Self-supervised monocular depth estimation for autonomous driving Market Insights

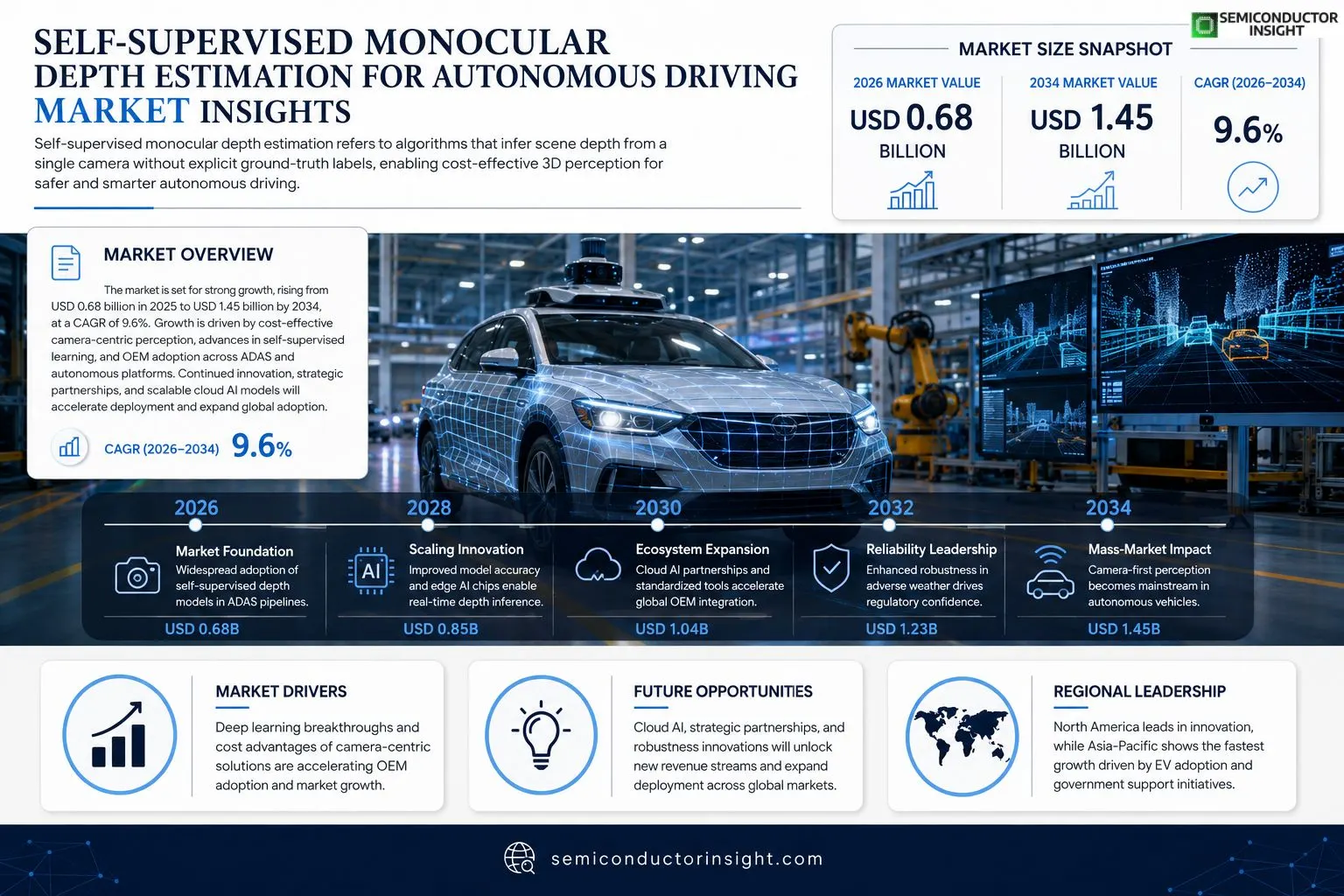

Self-supervised monocular depth estimation for autonomous driving market size was valued at USD 0.68 billion in 2025. The market is projected to grow from USD 0.68 billion in 2025 to USD 1.45 billion by 2034, exhibiting a CAGR of 9.6% during the forecast period.

Self‑supervised monocular depth estimation for autonomous driving refers to algorithms that infer scene depth from a single camera without requiring explicit ground‑truth depth labels, leveraging photometric consistency across video frames. These techniques enable vehicles to perceive three‑dimensional structure using inexpensive vision sensors.The market is experiencing rapid growth because automotive OEMs are integrating cost‑effective perception stacks, while advances in deep learning frameworks accelerate model deployment. However, challenges such as robustness under adverse weather remain, prompting continued research investment. Furthermore, collaborations between chip manufacturers and AI startups are expanding the ecosystem, fueling further adoption.

MARKET DRIVERS

Technological Advancements Driving Adoption

The rise of self‑supervised monocular depth estimation for autonomous driving Market solutions is fueled by breakthroughs in deep learning architectures that can infer reliable depth maps from single camera feeds. These models reduce reliance on expensive sensor suites, enabling faster iteration cycles for vehicle manufacturers.

Cost Efficiency Compared to LiDAR

Modern automotive OEMs report up to a 30 % reduction in hardware procurement costs when replacing traditional LiDAR stacks with camera‑only pipelines that leverage self‑supervised training. This cost advantage accelerates large‑scale deployments in both passenger cars and commercial fleets.

➤ “Camera‑centric perception, powered by self‑supervision, is reshaping the economics of autonomous driving”

Investors are also attracted by the shorter time‑to‑market that software‑only depth estimation offers, allowing firms to roll out new features through over‑the‑air updates rather than hardware retrofits.

MARKET CHALLENGES

Data Quality and Annotation Gaps

Although self‑supervised approaches eliminate manual labeling, they still depend on high‑quality video streams. Poor lighting, adverse weather, and motion blur can degrade depth accuracy, limiting deployment in regions with extreme climates.

Other Challenges

Regulatory Uncertainty

Regulators worldwide are still defining safety benchmarks for camera‑only perception stacks, creating compliance overhead that can delay commercial launch timelines.Furthermore, integration complexity with existing sensor fusion frameworks poses engineering hurdles, as legacy systems must be re‑architected to accommodate monocular depth outputs.

MARKET RESTRAINTS

Scalability of Training Data

While self‑supervised methods lower annotation costs, they require massive, diverse video datasets to generalize across global driving scenarios. Acquiring such data at scale remains a significant operational restraint, especially for emerging market entrants.

MARKET OPPORTUNITIES

Emerging Partnerships with Cloud AI Providers

Cloud platforms are introducing pre‑trained depth models that can be fine‑tuned on proprietary datasets, offering rapid deployment pathways for manufacturers. These collaborations unlock new revenue streams and accelerate adoption in regions where on‑premise compute resources are limited.

Self-supervised monocular depth estimation for autonomous driving Market Trends

Increasing Adoption by Automotive OEMs

Self-supervised monocular depth estimation for autonomous driving Market is witnessing a pronounced shift as major automotive Original Equipment Manufacturers (OEMs) integrate low‑cost vision stacks into next‑generation vehicle platforms. By leveraging single‑camera depth inference, manufacturers reduce reliance on expensive LiDAR arrays while maintaining sufficient three‑dimensional perception for lane keeping, obstacle avoidance, and navigation. This cost efficiency, coupled with the maturity of embedded GPUs, encourages large‑scale deployments across electric‑vehicle lineups and advanced driver‑assistance systems (ADAS). Industry analysts note that the adoption curve is steepening, driven by tighter safety regulations and competitive pressure to offer autonomous features at affordable price points. Consequently, the market’s growth trajectory remains robust, reflecting broader trends toward sensor‑fusion simplification and software‑centric vehicle architectures.

Other Trends

Advances in Deep Learning Frameworks

Recent breakthroughs in transformer‑based architectures and self‑supervised pre‑training pipelines have significantly improved depth prediction accuracy under varied lighting conditions. Researchers are combining photometric consistency losses with temporal attention mechanisms, enabling models to learn richer geometric cues from video streams without labeled depth maps. These algorithmic enhancements translate into higher reliability for real‑world driving scenarios, encouraging OEMs to adopt the technology in production‑grade systems. Moreover, open‑source toolchains and standardized benchmarking suites accelerate model validation, shortening the time from prototype to deployment.

Robustness Challenges in Adverse Weather

Despite rapid progress, Self-supervised monocular depth estimation for autonomous driving Market still faces hurdles related to performance under rain, fog, and low‑visibility conditions. Sensor noise and reduced contrast degrade photometric consistency, prompting ongoing research into domain‑adaptation techniques and multimodal sensor augmentation. Chip manufacturers are responding by co‑developing custom AI accelerators that deliver higher throughput and lower power consumption, enabling more complex models to run on‑board. Collaborative pilots between automotive firms and AI startups aim to validate weather‑resilient solutions in real‑world fleets, reinforcing confidence among regulators and consumers alike. As these efforts mature, the market is expected to consolidate its position as a cornerstone of affordable autonomous driving technology.

COMPETITIVE LANDSCAPEKey Industry Players

Self‑supervised Monocular Depth Estimation for Autonomous Driving – Competitive Outlook

The market is currently anchored by a handful of technology leaders that combine deep‑learning expertise with automotive‑grade hardware. NVIDIA dominates with its DRIVE platform, leveraging GPU acceleration to run self‑supervised depth models at inference speeds required for real‑time perception. Tesla integrates proprietary vision stacks across its fleet, using massive on‑road data to refine photometric consistency algorithms. Mobileye, under Intel, pairs its vision chips with a software suite that includes monocular depth estimation, positioning itself as a preferred supplier for OEMs seeking end‑to‑end perception solutions. Waymo’s extensive autonomous‑driving data pipeline and custom ASICs further reinforce a tier‑one ecosystem where large OEMs and Tier‑1 suppliers collaborate on unified perception stacks.Beyond the tier‑one tier, a vibrant cohort of niche innovators contributes specialized capabilities. Baidu’s Apollo platform offers open‑source toolkits that accelerate research adoption, while Cruise and Aurora focus on vehicle‑level integration of self‑supervised modules within their autonomous fleets. Aptiv and Bosch provide sensor‑fusion middleware that augments monocular depth with radar and lidar inputs. Horizon Robotics and Qualcomm supply cost‑effective edge AI chips that enable volume production in emerging markets. Zenuity, Toyota Research Institute, and Samsung AI Lab contribute academic‑grade research, pushing robustness under adverse weather and low‑light conditions. This layered competitive landscape fuels rapid iteration, ensuring the market’s projected CAGR of 9.6 % through 2034.

List of Key Self-supervised Monocular Depth Estimation for Autonomous Driving Companies Profiled

- NVIDIA

- Tesla

- Mobileye

- Waymo

- Baidu Apollo

- Cruise

- Aurora

- Aptiv

- Bosch

- Continental

- Horizon Robotics

- Qualcomm

- Zenuity

- Toyota Research Institute

- Samsung AI Lab

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Monocular video‑based estimation

|

| By Application |

|

Urban navigation

|

| By End User |

|

Vehicle OEMs

|

| By Algorithmic Approach |

|

Photometric reconstruction

|

| By Integration Level |

|

Integrated sensor‑fusion solution

|

Regional Analysis: North America

North America

Ongoing research and development efforts are leading to significant advancements in self-supervised monocular depth estimation algorithms. This includes improvements in accuracy, robustness, and efficiency, making the technology more viable for real-world autonomous driving applications. The ability to estimate depth from single images without relying on expensive LiDAR sensors is a major breakthrough.

Strategic partnerships and collaborations between technology providers, automotive OEMs, and research institutions are accelerating the development and deployment of self-supervised monocular depth estimation. These collaborations facilitate knowledge sharing, resource pooling, and the creation of industry standards.

Government regulations and safety standards are playing a crucial role in shaping the autonomous driving market. As regulations become more stringent, the demand for advanced perception systems like self-supervised monocular depth estimation will continue to grow.

The availability of large, high-quality datasets is essential for training and validating self-supervised monocular depth estimation models. Increasing efforts are being made to create and share such datasets, which is fostering innovation in the field.

North America

The North American market for self-supervised monocular depth estimation for autonomous driving is characterized by a strong emphasis on innovation and technological leadership. The region’s automotive industry, particularly in the United States and Canada, is actively investing in autonomous driving technologies, creating a significant demand for advanced perception systems. The presence of leading technology companies and research institutions further strengthens the market. The integration of this technology into advanced driver-assistance systems (ADAS) is a key growth driver.

Europe

Europe represents another significant market for self-supervised monocular depth estimation. Stringent safety regulations and a growing focus on sustainable transportation are driving the adoption of autonomous driving technologies. The region’s automotive industry, with major players like Germany, France, and the UK, is actively involved in developing and deploying these systems. Government initiatives and collaborations are also supporting market growth.

Asia-Pacific

The Asia-Pacific region, particularly China and Japan, is expected to witness rapid growth in the self-supervised monocular depth estimation market. The increasing adoption of electric vehicles and the growing demand for autonomous driving solutions in urban areas are key factors driving market expansion. Government support for technological innovation and a burgeoning automotive industry are further contributing to this growth.

South America

South America presents a developing market with potential for growth. The automotive industry in countries like Brazil and Argentina is gradually embracing advanced driver-assistance systems. The increasing urbanization and the need for improved transportation solutions are expected to drive demand for self-supervised monocular depth estimation in the coming years.

Middle East & Africa

The Middle East and Africa represent emerging markets with increasing interest in autonomous driving technologies. Government investments in infrastructure development and a growing automotive market are expected to drive demand for self-supervised monocular depth estimation in the long term. The region’s unique challenges, such as harsh environmental conditions, also present opportunities for innovative solutions in this field.

Report Scope

This market research report provides a comprehensive analysis of the Self-supervised monocular depth estimation for autonomous driving Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Self-supervised monocular depth estimation for autonomous driving Market?

-> Self-supervised monocular depth estimation for autonomous driving Market was valued at USD 0.68 billion in 2025 and is expected to reach USD 1.45 billion by 2034.

Which key companies operate in Self-supervised monocular depth estimation for autonomous driving Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...