy Vacuum Chambers designed for extreme vacuum integrity and compatibility with advanced process chemistries.

A mature supporting industry for high-grade aluminum alloys, precision machining, and specialized surface coatings (like anodization and high-purity polishing) has developed locally. This ecosystem reduces lead times and costs for chamber manufacturers and provides rapid on-site maintenance and refurbishment services, enhancing overall market efficiency.

North America

North America maintains a strategically vital position in Semiconductor Aluminum Alloy Vacuum Chamber Market, characterized by demand driven by leading-edge R&D and specialized manufacturing. The presence of major semiconductor equipment OEMs and intensive research into future nodes, including compound semiconductors and advanced packaging, creates a need for highly customized, research-grade vacuum chambers. Major fab investments in the United States, spurred by the CHIPS Act, are generating significant new demand for advanced fabrication tools. This region focuses heavily on innovation, requiring aluminum alloy chambers that support experimental processes and extreme specifications, which influences global design and material standards for the broader market.

Europe

The European market for Semiconductor Aluminum Alloy Vacuum Chambers is defined by specialized, high-value manufacturing and a strong focus on sustainability and precision engineering. Demand is anchored by key players in power semiconductors, MEMS, and specialized sensors, where vacuum integrity and chamber reliability are paramount. Stringent environmental and safety regulations influence chamber design, promoting the use of high-recyclability aluminum alloys and cleaner manufacturing processes. Collaborative research initiatives between academic institutions and equipment suppliers drive advancements in chamber materials science, particularly for applications in quantum computing and photonics, fostering a niche but technologically sophisticated market segment.

South America

Semiconductor Aluminum Alloy Vacuum Chamber Market in South America is nascent but developing, primarily serving regional assembly, testing, and packaging (ATP) operations and niche industrial applications. Market growth is linked to gradual increases in regional electronics production and technology investments in countries like Brazil. Demand is currently for standardized, cost-effective chamber solutions rather than highly advanced R&D systems. The market faces challenges related to import dependence for high-end components and limited local technical expertise for advanced fabrication, but represents a potential long-term growth area as regional industrial capabilities expand.

Middle East & Africa

This region represents an emerging frontier in Semiconductor Aluminum Alloy Vacuum Chamber Market, driven by ambitious national diversification strategies, particularly in the Gulf Cooperation Council (GCC) nations. Large-scale investments aimed at building knowledge-based economies include pledges to develop semiconductor design and limited manufacturing capabilities. Initial demand is expected to stem from research institutions, pilot production lines, and related high-tech industries entering the ecosystem. The market dynamics are currently shaped by technology transfer partnerships and the establishment of initial infrastructure, with a focus on acquiring foundational fabrication tools, including essential vacuum processing equipment.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor Aluminum Alloy Vacuum Chamber Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor Aluminum Alloy Vacuum Chamber Market?

-> Global Semiconductor Aluminum Alloy Vacuum Chamber Market was valued at USD 566 million in 2025 and is projected to reach USD 1190 million by 2034, growing at a CAGR of 11.5% during the forecast period.

Which key companies operate in Semiconductor Aluminum Alloy Vacuum Chamber Market?

-> Key players include Atlas Technologies, Vacgen, Foxsemicon, Kurt J. Lesker, VACOM, Keller Technology, Diener Electronic, GNB Corporation, Chung-Hsin Electric and Machinery Manufacturing Corp. (CHEM), and Ferrotec, among others.

What are the key growth drivers?

-> Key growth drivers include the widespread use in pan-semiconductor industries (integrated circuits, photovoltaics, display panel manufacturing), the material advantages of aluminum alloy such as low carbon content, lower magnetism, and faster radioactive decay, which reduce damage during semiconductor circuit manufacturing.

Which region dominates the market?

-> The U.S. and China are significant markets. The U.S. market size was estimated at USD million in 2025, while China is expected to reach USD million.

What are the emerging trends?

-> Emerging trends include the development and application in specific equipment like plasma cleaning machines and etching machines, alongside continuous innovation to overcome challenges in achieving ultra-high vacuum environments with aluminum alloy flanges.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...