Secure Digital Hardware Market Insights

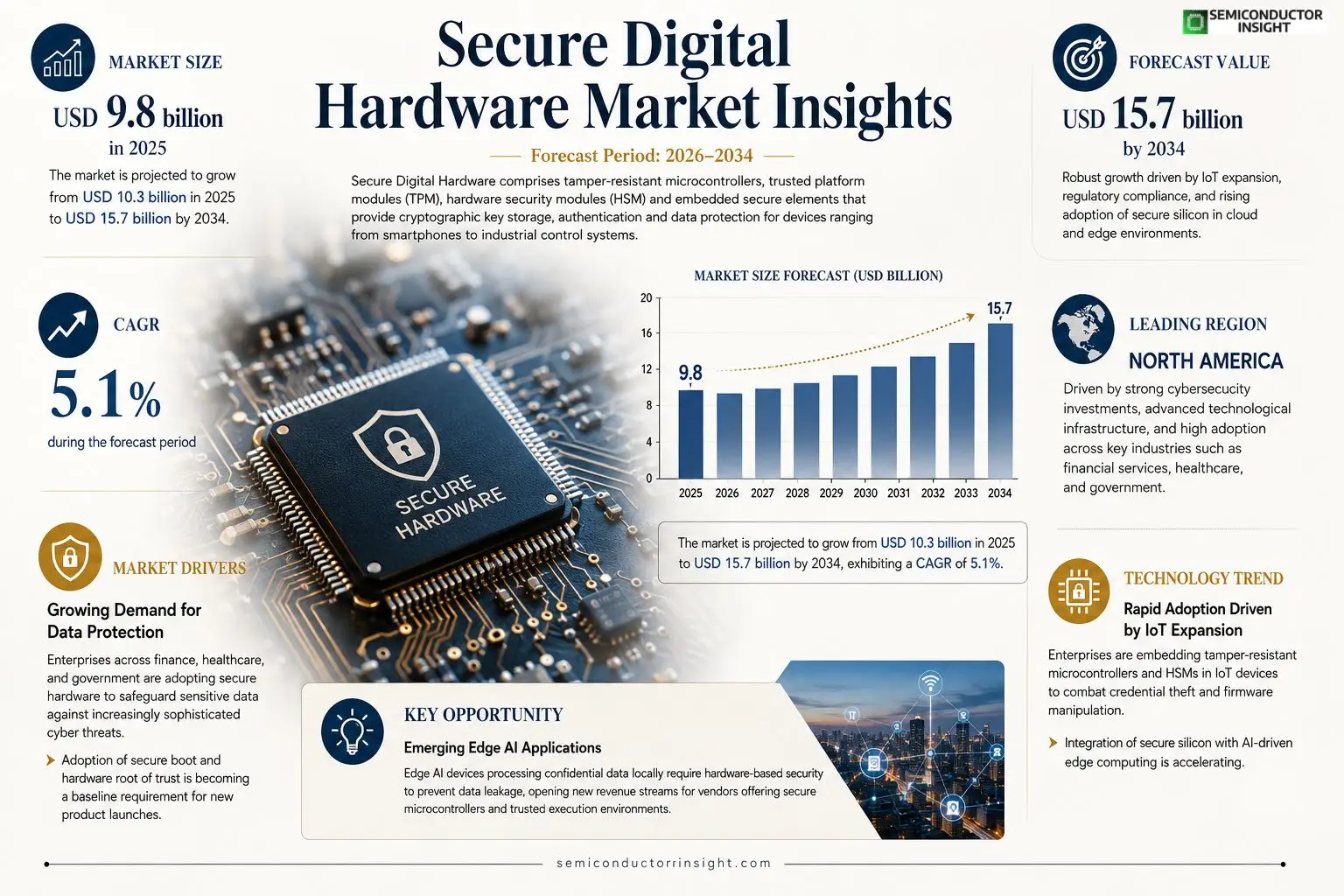

Secure Digital Hardware market size was valued at USD 9.8 billion in 2025. The market is projected to grow from USD 10.3 billion in 2025 to USD 15.7 billion by 2034, exhibiting a CAGR of 5.1% during the forecast period.

Secure Digital Hardware comprises tamper‑resistant microcontrollers, trusted platform modules (TPM), hardware security modules (HSM) and embedded secure elements that provide cryptographic key storage, authentication and data protection for devices ranging from smartphones to industrial control systems.The market is experiencing rapid expansion because cyber‑security concerns are intensifying across enterprises and governments; however, the surge in IoT deployments and stringent data‑privacy regulations further accelerate demand for robust hardware‑based protection. Furthermore, cloud service providers are integrating secure hardware into their infrastructure to ensure workload isolation. Key players such as Infineon Technologies, NXP Semiconductors, STMicroelectronics and Microchip Technology continue to innovate with next‑generation secure silicon solutions.

MARKET DRIVERS

Growing Demand for Data Protection

Enterprises across finance, healthcare, and government are adopting to safeguard sensitive data against increasingly sophisticated cyber threats. The shift toward edge computing and IoT devices amplifies the need for tamper‑resistant hardware, driving investment in encrypted processors and secure element solutions.

Regulatory Compliance Pressure

Stringent regulations such as GDPR, CCPA, and industry‑specific standards (e.g., HIPAA, PCI‑DSS) compel organizations to implement hardware‑based encryption, accelerating market growth. Companies view secure hardware as a cost‑effective path to achieve compliance while maintaining operational efficiency.

➤ Adoption of secure boot and hardware root of trust is becoming a baseline requirement for new product launches.

Finally, the rise of cloud‑native workloads and zero‑trust architectures encourages a move away from purely software‑based security, positioning hardware security modules as essential components in modern IT ecosystems.

MARKET CHALLENGES

High Initial Capital Expenditure

Deploying secure hardware often requires substantial upfront investment in specialized chips, firmware development, and integration services, which can deter small‑ and medium‑sized enterprises from rapid adoption.

Other Challenges

Complex Integration Processes

Integrating encrypted hardware into legacy systems can be technically demanding, requiring cross‑functional expertise and extended testing cycles that delay time‑to‑market.Additionally, a shortage of qualified engineers with cryptographic hardware experience further exacerbates deployment timelines and costs.

MARKET RESTRAINTS

Supply Chain Constraints

semiconductor shortages and limited foundry capacity for security‑focused chips constrain the ability of vendors to meet rising demand, creating lead‑time uncertainties for buyers.Furthermore, geopolitical tensions affecting key component manufacturers introduce additional risk, prompting some customers to reconsider sourcing strategies.The need for rigorous certification (e.g., FIPS 140‑2) adds another layer of delay, as products must undergo extensive testing before market entry.

MARKET OPPORTUNITIES

Emerging Edge AI Applications

Edge AI devices processing confidential data locally require hardware‑based security to prevent data leakage, opening new revenue streams for vendors offering secure microcontrollers and trusted execution environments.In parallel, the expansion of 5G networks creates demand for secure base‑station hardware, where built‑in encryption can protect massive data flows and support network slicing security.Finally, increasing interest from the automotive sector in secure over‑the‑air updates and encrypted in‑vehicle networks presents a sizable growth avenue for .

Secure Digital Hardware Market Trends

Rapid Adoption Driven by IoT Expansion

was valued at US $9.8 billion in 2025 and is projected to reach US $15.7 billion by 2034, reflecting robust demand across multiple sectors. Enterprises are increasingly embedding tamper‑resistant microcontrollers and hardware security modules within IoT devices to protect against credential theft and firmware manipulation. Cloud service providers are also integrating secure silicon to guarantee workload isolation, reinforcing the market’s upward trajectory. This convergence of cybersecurity imperatives and the massive rollout of connected sensors accelerates procurement cycles and encourages large‑scale deployments of trusted platform modules.

Other Trends

Regulatory Influence

Stringent data‑privacy regulations such as GDPR, CCPA and emerging national cybersecurity statutes compel organizations to adopt hardware‑based encryption solutions. Compliance audits now require cryptographic key storage that cannot be accessed through software exploits, driving the uptake of secure elements and hardware security modules. Government procurement policies in Europe and Asia increasingly mandate the use of tamper‑resistant components for critical infrastructure, creating a predictable pipeline of contracts that sustains market growth. As regulators expand the scope of required protections, vendors are compelled to certify their products against evolving standards, reinforcing confidence among enterprise buyers.

Competitive Innovation Landscape

Leading suppliersincluding Infineon Technologies, NXP Semiconductors, STMicroelectronics and Microchip Technologyare launching next‑generation secure silicon that supports post‑quantum cryptography, low‑power operation, and integrated secure boot. These advancements address the expanding attack surface of edge devices while meeting the power budgets of battery‑operated sensors. Collaborative initiatives between semiconductor firms and cloud providers accelerate the development of standardized APIs for hardware‑based key management, enabling seamless integration across heterogeneous environments. The competitive pressure to deliver higher security assurance with minimal latency is shaping product roadmaps and reinforcing ’s position as a cornerstone of modern cyber‑defense strategies.

COMPETITIVE LANDSCAPEKey Industry Players

Secure Digital Hardware Market – Competitive Overview

continues to be anchored by a handful of technology powerhouses that dominate both revenue and innovation pipelines. Infineon Technologies, NXP Semiconductors, STMicroelectronics, and Microchip Technology collectively account for a sizeable share of the tamper‑resistant microcontroller and trusted platform module segments, leveraging deep R&D capabilities to ship next‑generation secure silicon that meets stringent automotive, industrial, and cloud‑infrastructure requirements. Their extensive IP portfolios, design‑win programs, and strategic alliances with OEMs reinforce a tiered market structure where these leaders serve as platform suppliers, while a smaller cohort of specialized vendors focuses on niche form‑factors and custom secure element solutions.Beyond the core quartet, a diverse set of niche players contributes to the market’s vibrancy. Texas Instruments and Renesas Electronics provide competitively priced secure MCU families for embedded IoT devices, while Samsung Electronics and Qualcomm deliver secure elements integrated into mobile platforms. Broadcom and Cypress (now part of Infineon) address high‑speed networking and automotive safety applications. Companies such as Maxim Integrated, Analog Devices, and Marvell Technology are expanding into hardware security modules for data‑center workloads, and emerging firms like Giesecke & Devrient and Cryptographic Solutions are targeting government‑grade secure key storage. This fragmented layer of innovators sustains rapid feature evolution and price competition across the market’s value chain.

List of Key Secure Digital Hardware Companies Profiled

- Infineon Technologies

- NXP Semiconductors

- STMicroelectronics

- Microchip Technology

- Texas Instruments

- Renesas Electronics

- Samsung Electronics

- Qualcomm

- Broadcom

- Analog Devices

- Maxim Integrated

- Marvell Technology

- Giesecke & Devrient

- Cryptographic Solutions

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Tamper‑Resistant Microcontrollers

|

| By Application |

|

Cloud Infrastructure

|

| By End User |

|

Enterprises

|

| By Security Function |

|

Authentication

|

| By Deployment Model |

|

Edge Devices

|

Regional Analysis: North America

The financial sector in the United States is a major consumer of secure digital hardware, with rising concerns about financial fraud and data breaches. Hardware security modules (HSMs) and secure element (SE) technologies are crucial for protecting sensitive financial transactions and customer data.

The healthcare industry’s stringent data privacy regulations, such as HIPAA, necessitate the use of secure digital hardware to safeguard patient information. Secure storage and processing of medical data are key drivers for adoption in this sector.

Government agencies in the United States are increasingly prioritizing secure digital hardware to protect national security interests and critical infrastructure. This includes applications in defense, intelligence, and law enforcement.

The integration of secure digital hardware in connected and autonomous vehicles is gaining traction. Protecting vehicle systems from cyberattacks is crucial for safety and security, driving demand for specialized hardware solutions in this rapidly evolving market.

Europe

Europe presents a significant and rapidly growing market for secure digital hardware. The region’s emphasis on data protection and privacy, underscored by regulations like GDPR, is a major catalyst for innovation and adoption. Businesses across various sectors are actively seeking hardware-based security solutions to comply with these stringent requirements and mitigate cyber risks. The strong presence of established technology players and a focus on research and development further contribute to the market’s dynamism. The demand for secure hardware in financial services, critical infrastructure, and government applications is particularly strong.

Asia-Pacific

The Asia-Pacific region is emerging as a key growth engine for . Rapid digitalization, increasing cyber threats, and government initiatives promoting cybersecurity are driving significant demand. Countries like China, Japan, and South Korea are leading the way in adopting advanced hardware security solutions. The growth of the Internet of Things (IoT) in the region is also creating new opportunities for secure hardware deployments. However, fragmented regulatory landscapes and varying levels of cybersecurity awareness pose challenges to market growth.

South America

South America is witnessing increasing adoption of secure digital hardware, driven by growing concerns about cybercrime and data breaches. The financial sector is a primary driver of demand, with banks and financial institutions investing in hardware security to protect customer data and prevent fraud. The expansion of e-commerce and digital payments is also fueling the need for secure hardware solutions. While the market is still relatively nascent compared to North America and Europe, it offers significant long-term growth potential.

Middle East & Africa

The Middle East and Africa represent a developing market for secure digital hardware. Increasing investments in digital transformation, coupled with rising cyber threats, are driving demand. The financial services and government sectors are key adopters, with a growing emphasis on protecting critical infrastructure and sensitive data. The region’s unique geopolitical landscape and evolving regulatory frameworks present both opportunities and challenges for market players.

Report Scope

This market research report provides a comprehensive analysis of the Secure Digital Hardware Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Secure Digital Hardware Market?

-> Secure Digital Hardware market size was valued at USD 9.8 billion in 2025 and is expected to reach USD 15.7 billion by 2034, exhibiting a CAGR of 5.1% during the forecast period.

Which key companies operate in Secure Digital Hardware Market?

-> Key players include Infineon Technologies, NXP Semiconductors, STMicroelectronics, and Microchip Technology, among others.

What are the key growth drivers?

-> Key growth drivers include intensifying cyber‑security concerns, rapid IoT device proliferation, stricter data‑privacy regulations, and increased adoption of secure hardware by cloud service providers.

Which region dominates the market?

-> The reference does not specify a dominant region.

What are the emerging trends?

-> Emerging trends include greater adoption of trusted platform modules (TPM), hardware security modules (HSM), embedded secure elements, and integration of secure silicon with AI‑driven edge computing and cloud workloads.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...