Semiconductor Advanced Packaging Materials Market Insights

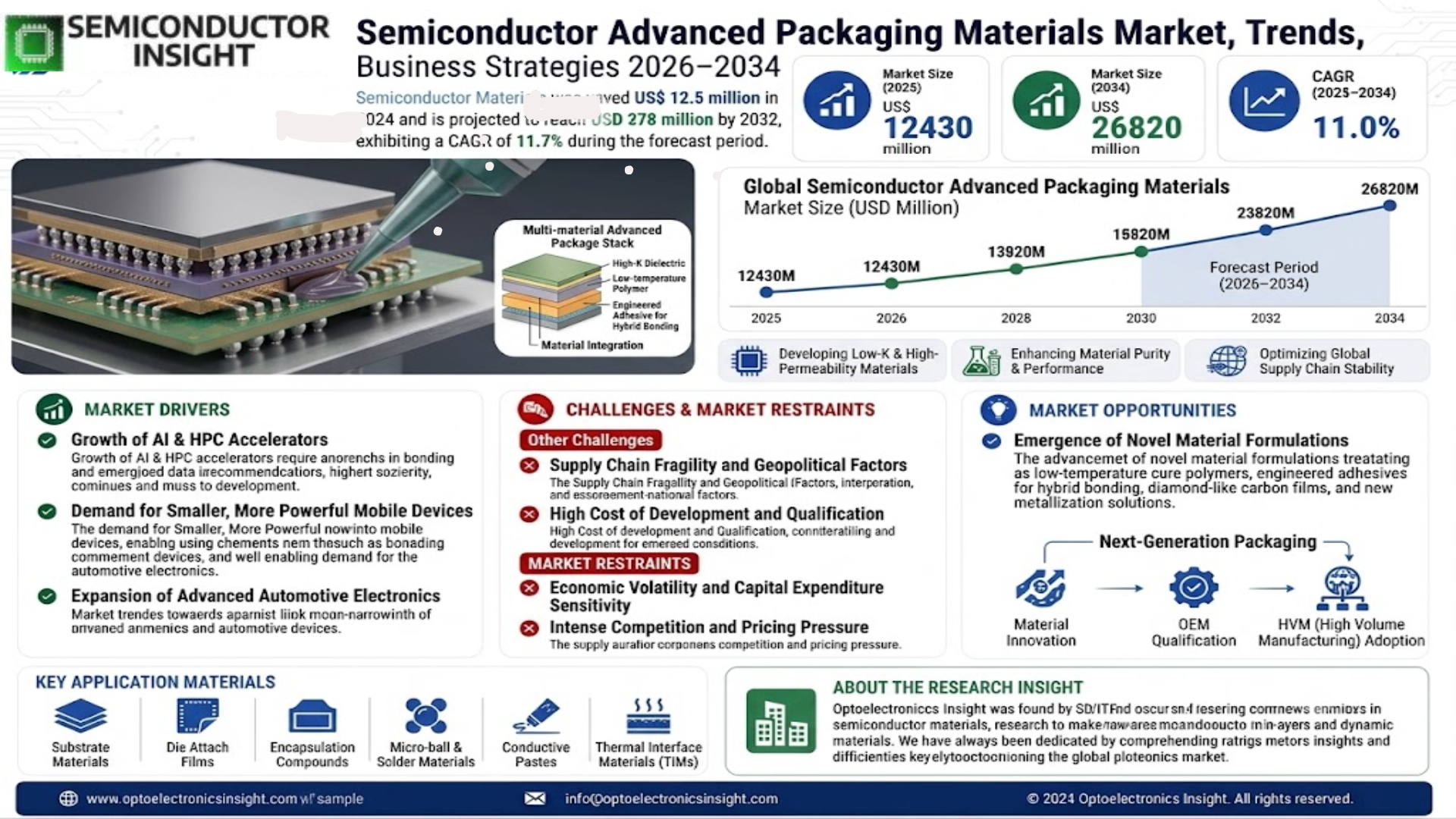

Global Semiconductor Advanced Packaging Materials market size was valued at USD 12.43 billion in 2025. The market is projected to grow from USD 13.79 billion in 2026 to USD 26.82 billion by 2034, exhibiting a CAGR of 11.0% during the forecast period.

Semiconductor advanced packaging materials are specialized substrates and compounds essential for protecting and interconnecting integrated circuits (ICs) in modern, high-density electronic packages. These materials facilitate critical functions such as electrical connection, thermal management, and mechanical support for chips, enabling technologies like flip-chip (FC), wafer-level chip-scale packaging (WLCSP), and ball grid array (BGA). Key material categories include FC Package Substrates (like ABF), WB Package Substrates, underfill, die attach materials (paste and wire), epoxy molding compounds, and others.

The market is experiencing robust growth driven by several factors, including the relentless demand for miniaturization and higher performance in consumer electronics, the proliferation of 5G infrastructure, and the expansion of high-performance computing (HPC) and artificial intelligence applications. Furthermore, the automotive sector’s increasing semiconductor content for electric vehicles and advanced driver-assistance systems (ADAS) is a significant contributor. Strategic initiatives by key players also fuel innovation; for instance, leading substrate manufacturers like Unimicron and Ibiden are continuously expanding capacity to meet demand. Other prominent players operating in this market with extensive portfolios include Shinko Electric Industries, AT&S, Kyocera, Henkel, Shin-Etsu Chemical, and Sumitomo Bakelite.

MARKET DRIVERS

Demand for Miniaturization and Heterogeneous Integration

The relentless push for smaller, more powerful, and energy-efficient electronic devices is a primary catalyst. As traditional Moore’s Law scaling faces physical and economic limits, the semiconductor industry increasingly relies on advanced packaging technologies like 2.5D, 3D-IC, and fan-out wafer-level packaging (FOWLP) to continue performance gains. This architectural shift fundamentally drives demand for specialized Semiconductor Advanced Packaging Materials, including advanced substrates, high-performance dielectrics, and underfills.

Proliferation of AI, HPC, and 5G/6G Infrastructure

Artificial intelligence, high-performance computing, and next-generation communications require immense data processing at lightning speeds. These applications utilize complex chiplet designs and high-density interconnects, which are impossible without sophisticated packaging. Materials enabling superior thermal management, signal integrity, and mechanical stability are critical, directly boosting the Semiconductor Advanced Packaging Materials Market.

➤ Advanced packaging is no longer just an option but a strategic imperative for continued semiconductor innovation, with the materials segment forming its foundational backbone.

Global semiconductor capacity expansion, particularly for leading-edge nodes, further solidifies this demand. Major foundries and integrated device manufacturers are making multi-billion-dollar investments in new fabrication and packaging facilities, creating a long-term, stable pipeline for material suppliers.

MARKET CHALLENGES

Extreme Technical Complexity and Integration Hurdles

The development and integration of new materials present significant technical challenges. Materials must meet exacting requirements for coefficient of thermal expansion (CTE) matching, ultra-low dielectric constant (low-k), high thermal conductivity, and exceptional reliability under stress. Achieving this while ensuring compatibility with complex, multi-step packaging processes is a formidable barrier for material science.

Other Challenges

Supply Chain Fragility and Geopolitical Factors

The market is highly dependent on specialized chemical and material suppliers, with certain key raw materials facing concentration risks. Geopolitical tensions and trade policies can disrupt this delicate supply chain, causing volatility in availability and pricing for critical Semiconductor Advanced Packaging Materials.

High Cost of Development and Qualification

The R&D investment required to create novel materials is substantial. Furthermore, the qualification cycle with OEMs and foundries is lengthy and expensive, often taking years. This high barrier to entry can slow innovation and limit the participation of smaller material science companies in the advanced packaging ecosystem.

MARKET RESTRAINTS

Economic Volatility and Capital Expenditure Sensitivity

The semiconductor industry is cyclical, and capital expenditure on new equipment and materials is highly sensitive to macroeconomic conditions. During downturns, investments in next-generation packaging technologies can be delayed or scaled back, directly impacting the Semiconductor Advanced Packaging Materials Market growth in the short to medium term.

Intense Competition and Pricing Pressure

The market, while growing, features intense competition among established chemical giants and specialized material firms. This environment, coupled with the constant cost-reduction demands from high-volume semiconductor manufacturers, creates significant pricing pressure. Maintaining profitability while funding continuous innovation is a persistent restraint for material suppliers.

MARKET OPPORTUNITIES

Emergence of Novel Material Formulations

Significant opportunities lie in developing next-generation materials. This includes low-temperature cure polymers, engineered adhesives for hybrid bonding, diamond-like carbon films for thermal interfaces, and new metallization solutions. Companies that can innovate in substrates, thermal interface materials (TIMs), and conductive pastes to meet future performance benchmarks will capture substantial market share.

Expansion into Automotive and IoT Applications

While AI and HPC are current drivers, the long-term growth of the Semiconductor Advanced Packaging Materials Market will be fueled by automotive electrification, autonomous driving, and the proliferation of IoT devices. These applications require packaging that offers high reliability under harsh conditions, creating a robust demand for durable, high-performance materials tailored for these environments.

Sustainability and Circular Economy Initiatives

Increasing regulatory and consumer focus on sustainability presents a forward-looking opportunity. Developing eco-friendly, halogen-free, recyclable, or bio-based advanced packaging materials can provide a distinct competitive advantage and align with corporate sustainability goals, opening new market segments and customer partnerships.

Key Semiconductor Advanced Packaging Materials Market Trends

Demand Driven by Heterogenous Integration and AI Hardware

The primary trend shaping the Semiconductor Advanced Packaging Materials Market is the shift towards heterogenous integration to meet the demands of artificial intelligence and high-performance computing. This architectural approach, which combines multiple chiplets within a single package, critically depends on advanced substrates like ABF, sophisticated underfill epoxies, and high-performance die attach materials. These materials are essential for managing the increased thermal loads and signal integrity challenges presented by densely packed, high-power chips, making material innovation a cornerstone for next-generation semiconductor performance.

Other Trends

Material Innovations for Substrate and Interconnect

A significant trend involves accelerated innovation in substrate and interconnect materials, particularly for FC-CSP and advanced BGA packages. Developments in Ajinomoto Build-up Film (ABF) substrates to support finer line spacing and new formulations of underfill materials with enhanced flow properties and reduced thermal stress are critical. These innovations directly address the needs for higher I/O density and improved reliability in 5G, automotive, and consumer electronics applications within the Semiconductor Advanced Packaging Materials Market.

Geographic Supply Chain Recalibration

The market is experiencing a strategic recalibration of the supply chain, with increased investment in advanced packaging materials capacity across Southeast Asia and efforts to bolster domestic capabilities in North America and Europe. This trend, driven by geopolitical factors and the need for supply resilience, is influencing capital expenditure among leading material suppliers and substrate manufacturers, potentially altering competitive dynamics over the medium term.

Convergence with Sustainability Directives

Environmental regulations and corporate sustainability goals are becoming a tangible influence on the Semiconductor Advanced Packaging Materials Market. This is prompting research into halogen-free epoxy molding compounds, lead-free die attach pastes, and the development of materials with lower curing temperatures to reduce energy consumption during manufacturing. This trend aligns material performance requirements with broader environmental, social, and governance (ESG) criteria across the semiconductor industry.

COMPETITIVE LANDSCAPE

Key Industry Players

A Market Defined by Specialized Material Science and Global Supply Chains

Global Semiconductor Advanced Packaging Materials market is a highly concentrated and technical arena, primarily led by established Asian manufacturers specializing in critical substrate technologies. Dominance in this sector is rooted in expertise with materials like Ajinomoto Build-up Film (ABF) substrates, which are essential for flip-chip (FC) and wafer-level chip-scale packaging (WLCSP). Companies such as Unimicron (Taiwan), Ibiden (Japan), and Nan Ya PCB (Taiwan) collectively command a significant share of Global revenue, establishing a strong oligopoly, particularly in the high-growth FC package substrate segment. These leaders are deeply integrated with major semiconductor foundries and OSATs (Outsourced Semiconductor Assembly and Test providers), driving innovation for applications in consumer electronics, high-performance computing, and 5G infrastructure. The competitive dynamic is characterized by intensive R&D investment to develop materials with finer pitches, higher thermal conductivity, and lower dielectric loss to meet the demands of next-generation advanced packaging architectures like 2.5D/3D IC integration.

Beyond the substrate giants, the landscape includes a diverse range of specialized and niche players supplying other essential materials. This includes global chemical corporations like Henkel and NAMICS in underfill and die-attach pastes, Japanese leaders such as Shin-Etsu Chemical and Resonac in molding compounds and high-purity chemicals, and key suppliers like MacDermid Alpha and Indium Corporation in solders and thermal interface materials. Competition in these segments is driven by formulations that ensure reliability under thermal stress and miniaturization. Furthermore, companies like AT&S and Shinko Electric Industries are expanding their technological portfolios to capture growth, while regional players in China and South Korea are rapidly scaling to secure their positions in the domestic and global supply chain, making the market both collaborative and intensely competitive.

List of Key Semiconductor Advanced Packaging Materials Companies Profiled

- Unimicron

- Ibiden Co., Ltd.

- Nan Ya PCB

- Shinko Electric Industries Co., Ltd.

- Kinsus Interconnect Technology Corp.

- AT&S

- SEMCO

- Kyocera Corporation

- TOPPAN Inc.

- Zhen Ding Technology Holding Limited

- Henkel AG & Co. KGaA

- NAMICS Corporation

- Resonac Holdings Corporation

- MacDermid Alpha Electronics Solutions

- Shin-Etsu Chemical Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

FC Package Substrate (FC-CSP and ABF) continues to be the foundation for high-performance and miniaturized chip packaging, driving its leadership position. This material is indispensable for enabling fine-line circuitry and high-density interconnects in modern processors and application-specific integrated circuits. Its critical role is further amplified by the relentless demand for greater functionality in smaller form factors, particularly within cutting-edge consumer electronics and data center applications, ensuring it remains a high-value and technically demanding segment for material suppliers. |

| By Application |

|

High Performance Computing (HPC) is the most demanding and innovation-driven application segment, setting the pace for material requirements. The computational intensity of artificial intelligence, machine learning, and advanced data analytics necessitates packaging materials with exceptional thermal management, signal integrity, and reliability. This segment consistently pushes the boundaries, adopting novel substrate technologies and underfill formulations to manage heat dissipation and power delivery in complex multi-chip modules and 3D architectures, thereby serving as a primary research and development focus for material science innovators. |

| By End User |

|

Foundries & IDMs (Integrated Device Manufacturers) represent the primary and most influential end-user segment, exerting significant pull on material specifications and supply chains. These companies, which design and manufacture their own chips, develop deep collaborative partnerships with material suppliers to co-engineer solutions for their most advanced nodes and packaging technologies. This segment’s pursuit of performance and integration creates a concentrated demand for high-margin, specialty materials, making it a critical strategic customer base that drives long-term material roadmaps and qualification cycles. |

| By Material Innovation Focus |

|

Thermal Management Materials are experiencing the most pronounced research and development activity as power densities continue to escalate. Innovations in thermally conductive underfills, interface materials, and advanced epoxy molding compounds are paramount to prevent overheating and ensure long-term operational stability in compact devices. The ability to effectively dissipate heat has become a key differentiator for packaging performance, especially in automotive electrification and HPC systems where failure is not an option, placing immense value on materials that offer superior thermal conductivity without compromising mechanical or electrical properties. |

| By Integration Level |

|

2.5D & 3D-IC Packaging stands as the frontier for integration, presenting unique and sophisticated material challenges that command premium solutions. These architectures require specialized materials such as temporary bonding adhesives for wafer handling, ultrafine-pitch micro-bump alloys, and highly uniform dielectric layers for silicon interposers. The complexity of stacking multiple dies vertically or placing them side-by-side on an interposer creates intense demand for materials that ensure mechanical stability, manage heterogeneous thermal expansion, and provide exceptional electrical isolation, positioning this segment as the highest-value arena for material science breakthroughs. |

Regional Analysis: Global

Asia-Pacific

The region’s strength stems from its complete semiconductor value chain, from design and wafer fabrication to ATP. This concentration creates a synergistic pull for advanced packaging materials, enabling rapid prototyping, close collaboration between material suppliers and packaging houses, and streamlined supply logistics that are critical for time-to-market in fast-evolving segments.

National policies across the Asia-Pacific, including China’s “Made in China 2025” and similar programs in South Korea and Taiwan, prioritize semiconductor self-sufficiency. These initiatives directly fund and incentivize the development of domestic capabilities in advanced packaging and the underlying critical materials, reducing reliance on foreign sources and shaping long-term market dynamics.

A dense network of specialized chemical and material companies exists to serve the local packaging industry. This ecosystem is characterized by rapid innovation cycles, with suppliers developing next-generation epoxy molding compounds, low-loss substrate materials, and advanced thermal solutions tailored to the specific requirements of leading-edge logic and memory packaging.

Leadership in manufacturing devices for artificial intelligence, 5G infrastructure, and automotive electronics ensures sustained, high-value demand for advanced packaging materials. The performance requirements of these applications,such as extreme miniaturization and heat dissipation,are primary drivers for material innovation and premiumization within the regional Semiconductor Advanced Packaging Materials Market.

North America

North America remains a critical hub for innovation and high-value design in the Semiconductor Advanced Packaging Materials Market. The region is home to major fabless semiconductor companies and integrated device manufacturers (IDMs) that drive specifications for next-generation packaging architectures like chiplets and 3D system-in-package (SiP). This design leadership creates a “pull-through” effect, where material requirements are defined early in the development cycle. A strong base of specialized material science firms and equipment suppliers supports this ecosystem through R&D in novel polymers, dielectrics, and conductive adhesives. The market dynamic is characterized by a close-knit collaboration between OEMs, packaging consortia (like IMEC USA), and material innovators to overcome technical bottlenecks, ensuring a steady pipeline of advanced solutions that later proliferate to high-volume manufacturing regions.

Europe

The European Semiconductor Advanced Packaging Materials Market is defined by a focus on specialized, high-reliability applications and strategic initiatives to bolster technological sovereignty. Strong automotive and industrial sectors demand packaging materials that meet stringent longevity and performance standards under harsh conditions, driving demand for robust underfills, high-temperature mold compounds, and specialized substrates. The European Chips Act is catalyzing investment across the semiconductor value chain, including in packaging R&D and pilot lines, which will stimulate demand for advanced materials. The regional landscape features a network of specialized chemical companies and research institutes excelling in material science for niche applications, positioning Europe as a leader in quality and innovation for specific segments rather than competing in high-volume, mainstream packaging.

South America

Participation in Global Semiconductor Advanced Packaging Materials Market from South America is currently nascent but shows potential for gradual integration into select supply chains. The region’s role is primarily as a consumer of packaged semiconductor devices for its telecommunications, automotive, and consumer electronics industries, which indirectly influences material specifications demanded by global suppliers. Efforts to develop a more significant local electronics manufacturing base could, over the long term, create localized demand for foundational packaging materials. However, the current market dynamic is characterized by import dependency, with any significant advancement tied to foreign direct investment and technology transfer agreements with established players from leading regions in the Semiconductor Advanced Packaging Materials Market.

Middle East & Africa

The Middle East & Africa region represents an emerging and strategically motivated participant in the broader semiconductor landscape, with implications for the Semiconductor Advanced Packaging Materials Market over the long horizon. Nations, particularly in the Gulf Cooperation Council (GCC), are making substantial sovereign investments to diversify their economies and establish high-tech sectors, which includes ambitions in semiconductor design and potentially niche packaging capabilities. While a local market for advanced packaging materials is virtually non-existent today, these strategic investments could lead to the establishment of specialized R&D facilities or pilot packaging lines. This would initially generate demand for materials on a smaller, innovation-focused scale, positioning the region as a future niche player rather than a volume driver in the near term.

Report Scope

This market research report provides a comprehensive analysis of the Semiconductor Advanced Packaging Materials Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Semiconductor Advanced Packaging Materials Market?

-> Global Semiconductor Advanced Packaging Materials Market was valued at USD 12430 million in 2025 and is projected to reach USD 26820 million by 2034, growing at a CAGR of 11.0% during the forecast period.

Which key companies operate in Semiconductor Advanced Packaging Materials Market?

-> Key players include Unimicron, Ibiden, Nan Ya PCB, Shinko Electric Industries, Kinsus Interconnect, AT&S, Semco, Kyocera, TOPPAN, and Zhen Ding Technology, among others. In 2025, Global top five players held a significant revenue share.

What are the key growth drivers?

-> Key growth drivers include increasing demand from end-use industries like Consumer Electronics, Automotive, IoT, 5G, and High Performance Computing, coupled with technological advancements in packaging solutions such as FC, WB, and WLCSP.

Which region dominates the market?

-> Asia is a major market, with significant contributions from China, Japan, and South Korea. The U.S. market is also a key estimated segment in North America.

What are the emerging trends?

-> Emerging trends include the rising adoption of advanced packaging materials like FC Package Substrate (ABF), Underfill, and Epoxy Molding Compounds, driven by the miniaturization and performance requirements of next-generation semiconductors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...