Security Processor Chip Market Insights

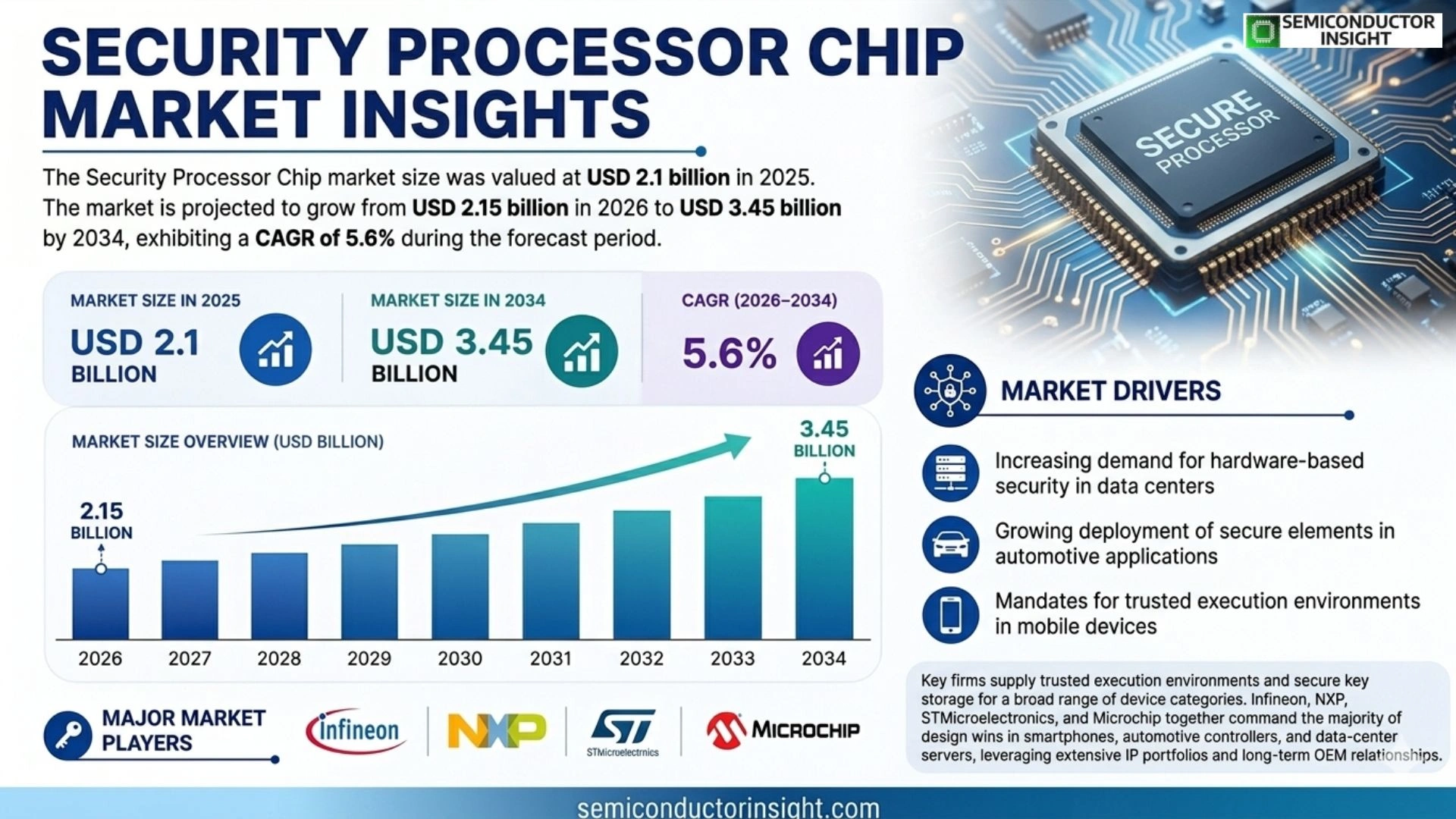

Global Security Processor Chip market size was valued at USD 2.1 billion in 2025. The market is projected to grow from USD 2.15 billion in 2026 to USD 3.45 billion by 2034, exhibiting a CAGR of 5.6 % during the forecast period.

Security processor chips are dedicated hardware modules that execute cryptographic algorithms, provide secure key storage, and host trusted execution environments across devices such as smartphones, IoT gateways, automotive controllers, and data‑center servers.

The market is experiencing rapid growth because of expanding IoT deployments, heightened demand for secure cloud services, and stricter automotive safety regulations; furthermore, rising cyber‑threat awareness pushes enterprises toward hardware‑based protection solutions. Leading vendors including Infineon Technologies, NXP Semiconductors, STMicroelectronics and Microchip Technology are driving innovation through new product launches and strategic partnerships.

MARKET DRIVERS

Rising Demand for Hardware‑Based Security

Security Processor Chip market is being propelled by heightened concerns over data breaches, prompting enterprises to adopt dedicated security processors that isolate cryptographic functions from general‑purpose CPUs. This architectural separation reduces attack surfaces and improves compliance with stringent regulations.

Proliferation of IoT and Edge Devices

Rapid expansion of connected sensors and edge gateways creates a critical need for tamper‑resistant processing, driving OEMs to embed security chips at the silicon level. The resulting market traction is evident in a steady increase in design wins across automotive, industrial, and consumer segments.

➤ ‘Hardware security becomes the default, not the exception, as data protection moves from software patches to silicon guarantees.’

Investors are also responding positively, with venture capital flows favoring startups that specialize in secure enclave technologies, further accelerating product pipelines and reinforcing the growth trajectory of Security Processor Chip market.

MARKET CHALLENGES

Complex Integration with Existing Architectures

Integrating dedicated security processors into legacy systems often requires redesign of firmware and validation of secure boot processes, which can extend time‑to‑market and increase engineering overhead. Companies must balance performance gains against potential compatibility issues.

Other Challenges

Supply Chain Constraints

Global semiconductor shortages have limited the availability of high‑performance silicon, causing lead times to stretch and pricing pressure to rise, thereby constraining the pace of adoption for many manufacturers.

MARKET RESTRAINTS

High Development Costs

Designing and certifying security processor chips demand significant R&D investment, including extensive validation against cryptographic standards and side‑channel attack mitigation. These cost barriers can deter smaller players and limit the overall market expansion.

MARKET OPPORTUNITIES

Emerging AI‑Driven Security Solutions

Artificial‑intelligence algorithms are being integrated into security processors to enable real‑time anomaly detection and adaptive encryption. This convergence opens new revenue streams, particularly in high‑value sectors such as finance and critical infrastructure, where predictive security is becoming a decisive competitive advantage.

Security Processor Chip Market Trends

Rising Adoption in IoT and Edge Devices

Security Processor Chip market is witnessing a pronounced shift as manufacturers embed dedicated cryptographic modules into a broader range of connected products. Smartphones, IoT gateways, and data‑center servers increasingly rely on these chips to execute encryption algorithms, protect secret keys, and establish trusted execution environments. This hardware‑based approach addresses the limitations of software‑only protection, delivering lower latency and stronger isolation for critical workloads. As enterprises expand cloud services and edge computing, the demand for built‑in security at the silicon level continues to accelerate.

Other Trends

Automotive Safety and Trusted Execution Environments

Automotive controllers are another focal point for Security Processor Chip market. Stricter safety regulations and the rise of autonomous driving functions require robust protection of firmware and sensor data. Chip vendors such as Infineon Technologies and NXP Semiconductors have introduced processors that integrate secure key storage and runtime attestation, enabling vehicles to verify software integrity in real time. These capabilities reduce the risk of malicious code injection and support compliance with emerging automotive cybersecurity standards.

Strategic Partnerships and Innovation

Leading suppliers,including STMicroelectronics and Microchip Technology,are deepening collaborations with cloud providers and OEMs to co‑develop next‑generation security solutions. Joint development programs focus on enhancing hardware‑rooted trust, expanding support for post‑quantum cryptography, and streamlining integration with heterogeneous system‑on‑chip architectures. By aligning product roadmaps with industry demands, these partnerships accelerate time‑to‑market for secure silicon and reinforce the overall resilience of Security Processor Chip market.

COMPETITIVE LANDSCAPE

Key Industry Players

Security Processor Chip Market – Competitive Overview

The security processor segment is currently anchored by a handful of large semiconductor firms that supply trusted execution environments and secure key storage to a broad range of device categories. Infineon Technologies, NXP Semiconductors, STMicroelectronics and Microchip Technology together command the majority of design wins in smartphones, automotive controllers and data‑center servers, leveraging extensive IP portfolios and long‑term OEM relationships. Their product roadmaps emphasize integration of hardware‑based cryptography with low‑power enclaves, enabling compliance with emerging automotive safety standards and data‑privacy regulations. These incumbents also benefit from strategic partnerships with cloud providers and IoT platform vendors, reinforcing a market structure that favours scale, reliability and certification depth.

Beyond the dominant quartet, a diverse set of niche innovators contributes to market depth and specialization. Texas Instruments and Renesas Electronics focus on embedded security for industrial and automotive edge devices, while Broadcom and Qualcomm embed secure cores within networking and communications silicon. Samsung Electronics and MediaTek bring integrated security modules to consumer‑grade SoCs, and Intel and AMD explore secure enclaves for server‑grade processors. Huawei’s HiSilicon, ON Semiconductor and Marvell Technology round out the competitive field with region‑specific solutions and differentiated cryptographic accelerators, sustaining a vibrant ecosystem of specialty providers that address emerging use‑cases such as secure AI inference and edge‑to‑cloud authentication.

List of Key Security Processor Chip Companies Profiled

- Infineon Technologies

- NXP Semiconductors

- STMicroelectronics

- Microchip Technology

- Texas Instruments

- Renesas Electronics

- Broadcom

- Qualcomm

- Samsung Electronics

- Intel

- AMD

- MediaTek

- Huawei HiSilicon

- ON Semiconductor

- Marvell Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Secure Enclave Processors

|

| By Application |

|

IoT Gateways

|

| By End User |

|

Enterprises

|

| By Architecture |

|

ARM‑based Secure Processors

|

| By Security Feature |

|

Hardware Root of Trust

|

Regional Analysis: North America

United States

Government funding for cybersecurity research and development significantly impacts Security Processor Chip market. Initiatives aimed at securing critical infrastructure and protecting sensitive data drive demand for advanced security chip solutions.

The financial industry’s relentless pursuit of robust security measures fuels the demand for secure processor chips. Protecting financial transactions and customer data is paramount, driving investment in hardware security modules (HSMs) and other specialized chips.

The proliferation of Internet of Things (IoT) devices presents significant security challenges, creating a need for secure processor chips at the edge. Securing these devices and the data they generate is a key market driver.

Cloud computing security is a major focus, leading to increased demand for security processor chips that can enhance data protection and access control within cloud environments.

Europe

Europe is steadily strengthening its position Security Processor Chip market, spurred by growing concerns about data security and privacy regulations like GDPR. The region’s focus on building a strong domestic semiconductor industry, alongside increasing cybersecurity investments across various sectors, is fostering market expansion. European enterprises are increasingly adopting hardware-based security solutions to meet stringent regulatory requirements and protect sensitive data. Collaboration between public and private entities is also playing a vital role in driving innovation and market growth within the region’s Security Processor Chip Market. The emphasis on secure communication and data sovereignty presents promising opportunities for specialized security chip designs.

Asia-Pacific

Asia-Pacific represents a dynamic and rapidly growing market for Security Processor Chips. The region’s burgeoning digital economy, coupled with increasing cyber threats, is driving substantial demand for robust security solutions. Government initiatives focused on digital transformation and cybersecurity are further fueling market expansion. Countries like China, Japan, and South Korea are significant consumers and manufacturers of security processor chips, creating a vibrant ecosystem. The increasing adoption of cloud services and the proliferation of IoT devices in Asia-Pacific contribute significantly to the region’s market growth. The demand for secure mobile devices and data protection is particularly strong in this region.

South America

South America exhibits a moderate growth trajectory Security Processor Chip market. Increasing awareness of cyber threats and the growing adoption of digital technologies are driving demand for security solutions. The financial sector and government agencies are key consumers of security processor chips in the region, seeking to protect sensitive data and critical infrastructure. While the market is relatively nascent compared to North America and Asia-Pacific, it presents considerable potential for future growth as digital adoption continues to expand.

Middle East & Africa

The Middle East & Africa region is witnessing nascent but promising growth Security Processor Chip market. Rising cyber threats, coupled with increasing investments in digital infrastructure, are creating demand for security solutions. Government initiatives focused on cybersecurity and the growing adoption of smart city technologies are contributing to market expansion. The financial sector and government agencies are key drivers of demand in this region, seeking to protect critical infrastructure and sensitive data. As digital transformation accelerates across the region, Security Processor Chip market is expected to witness significant growth in the coming years.

Report Scope

This market research report provides a comprehensive analysis of the Security Processor Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Security Processor Chip Market?

-> Security Processor Chip market was valued at USD 2.1 billion in 2025 and is expected to reach USD 3.45 billion by 2034, exhibiting a CAGR of 5.6 % during the forecast period.

Which key companies operate Security Processor Chip Market?

-> Key players include Infineon Technologies, NXP Semiconductors, STMicroelectronics, Microchip Technology.

What are the key growth drivers?

-> Key growth drivers include expanding IoT deployments, heightened demand for secure cloud services, stricter automotive safety regulations, and rising cyber‑threat awareness.

Which region dominates the market?

-> Regional dominance information is not detailed in the provided data.

What are the emerging trends?

-> Emerging trends include hardware‑based security solutions, integration of AI/IoT for secure processing, and increased adoption of trusted execution environments in automotive and data‑center applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...